Why the 2026 Midterm Could Break a Rare Presidential Streak

1 hr ago

Brent crude fell more than 5% in a single overnight session on 20 May 2026, not because of a new oil discovery or a demand shock, but because two governments started talking through intermediaries in Pakistan and Oman. Since Operation Epic Fury commenced on approximately 28 February 2026, the partial closure of the Strait of Hormuz has embedded a structural risk premium across energy, bond, and equity markets simultaneously. That premium is now being repriced in real time as US-Iran negotiations enter what the Trump administration describes as an advanced phase. What follows traces the causal chain from the Hormuz disruption to oil prices, bond yields, central bank posture, and equity valuations, and explains what a resolution, or its failure, means for investors with exposure across those asset classes.

The disruption began with a specific act. US and Israeli airstrikes designated Operation Epic Fury commenced on approximately 28 February 2026, and Iran’s partial closure of the Strait of Hormuz followed as a direct response. The strait carries a significant share of global seaborne oil, and even a partial restriction created cascading supply uncertainty across every linked market.

According to the Congressional Research Service (March 2026), the Strait of Hormuz remains the single most consequential chokepoint for global crude oil supply, with no alternative route capable of absorbing its full volume at comparable cost or speed.

From late February through mid-May, disruption compounded in identifiable stages:

The result was a Brent crude trading range of approximately $105-$118 per barrel across the period, a premium that reflected not abstract uncertainty but the measurable reduction in physical supply reaching global markets. Understanding the size of that accumulated premium is the first step in evaluating what any diplomatic resolution is actually worth in price terms.

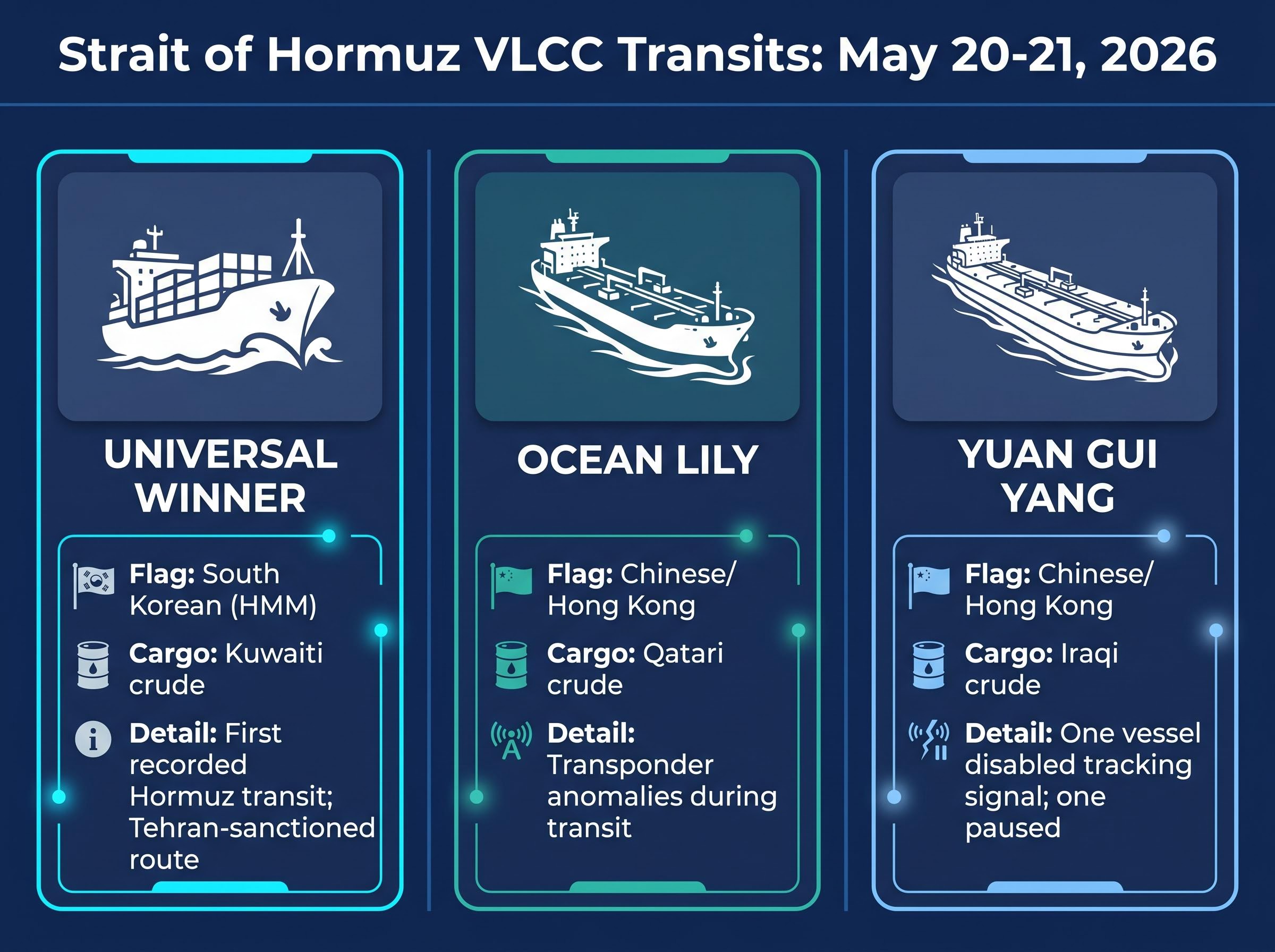

On 20-21 May 2026, three very large crude carriers (VLCCs) transited or exited the Strait of Hormuz within the same window. A simultaneous three-VLCC crossing would represent among the highest single-day supertanker volumes since the conflict began, making it a data point that moved markets independently of official diplomatic statements.

| Vessel | Flag | Cargo Origin | Notable Detail |

|---|---|---|---|

| Universal Winner | South Korean (HMM) | Kuwaiti crude | First recorded Hormuz transit; Tehran-sanctioned route |

| Ocean Lily | Chinese/Hong Kong | Qatari crude | Transponder anomalies during transit |

| Yuan Gui Yang | Chinese/Hong Kong | Iraqi crude | One vessel disabled tracking signal; one paused |

Overall tanker traffic remains substantially below pre-conflict levels. The composition of these specific transits, however, reveals more than the volume alone.

The Universal Winner’s passage was not a commercial gamble. According to Bloomberg reporting (20-21 May 2026), the transit was coordinated between the South Korean government and Tehran, with the vessel following a designated route sanctioned by Iranian authorities. This is a state-to-state arrangement, not a shipping company accepting elevated risk for profit. Its successful completion signals that the diplomatic channel is producing operational outcomes, not just communiqués.

The Ocean Lily and Yuan Gui Yang tell a different story. Both are Chinese/Hong Kong-flagged, and their transits involved transponder anomalies consistent with vessels operating under elevated but managed risk. China has reportedly arranged direct safe-passage terms with Iran, meaning Beijing’s willingness to send VLCCs reflects its own independent assessment of the threat level. That assessment, distinct from what Western governments are saying publicly, adds a second data source for investors tracking normalisation.

The Strait of Hormuz is narrow, shallow at its margins, and funnels crude from the Gulf’s largest exporters, including Kuwait, Qatar, Iraq, and the UAE, through a single navigable channel. According to the Congressional Research Service (March 2026), no alternative route exists that can absorb its full volume at comparable cost or speed. That physical reality is what converts a regional military conflict into a global pricing event.

EIA Strait of Hormuz data quantifies the waterway’s throughput as a share of global petroleum liquids consumption and confirms that no bypass route can absorb its full volume at comparable cost, providing the statistical foundation for why even a partial closure reprices the entire crude futures curve rather than a regional subset of it.

The strait’s share of global seaborne oil supply means that even a partial closure, rather than a full blockade, is sufficient to disrupt pricing across the entire crude futures curve.

Alternative routes exist, but each carries material penalties:

These constraints mean the strait cannot be simply routed around. Investors who grasp this structural irreplaceability will have a calibrated framework for evaluating any future disruption or resolution event, rather than treating each headline as equally significant.

The physical case for why the strait cannot simply be routed around rests on bypass infrastructure limits that are documented in the EIA’s May 2026 modelling: Saudi Arabia’s East-West Pipeline and the UAE’s ADCOP Pipeline together cannot replace the volume that transits Hormuz on a normal operating day, making alternative routing a partial relief measure rather than a structural substitute.

The Brent spike above $100 per barrel did not stay confined to energy markets. It fed directly into headline inflation expectations, narrowing the policy space available to central banks that had been edging toward rate reductions.

The April 2026 FOMC minutes, released on 20 May 2026, made this explicit. A majority of participants signalled openness to tightening if inflation remained persistent above 2%. Three officials formally dissented from retaining easing-oriented language. The Hormuz crisis was cited directly as a factor in the committee’s inflation outlook.

The April 2026 FOMC minutes document the committee’s explicit linkage between Middle East energy disruptions and the inflation outlook, recording that a majority of participants signalled openness to tightening and that three officials formally dissented from retaining easing-oriented language.

| Central Bank | Current Rate Stance | Key Inflation Data | Hormuz Reference | Rate Market Pricing |

|---|---|---|---|---|

| Federal Reserve | Open to tightening if inflation persists | Above 2% target | Explicitly cited in April minutes | ~14bp of cuts priced through year-end 2026 |

| Bank of England | Market pricing majority for 25bp hike | April CPI: 2.8% (below 3.0% consensus) | Economists warned relief temporary given ME energy disruptions | 25bp increase to 4.0% expected at July 2026 meeting |

US 30-year Treasury yields sat at a 19-year high ahead of the diplomatic developments, reflecting markets pricing in prolonged elevated inflation. Fed rate cut pricing compressed to approximately 14 basis points through year-end 2026, down from approximately 19 basis points the prior session.

Central bank rate expectations shifted across the Fed, ECB, and Bank of England simultaneously as Brent crossed $100 per barrel, a synchronised repricing that Morningstar’s three fixed income scenarios show can produce materially different bond portfolio outcomes depending entirely on whether the Hormuz disruption resolves in weeks, months, or longer.

Gavekal Research characterised the current environment as one of “persistent inflation,” contrasting it with prior equity market complacency toward bond market signals.

The UK data reinforced that this was not a US-only phenomenon. April 2026 CPI came in at 2.8%, below the 3.0% consensus, but economists cautioned that relief was temporary given ongoing Middle East energy disruptions. The Bank of England rate path has shifted accordingly. The Hormuz disruption, in other words, has already altered the central bank policy trajectory that underlies equity valuations in every major market.

The overnight session on 20-21 May 2026 produced a measurable partial unwind. Brent crude fell approximately 5.1% to $105 per barrel. The S&P 500 rose 1.1%, the Nasdaq gained 1.5%, and the Dow Jones reclaimed 50,000. US Treasury yields fell 7-10 basis points across the curve. ASX 200 futures were up 104 points (approximately 1.21%) ahead of the 21 May open.

These moves are real, but they are partial.

MSCI Asia Pacific data compiled by Gavekal (cited via Bloomberg) shows the index declined in 16 of 19 weeks when US 10-year yields rose 20 basis points or more, with an average loss of 1.6%. That yield sensitivity has not disappeared because of a single diplomatic session.

The distinction that matters for portfolio positioning is between a sentiment-driven relief rally and a durable repricing. A durable repricing requires three conditions that have not yet been met:

Until all three conditions are satisfied, the current rally remains fragile and subject to reversal on any deterioration in the negotiating process.

The FOMC minutes confirm that Fed officials would view rate reductions as likely appropriate if the geopolitical conflict resolved. They also confirm the opposite: a prolonged or escalating conflict would support tightening. This asymmetry means the policy response amplifies the market move in both directions.

| Scenario | Brent Crude | Treasury Yields | Fed Rate Cut Probability | Equity Multiples |

|---|---|---|---|---|

| Full Resolution | Decline toward pre-crisis levels | Fall as inflation expectations ease | Increases materially | Expansion supported by lower discount rate |

| Partial Ceasefire | Remains elevated ($100-$110 range) | Modest decline; volatility persists | Limited shift; data-dependent | Range-bound; sector rotation continues |

| Breakdown | Spikes above $118; potential for $130+ | Rise on inflation re-acceleration | Eliminated; tightening probable | Compression, particularly in rate-sensitive growth |

The tail risk in the breakdown scenario is specific. The Islamic Revolutionary Guard Corps (IRGC) has warned that any resumption of US military action could trigger retaliatory strikes beyond the Middle East, according to Bloomberg reporting. Gulf state leaders have reportedly told the Trump administration that a resolution was imminent, but this remains unverified.

The Hormuz oil risk premium embedded in current Brent prices is not simply a reflection of current physical disruption: the near-total withdrawal of commercial war-risk insurance means freight economics remain broken even when the strait is technically passable, and the IEA projects a two-year supply chain recovery timeline under a best-case resolution.

Conditions that would confirm which scenario is materialising:

Nvidia’s Q1 FY2027 data centre revenue of $75.2 billion (up 92% year-on-year) illustrates the stakes: elevated rates are compressing the multiples on the AI-driven growth names that underpin the current market cycle. A resolution that frees the Fed to cut would reprice those valuations directly.

The 20 May market moves represent a partial, sentiment-driven unwinding of a risk premium that took three months to accumulate. A durable repricing requires verified strait access, formal diplomatic text, and sustained oil price normalisation, none of which have been confirmed.

The transmission chain is now established: Hormuz disruption fed a Brent spike, which elevated inflation expectations, which shifted central bank posture toward tightening, which compressed equity multiples globally. Each link in that chain can reverse, but only if the underlying cause, the physical disruption, is resolved verifiably rather than rhetorically.

US-Iran negotiations remain the single geopolitical variable with the largest simultaneous impact on energy, bond, and equity markets through the remainder of 2026. The diplomatic channel is producing operational signals (tanker transits, proposal exchanges) that outpace official statements, but the gap between a ceasefire and a settlement is where the remaining risk premium lives.

US-Iran diplomatic negotiations have repeatedly reset the crude price curve in both directions since February 2026, with the May 11 session illustrating how a single rejected counteroffer can erase a week of price declines in one session and push Brent back toward $106.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These forward-looking statements are speculative and subject to change based on market developments and diplomatic outcomes.

The Hormuz risk premium is the additional cost built into crude oil prices due to the partial closure of the Strait of Hormuz, which carries a significant share of global seaborne oil. Since Operation Epic Fury commenced in late February 2026, this premium pushed Brent crude into a trading range of approximately $105-$118 per barrel.

Elevated oil prices from the Hormuz disruption fed directly into headline inflation expectations, causing the Federal Reserve to signal openness to tightening and compressing rate cut pricing to approximately 14 basis points through year-end 2026. A verified resolution could reverse this, freeing central banks to resume rate reductions.

A durable repricing requires a formal diplomatic agreement with verifiable terms, confirmed reopening of the Strait of Hormuz to normal commercial traffic supported by sustained MarineTraffic data, and Brent crude falling and holding below its crisis-era trading range for consecutive sessions.

State-coordinated VLCC transits, such as the South Korean government arranging the Universal Winner's passage with Tehran's approval in May 2026, indicate that diplomatic channels are producing operational outcomes rather than just statements. China's separate bilateral safe-passage arrangements for its own vessels provide an independent second data source on normalisation progress.

A breakdown scenario would likely push Brent crude above $118 per barrel with potential spikes toward $130, re-accelerate inflation, eliminate Fed rate cut probability, and compress equity multiples, particularly for rate-sensitive growth stocks. The FOMC minutes explicitly confirm that a prolonged or escalating conflict would support tightening rather than easing.