Most retail investors using AI to research ASX small cap stocks are not gaining an edge. They are confirming what they already believe, using a tool that cannot access the information that actually matters.

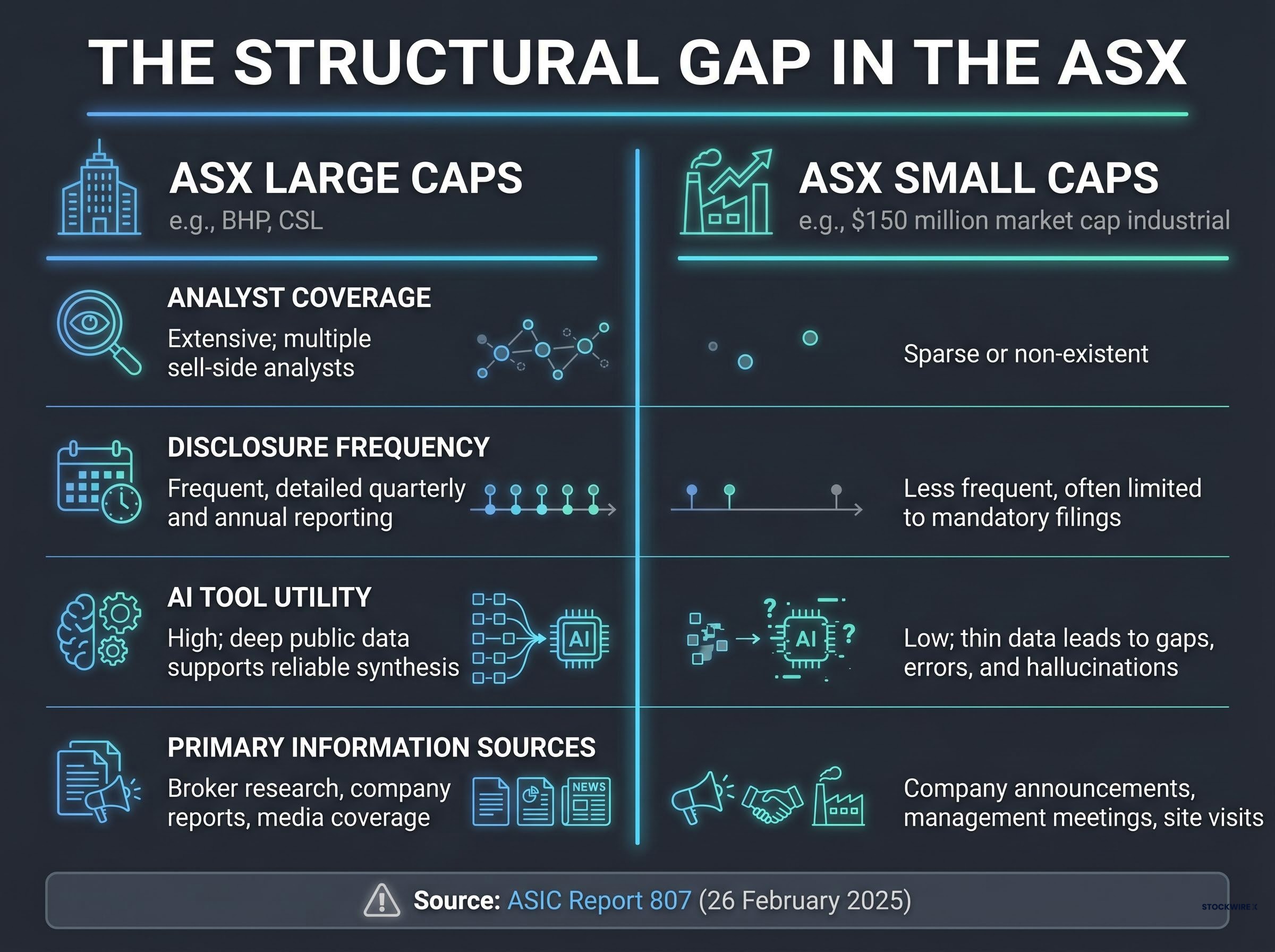

AI tools have reshaped how many Australians approach investment research, but their utility depends entirely on the quality and depth of available data. For ASX small cap stocks, that data is structurally thin. The same systems that can summarise a decade of BHP or CSL disclosures hit a wall when pointed at a $150 million market cap industrial where analyst coverage is sparse and public filings tell only part of the story.

What follows explains why AI cannot generate differentiated insights in ASX small caps, what ASIC says about the structural information gap between retail and professional investors, and what professional small cap fund managers actually do every day to build a genuine edge. Readers will finish with a clear understanding of where AI fits (and does not fit) in small cap research, and what separates an amateur process from a professional one.

AI investment research: capabilities, constraints, and the small cap ceiling

AI does some things well. It can synthesise publicly available information quickly, summarise company filings, and map consensus views across an industry in minutes. For large cap stocks with decades of disclosures, extensive analyst coverage, and deep historical datasets, these capabilities are genuinely useful.

The problem is structural. AI systems process large datasets through language models. They synthesise what already exists in the public domain. They cannot generate novel analysis, develop non-consensus views, or access information that has never been published.

In the ASX small cap universe, the public domain is thin. According to practitioner observations from Seneca Financial Solutions, AI tools cannot reliably provide accurate share prices or company names for roughly half of their investable universe. ASIC’s Moneysmart guidance (updated 2024) warns that AI tools rely on the data they are trained on, may be biased, may hallucinate, and cannot consider an individual’s circumstances. The ASX Investor Education Hub (updated 2025) categorises AI tools and screeners as supplements to, not substitutes for, fundamental research.

Three core limitations define AI’s ceiling in small cap research:

- Data thinness: Smaller companies generate fewer public disclosures, less analyst commentary, and less media coverage, leaving AI models with insufficient input to produce reliable output.

- Consensus-only synthesis: AI can tell an investor what the market already thinks. It cannot identify where the market is wrong.

- Hallucination risk: When data is sparse, AI models fill gaps with plausible but fabricated information, including incorrect company names and share prices.

AI stock trading systems adapt their behaviour from incoming data rather than following fixed rules, which makes their failure modes less transparent and harder for retail investors to anticipate than traditional algorithmic tools; when the underlying dataset is thin, as it is across most of the ASX small cap universe, that opacity compounds rather than reduces investment risk.

Why AI output reflects the market’s existing view, not its blind spots

Alpha in small caps comes from non-consensus views: identifying something the market has mispriced before the rest of the market recognises the error. AI, by construction, can only synthesise consensus. It aggregates what has been published, what has been said, and what has been widely circulated.

Seneca Financial Solutions draws this distinction explicitly. AI is useful for understanding what the market already thinks about a company or sector. It is not useful for finding where the market is wrong. If the tool cannot name the company correctly, it certainly cannot assess whether management is credible or whether a capital raising is worth participating in.

When big ASX news breaks, our subscribers know first

Why the ASX small cap market is structurally different from the rest of the exchange

The limitations described above are not an opinion about AI. They are a documented structural feature of the market itself.

ASIC Report 807, published 26 February 2025, found that smaller issuers receive less analyst coverage and produce less frequent or less detailed public disclosure than larger companies. Information about these companies is more dispersed, and institutional investors can access alternative information channels, including management meetings, bespoke research, and site visits, that are largely unavailable to retail investors.

ASIC REP 807 (26 February 2025): Institutional investors can better exploit alternative information channels, including management access and bespoke research, compared with retail investors, contributing to a structural information gap in small caps.

The ASX 2025 Annual Report confirms that a large proportion of listed companies sit in lower-capitalisation bands and receive less analyst coverage. ASX investor education material advises that investors in smaller companies should review company announcements thoroughly and consider management quality and strategy.

The table below illustrates the structural gap:

| Characteristic | ASX large caps | ASX small caps |

|---|---|---|

| Analyst coverage | Extensive; multiple sell-side analysts | Sparse or non-existent |

| Disclosure frequency | Frequent, detailed quarterly and annual reporting | Less frequent, often limited to mandatory filings |

| AI tool utility | High; deep public data supports reliable synthesis | Low; thin data leads to gaps, errors, and hallucinations |

| Primary information sources | Broker research, company reports, media coverage | Company announcements, management meetings, site visits |

This is why the challenge is not fixable with a better AI tool. The information that drives alpha in small caps does not exist in any publicly available dataset. No AI model, however advanced, can access it.

ASIC REP 822 on structural information gaps in small-cap markets identifies this disparity as a barrier to retail participation, and flags lighter disclosure frameworks for smaller issuers as part of its broader capital markets reform agenda, reinforcing why the information asymmetry documented in REP 807 is a persistent, system-level feature rather than a temporary oversight.

How behavioural bias interacts with AI to entrench investor errors

The structural gap is one problem. How retail investors use AI within that gap is another.

Confirmation bias, the tendency to seek out information that supports a pre-existing belief while ignoring evidence that contradicts it, is well documented in investment behaviour. AI tools tend to reinforce this pattern rather than disrupt it.

ASIC’s Moneysmart guidance (updated 2024) warns that AI outputs can amplify existing biases rather than correct them, and that investors may not understand how AI tools work, leading to misplaced confidence. Practitioner observations from Seneca Financial Solutions describe a common pattern: retail investors frequently seek confirmation of a stock thesis they have already formed, rather than genuinely differentiated analysis.

ASIC Report 807 adds a market-level dimension, noting that online platforms and social media can drive herding and momentum in smaller stocks with limited fundamental information, interacting with behavioural biases including confirmation bias. An investor who prompts an AI tool with a bullish thesis on a small cap stock will almost certainly receive a bullish-sounding response. The tool has no incentive or mechanism to push back.

Investor psychology research documents this pattern precisely: six interlocking biases including loss aversion, overconfidence, herd behaviour, recency bias, confirmation bias, and anchoring form a feedback loop that intensifies during market extremes, and online platforms that amplify momentum can trigger the same loop in smaller stocks where fundamental information is sparse.

In small caps, the stakes of being wrong are higher. Thinner liquidity means exits are harder. Less public information means errors take longer to surface. Misplaced confidence, amplified by an AI tool that confirms what the investor wanted to hear, can compound losses.

Three questions that challenge your thesis instead of confirming it

Recognising confirmation bias is the first step to countering it. Professional fund managers approach every thesis with structured scepticism. Three questions, drawn from how professionals approach disconfirmation, can serve as a practical starting point:

- What would have to be true for this thesis to be wrong? Identify the specific assumptions underpinning the investment case and ask what evidence would invalidate them.

- What does management have an incentive to obscure? Every management team presents its company in the best available light. Consider what is absent from the narrative, not just what is present.

- What does the market know that I do not? If the stock is cheap relative to its apparent quality, consider the possibility that better-informed participants have already assessed and passed on it.

The daily discipline behind professional small cap research

The daily routine of a professional small cap team looks nothing like an AI prompt submitted after market close.

At Seneca Financial Solutions, broker research notes begin arriving in inboxes as early as 3:00 a.m. These are reviewed before the market opens, providing context for the day’s trading and any overnight developments relevant to portfolio positions.

ASX announcements begin flowing from approximately 8:00 a.m., with the window between 8:00 a.m. and 10:00 a.m. representing the highest volume period. Every announcement published each day is manually reviewed by the team, without reliance on automated filtering tools.

Seneca Financial Solutions: Every ASX announcement published each day is manually reviewed, without reliance on automated filtering. This daily discipline builds the layered knowledge base that allows rapid, high-confidence decisions when opportunities arise.

This is not a one-off research sprint. It is a daily discipline, repeated every trading day, that compounds into a knowledge base no AI model can replicate.

The daily workflow follows a consistent sequence:

- Pre-market broker notes (from 3:00 a.m.): Review overnight research, sector updates, and earnings commentary relevant to the portfolio and watchlist.

- Announcement flow (from 8:00 a.m.): Begin reviewing every ASX announcement as it is published, identifying material developments across the investable universe.

- High-volume window management (8:00-10:00 a.m.): Process the largest concentration of daily announcements, cross-referencing against the existing knowledge base.

- Portfolio weight review: Assess position sizing and weighting decisions in light of new information, with discussions focused on how today’s developments change the forward view.

Ophir Asset Management, in its 2024-2025 investor letters, stresses that frequent management interaction and channel checks are at the core of the small cap edge, especially where public information is sparse. The contrast with an AI prompt submitted at 9:00 p.m. the night before is implicit but unmistakable.

How professionals build the knowledge base that makes fast decisions possible

The daily announcement review is the foundation. What sits on top of it is a knowledge base built through years of management meetings, competitive intelligence gathering, and structured scepticism.

Intelligence from management meetings at Seneca Financial Solutions is not simply recorded and filed. It is layered into a growing knowledge base that informs every future decision. Three types of intelligence are built from each interaction:

- Competitive context: What a company’s management reveals about competitors, market dynamics, and industry pricing provides cross-referencing material for future meetings with those same competitors.

- Personnel assessment: Backgrounds, track records, and credibility of management teams are catalogued and updated, building a longitudinal view of whether leadership delivers on stated plans.

- Strategic trajectory: Where management says the business is heading, and whether that direction has shifted since the last meeting, provides a real-time map of corporate strategy that no public filing captures with the same granularity.

Information gathered from one company’s management about a competitor is used to generate better questions for the next meeting, not accepted at face value. ASIC Report 807 confirms this approach at the institutional level, noting that active managers in small caps use meetings, site visits, and primary research to form differentiated views where public information is sparse.

This compounding knowledge base is what allows professional teams to make fast, high-confidence decisions when opportunities arise. They are not encountering a company for the first time. They have been building a view for months or years.

Selective participation in capital raisings: how prior knowledge drives the decision

Capital raisings in small caps often come with tight timelines. Companies need to raise funds quickly, and participants must decide within hours or days.

Speed without depth is a liability here, not an advantage. Seneca Financial Solutions routinely declines the vast majority of capital raising opportunities, typically because the companies involved have already been assessed multiple times and found wanting. Making a rapid investment decision on a capital raising without prior knowledge of the business is considered poor practice.

The discipline of saying no most of the time is itself a product of the knowledge base. The team already knows which companies it would back under which conditions. When a raising arrives, the decision draws on years of accumulated intelligence rather than a hurried review of the offer document.

AI as orientation tool: practical boundaries for professional and retail research

AI does have a role in professional small cap research. It is narrow, but it is genuine.

Seneca Financial Solutions uses AI tools in a limited capacity to accelerate understanding of specific business segments, such as identifying competitors in a software logistics market, as a starting point for deeper work. This is orientation, not analysis. The AI output frames the landscape; the primary research that follows determines whether any investment thesis has merit.

ASIC’s Moneysmart guidance (updated 2024) is direct: AI does not remove information disadvantages. It cannot replace professional research in less-researched parts of the market. The ASX Investor Education Hub (updated 2025) reinforces this, categorising AI tools as supplements to, not substitutes for, fundamental research.

For retail investors, the practical takeaway is calibration. AI can orient an investor within an unfamiliar industry. It cannot build the thesis that supports an actual investment decision. For anything that informs a buy or sell, push into primary sources: company announcements on the ASX platform, management presentations, and shareholder letters from fund managers who operate in the space.

Missing financial reports are among the most visible governance warning signs in ASX small caps, and ASIC’s 2026 enforcement campaign, which found 151 allegedly non-compliant companies from a survey of 217, confirms that the risk of investing in companies with incomplete disclosure records is concentrated precisely in the lower-capitalisation segment where AI tools are least reliable.

| Research task | AI-appropriate | Requires primary research |

|---|---|---|

| Industry orientation | Yes; mapping competitors, understanding market segments | No |

| Company-specific thesis building | No | Yes; requires announcements, filings, management assessment |

| Management quality assessment | No | Yes; requires direct engagement or detailed track record analysis |

| Capital raising evaluation | No | Yes; requires prior knowledge of the business and offer terms |

| Position sizing rationale | No | Yes; requires portfolio context and conviction-weighted assessment |

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Primary research is the irreplaceable foundation of small cap alpha

Alpha in ASX small caps derives from non-consensus views formed through primary research. No publicly trained AI model can access the information that generates those views.

The professional workflow is built on daily announcement review without automated filtering, a compounding knowledge base assembled from years of management engagement, and a capital raising discipline grounded in prior due diligence rather than rushed assessment. These are not secrets. They are habits that require sustained commitment.

The lesson for retail investors is not that small cap investing is inaccessible. It is that the tools and habits that matter are different from what most investors currently rely on. ASX company announcement pages, fund manager letters (such as Ophir Asset Management’s publicly available investor letters), and ASIC’s investor education resources are practical starting points for building a more grounded research approach.

AI can orient the search. It cannot do the work.

For investors ready to build a sourcing process from the ground up, our dedicated guide to finding undervalued stocks in low-coverage markets walks through the specific methods used by Warren Buffett, Peter Lynch, Seth Klarman, and Joel Greenblatt to identify mispricings where analyst attention is absent, including the screening tools and primary research steps that apply directly to the ASX small cap universe.