What UK Traders Lose When Their CFD Account Goes Offshore

45 mins ago

Investors typically make their worst decisions not during ordinary markets but at precisely the moments when the stakes are highest. The April 2025 tariff shock offered a live demonstration: the S&P 500 fell 10.5% in two days, triggering a wave of panic selling, before recovering to deliver a 16.39% full-year return in 2025. The gap between those who held through that whipsaw and those who locked in losses was not a gap in information or intelligence. It was a gap in psychology. Understanding investor psychology, the specific cognitive forces that activate at market extremes, is not a secondary concern for portfolio construction. It is the primary mechanism through which temporary volatility becomes permanent loss. The biases that cause overconfidence at market peaks and panic at market troughs are well documented, structurally embedded in human cognition, and remarkably consistent across decades of market history. What follows maps these forces in detail, explains why they are so difficult to resist through willpower alone, and provides the concrete disciplines that experienced Australian investors use to counteract them across the full market cycle.

The foundation for understanding how investors behave under stress begins with prospect theory, developed by Daniel Kahneman and Amos Tversky. Their research established a deceptively simple finding: losses feel approximately twice as painful as equivalent gains feel rewarding. A $10,000 portfolio loss generates roughly double the emotional intensity of a $10,000 gain.

Kahneman and Tversky’s loss aversion research, which forms the empirical foundation of prospect theory, established that the pain of losing is psychologically approximately twice as powerful as the pleasure of an equivalent gain, a finding that has been replicated across decades of experimental and market settings.

That single asymmetry predicts a wide range of self-defeating behaviour. It explains why investors sell winning positions too early (locking in the pleasure of a gain before it can reverse) and hold losing positions too long (refusing to crystallise the pain of a loss). It explains why a 10% drawdown triggers more portfolio activity than a 10% rally. And it explains why bear markets produce far more impulsive decision-making than bull markets, even though both represent temporary conditions.

Richard Thaler’s nudge theory extended this framework into institutional design, arguing that default settings in financial structures can counteract bias-driven inaction. In Australia, this insight is directly relevant to the superannuation system, where compulsory contributions and well-designed default investment options quietly counteract the inertia that would otherwise leave many investors underinvested or unallocated.

These biases are not personality flaws. They evolved for survival contexts where following the crowd and fleeing danger were adaptive responses. In financial markets, they misfire systematically.

Institutional market timing by large super funds carries the same recency bias risk as individual investor behaviour, with AustralianSuper’s outgoing CIO acknowledging in March 2026 that the fund missed significant gains by underweighting AI and digital stocks from approximately 2022, illustrating that professional mandates do not immunise portfolios from the same cognitive forces that affect retail investors.

The core biases operate not as isolated quirks but as an interlocking system, each reinforcing the others under market stress:

These biases form a feedback loop. Recency bias feeds overconfidence. Overconfidence feeds herding. Herding amplifies both bull and bear extremes. And loss aversion ensures that the emotional cost of being wrong is asymmetric, making rational correction harder at precisely the moments it matters most.

A bull market is conventionally defined as a sustained rise of 20% or more from a recent low. The 2023-2024 recovery, driven substantially by AI-sector enthusiasm and technology stock momentum, offers a recent example of the cognitive state that characterises late-stage optimism.

During rising markets, overconfidence becomes the dominant bias. Investors begin to attribute portfolio gains to their own skill rather than broad market conditions. Recency bias compounds this: months of positive returns create an expectation that the trajectory will continue indefinitely. Confirmation bias completes the loop, as investors increasingly consume bullish commentary and dismiss cautionary analysis.

Prospect theory asymmetry: Losses feel approximately twice as painful as equivalent gains. In a bull market, this manifests as premature profit-taking on individual positions, even as overall risk appetite expands; investors lock in small wins while simultaneously taking on concentrated, speculative exposure elsewhere.

The result is a paradox. Bull markets feel like the safe phase, but they are where the seeds of future losses are planted: overconfident positioning, inadequate diversification, and complacency about valuation all accumulate during the up-cycle.

Herd behaviour in a rising market operates differently from herd behaviour in a falling one. It is not fear-driven but FOMO-driven: watching peers profit, reading bullish media coverage, and feeling the pull to concentrate in whatever is already rising.

On the ASX, this dynamic is amplified by the market’s structural concentration in financials and materials. When one of these sectors runs, the gravitational pull toward rotation is stronger than it would be in a more diversified index. Investors who chase sector-level momentum during a bull phase often arrive at concentrated positions that magnify losses when the cycle turns.

The 2023-2024 AI-driven rally demonstrated this pattern clearly. Rising confidence in technology names caused many investors to systematically underweight downside risk, treating recent performance as a reliable indicator of future returns.

The shift from bull-market overconfidence to bear-market fear is not gradual. It is a qualitative break. The cognitive architecture is the same; the emotional register is entirely different.

Loss aversion activates through a specific sequence during a downturn. Paper losses accumulate. The urge to stop the bleeding overrides the long-term plan. Selling at the trough locks in permanent loss just before recovery. Recency bias makes each downturn feel like the beginning of a permanent decline, while confirmation bias amplifies only the most pessimistic signals, filtering out evidence that the market has historically recovered from every prior crash.

The historical evidence for the cost of this pattern is extensive.

| Event | Approximate decline | Recovery outcome | Key behavioural pattern |

|---|---|---|---|

| 2008 GFC | All Ords fell ~55% | Disciplined holders rewarded by subsequent multi-year recovery | Pronounced loss aversion; significant panic selling among retail investors |

| March 2020 COVID | Rapid broad-market sell-off | Investors who sold locked in losses and missed the rapid recovery | Loss aversion drove exit at the trough; recovery began within weeks |

| April 2025 tariff shock | S&P 500 fell 10.5% in two days | S&P 500 delivered +16.39% for full-year 2025 | Confidence collapse, but majority of Australian retail investors held positions |

ASIC data indicates that herd behaviour amplified the 1987 crash in Australian markets, reinforcing that this pattern is neither new nor limited to a single market regime.

Headline-driven trading patterns among Australian retail investors have become a structural feature of the market rather than an episodic response, with ASX Q1 2026 volumes running 32% above Q1 2025 levels and the conditions driving that elevated reactivity, ongoing macro uncertainty and an extended RBA inflation timeline, showing no sign of normalising.

The Westpac-Melbourne Institute Consumer Sentiment Index fell 12.5% to 80.1 following the April 2025 tariff announcements, capturing the emotional severity of the moment in a single data point.

Across every major downturn in recent history, the investors who exited at the worst moments locked in losses that systematic holders avoided. The recovery phase rewards those who could withstand the psychological pressure, not those who reacted to it.

The April 2025 tariff shock was a real-world stress test of investor psychology. The Westpac-Melbourne Institute confidence collapse (down 12.5% to 80.1) captured the emotional context. What investors actually did with their portfolios told a more nuanced story.

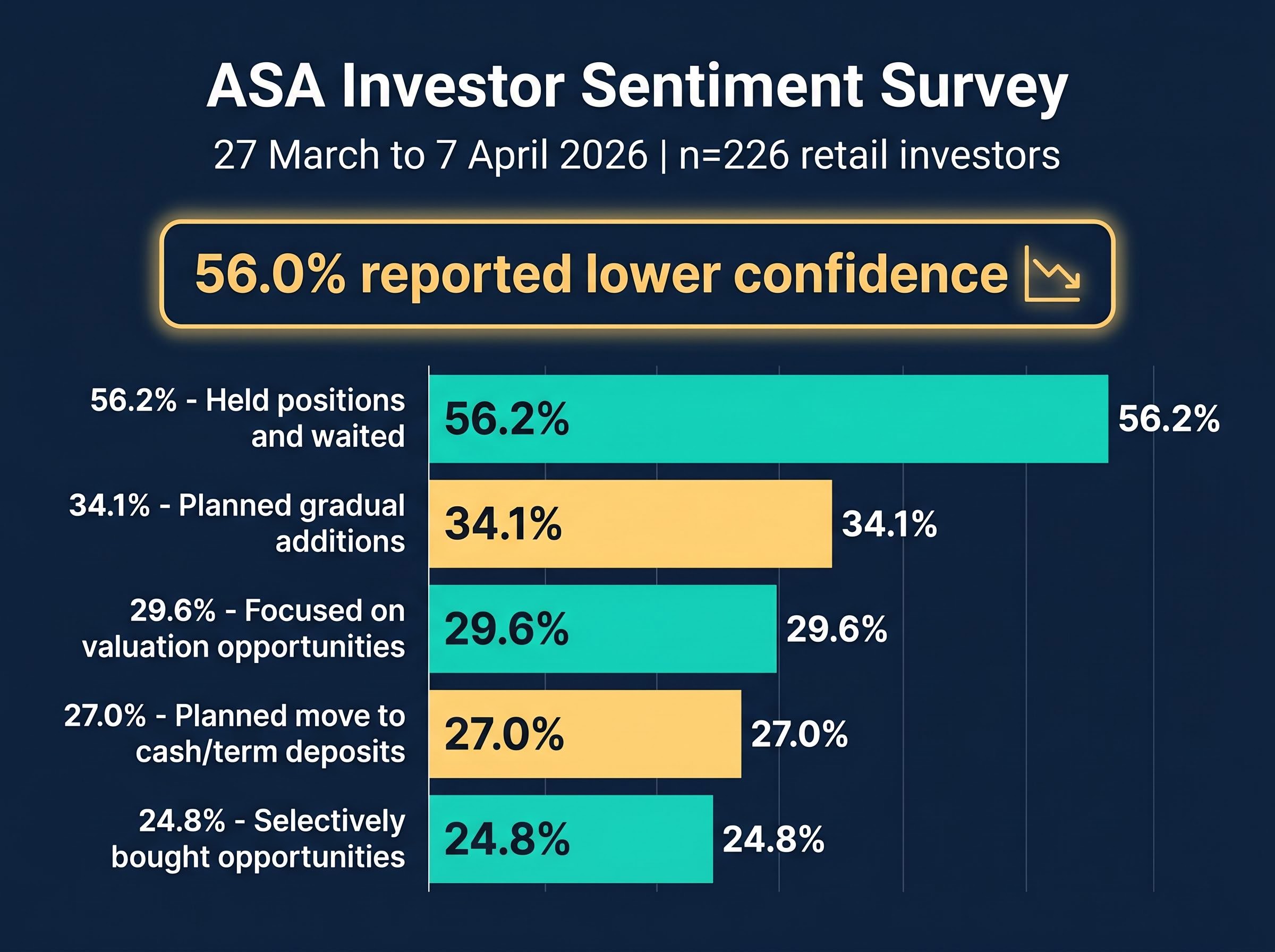

The emotional response was severe. According to the Australian Shareholders’ Association (ASA) Investor Sentiment Survey (conducted 27 March to 7 April 2026, n=226 retail investors), 56.0% of respondents reported lower confidence due to geopolitical tensions.

The behavioural response was more disciplined than the sentiment data alone would suggest. Key findings from the ASA survey:

The selective rotation toward gold and commodities visible in the ASA data is consistent with safe-haven psychology theory. Global gold ETF inflows reached $89 billion in 2025, reflecting the same loss-aversion-driven impulse at a worldwide scale: when loss feels proximate, capital flows toward assets perceived as stores of value independent of equity market dynamics.

The behaviour visible in the ASA survey data reflects a broader pattern of capital rotation rather than mass retreat, with offshore-focused funds replacing domestic standalone equities as the primary vehicle for international exposure among Australian retail investors who are repositioning rather than liquidating.

The 27% planning cash preservation is consistent with loss aversion. The majority holding or buying is consistent with disciplined process. Both bias-driven and disciplined responses coexisted in the data, but the dominant behaviour was restraint, not panic. For context, the RBA cut rates by 0.25% in May 2025 (to 3.85%) and again by 0.25% in August 2025 (to 3.60%), providing some monetary support during the period of elevated uncertainty.

This evidence matters because it shows that disciplined investor behaviour is achievable under genuine stress, not merely an aspiration discussed in theory.

Understanding the biases is the first step. Designing systems that counteract them before they activate is the step that determines outcomes. Each discipline below maps directly to a named bias:

The Australian superannuation system offers a structural example of Thaler’s nudge framework in practice. Well-designed default investment options in super funds counteract inertia and bias-driven inaction, effectively making disciplined investing the path of least resistance for millions of Australians who might otherwise remain unallocated or underinvested.

The S&P 500 delivered a 16.39% full-year return in 2025 despite falling 10.5% in two days during April. That return accrued to investors who stayed invested through the volatility, not to those who sold into it.

These are not disciplines reserved for professionals. They are structures any Australian investor can put in place before the next market extreme arrives, when the capacity for clear-headed decision-making will be at its lowest.

The same biases that cause overconfidence at market peaks cause panic at market troughs. The same loss aversion that drives premature selling in a downturn drives premature profit-taking in a rally. The market cycle is predictable in its psychological shape even when its timing is not, and the investors who outperform across full cycles are those who have designed systems to counteract these forces before they activate.

Historically, bull markets outlast bear markets. The long-term case for staying invested is supported by decades of data across Australian and global markets. But staying invested through the worst moments requires more than conviction. It requires process.

The same recency bias that drives panic selling at market troughs also creates the conditions for a contrarian buy signal: when consumer sentiment reaches record lows and the crowd extrapolates short-term pain into permanent decline, historical precedent suggests the probability-weighted outcome favours patience over exit.

The ASX’s heavy weighting toward financials and materials makes diversification discipline particularly relevant for Australian investors, whose default exposure is more concentrated than many global peers.

The practical question is specific. Does the current portfolio have predefined rebalancing triggers? Is investing happening systematically, regardless of market conditions? Are decisions being recorded in a way that allows patterns to be reviewed? If the answer to any of these is no, the next market extreme, whenever it arrives, will test willpower rather than process. The evidence across every major downturn suggests which of those two tends to win.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Investor psychology refers to the cognitive biases and emotional forces that influence financial decision-making, such as loss aversion, overconfidence, and herd behaviour. These biases are structurally embedded in human cognition and consistently cause investors to sell at market lows and buy at market peaks, turning temporary volatility into permanent loss.

Loss aversion is a cognitive bias, identified by Daniel Kahneman and Amos Tversky, whereby losses feel approximately twice as painful as equivalent gains feel rewarding. In practice, this causes investors to panic-sell during downturns, hold losing positions too long, and take premature profits on winning positions.

According to an Australian Shareholders' Association survey, 56.2% of retail investors held their positions rather than selling during the April 2025 market sell-off, and 24.8% selectively bought during the downturn. The S&P 500 ultimately delivered a 16.39% full-year return in 2025, rewarding those who stayed invested through the volatility.

Experienced investors use predefined rebalancing rules, dollar-cost averaging, deliberate sector diversification, and decision journaling to counteract biases before they activate. These systems remove high-stakes decisions from moments of peak emotional distortion, replacing willpower with structured process.

Recency bias causes investors to overweight recent negative events when forming expectations, leading them to extrapolate short-term market pain into a belief in permanent decline. This makes each downturn feel uniquely catastrophic and amplifies panic selling, even though historical data shows markets have recovered from every major crash.