Why Most Wealth-Building Strategies Aren’t Built for You

5 hrs ago

Every major online broker in Australia is either free or nearly free, yet every one of them is a profitable business. That contradiction deserves an explanation before anyone trusts a platform with their money. The Australian ETF market has grown to approximately A$331 billion in funds under management as of the end of 2025, and a new generation of zero-fee and near-fee brokerage platforms has emerged to compete for retail accounts. BetaShares Direct, Superhero, Stake, and others have pushed brokerage costs toward zero, while even traditional brokers have reduced per-trade fees substantially. But every platform’s product disclosure statement quietly confirms revenue channels that never appear in headline fee comparisons: retained interest on uninvested cash, management fees from proprietary fund relationships, and foreign exchange margins. This guide explains exactly how these platforms generate revenue, what that means for total investment costs, and how to use that knowledge to choose a platform that genuinely suits a specific investing style.

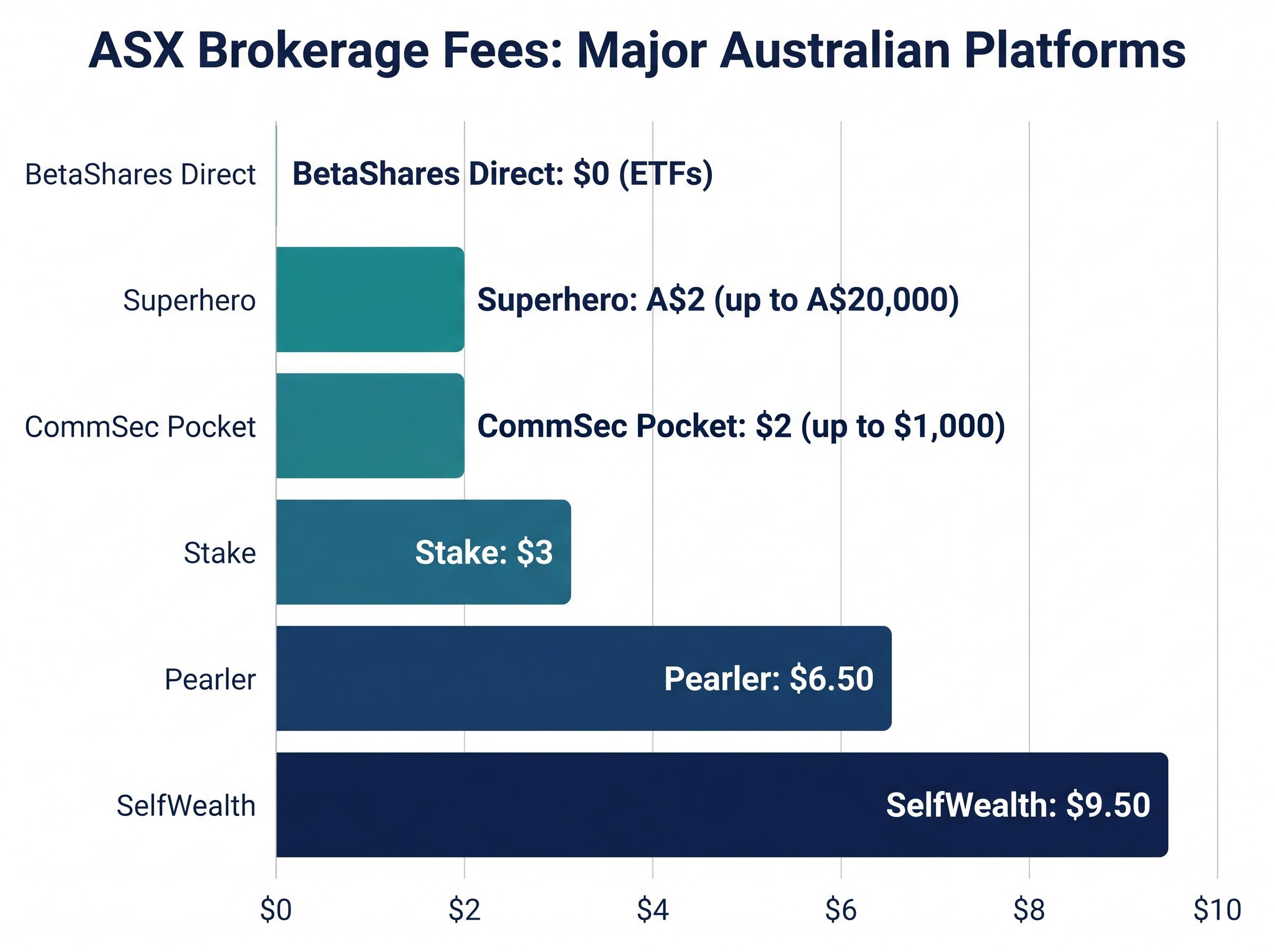

Two forces drove the fee collapse. Technology reduced the marginal cost of executing a trade to near zero, and competition ensured that saving got passed to clients, or at least appeared to. Superhero cut its ASX brokerage to A$2 flat per trade (up to A$20,000) and its US brokerage to US$2 flat in April 2024, a move that forced every competitor to justify its own pricing. Meanwhile, BetaShares Direct launched with zero brokerage on ETFs, and CommSec Pocket held its micro-investing fee at A$2 per trade up to A$1,000.

The Australian ETF market reached A$330.6 billion in funds under management at the end of 2025, with 411,000 first-time ETF investors entering in that year alone, a scale that explains why zero-fee and near-zero-fee brokerage platforms can sustain profitable businesses on indirect revenue channels that most investors never examine.

The range is still wide enough to matter. SelfWealth charges A$9.50 per ASX trade. Pearler charges A$6.50. But the direction is uniform: down.

Here is the current fee structure across six major platforms:

| Platform | ASX Brokerage Fee | US Brokerage Fee | Account Fee |

|---|---|---|---|

| BetaShares Direct | $0 (ETFs) | N/A | $0 |

| Superhero | A$2 (up to A$20,000) | US$2 (up to US$20,000) | $0 |

| Stake | $3 | $0 (FX margin applies) | $0 |

| SelfWealth | $9.50 | US$0 (FX margin applies) | $0 |

| Pearler | $6.50 | N/A | $0 |

| CommSec Pocket | $2 (up to $1,000; 0.2% above) | N/A | $0 |

The question these numbers raise is straightforward. If visible fees are approaching zero, where does the revenue come from? The answer sits in the documents most investors never read.

When an investor deposits money into a brokerage account, those funds typically sit in a trust account with a third-party bank before they are deployed into shares or ETFs. The bank pays interest on that cash. The platform may retain some or all of that interest rather than passing it to the client.

This practice is confirmed in the financial services guides (FSGs) of every major low-cost platform in Australia. Superhero’s FSG states the mechanism plainly:

“We may receive interest on the cash held in trust for you and may retain some or all of this interest.”

What no platform publishes is the numeric margin. Not one of the six major platforms covered in this guide discloses a specific retention percentage or spread in its marketing materials or fee comparison pages. The current client rate, where one exists, is typically visible only within the app after account creation.

Here is the disclosure status across platforms:

ASIC’s Moneysmart website, updated in 2024, warns that platforms appearing “free” may monetise via interest on cash and product rebates. The regulator’s language confirms the practice exists at an industry level. Yet the absence of published figures means investors cannot calculate this cost at the point of platform selection, which is precisely when the information would be most useful.

The second indirect revenue channel is structural, and it applies most directly where the brokerage platform and the ETF issuer share the same parent company.

The revenue flow works in three steps:

Matt Fish, Head of Product at BetaShares Direct, has confirmed that the platform’s revenue model relies on management fees from BetaShares-branded ETFs chosen by investors and on interest retained from uninvested cash. The platform does offer all ASX-listed ETFs, not exclusively its own products, alongside over 500 Australian shares. Investors are not restricted to proprietary funds.

The conflict is not hidden. It is structural. When a platform earns more revenue from investors choosing its parent’s ETFs, the commercial incentive to surface those products prominently in search results, default lists, and educational content is self-evident. That does not mean wrongdoing has occurred. It means the economics reward a particular pattern of behaviour.

ASIC’s regulatory framework for managing these conflicts relies on general obligations rather than bespoke zero-fee brokerage rules. Sections 912A of the Corporations Act and Regulatory Guide 175 require brokers promoting related-party products to manage and disclose conflicts of interest. Regulatory Guide 168 governs product disclosure statements.

ASIC’s Moneysmart site, updated in 2024, warns that “featured” or “curated” product lists on investment platforms may reflect commercial relationships rather than objective suitability. ASIC Report 714 on gamification and app design in trading platforms continues to be referenced in 2024-25 regulatory commentary as relevant to in-app product promotion and conflicted design.

No bespoke ASIC enforcement action has specifically targeted a zero-fee ETF broker for conflicts tied to proprietary ETF promotion. The regulatory framework places the disclosure burden on the platform and the due diligence burden on the investor.

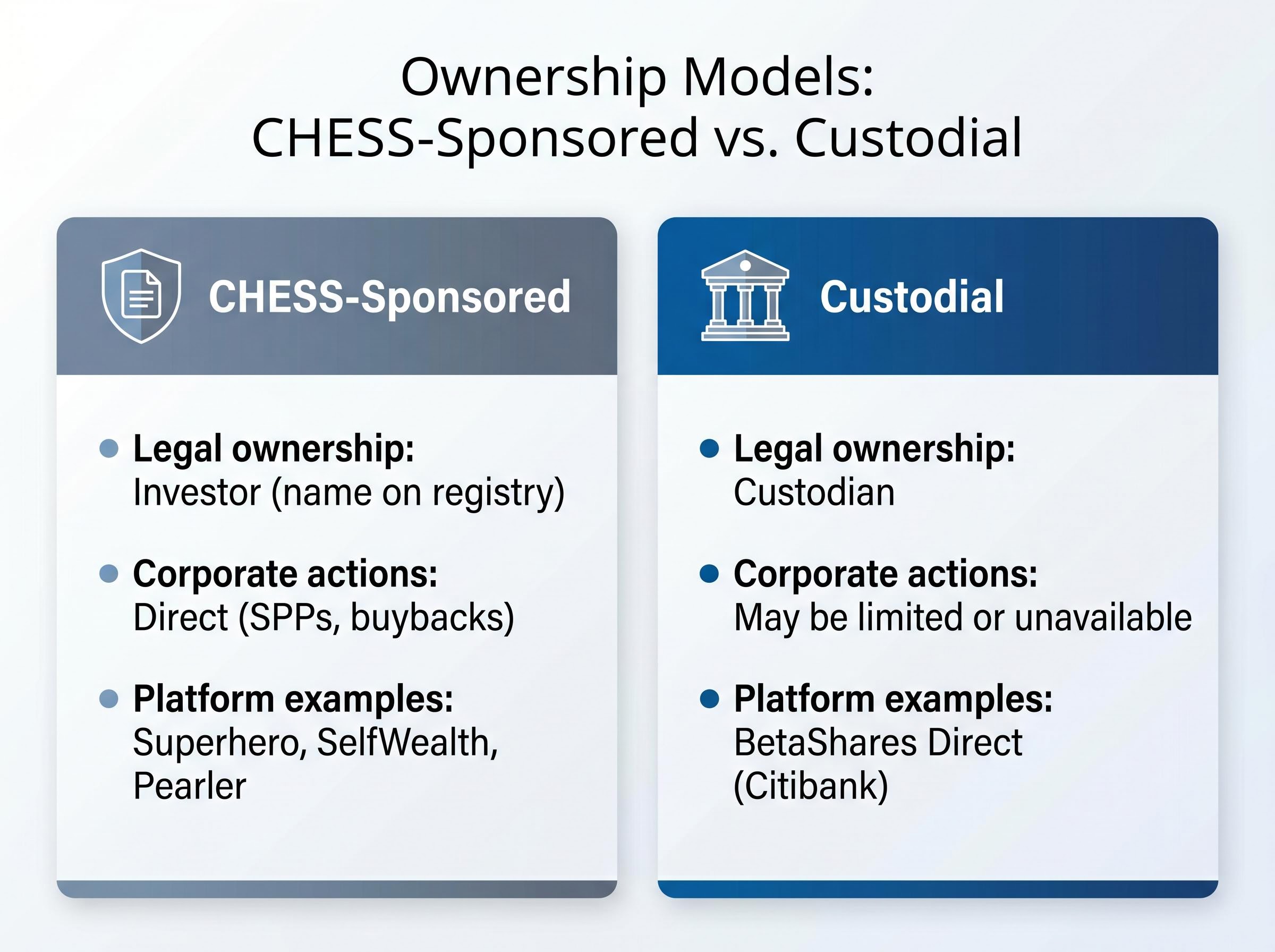

Platform selection involves a question most fee-comparison tables ignore entirely: what does the investor actually own, and how is that ownership recorded?

Under the CHESS-sponsored model, the ASX’s Clearing House Electronic Subregister System records the investor as both the legal and beneficial owner of the security. The investor’s name appears directly on the share registry (operated by Computershare or MUFG). This grants direct access to corporate actions such as share purchase plans and buybacks, and generates physical correspondence from the ASX. It also requires separate tax file number (TFN) supply to each registry.

The ASX CHESS sponsorship fact sheet confirms that securities held under CHESS sponsorship are recorded as the investor’s property on the ASX registry, providing a direct recovery path that does not depend on the platform’s continued operation in an insolvency scenario.

Under the custodial model, an independent institution holds the assets on the investor’s behalf. BetaShares Direct, for example, uses Citibank as its custodian. The investor retains beneficial ownership (the economic interest in the asset) but not legal ownership (the name on the registry). The custodian’s name appears on the register instead.

| Dimension | CHESS-Sponsored | Custodial |

|---|---|---|

| Legal ownership | Investor (name on registry) | Custodian (e.g. Citibank) |

| Beneficial ownership | Investor | Investor |

| Corporate action access | Direct (SPPs, buybacks) | May be limited or unavailable |

| Administrative overhead | Higher (registry, TFN, correspondence) | Lower (platform handles admin) |

| Platform examples | Superhero, SelfWealth, Pearler | BetaShares Direct (Citibank) |

Australia’s A$4.5 trillion superannuation sector operates predominantly under custodial structures. The model is not unusual or inherently inferior; it is the dominant form of institutional wealth-holding in the country.

Under both models, client assets are legally separated from the platform’s own assets. They are not available to creditors in the event of platform insolvency.

Under CHESS, the investor’s ownership is independently recorded by the ASX registry, providing a direct recovery path that does not depend on the platform’s continued operation. Under custodial arrangements, the investor’s claim runs through the custodian rather than the platform. The strength and stability of the custodian (in BetaShares Direct’s case, Citibank) becomes the relevant consideration.

Knowing where the hidden costs sit is useful. Turning that knowledge into a platform decision requires a structured evaluation. The following six criteria move beyond headline fees:

| Platform | ASX Brokerage | Cash Interest Disclosed | Custody Model | Tax Reporting |

|---|---|---|---|---|

| BetaShares Direct | $0 (ETFs) | In-app only | Custodial (Citibank) | myGov pre-fill |

| Superhero | A$2 | Not published | CHESS-sponsored | Tax reports available |

| Stake | $3 | Not published | Custodial | Tax reports available |

| SelfWealth | $9.50 | Not published | CHESS-sponsored | Tax reports available |

| Pearler | $6.50 | Not published | CHESS-sponsored | Tax reports available |

| CommSec Pocket | $2 (up to $1,000) | CBA standard rate | Custodial | Via CommSec |

Matt Fish of BetaShares Direct has noted that investors are generally able to transfer holdings between platforms, though fees may apply. The first choice is reversible. BetaShares Direct offers a $10 minimum ETF investment with fractional ownership, auto-invest functionality, and tax statement pre-fill to myGov. Pearler provides strong auto-invest and direct debit features. Both Finder and Canstar (2024-25) rate CHESS sponsorship as a differentiator for long-term investors in their independent comparison methodologies.

For most standard ETF investors, most major platforms provide sufficient functionality. Starting is more important than identifying a theoretically perfect platform.

The indirect cost channels covered in this guide, cash interest retention, management fee flows from proprietary products, and FX margins on international trades, do not appear in any fee schedule. But they compound.

ASIC’s Moneysmart website warns that platforms appearing “free” may monetise via spreads, FX margins, interest on cash, and product rebates.

ETF selection remains the single largest fee lever for most investors. A difference of 0.10% in MER on a $100,000 portfolio costs $100 per year before compounding. But platform-level costs layer on top of that, and over a 10-20 year horizon, even small ongoing drags accumulate meaningfully.

ETF management fee compounding is typically the largest single cost lever in a retail investor’s portfolio: a 0.9 percentage point difference in annual MER on a A$100,000 investment erases approximately A$98,917 over 20 years, with no market downturn required and no line-item charge ever appearing in an account statement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

No single platform is objectively best for every Australian investor. The right choice depends on how frequently someone invests, how large each contribution is, whether international exposure is needed, and how much administrative simplicity matters.

| Investor Type | Best-Suited Platform Characteristics | Key Trade-off |

|---|---|---|

| Frequent DCA (small amounts) | Zero or minimal brokerage, auto-invest, fractional ownership | May use custodial model; cash interest retention on regular deposits |

| Infrequent lump-sum investor | CHESS-sponsored, low per-trade fee acceptable given fewer trades | Higher brokerage per trade offset by fewer transactions per year |

| International ETF access | Low US brokerage, competitive FX margin, USD account option | FX margin may exceed brokerage savings; custodial structures common |

Four criteria should shape the final decision:

Matt Fish of BetaShares Direct has noted that choosing a platform and beginning to invest matters more than identifying the theoretically optimal platform before committing. Holdings can generally be transferred between platforms if circumstances change, though fees may apply.

For readers who have worked through the platform comparison and are ready to commit capital, our dedicated guide to starting investing in Australia covers what realistic first-year expectations look like, how compounding rewards patience over portfolio size, and why finishing year one with roughly the same capital is a genuine marker of success rather than a disappointment.

The Australian ETF market, at A$331 billion in funds under management and projected to reach A$380 billion in 2026, is large enough that the platforms serving it can sustain profitable businesses on revenue that never appears in a fee comparison table. Three channels generate that revenue: retained interest on uninvested cash, management fees flowing to platform parent companies through proprietary ETFs, and foreign exchange margins on international trades.

The BetaShares 2025 ETF industry review recorded total Australian ETF funds under management at A$330.6 billion by year-end, with net inflows accelerating across both equity and fixed income categories, confirming the scale of retail capital now flowing through the low-cost brokerage platforms this guide evaluates.

ASIC’s regulatory framework requires disclosure of these channels, but the details sit in FSGs and product disclosure statements, not in the marketing materials or comparison tools that most investors use to choose a platform. Superhero’s April 2024 fee cut to A$2 per trade signals that headline brokerage competition will continue to intensify, which makes understanding indirect revenue channels more important over time, not less.

The evaluation checklist in this guide, covering brokerage, cash interest transparency, proprietary product exposure, custody model, FX margins, and tax reporting, provides a framework for assessing total platform cost. Apply it, account for the cost channels that fee tables omit, confirm whether the custody model suits your ownership preferences, and start investing. The real price of “free” is knowable. It simply requires reading the documents that platforms would prefer investors to skip.

Total cost of ETF ownership extends beyond the headline MER and includes tracking difference, bid-ask spreads, and brokerage commissions, all of which compound silently in ways that parallel the cash interest retention and FX margin channels this article documents at the platform level.

CHESS sponsorship means the ASX's Clearing House Electronic Subregister System records you as the direct legal and beneficial owner of your shares, with your name appearing on the share registry. This matters because your holdings are independently recorded and recoverable without depending on your broker's continued operation, unlike custodial models where a third party holds assets on your behalf.

Zero-fee and near-zero-fee Australian brokers generate revenue through three main channels: retaining interest earned on uninvested client cash held in trust accounts, receiving management fees from proprietary ETFs promoted on their platforms, and applying foreign exchange margins on international trades. None of these costs appear in standard fee comparison tables.

Superhero, SelfWealth, and Pearler use CHESS-sponsored models, meaning investors hold direct legal ownership of their securities. BetaShares Direct uses a custodial model with Citibank as custodian, while Stake and CommSec Pocket also operate custodial structures.

BetaShares Direct charges zero brokerage on ETF trades and zero account fees, making it the lowest visible-cost option for ASX ETF investors. However, the platform retains interest on uninvested cash and earns management fees from BetaShares-branded ETFs, costs that do not appear in its headline fee schedule.

A complete platform comparison should cover six criteria: the per-trade brokerage fee, whether cash interest rates are publicly disclosed, whether the platform promotes proprietary ETFs from a related issuer, the custody model (CHESS versus custodial), the foreign exchange margin on international trades, and the availability of automated tax reporting. Evaluating all six gives a more accurate picture of total investment cost than brokerage fees alone.