Marcus Ericsson won the Indianapolis 500 in 2022. He finished second in 2023 and again in 2025. On the 7 May 2026 episode of the Trackside Extra podcast, he admitted something that had nothing to do with racing and everything to do with how the human brain processes setbacks: the near-misses occupy his mind more than the victory. The second places replay on a loop. The win sits quietly in the background. That asymmetry, the tendency for losses and near-losses to carry more psychological weight than equivalent gains, has a name. It is called loss aversion, and it was first documented by Daniel Kahneman and Amos Tversky in 1979. It is the same force that causes investors to sell at market lows, sit in cash while prices recover, and lock in the very losses they were trying to avoid. What follows is a progressive explanation of what loss aversion is, what it costs investors in measurable terms, and how to apply the same deliberate-learning process Ericsson uses to break its grip on financial decisions.

What Kahneman and Tversky proved in 1979 (and why it still governs your portfolio)

Consider a simple proposition. Someone offers a coin flip: heads, the outcome is a $100 gain; tails, a $100 loss. Most people reject the bet, even though the expected value is zero. The reason is not mathematical. It is emotional.

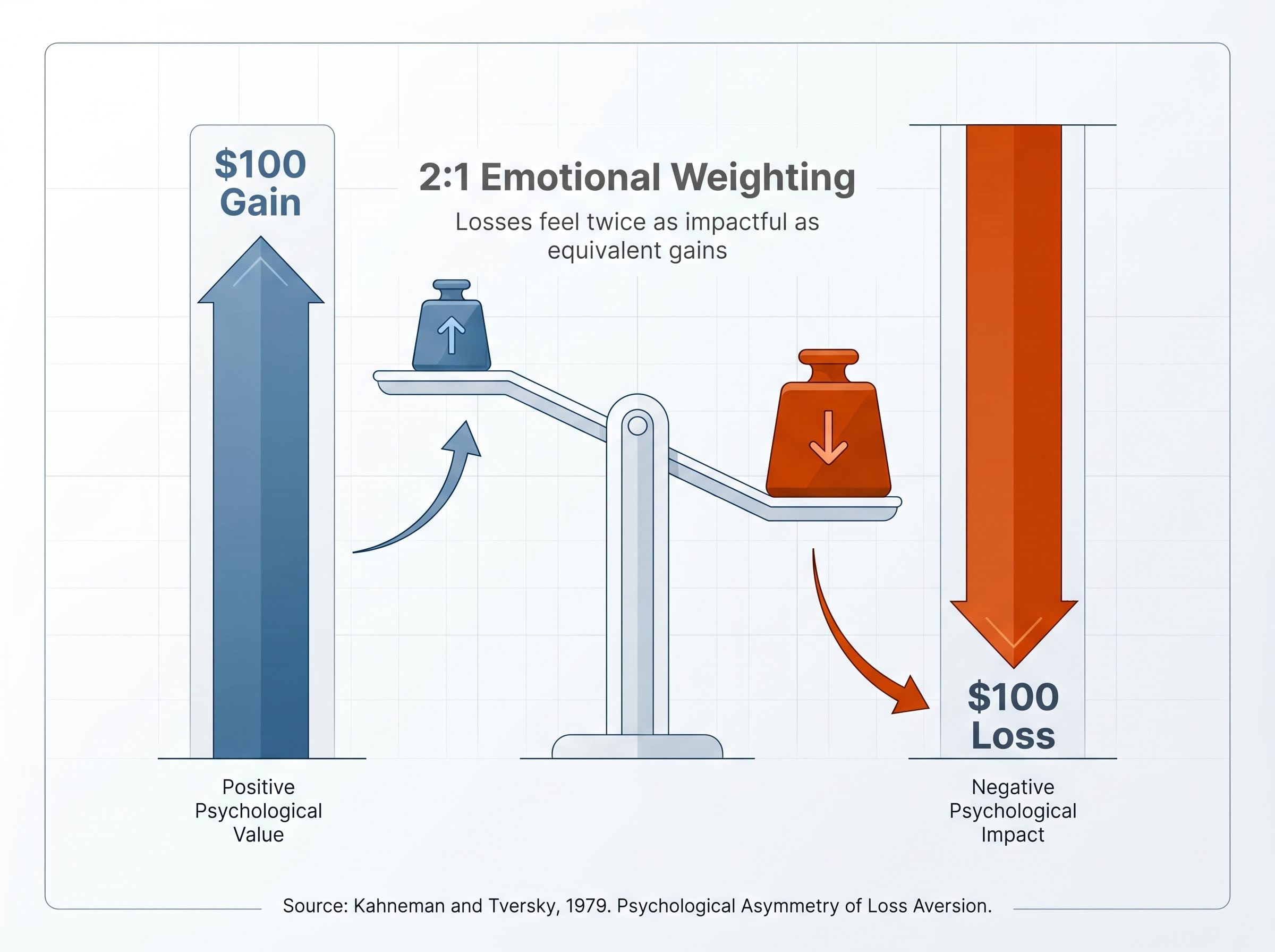

In 1979, psychologists Daniel Kahneman and Amos Tversky published “Prospect Theory: An Analysis of Decision under Risk” in Econometrica, the paper that would become a cornerstone of behavioural economics. Their core finding was precise: the pain of losing a given amount feels roughly twice as intense as the pleasure of gaining the same amount. A $100 loss does not simply cancel out a $100 gain. It stings approximately 2:1.

The pain of losing $100 feels roughly twice as intense as the pleasure of gaining $100, according to Kahneman and Tversky’s Prospect Theory.

This is not the same as risk aversion, which describes a general preference for certainty. Loss aversion is specifically about the asymmetric emotional weight assigned to losses versus gains, even when the probabilities and amounts are identical. Kahneman later made this framework accessible to general readers in Thinking, Fast and Slow (2011), where he described the asymmetry as a fundamental feature of human cognition rather than a personal weakness.

| Dimension | Gain of $100 | Loss of $100 |

|---|---|---|

| Emotional weight | Moderate pleasure (baseline 1x) | Intense pain (approximately 2x) |

| Typical behavioural response | Satisfaction fades quickly | Rumination, urgency to act |

| Long-term portfolio impact | Gains held or taken early | Panic selling near market lows |

Understanding the mechanism, not merely the label, is the first step toward recognising it in real-time financial decisions. The asymmetry is built into cognition. It operates automatically unless a deliberate system overrides it.

Loss aversion does not operate in isolation; cognitive biases in investor psychology form an interlocking system in which overconfidence, herd behaviour, recency bias, and anchoring each amplify the others, creating feedback loops that intensify at precisely the moments when clear thinking matters most.

When big ASX news breaks, our subscribers know first

The moment that explains everything: why near-misses haunt us more than losses

Before the financial data arrives, consider how loss aversion feels from the inside through the lens of someone who has lived it publicly.

Marcus Ericsson’s Indianapolis 500 record reads like a sequence designed to test the limits of the 2:1 ratio:

- 2022: Won the Indianapolis 500

- 2023: Finished second

- 2025: Finished second, then retroactively disqualified following a post-race technical violation

The disqualification did not just erase a runner-up finish. It triggered a measurable performance spiral. Ericsson finished the remainder of the 2025 season ranked 20th out of 27 full-time drivers.

“I think about the second places more than the win”

On the 7 May 2026 episode of Trackside Extra, hosted by Kevin Lee on Fox Sports, Ericsson described the mental preoccupation directly. The near-wins replay in his mind more than the victory. He attributed this not to self-pity but to a natural human response: the brain replays scenarios, questions past decisions, and fixates on outcomes that fell just short.

That self-awareness, the act of naming the pattern rather than being silently governed by it, is precisely the cognitive shift that separates a performance spiral from a recovery. It is also the shift that separates an investor who panic-sells from one who pauses long enough to examine the impulse.

What loss aversion actually costs investors (the evidence base)

The psychological asymmetry Kahneman and Tversky documented translates directly into a measurable return drag that shows up in fund flow data year after year.

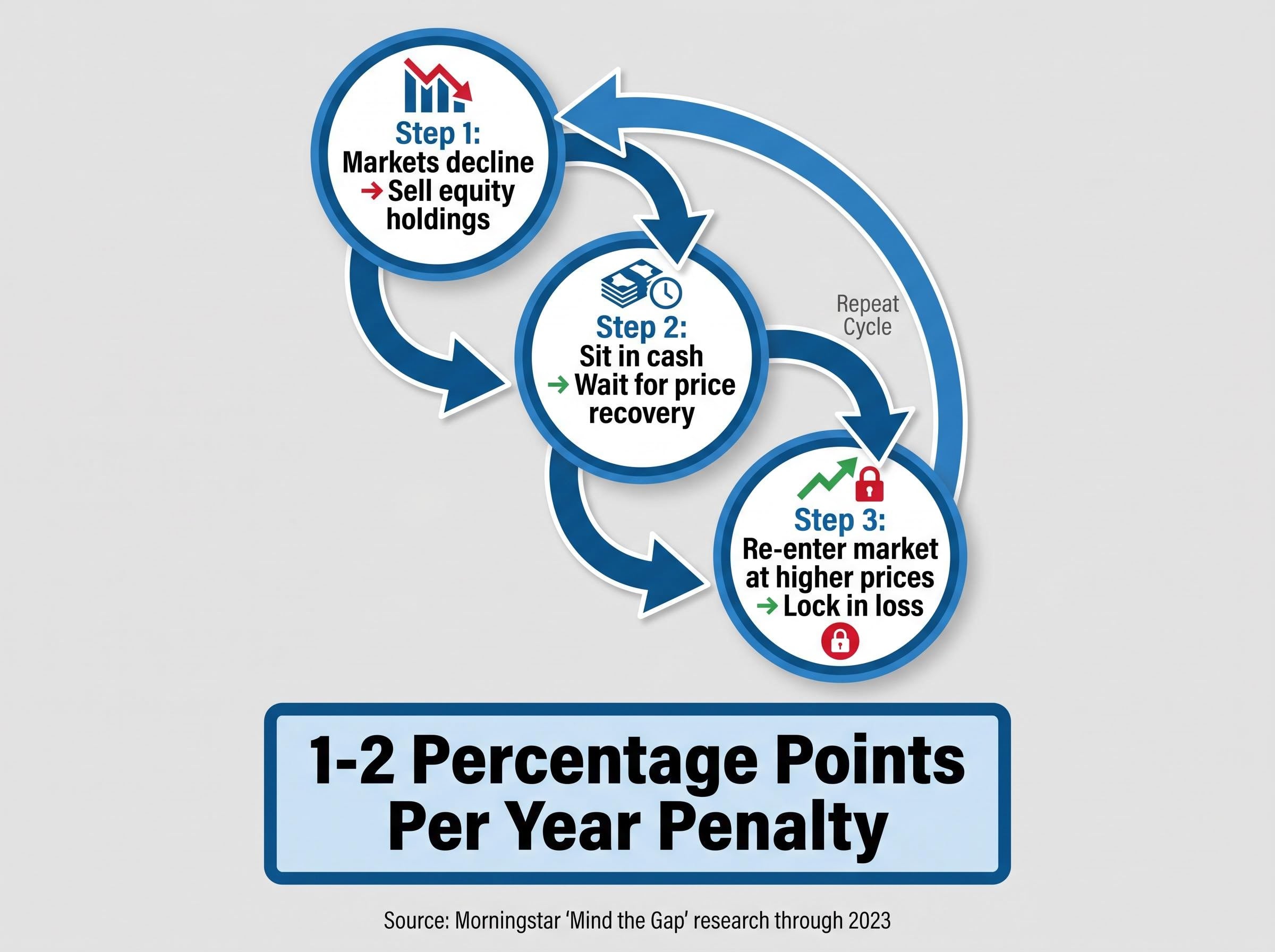

The pattern follows a predictable three-step sequence:

- Markets decline, and the emotional pain of watching portfolio values fall triggers an urgent desire to act. Investors sell equity holdings to “stop the bleeding.”

- Cash feels safe. The investor waits for confirmation that the recovery is real, which means waiting until prices have already risen significantly.

- The investor re-enters the market at higher prices, having locked in the loss and missed the early recovery.

This sequence, selling near lows and buying near highs, means the average dollar invested earns worse-than-average returns even when the funds themselves perform well.

Morningstar’s Mind the Gap research tracks the dollar-weighted returns earned by actual fund investors against the time-weighted returns reported by those same funds, consistently finding a behavioural shortfall of roughly 1-2 percentage points per year attributable to poorly timed buying and selling decisions.

Morningstar’s “Mind the Gap” research series, published through at least 2023, has systematically documented this phenomenon. The series consistently finds a gap of roughly 1-2 percentage points per year between what funds return (time-weighted) and what the average investor in those funds actually earns (dollar-weighted). The difference is attributable primarily to behavioural timing errors driven by loss aversion.

JP Morgan Asset Management’s annual “Guide to Retirement” publication has historically included a “Behaviour of the Average Investor” analysis illustrating the same pattern. ICI (Investment Company Institute) fund flow data for 2022 and 2023 confirms the directional reality: large retail equity outflows during the 2022 inflation and rate shock, followed by inflows in 2023 after markets had already recovered.

The compounding cost of getting the timing wrong

A 1-2 percentage point annual shortfall may sound modest in any single year. Compounded over a 20-30 year investment horizon, the cumulative cost is severe.

Morningstar’s data shows this behaviour gap persists across market environments, not only during sharp downturns. It appears in rising markets, flat markets, and volatile markets alike, because the emotional asymmetry is always operating. According to Gallup’s ongoing polling, roughly 61-62% of U.S. adults hold stocks directly or through funds, making this bias relevant at population scale.

The cost is not theoretical. It is the measurable distance between what a portfolio could have returned and what the investor’s own decisions allowed it to return.

Reactive trading costs accumulate through four compounding mechanisms: transaction fees, tax drag from forfeiting long-term capital gains treatment, timing errors from missing early recovery sessions, and opportunity cost from uninvested cash sitting idle while prices recover.

How Ericsson broke the spiral (and what investors can copy)

After the 2025 season collapse, Ericsson did not simply resolve to try harder. He built a structured recovery process, one that maps directly to the kind of deliberate review investors can apply after a poor financial decision.

On the 7 May 2026 podcast, Ericsson described the specific steps: working with a mental performance coach, reviewing race footage, analysing competitor strategies, identifying the precise decision point that cost him the result, and developing a corrective plan specific enough that he expressed confidence he would execute differently in a comparable future situation.

Ericsson stated on the 7 May 2026 Trackside Extra podcast that the structured review gave him confidence he would make different decisions if placed in the same circumstances again.

The process produced measurable results. His 2026 Indy 500 qualifying position came in at 17th out of 33 drivers, outperforming his Andretti Global teammates, evidence that the structured approach restored competitive function.

The investor parallel is direct. The same four-step structure applies to any portfolio decision that went wrong:

- Acknowledge the error. Identify the specific trade, exit, or inaction that produced the loss.

- Identify the reasoning flaw. Was the decision driven by an emotional trigger (fear, panic, frustration) or by an analytical error (incorrect thesis, missed data)?

- Classify the mistake. Distinguish between an emotionally driven error and an analytical one. The remedies are different.

- Develop a targeted corrective rule. Write a specific “if X occurs, I will do Y” statement that pre-commits to a different response.

This approach draws on the same psychological principle that Peter Gollwitzer’s foundational research on implementation intentions documents: pre-specifying a response substantially increases the likelihood of following through under stress.

The distinction that matters is between dwelling, which is unstructured emotional replay that deepens the spiral, and reviewing, which is structured analysis that produces a forward rule.

The next major ASX story will hit our subscribers first

Three tools that interrupt loss aversion before it strikes

Knowing that loss aversion exists is useful. Having a system in place before the next market decline is what actually changes outcomes. The following three tools address the bias at the architectural level of decision-making, not at the level of willpower.

Write your rules before the market moves

An Investment Policy Statement (IPS) is a written document prepared during calm market conditions that specifies what the investor will and will not do during downturns. It functions as a pre-commitment device.

Pre-committed investing strategies, including rules-based rebalancing, dollar-cost averaging schedules, and written allocation targets, have documented performance advantages over discretionary approaches precisely because they operate at the system level rather than at the level of in-the-moment judgment.

- Include target asset allocation, specific rebalancing triggers, and a review schedule

- Explicitly list prohibited panic actions (e.g., “I will not sell equities solely because the portfolio has declined more than 10% from its peak”)

- The IPS works because it was written by the investor’s rational self and binds the investor’s emotional self

The IPS concept is embedded in professional financial planning standards, including CFP frameworks, as a recognised behavioural safeguard.

If-then rules that remove the in-the-moment decision

Implementation intentions, grounded in Gollwitzer’s research, take the form of concrete “if-then” rules written in advance.

- Example rule: “If my portfolio falls 15% from its peak, I will do nothing for 30 days and then reassess against my original investment thesis”

- The pre-specified rule removes the need for in-the-moment judgment, which is precisely when loss aversion is strongest

- Gollwitzer’s research demonstrates that pre-specified if-then plans substantially increase follow-through under stress compared to general intentions

Check less, earn more

Investors who check their portfolios daily experience many more “loss” observations than those who check quarterly or annually, even when long-term returns are identical. Day-to-day volatility creates frequent negative readings that amplify the emotional experience of losses, a phenomenon known as myopic loss aversion.

- Schedule portfolio reviews at quarterly or semi-annual intervals aligned with the actual investment time horizon

- Remove real-time portfolio apps from primary device screens during volatile periods

- Kahneman’s dual-process framework (System 1 and System 2 thinking) explains why: frequent checking activates the fast, emotional system; infrequent, scheduled review engages the slower, analytical system

| Tool | What it does | How to implement it this week |

|---|---|---|

| Investment Policy Statement | Pre-commits to rules written during calm conditions | Draft a one-page document listing target allocation and three prohibited panic actions |

| If-then rules | Removes in-the-moment discretion during market stress | Write one specific rule: “If [trigger], then I will [pre-planned response]” |

| Check frequency reduction | Reduces the number of perceived “loss” events | Move portfolio apps off the home screen and set a calendar reminder for a quarterly review |

The race is long, and the replay is optional

Marcus Ericsson lines up 17th on the grid for the 2026 Indianapolis 500, which takes place on Sunday 19 May 2026. He is a driver who has processed his losses deliberately, improved his qualifying position relative to teammates, and returned to compete rather than withdraw. The spiral that followed the 2025 disqualification did not define the rest of his career. The structured review did.

The parallel for investors is not about willpower or emotional toughness. It is about system design.

Contrarian signals at sentiment extremes illustrate exactly what a loss-aversion override looks like in practice: when record-low consumer confidence coincides with equity markets near all-time highs, the investor who has pre-committed to holding through emotional pressure finds themselves positioned precisely where historical precedent suggests returns are strongest.

Loss aversion is not a character flaw to be overcome by resolve. It is a predictable feature of human psychology that can be managed by designing decision-making systems that account for it in advance.

Kahneman and Tversky documented the asymmetry nearly five decades ago. It has not changed. The brain still weights losses roughly twice as heavily as equivalent gains. What has changed is the availability of tools, IPS documents, if-then rules, and scheduled review cadences, that interrupt the bias before it reaches the sell button.

The single most actionable step is also the simplest. Write down one if-then rule for the portfolio this week, before the next market move creates the conditions where it will be needed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.