Global semiconductor sales are forecast to grow approximately 16% in 2025, AI-related chip revenue is expected to reach US$200 billion by 2027, and SEMI, an ASX-listed ETF tracking the chip supply chain, has returned +138.60% over the past year. For Australian retail investors, the question is no longer whether AI and semiconductors matter. It is how to access the opportunity from the ASX.

Artificial intelligence has moved well past the hype cycle. McKinsey data from 2024 shows 72% of surveyed organisations have adopted at least one AI use case, and IDC projects global AI systems spending will reach over US$500 billion by 2027. Every dollar of that spending eventually flows through silicon: chips, memory, fabrication equipment, and the broader supply chain. Two ASX-listed ETFs from Global X, GXAI and SEMI, offer structurally distinct but complementary pathways into this demand story.

This analysis examines the investment thesis behind each fund, explains how they fit together in a portfolio context, assesses the risks Australian investors should weigh, and compares them against alternatives in the ASX thematic ETF universe.

Why AI has become a chip demand story, not just a software story

Most investors encounter artificial intelligence through its consumer-facing layer: chatbots, image generators, automated customer service. That framing obscures where the money actually moves. Every AI model, whether it runs inference for a healthcare imaging tool or trains on financial transaction data, requires silicon to function. More models, larger parameter counts, and broader enterprise deployment all translate into higher demand for GPUs, high-bandwidth memory, and advanced logic chips.

The adoption data confirms this is no longer a Big Tech phenomenon. According to McKinsey’s 2024 survey, 72% of organisations have adopted at least one AI use case. Deloitte’s 2024 enterprise survey found 79% of respondents deploying at least three AI applications. The use cases span sectors:

- Healthcare: diagnostic imaging, triage support, and operational optimisation across more than 40% of large providers in advanced economies

- Finance: credit scoring, fraud detection, and risk management at over two-thirds of major banks

- Manufacturing: predictive maintenance and quality control automation

- Retail: demand forecasting, personalisation engines, and supply chain optimisation

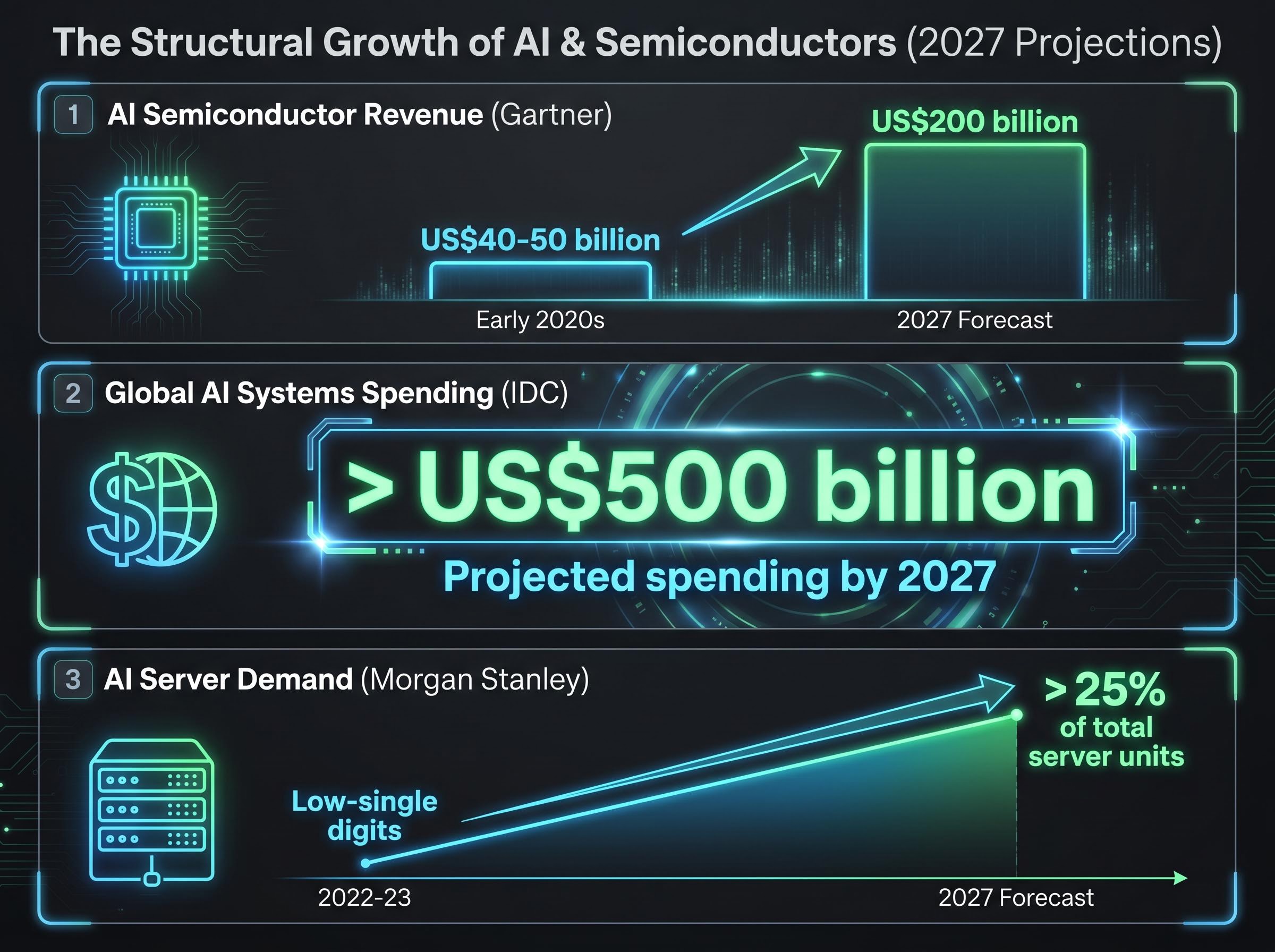

IDC projects global AI systems spending to grow at a 26.9% compound annual growth rate from 2023 to 2027, reaching over US$500 billion by 2027.

Gartner forecasts AI semiconductor revenue at approximately US$200 billion by 2027, up from roughly US$40-50 billion in the early 2020s. Analysts at Morgan Stanley and Goldman Sachs consistently frame this as a structural demand shift rather than a cyclical bump. The implication for investors is direct: the AI investment thesis and the semiconductor investment thesis are, at their core, the same thesis expressed at different layers of the value chain.

The scale of this capital commitment is without historical precedent: the AI investment boom has pushed US IT hardware and software spending to 4.9% of GDP in Q1 2026, surpassing both the dot-com era peak and the cloud buildout cycle, with combined hyperscaler capital expenditure commitments for 2026 sitting in the $600-$805 billion range.

When big ASX news breaks, our subscribers know first

Deconstructing SEMI: what the semiconductor ETF holds and how it works

SEMI does not simply buy chip designers. The fund captures multiple layers of the semiconductor supply chain, spanning:

- Design: companies that architect the chips powering AI workloads

- Fabrication: foundries such as TSMC that manufacture at advanced nodes

- Equipment: toolmakers including ASML that build the lithography systems foundries depend on

- Memory: producers of high-bandwidth memory tied to AI accelerator demand

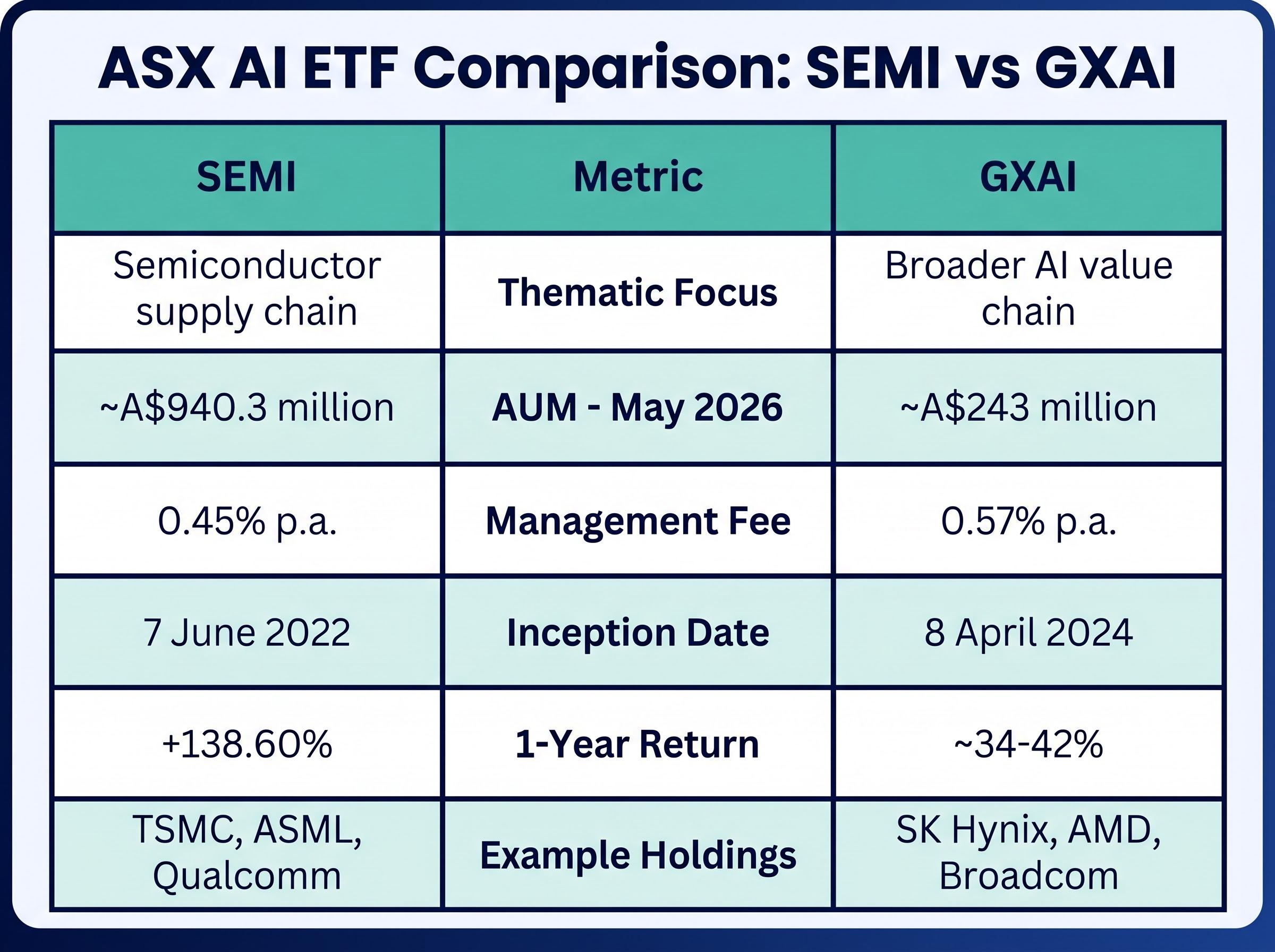

Holdings such as TSMC, ASML, and Qualcomm illustrate the fund’s breadth. A single trade in SEMI provides exposure to the full production chain that converts AI demand into silicon output.

The fund’s trajectory over the past 14 months reflects that proposition. Assets under management have grown from approximately A$214.7 million in March 2025 to approximately A$940.3 million as at May 2026, more than quadrupling. That AUM growth signals sustained and accelerating investor conviction rather than a speculative spike.

| Metric | Value |

|---|---|

| AUM (May 2026) | ~A$940.3 million |

| Management fee | 0.45% p.a. |

| Inception date | 7 June 2022 |

| 1-month return | +31.46% |

| 3-month return | +44.78% |

| 1-year return | +138.60% |

| 3-year return (p.a.) | +63.11% |

| Since inception (p.a.) | +36.03% |

All performance figures are after fees, NAV-based, as at 13 May 2026. Past performance does not guarantee future results.

The semiconductor cycle has historically been volatile, tied to consumer electronics replacement patterns and inventory corrections. What analysts describe as structurally different about the current cycle is the AI-driven demand floor. TSMC has committed over US$100 billion in capital expenditure across 2024-2027 for advanced node expansion, while SK Hynix has reported HBM3E capacity largely sold out through 2025 with sustained price strength. These are multi-year commitments, not quarter-to-quarter bets.

TSMC’s competitive moat runs considerably deeper than its headline market share figures suggest: Bank of America’s May 2026 analysis found TSMC targeting approximately 180,000 wafers per month at 3nm by end-2026, roughly eight times the estimated capacity at Samsung and Intel combined, with CoWoS advanced packaging yields above 98% against Intel’s competing pilot yields of 80-85%.

The GXAI fund: capturing the broader AI value chain

Where SEMI concentrates on the chip supply chain, GXAI casts a wider net across the AI value chain. The fund spans both hardware and software components of the AI ecosystem, holding companies involved in chip design, cloud infrastructure, enterprise AI software, and AI-enabled services.

Named holdings include SK Hynix (memory tied to AI accelerators), AMD (AI GPU and accelerator competition with Nvidia), and Broadcom (networking and custom silicon for hyperscale data centres). Each represents a different revenue stream within the AI economy.

| Metric | Value |

|---|---|

| AUM (May 2026) | ~A$243 million |

| Management fee | 0.57% p.a. |

| Inception date | 8 April 2024 |

| 1-year return | ~34-42% |

| YTD return | ~11-14% |

| Since inception (p.a.) | ~27-28% |

All performance figures are after fees, NAV-based, as at approximately 13-15 May 2026. Past performance does not guarantee future results.

GXAI’s shorter track record (launched April 2024) limits the historical comparison with SEMI, but the fund’s construction addresses a different investor need. Morgan Stanley projects AI server demand will account for more than 25% of total server units by 2027, up from low-single digits in 2022-23. GXAI’s breadth positions it to capture revenue growth across the software platforms and services that monetise AI at scale, layers that SEMI does not directly reach.

Goldman Sachs forecasts global AI infrastructure capital expenditure (GPUs, accelerators, networking) to grow at a 34% compound annual growth rate from 2024 to 2028.

For investors who view AI as an economic phenomenon rather than purely a manufacturing story, GXAI’s value-chain breadth is a feature of its design, not a dilution of conviction.

How GXAI and SEMI fit together in an Australian investor’s portfolio

The question most Australian retail investors face is not which fund is better. It is whether to hold one, both, or neither, and how each interacts with existing portfolio holdings. SEMI provides semiconductor-specific conviction. GXAI provides broader AI thematic coverage. Holding both avoids the false choice between chip-layer and application-layer exposure.

Australian financial platforms frame these funds as thematic satellite allocations. Both CommSec and nabtrade reference SEMI and GXAI as examples of ASX-listed options for thematic positioning within a broader portfolio. Morningstar categorises both as high-risk, growth-oriented sector and thematic ETFs, reinforcing that these sit alongside a core allocation rather than replacing one.

A practical framework for positioning:

- Assess existing technology exposure in core holdings. Broad global equity ETFs already contain Nvidia, Microsoft, and Alphabet. The question is whether that passive weighting provides sufficient AI and semiconductor exposure for the investor’s conviction level.

- Determine whether chip-specific or broad AI exposure better fills the gap. SEMI suits investors with higher conviction in the physical infrastructure layer. GXAI suits those who want to capture software and services monetisation alongside hardware.

- Size the satellite allocation relative to risk tolerance. Morningstar’s high-risk categorisation and the concentration inherent in thematic funds mean position sizing matters more than fund selection.

The new entrant: Global X AINF and what it adds

Global X has launched a third fund in the family, the Artificial Intelligence Infrastructure ETF (AINF), now listed on the ASX. AINF targets AI infrastructure specifically, distinct from both GXAI’s broader value-chain approach and SEMI’s semiconductor supply-chain focus. Fee and AUM data for AINF are not yet fully disclosed, limiting direct comparison.

The three funds together allow investors to build layered AI exposure: infrastructure (AINF), semiconductor supply chain (SEMI), and broad AI value chain (GXAI). This optionality within a single fund family is a relatively new development for the ASX thematic landscape.

The next major ASX story will hit our subscribers first

The risks that experienced investors in this space are watching

The structural demand case is strong. That does not make SEMI and GXAI risk-free. Four categories of risk warrant attention:

- Geopolitical and export controls: US export controls on advanced AI chips and equipment were tightened in October 2023, with additional licensing scrutiny on Nvidia’s China-specific AI chips in late 2024 and early 2025. Nvidia has warned of potential China-related revenue impact. China’s restrictions on critical mineral exports (gallium, germanium) add a supply-side variable.

- Taiwan concentration: TSMC fabricates the majority of the world’s advanced logic chips from Taiwan. Any disruption to Taiwanese production would ripple directly through SEMI’s holdings. Supply-chain diversification to the US, Japan, and the EU is underway but remains a medium-term process.

- Semiconductor cyclicality: The AI demand floor may be structural, but over-investment risk persists. If hyperscaler capital expenditure overshoots near-term AI workload growth, the traditional semiconductor cycle of build, oversupply, and correction could reassert itself.

- Currency exposure for Australian investors: Both funds hold USD-denominated offshore assets. Australian dollar strength against the US dollar compresses returns in AUD terms regardless of underlying fund performance.

AI stock valuation risk has become harder to read at the index level precisely because large opposing moves by individual winners and losers cancel each other out, creating a surface-level calm in benchmark volatility metrics that conceals the single-stock dispersion underneath, a pattern Goldman Sachs identified in its May 2026 assessment as analogous to the late-1990s technology spending cycle.

The geopolitical dimension creates an asymmetric risk profile that investors should model explicitly: Bloomberg Intelligence estimated a 70% probability of partial de-escalation from the May 2026 US-China summit, yet that most-likely outcome projected only 8-12% upside for semiconductor benchmarks, while the 25% probability hardening scenario projected 10-20% downside for SOXX and SMH, a skew that favours defensive sizing rather than maximum conviction.

The BIS export control rules on advanced computing chips, first introduced as an interim final rule in October 2023 and subsequently clarified through 2024, restrict the transfer of advanced semiconductors and related manufacturing equipment to China, creating direct revenue and supply-chain uncertainty for SEMI constituents with significant China exposure.

Morningstar categorises both SEMI and GXAI as high-risk, growth-oriented sector/thematic ETFs. Headline return figures should be assessed alongside this risk profile.

Counterbalancing these risks, US CHIPS Act grants and loans have been disbursed through 2024-25 to TSMC, Intel, and Micron, supporting domestic advanced fabrication. EU and Japanese subsidy programmes run in parallel. These initiatives benefit SEMI constituents directly and partially offset the geographic concentration risk.

Financial projections are subject to market conditions and various risk factors. Investors should weigh these considerations alongside the growth thesis when determining allocation size.

The structural case is intact, and the ASX now offers genuine ways to express it

The evidence across industry forecasters points in a consistent direction. The Semiconductor Industry Association’s Spring 2025 forecast projects global chip sales growth of approximately 16% in 2025, with data-centre and AI chips as the primary drivers. Global X’s own research, citing IDC and Gartner data, frames AI-related semiconductor revenue as growing at 20%+ compound annual growth rates through 2028. Cross-sector adoption, from healthcare to manufacturing to financial services, underpins demand that is broad-based rather than concentrated in a handful of hyperscalers.

Three years ago, Australian investors had limited ASX-listed options to express this thesis. That has changed. SEMI’s AUM growth from A$215 million to A$940 million in roughly 14 months reflects not just performance but sustained capital allocation into the theme. Both funds carry competitive fee structures (SEMI at 0.45%, GXAI at 0.57%) relative to active fund alternatives.

SEMI’s assets under management grew from approximately A$215 million in March 2025 to approximately A$940 million by May 2026, more than quadrupling in 14 months.

The analytical question is no longer whether AI and semiconductors represent a durable investment theme. It is how much of a portfolio should be allocated, whether the risk profile matches the investor’s objectives, and which layer of the value chain deserves the capital. SEMI and GXAI provide distinct, liquid, and fee-competitive answers to that question. The decision sits with the investor.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.