An index falls 10%, then rises 10%. It finishes roughly where it started, down just 1%. A 3x leveraged fund tracking those same two moves does not finish down 3%. It finishes down 9%. The arithmetic is not a rounding error or a fee; it is a structural feature baked into every leveraged exchange-traded fund on the market. Products carrying this structure now sit at the centre of one of the largest and fastest-growing segments of the U.S. ETF market, with ProShares UltraPro QQQ (TQQQ) alone holding assets near $20 billion. FINRA’s 2024 Annual Regulatory Oversight Report flagged retail investors’ persistent misunderstanding of these products as a supervisory priority. What follows will not advise whether to trade leveraged ETFs. It will supply the mechanical understanding, covering daily reset, volatility drag, and path dependency, that turns the arithmetic paradox above from a curiosity into a fully legible structural feature of every leveraged product on a U.S. exchange.

What a leveraged ETF is actually built to do

The promise is narrow and precise. A leveraged ETF is designed to deliver a set multiple of an index’s performance over a single trading day, not over a week, a quarter, or a year. TQQQ targets 3x the daily return of the Nasdaq-100. TECL targets 3x the daily return of the technology sector index. Both reset that target every night.

This is structurally different from a standard index ETF, which gives an investor exposure to the index’s cumulative return over whatever holding period they choose. A leveraged ETF makes no promise about cumulative returns. It promises one day at a time.

A standard index ETF delivers cumulative exposure to its benchmark over whatever holding period the investor chooses, with passive vehicles like VOO and IVV charging as little as 0.03% annually and using in-kind creation and redemption to give investors meaningful control over when taxable events occur.

Three design features separate a leveraged ETF from its standard counterpart:

- Daily performance target: The fund aims to deliver a fixed multiple (2x or 3x) of the underlying index’s return for that day only.

- Daily reset mechanism: At the close of each trading session, the fund rebalances its positions to restore the target leverage ratio from a new starting value.

- Derivative-based leverage: The fund achieves its magnified exposure through swaps, futures, and other derivative contracts rather than by borrowing cash to buy more shares.

Inverse ETFs apply the same architecture in reverse, targeting -1x, -2x, or -3x the daily return. The mechanics described throughout this article apply equally to both directions.

FINRA Regulatory Notice 22-08 establishes the compliance framework under which broker-dealers must evaluate retail customers before granting access to leveraged and inverse exchange-traded products, requiring firms to assess whether customers understand the daily reset, compounding risk, and the divergence between daily and multi-day performance.

FINRA Regulatory Notice 22-08, the standing U.S. regulatory framework for complex products, classifies leveraged and inverse ETFs as complex and requires firms to confirm that retail customers understand the daily reset and compounding risks before granting access.

When big ASX news breaks, our subscribers know first

How the daily reset works and why it resets everything

Each evening, after markets close, a leveraged ETF’s fund manager rebalances the portfolio’s derivative positions. The objective is to restore the target leverage ratio, whether 2x or 3x, from the fund’s new net asset value. The fund does not carry a fixed dollar amount of notional exposure from one day to the next. It recalculates.

This reset exists for a practical reason. Without it, a 3x fund that suffered a large loss on Monday would enter Tuesday with less capital but the same notional exposure, effectively running at a leverage ratio higher than 3x. A fund that gained sharply would enter the next day at a ratio below 3x. The reset is what keeps the stated multiple accurate each morning.

The 2x and 3x products discussed here occupy one end of the reset period spectrum; modestly leveraged funds from issuers like Global X Canada and NEOS carry 25-50% additional exposure as a permanent structural feature with no daily reset mechanism, producing a fundamentally different compounding profile than the products that prompted FINRA’s supervisory flagging.

Understanding the reset as a mechanical process rather than a marketing footnote is what allows investors to reason about when it helps and when it hurts. The consequences are symmetric: the same mechanism that produces decay in choppy markets produces outsized gains in trending ones.

When the reset amplifies rather than erodes

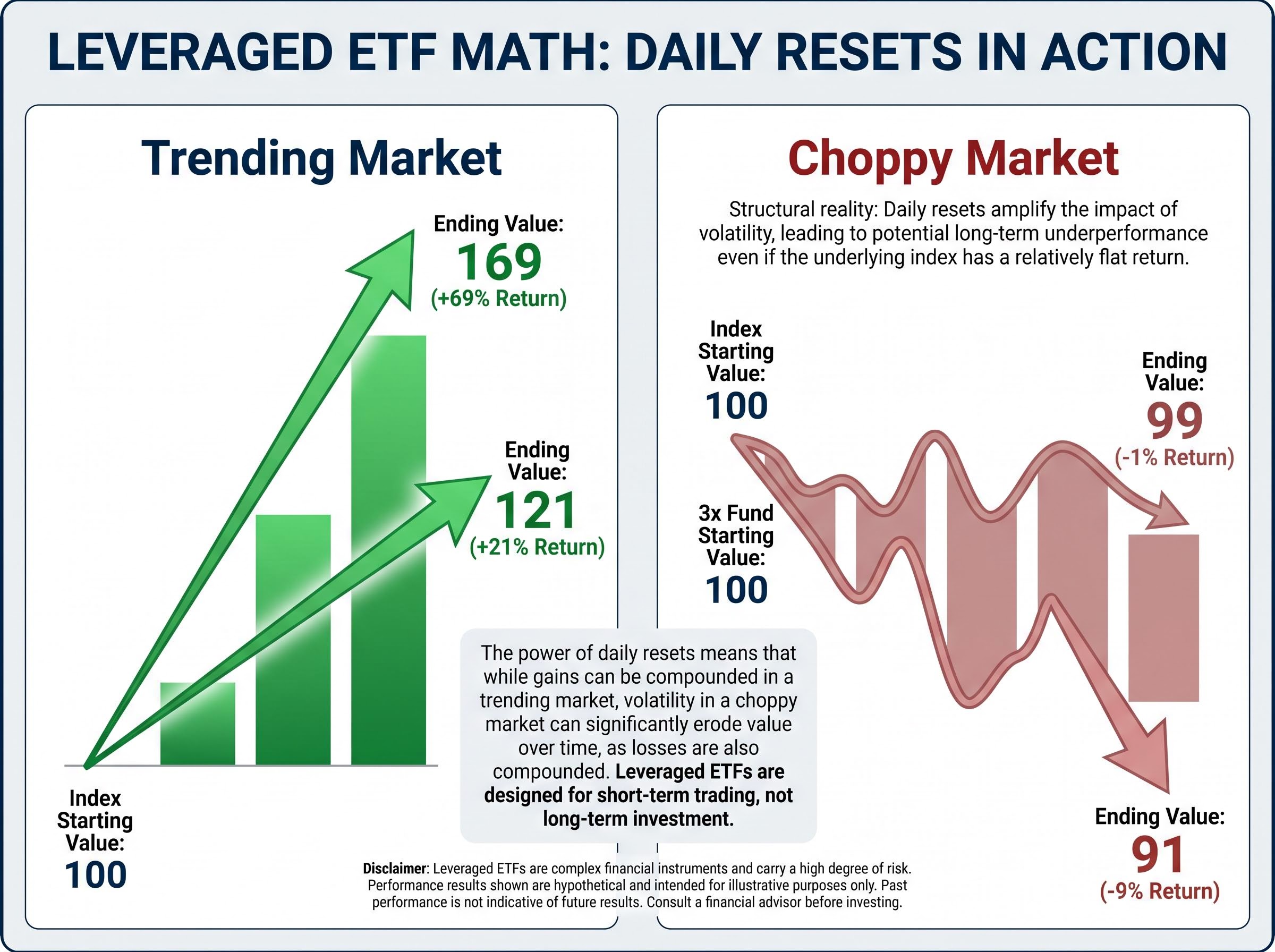

Consider an index that rises 10% on two consecutive days. It moves from 100 to 110 to 121, a cumulative gain of 21%. A 3x fund tracking those same moves goes from 100 to 130 on Day 1 (a 30% gain), then the reset establishes 130 as the new base. On Day 2, the index rises another 10%, so the fund gains 30% of 130, reaching 169. That is a 69% gain, more than three times the index’s 21% return.

| Day 0 | Day 1 | Day 2 | Total Return | |

|---|---|---|---|---|

| Index | 100 | 110 | 121 | +21% |

| 3x Fund | 100 | 130 | 169 | +69% |

The daily reset compounded in the investor’s favour because the direction was consistent. Research by Guedj, Li, and McCann (2010), the foundational academic treatment of rebalancing frequency and path dependency, established that this amplification is the mirror image of the decay that occurs when direction reverses. Both flow from the same mechanism.

The arithmetic of volatility drag, explained from first principles

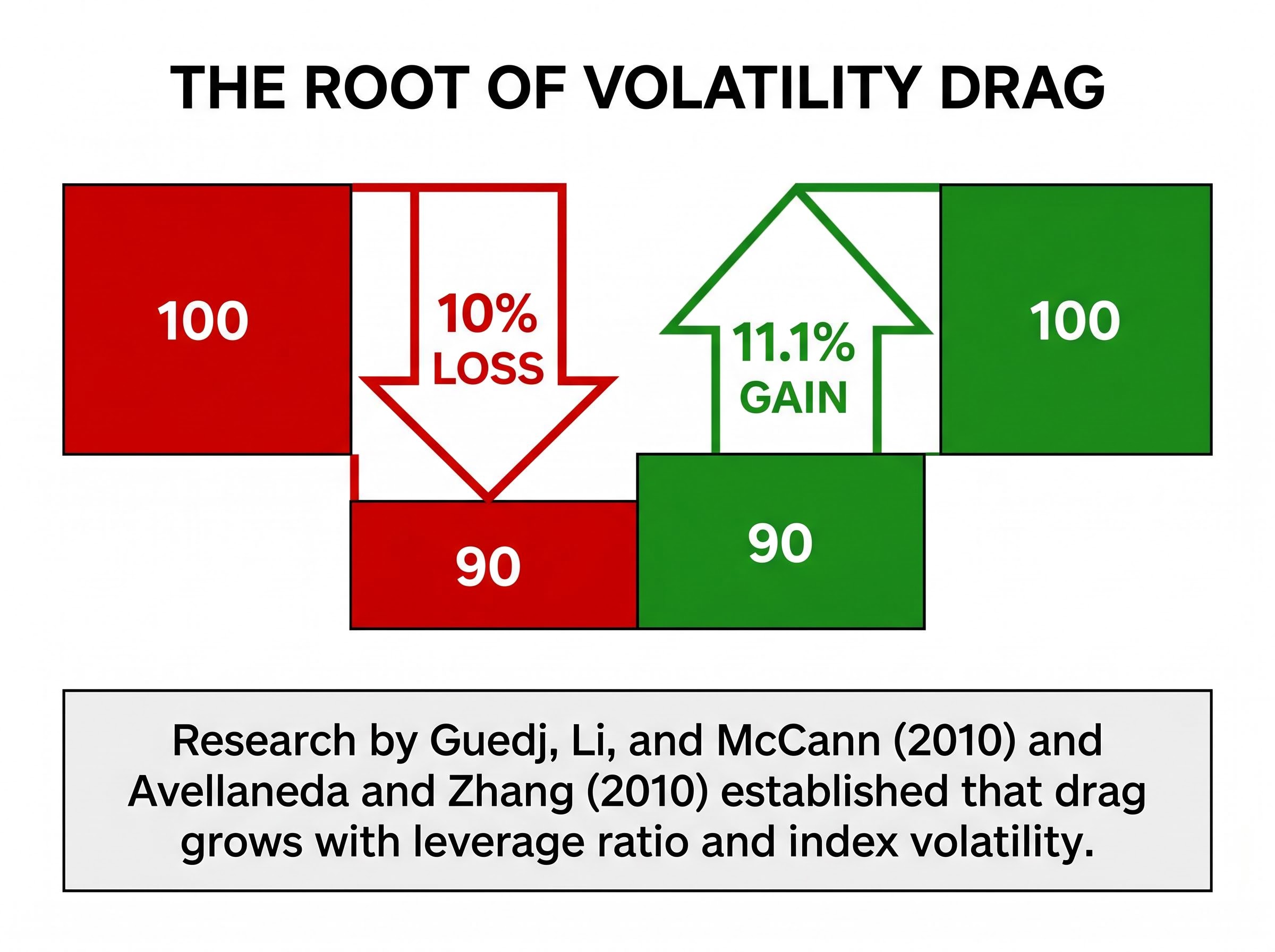

The root of volatility drag sits in a mathematical asymmetry that exists independently of leverage. A 10% loss does not require a 10% gain to recover. It requires an 11.1% gain. A portfolio that falls from 100 to 90 needs to rise by 11.1% just to return to 100. The larger the loss, the wider this asymmetry becomes.

Leverage magnifies the asymmetry. Take the sequence from the opening of this article: an index starts at 100, rises 10% to 110, then falls 10% to 99. The index lost 1%. Now apply a 3x fund to the same two moves. On Day 1, the fund gains 30%, moving from 100 to 130. The reset establishes 130 as the new base. On Day 2, the index falls 10%, so the fund loses 30% of 130, dropping to 91. The fund lost 9% while the index lost 1%.

| Start | Day 1 Move | Day 1 Value | Day 2 Move | Day 2 Value | |

|---|---|---|---|---|---|

| Index | 100 | +10% | 110 | -10% | 99 |

| 3x Fund | 100 | +30% | 130 | -30% | 91 |

The index completed a near-round-trip, losing 1%. The 3x fund lost 9% over the identical two-day period. The gap is not a fee, a spread, or a management cost. It is the mechanical result of how percentages compound when they alternate direction under leverage.

This drag is not fixed. Research by Guedj, Li, and McCann (2010) and Avellaneda and Zhang (2010) established closed-form estimates showing that the drag grows with both the magnitude of the leverage ratio and the volatility of the underlying index. A 3x fund in a high-volatility environment suffers materially more drag than a 2x fund in a low-volatility environment. These two papers remain the foundational quantitative treatment of the phenomenon; no subsequent study has overturned their estimates.

Path dependency: why the journey matters more than the destination

Volatility drag is a specific instance of a broader structural property called path dependency. Two portfolios can start at the same index level, end at the same index level, and land at materially different values in a leveraged fund if the sequence of daily moves between start and end differed.

This is what makes leveraged ETFs fundamentally different from a margin account or any fixed-leverage vehicle. In a margin account, borrowing a fixed amount to buy more shares, a 21% index gain produces a 21% gain on the borrowed portion regardless of whether the index rose steadily or swung violently on the way there. In a leveraged ETF, the daily reset actively changes the effective dollar exposure as the fund’s value fluctuates.

Three conditions cause path dependency to most severely punish leveraged ETF holders:

- High underlying volatility: Larger daily swings widen the percentage asymmetry that drives drag, compounding losses faster than gains.

- Long holding period: More trading days mean more resets, each of which can compound drag if direction is inconsistent.

- Range-bound or mean-reverting market: An index that oscillates without sustained directional movement maximises the number of alternating up-down sequences that produce the drag illustrated above.

What the academic record shows about holding periods

Guedj, Li, and McCann (2010) compared five rebalancing frequencies across a study period from December 2008 to December 2009 and found that portfolios rebalanced daily, the standard leveraged ETF structure, finished lowest. Portfolios without any rebalancing finished highest. The finding directly quantified how increasing rebalancing frequency amplifies sensitivity to path.

Real-world data corroborates the academic work. TECL and TECS (the 3x bull and 3x bear technology ETFs) both delivered returns during the volatile period from late 2008 to early 2009 that deviated sharply from simple multiples of the underlying technology index. According to Avellaneda and Zhang (2010), this divergence scales predictably with both volatility and leverage ratio, confirming the closed-form estimates in the Guedj research.

Identifying appropriate use cases and their structural requirements

Leveraged and inverse ETFs were designed for intraday and short-duration tactical use, not for multi-week or multi-month holding. This is not a matter of preference or risk appetite. It is a consequence of the structural design described above: the daily reset, combined with the percentage asymmetry, means the product’s mechanics work against any investor who cannot specify a short, defined holding period before entering.

Three legitimate short-term use cases emerge from the product’s design:

- Directional speculation over a defined brief window: An investor with a specific, time-bound thesis on near-term index direction, with a pre-set exit point.

- Hedging a core position around a known event: Using an inverse leveraged ETF to reduce portfolio exposure for a single session surrounding a specific catalyst, such as a Federal Reserve meeting.

- Relative-value pair trades across sectors: Pairing a bull leveraged ETF in one sector against a bear leveraged ETF in another to express a short-term relative view.

Each use case shares the same structural requirement: a defined holding period measured in hours or days, not weeks.

Investors drawn to inverse leveraged ETFs as a bearish tool should also weigh the short selling risks embedded in adjacent bearish instruments: borrow fees that can exceed 15% annualised, forced buyback events during short squeezes, and the asymmetric loss profile that makes directional accuracy alone insufficient to produce a profit.

One risk that compounds the daily reset problem is stacked leverage. A 3x leveraged ETF purchased on 2x margin creates a 6x effective exposure to the underlying index. Some U.S. brokerages restrict or prohibit margin use for these products for precisely this reason. Position sizing must account for the amplified move: in a 3x fund where a 5% underlying move becomes approximately a 15% fund move, sizing to risk $1,000 on a $100,000 portfolio means a maximum allocation of roughly $6,667 to the leveraged fund, not $20,000.

According to FINRA Regulatory Notice 22-08, firms are required to confirm that retail customers understand daily reset mechanics, compounding, and holding-period risk before granting access to leveraged and inverse exchange-traded products. FINRA’s 2024 Annual Regulatory Oversight Report confirmed the regulator continues to review how firms approve and supervise retail customers for these products.

The structural reality that the “3x” label does not tell you

The same daily reset mechanism produced two starkly different outcomes in the examples above. In a consistently rising market, the 3x fund turned a 21% index gain into a 69% fund gain. In a choppy market that completed a near-round-trip, the 3x fund turned a 1% index loss into a 9% fund loss. Both outcomes flow from identical mechanics.

| Scenario | Index Start | Index End | Index Return | Fund Start | Fund End | Fund Return |

|---|---|---|---|---|---|---|

| Trending (up 10%, up 10%) | 100 | 121 | +21% | 100 | 169 | +69% |

| Choppy (up 10%, down 10%) | 100 | 99 | -1% | 100 | 91 | -9% |

This paired comparison captures the single transferable test the mechanics above produce. Before holding a leveraged ETF beyond one trading day, the question is whether the market is trending directionally or moving with high intraday volatility and no net direction. Those two environments produce structurally opposite outcomes from the same product.

The “3x” label is accurate for its designed purpose: one trading day. For any longer period, volatility drag and path dependency reshape the outcome in ways the label cannot predict. FINRA Regulatory Notice 22-08 classifies these as complex products precisely because of this divergence between the daily promise and the multi-day reality.

This is not a product defect. It is a definitional precision that most marketing and most investor conversations obscure.

What every investor owes themselves before touching a leveraged ETF

Two structural phenomena, daily reset and volatility drag, make leveraged ETFs different from every other ETF a retail investor is likely to hold. A standard index fund delivers cumulative exposure regardless of how long it is held. A leveraged ETF delivers a daily multiple that compounds unpredictably, and often destructively, over any longer period.

The practical takeaway reduces to a single test: if an investor cannot specify a defined, short-duration rationale and an exit point before entering the position, the structural math works against them from the second trading day onward. This is not a matter of discipline or conviction. It is a consequence of the percentage asymmetry that daily resets impose.

FINRA classifies leveraged and inverse ETFs as complex products. Industry experts, including VettaFi’s head of research Todd Rosenbluth, have consistently characterised them as short-term trading instruments rather than core holdings. The regulatory and expert consensus does not constitute a ban, but it reflects a clear-eyed reading of the mechanics: these are precision instruments designed for a narrow purpose, and holding them beyond that purpose introduces risks that the product label does not communicate.

Investors exploring the broader leveraged product landscape beyond 2x and 3x daily-reset structures will find our deep-dive into leveraged covered call ETFs, which examines how a 1.25x equity exposure combined with a call-writing overlay produces a portfolio delta of approximately 0.92, yields exceeding 13%, and a compounding profile that differs structurally from the daily-reset products covered here.

“This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.”