Michael Burry just disclosed a leveraged short position against semiconductors. In the same breath, he told retail investors not to do what he is doing. The contradiction is worth unpacking, because it contains a structural truth about bearish investing that most individual traders learn only after losing money.

Burry’s May 2026 Substack post warning of a semiconductor bubble has reignited retail interest in shorting, arriving as the Philadelphia Semiconductor Index has rallied 65% in 2026 and major U.S. indices have surged approximately 11% since late March. When markets run this hard, the temptation to bet against them intensifies. But the same conditions that make a short thesis intellectually compelling are precisely what make the trade mechanically punishing for individual investors.

What follows is a step-by-step explanation of why short selling and put options carry a fundamentally different risk structure than going long, why the current environment has made bearish bets especially expensive, and what retail investors can do instead if they genuinely want to reduce equity exposure. The goal is a clear-eyed understanding of why even correct bearish calls frequently lose money in the hands of individual investors.

What Burry is actually doing (and what he said about you doing it)

Burry’s disclosed position consists of put options on the iShares Semiconductor ETF (SOXX) expiring January 2027. His 8 May 2026 Substack post compared the current semiconductor rally to the dot-com bubble and referenced employing a similar strategy around 2000. The position is a defined-risk bet that the SOX’s 65% surge will reverse before his options expire.

Then came the caveat. Burry explicitly warned that short selling is unsuitable and overly costly for most individual investors, characterising bearish bets as “increasingly expensive” in the current environment.

Burry’s explicit warning: short selling is not appropriate for most individual investors. The instruments are too costly, the timing risk too severe, and the capital requirements too demanding for retail accounts.

This is not hypocrisy. It is an acknowledgement of structural asymmetry. Burry operates with institutional capital buffers, negotiated fee structures, and the capacity to absorb months of adverse price movement. His track record includes being correct on direction but devastatingly early on timing, a combination that nearly destroyed his fund in 2007 before the mortgage trade paid off in 2008. A retail account facing the same gap between thesis and realisation does not survive it.

When big ASX news breaks, our subscribers know first

The mechanics of going short: why this is not simply the mirror image of buying

Most retail investors approach shorting with a simple mental model: if buying profits from prices going up, shorting profits from prices going down. The symmetry feels intuitive. It is also dangerously incomplete.

A naked short sale works as follows: the trader borrows shares through a broker, sells them at the current market price, and later buys them back (ideally at a lower price) to return to the lender. The profit equals the price decline minus all friction costs. The problem is the loss structure. A long stock position can fall to zero, a 100% loss. A short position faces a stock that can, in theory, rise without limit. Losses have no ceiling.

A naked short sale intervenes directly in price discovery mechanics: borrowed shares sold into the market create genuine sell-side pressure that can influence the order book, which is one reason regulators require margin accounts and impose maintenance thresholds rather than treating short positions as straightforward market transactions.

Put options offer a defined-risk alternative. The buyer pays a premium for the right to sell shares at a specified strike price before expiration. The maximum loss is capped at the premium paid. The trade-off is time decay (theta), which erodes the option’s value every day regardless of where the underlying stock trades.

| Attribute | Long stock | Short stock | Long put |

|---|---|---|---|

| Maximum loss | 100% of investment | Theoretically unlimited | Premium paid |

| Maximum gain | Unlimited | Capped at 100% (stock falls to zero) | Strike price minus premium |

| Margin required | No (cash account eligible) | Yes (margin account mandatory) | No |

| Time-sensitivity | None | Ongoing (borrow fees accrue daily) | High (theta decay daily) |

Short selling also requires meeting specific account conditions:

- A margin account (cash accounts are ineligible)

- A minimum account balance set by the brokerage, typically $2,000 or more

- Maintenance margin thresholds that, if breached, trigger margin calls demanding additional capital; failure to meet the call results in forced liquidation at the worst possible moment

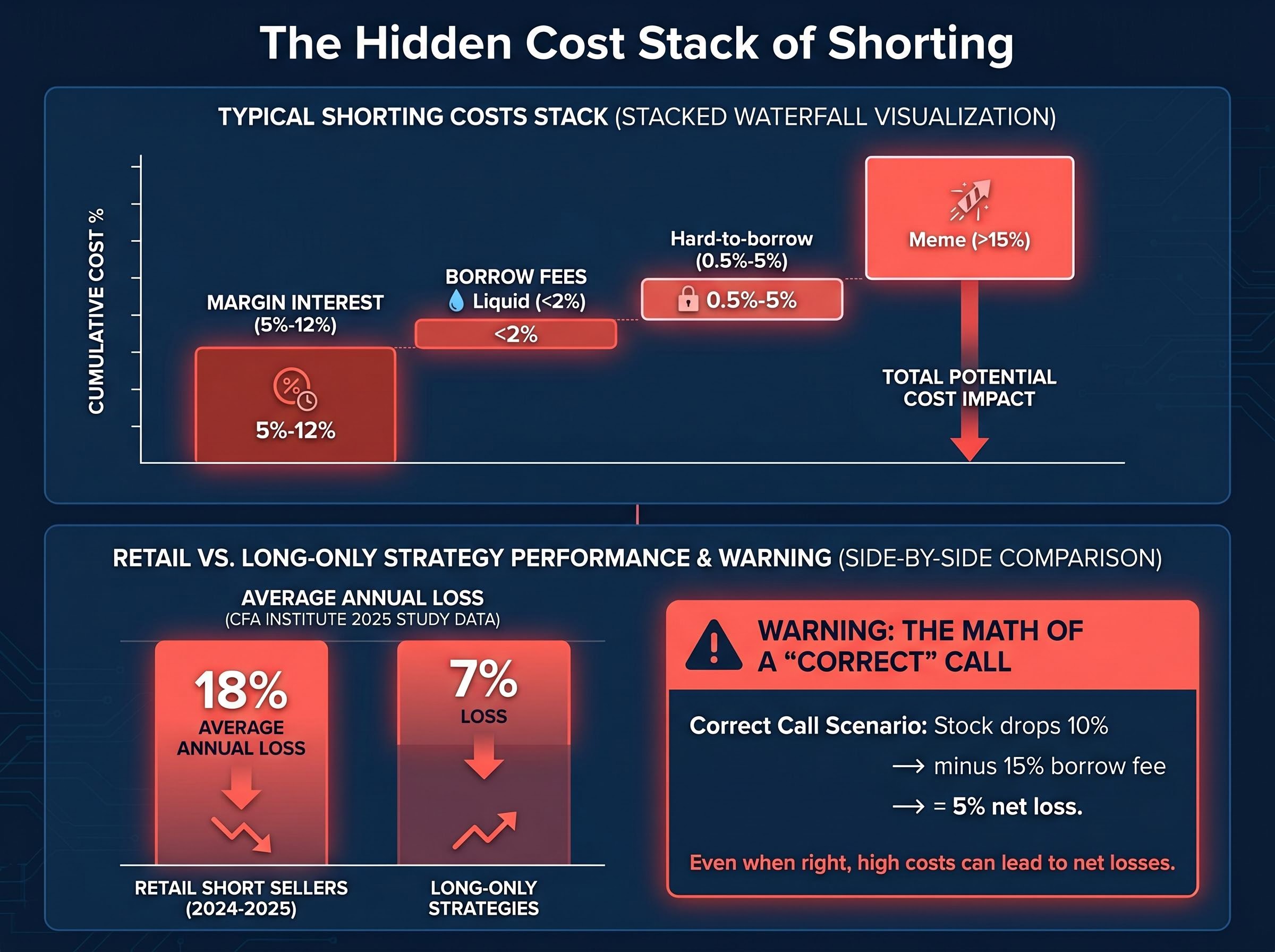

The hidden cost stack: what shorting actually costs before the trade pays off

Borrow fees are the primary friction cost. For most liquid, easy-to-borrow stocks, these run under 2% annualised. Common hard-to-borrow names typically cost 0.5%-5% annualised. In extreme conditions, heavily shorted meme stocks have seen borrow fees exceed 15% annualised, with rare cases documented above 100%.

Margin interest layers on top. With the federal funds rate at 3.5%-3.75% as of May 2026, typical retail margin interest rates range from approximately 5%-12% annualised depending on broker and account size. These charges accrue regardless of whether the short position is profitable.

For put buyers, the cost takes a different form. When markets have rallied sharply, put options carry elevated implied volatility and volatility skew, meaning investors pay above theoretical fair value for downside protection. The SOX’s 65% rally has driven semiconductor put premiums higher. Theta decay then erodes that premium daily, creating a cost that compounds even when the underlying stock moves sideways.

The cumulative effect is visible in the data.

A 2025 CFA Institute study found that retail short sellers lost an average of 18% annually from 2024-2025, compared to 7% losses for long-only strategies. Fee drag and timing errors were identified as the primary causes.

The following worked example illustrates why a correct directional call can still produce a loss:

| Scenario metric | Short seller result | Long holder result |

|---|---|---|

| Stock price movement (1 year) | -10% decline (correct call) | -10% decline |

| Borrow fee (annualised) | -15% | N/A |

| Net result | -5% loss despite correct direction | -10% loss |

The short seller was right about direction and still lost money. The cost stack consumed the entire profit and then some.

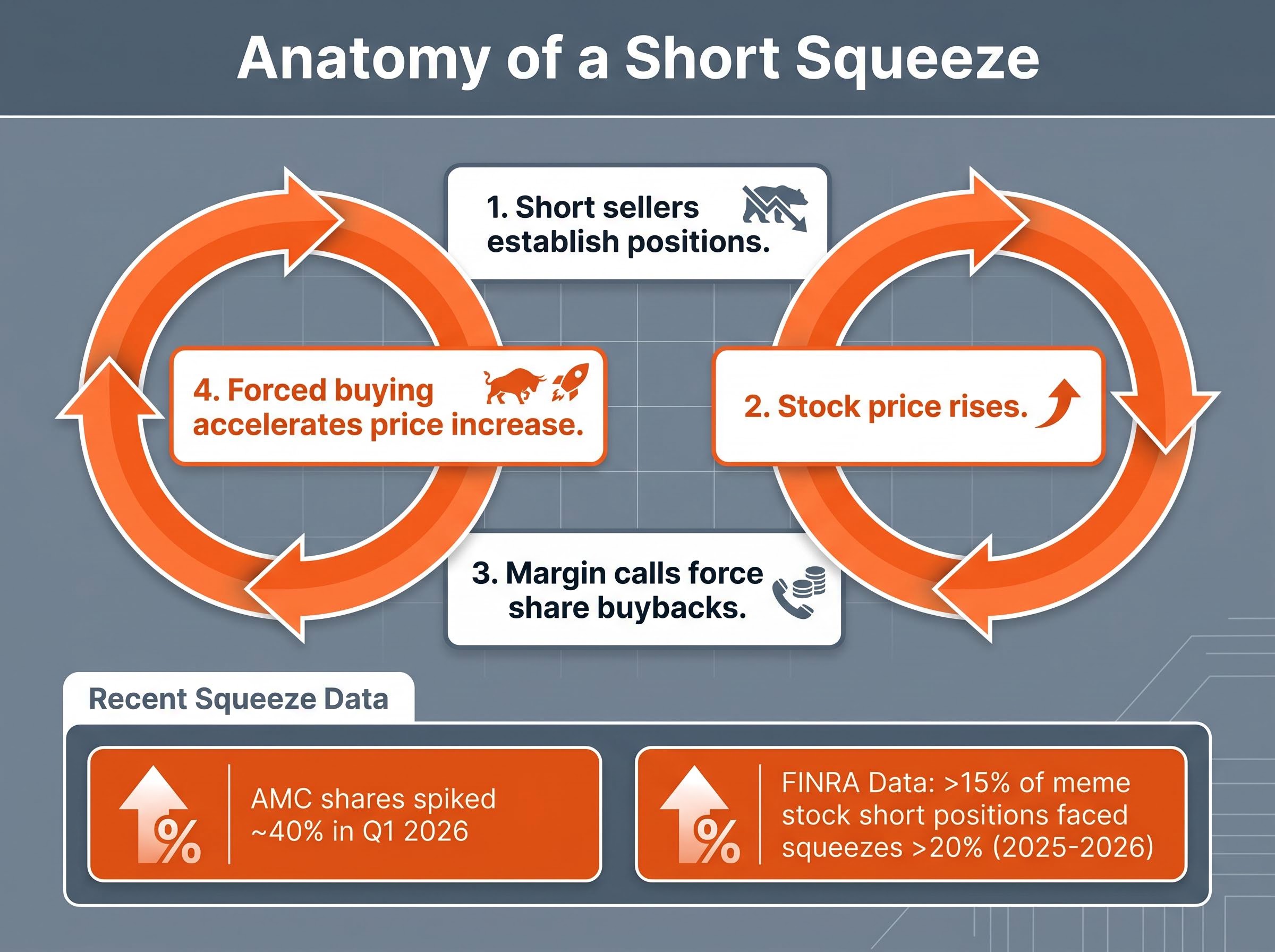

Short squeezes and the risk no model captures

A short squeeze occurs when a stock’s price rises sharply, forcing short sellers to buy back shares to limit losses. Their buying accelerates the price increase, which forces more short sellers to cover, creating a self-reinforcing feedback loop. The mechanics unfold in a predictable sequence:

- Short sellers establish positions, borrowing and selling shares they expect to decline

- The stock price rises, whether from fundamental news, coordinated buying, or momentum

- Margin calls hit short sellers whose losses exceed maintenance thresholds, forcing them to buy back shares

- That forced buying accelerates the price increase, triggering more margin calls and more covering in a cascading loop

This is not a theoretical scenario. AMC shares spiked approximately 40% in Q1 2026, causing significant retail short-seller losses. The GameStop and AMC events of 2021 established the template; the pattern has continued into the current cycle.

According to FINRA data, over 15% of short positions in meme stocks faced squeezes exceeding 20% during 2025-2026.

Regulatory changes have added a new dimension. SEC Rule 10b-21 now requires disclosure of short positions exceeding 2.5% of a company’s shares outstanding. While the rule enhances market transparency, it also increases the visibility of large short positions, which can amplify squeeze dynamics when those positions become publicly known. Coordinated buying campaigns have, in documented cases, targeted disclosed short concentrations.

For retail investors without institutional capital buffers, a single squeeze can exceed losses accumulated over years of careful investing. The risk is not gradual erosion. It is sudden, catastrophic, and largely uncontrollable once the feedback loop begins.

What retail investors can actually do if they are bearish

Reducing equity exposure does not require a margin account or instruments with unlimited loss potential. Four alternatives, ordered from simplest to most complex, offer genuine downside management.

Increasing cash allocation is the most straightforward approach. Selling equity positions and holding the proceeds in money market funds or Treasury bills generates meaningful yield in a 3.5%-3.75% rate environment with no risk beyond opportunity cost.

Defensive sector rotation shifts portfolio weight toward sectors that have historically held up better during downturns: utilities, consumer staples, healthcare, and dividend-paying equities. This reduces portfolio beta without requiring margin or options approval.

Inverse ETFs such as SOXS (3x inverse semiconductors) and SQQQ (3x inverse NASDAQ) provide daily inverse exposure without a margin account. The critical limitation: these instruments are designed for daily rebalancing. Over multi-week or multi-month holds, volatility drag (the compounding effect of daily resets) can cause significant underperformance versus the expected inverse return.

Put spreads involve buying a put at one strike price while simultaneously selling a put at a lower strike. The net premium paid is lower than a naked long put, and theta decay is partially offset by the premium received from the sold put. Maximum profit is capped, but maximum loss is defined and known at entry.

| Alternative | Margin required | Defined maximum loss | Time decay exposure | Complexity |

|---|---|---|---|---|

| Cash allocation | No | Yes (opportunity cost only) | None | Low |

| Defensive rotation | No | Yes (sector risk remains) | None | Low |

| Inverse ETFs | No | Yes (investment amount) | Volatility drag over time | Moderate |

| Put spreads | Options approval required | Yes (net premium paid) | Moderate (partially offset) | High |

When evaluating these alternatives, publications from Morningstar, Vanguard, and the CFA Institute consistently recommend assessing:

Investors evaluating whether to act on a bearish macro thesis should weigh US recession risk indicators beyond equity valuations, including consumer savings depletion and the growing divergence between headline spending data and underlying sentiment, because these signals determine whether a bearish thesis has fundamental economic backing or merely reflects a stretched multiple.

- Time horizon (inverse ETFs decay over time; puts have expiration dates)

- Cost relative to conviction level

- Whether the goal is hedging existing exposure or speculating on a decline

- Account type eligibility (IRA versus taxable, margin versus cash)

The gap between being right and making money: timing, conviction, and the retail disadvantage

The 2008 lesson Burry does not advertise

Burry’s mortgage short, the trade depicted in The Big Short, is remembered as a triumph of analytical conviction. The less-discussed chapter is what happened between 2005 and 2007, when the trade was deeply underwater on paper.

During that period, Burry’s investors demanded redemptions. The fund was haemorrhaging capital precisely because the thesis had not yet been validated by price. What preserved the trade was institutional structure: lock-up agreements that prevented investors from pulling capital, and a fund structure that could absorb years of adverse mark-to-market losses. The analytical thesis was correct. Without the institutional scaffolding, it would have been liquidated before it paid off.

What “being early” costs in time-limited instruments

Retail investors using puts face a constraint Burry’s fund structure mitigated: expiration dates. Every day of adverse or sideways movement costs theta. A correct thesis that arrives 90 days too late is a 100% loss of premium.

CFA Institute research on retail options traders consistently shows negative expected returns after fees, bid-ask spreads, and implied volatility premium for directional put buyers. The wash-sale rule adds a further complication: losses on short positions and puts may be deferred for tax purposes if a substantially identical position is re-established within 30 days. Being early is, in practical terms, functionally identical to being wrong when using time-limited instruments.

FINRA and SEC suitability standards require brokerage approval for margin and options accounts precisely because regulators recognise this asymmetric risk to retail participants. The approval process itself is an implicit acknowledgement that these instruments are not designed for the typical individual investor.

FINRA suitability standards require brokers to assess a customer’s full investment profile before recommending margin accounts or options trading, a framework that codifies what Burry’s warning articulates informally: these instruments carry risk characteristics that disqualify them for most retail participants.

Shorting is a professional tool in a retail market: what to take from Burry’s warning

Short selling and naked put buying are instruments with asymmetric cost structures, time pressure, and squeeze exposure. Institutional investors are equipped to absorb these forces. Retail investors, by the empirical evidence, generally are not. The CFA Institute’s finding of 18% average annual losses among retail short sellers from 2024-2025 is not an anomaly; it is the baseline outcome when these instruments meet retail capital constraints.

Bearish views can be correct and valuable without requiring bearish instruments. Cash allocation, defensive sector rotation, and defined-risk structures allow investors to act on a cautious outlook without accepting unbounded or time-decayed downside.

Before initiating any bearish position, three questions deserve honest answers:

- Can the full cost stack be modelled in advance (borrow fees, margin interest, implied volatility premium, theta decay)?

- Can the time horizon survive being early by weeks or months?

- Is the goal hedging existing portfolio exposure, or speculating on a directional move?

If any answer is uncertain, the position is likely unsuitable. Burry’s warning was not a confession that shorting is too complex for retail investors to understand. It was an acknowledgement that the instruments themselves are structurally disadvantageous for anyone without institutional capital behind them.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.