European Stocks Hit Highs While Institutional Money Stays Out

6 mins ago

While global markets have spent the past two years bidding up semiconductor and AI-exposed equities to historically stretched multiples, a smaller but credible group of professional investors has been moving in the opposite direction. Their target: beaten-down beverage companies, branded household goods, and consumer staples.

The divergence is not accidental. Persistent inflation, elevated mortgage rates, and cautious consumer spending have hammered sentiment toward consumer-facing businesses, dragging valuations to levels that contrarian managers argue price in a permanently weak consumer unlikely to materialise. Morningstar Investment Management, Magellan Financial Group, Platinum Asset Management, and Orbis Investments are among the Australian-accessible firms that have flagged this gap between market pessimism and underlying franchise value.

What follows unpacks the contrarian investing strategy behind the case for consumer defensives, what the historical record says about similar moments of sector-level dislocation, what it means for Australian retail investors, and where the genuine risks in this thesis lie.

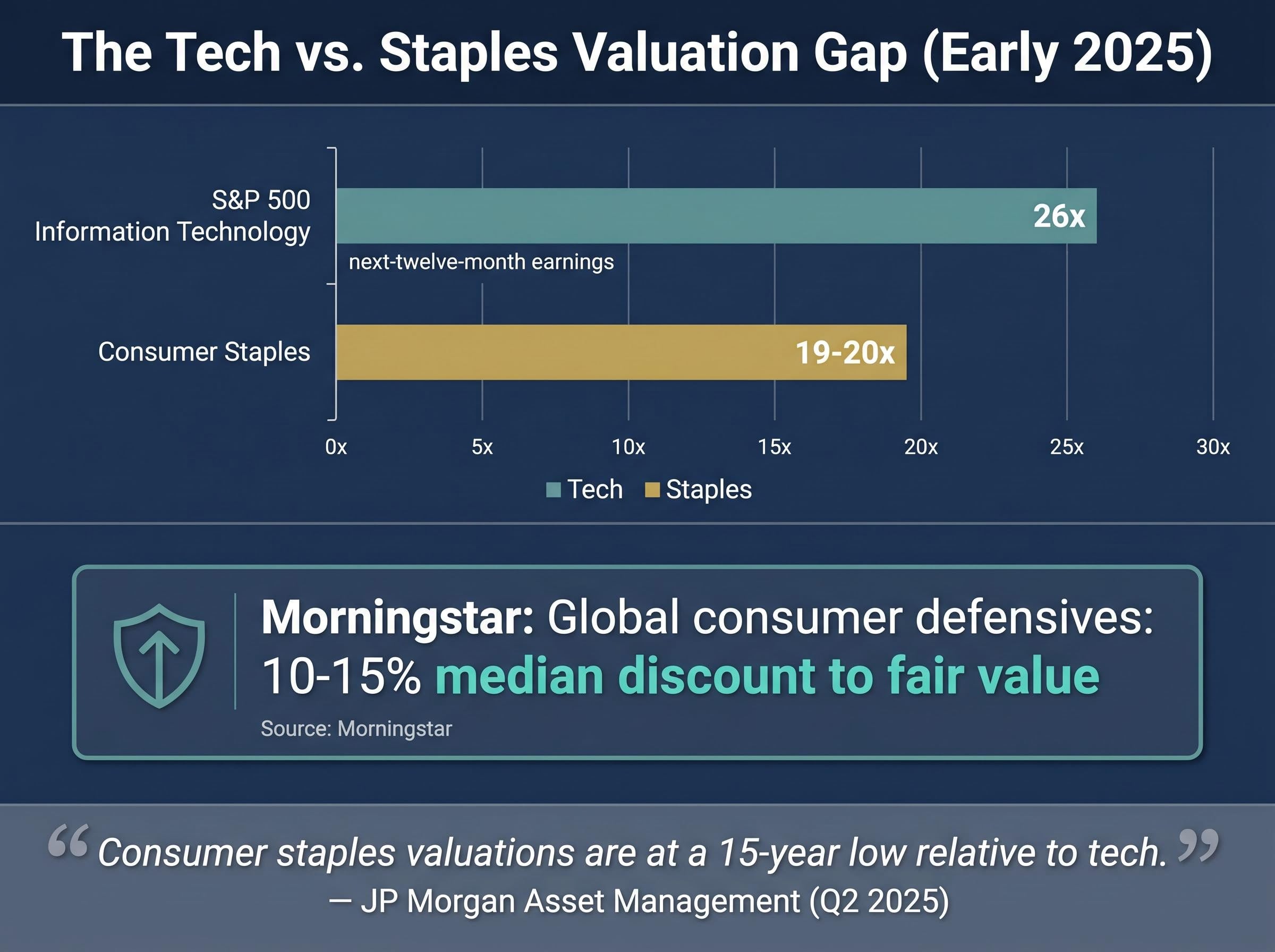

Market leadership over the past two years has been extraordinarily narrow. Capital has poured into a concentrated group of AI and semiconductor names, pushing forward valuations for S&P 500 Information Technology to approximately 26x next-twelve-month earnings as of early 2025, compared with roughly 19-20x for Consumer Staples. That differential is not subtle; it reflects a market that has decided one corner of the equity universe deserves a substantial premium while another deserves to be left behind.

The de-rating of consumer defensives has been driven less by deterioration in business quality than by the gravitational pull of capital toward AI. Morningstar has characterised global consumer defensives as trading at a median discount of 10-15% to fair value, while the technology sector has traded at or above fair value. Money that rotated into semiconductor fabricators and hyperscaler infrastructure did not come from nowhere; it came, in part, from the sectors now sitting at cyclical valuation lows.

Dennis Li, associate portfolio manager at Morningstar Investment Management, offered a direct challenge to the consensus in his May 2026 commentary. Li observed that AI capital expenditure remains concentrated among hyperscalers and a small number of large enterprises, raising questions about the durability of the spending cycle. He identified several conditions that remain unresolved for AI monetisation:

Li noted that the semiconductor sector is not particularly attractive at current valuations given these unresolved monetisation questions, a view that sits at odds with the market’s prevailing enthusiasm.

Semiconductor sector valuations are more internally varied than the index-level comparisons suggest, with Micron trading below 9x forward earnings while Intel sits above 100x, a dispersion that complicates the blanket dot-com parallel but does not undermine the observation that concentration in a narrow group of names has pulled capital away from other sectors.

For Australian investors who have benefited from technology-sector exposure, the valuation gap raises a straightforward question: what has been left behind while capital chased the AI thesis?

Contrarian investing, in its simplest form, means deliberately targeting assets where market sentiment is most negative, on the premise that pessimism has driven prices below what the underlying business is worth. It sounds straightforward. In practice, it is one of the most psychologically demanding strategies available to investors.

The logic rests on mean reversion: markets tend to over-extrapolate short-term conditions into long-run valuations, creating systematic mispricings. When a sector falls out of favour, its earnings multiple compresses beyond what the fundamentals justify. Patient capital that enters during the compression phase captures returns as sentiment normalises and the multiple expands back toward its long-run average.

The central analytical challenge for any investor considering the contrarian case is classifying sector declines correctly before assigning a valuation: a consumer staples de-rating driven by temporary cost-of-living sentiment is a fundamentally different situation from one caused by permanent structural disruption to the category itself, and conflating the two is where most contrarian bets go wrong.

Orbis Investments framed the current environment in its January 2025 investor letter as carrying “echoes of the dot-com bubble,” drawing a direct parallel to conditions in 1999-2000 when technology concentration reached similar extremes. Andrew Clifford of Platinum Asset Management described markets as pricing in a “permanently weak consumer” that most experienced value managers regard as an unlikely steady state. Martin Conlon, head of Australian equities at Schroders Australia, observed that consumer staples competitive positions are “as strong as ever” even as valuations price in permanent volume pressure.

Investors anchor to recent sector performance and extrapolate it forward. A sector that has underperformed for two years feels like it will underperform for another two. This anchoring effect is reinforced by career risk: institutional managers who underweight popular sectors risk near-term underperformance relative to benchmarks, creating structural resistance to contrarian positions even when the valuation signal is clear.

Three conditions typically sustain a contrarian opportunity:

Consumer defensives, as of mid-2026, meet all three.

The cost-of-living pressure facing Australian households is real and well documented. Elevated mortgage rates, persistent inflation, and declining real discretionary income have driven trade-down behaviour across supermarket categories. Both the Westpac-Melbourne Institute Consumer Sentiment Index and the ANZ-Roy Morgan Consumer Confidence Index have remained below the neutral level of 100 through 2024-2025, reflecting a household sector under sustained strain.

The RBA’s May 2025 Statement on Monetary Policy documented the extent of household substitution behaviour, noting that consumers had increasingly shifted toward cheaper private-label alternatives and reduced non-essential purchases as mortgage and inflation pressures persisted through the first half of 2025.

The RBA’s May 2025 Statement on Monetary Policy noted that households have “increasingly substituted towards cheaper brands and reduced non-essential purchases” in response to cost-of-living pressures.

Coles Group’s FY25 half-year results, released on 20 February 2025, confirmed a “continued shift towards Coles Own Brand and value-oriented ranges,” with Own Brand penetration increasing as customers sought to manage budgets. ABS Household Spending Indicator data from January 2025 showed that discretionary goods spending softened while non-discretionary categories including food grew modestly in nominal terms.

The ABS Monthly Household Spending Indicator for January 2025 confirmed the divergence between discretionary and non-discretionary categories, with food and essential goods holding positive nominal growth while clothing, recreation, and household furnishings softened, a pattern consistent with the valuation compression thesis rather than a broad consumer collapse.

The investment implication sits in the gap between this genuine consumer stress and what equity markets have priced. Markets have de-rated consumer staples equities on fears of prolonged demand weakness, but staples category volumes have held up better than the most pessimistic assumptions implied. Morningstar’s Australian equity outlook for Q1 2025 characterised ASX consumer defensives as trading at “the largest discount among non-cyclical sectors,” flagging several names as undervalued or fairly valued relative to their intrinsic worth.

| Company | Ticker | Directional Valuation Signal | Morningstar Commentary Note | Verification Status |

|---|---|---|---|---|

| Coles Group | COL | Trading below estimated fair value | Defensive earnings story amid cost-of-living pressures | Requires re-verification |

| Woolworths Group | WOW | Slight discount to estimated fair value | Margin pressures largely priced in | Requires re-verification |

| Treasury Wine Estates | TWE | Trading below estimated fair value | China tailwinds underappreciated by the market | Requires re-verification |

For Australian retail investors living through this consumer environment, the macro context is personally familiar. The contrarian thesis rests on a specific observation: staples volumes are holding while equity valuations have been compressed, suggesting the market’s most bearish assumptions are not being validated in the actual data.

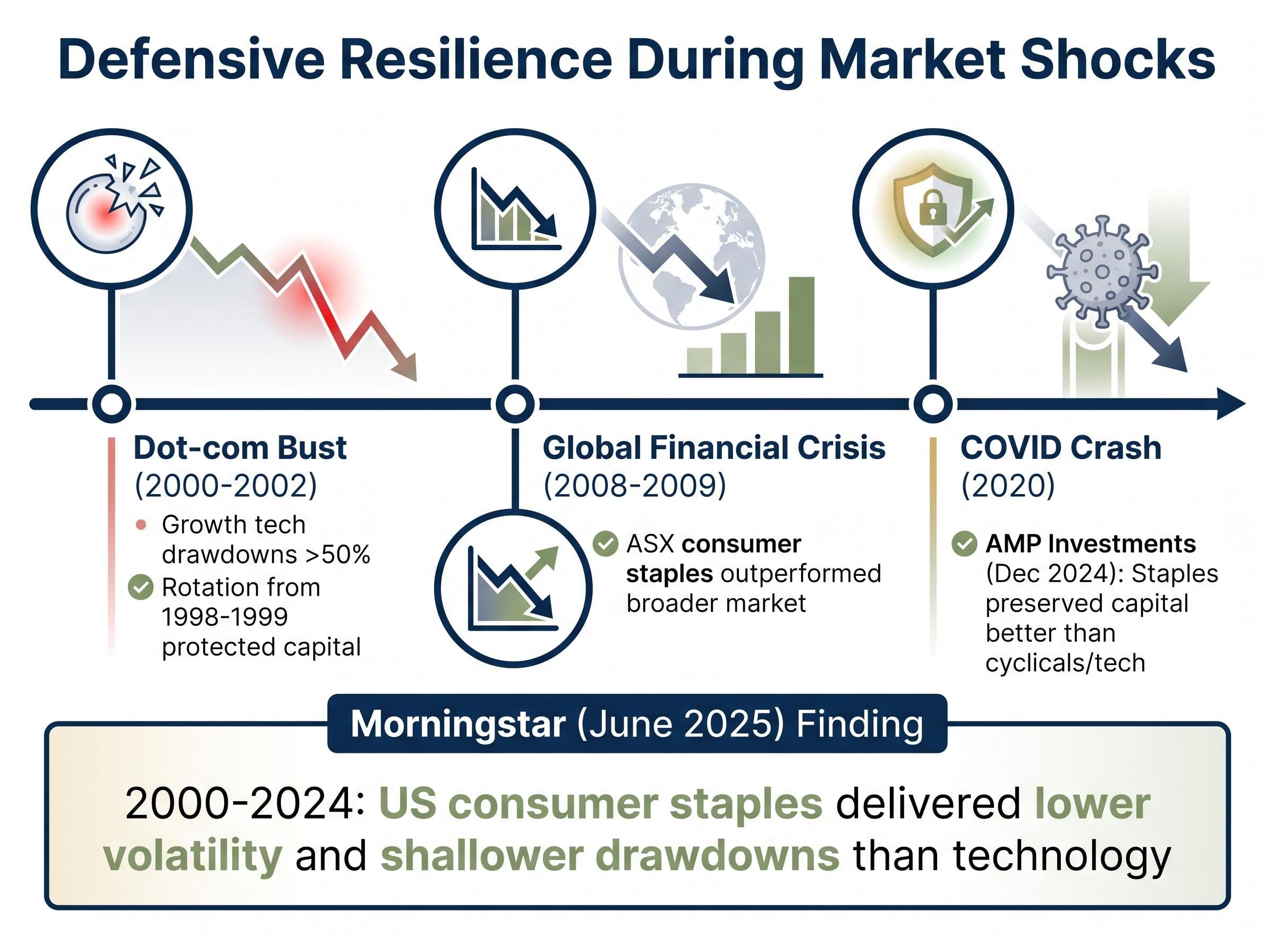

The current environment is not without precedent. Two episodes in particular illustrate what has historically happened when narrow technology leadership stretches valuations and contrarian capital rotates toward defensives.

GMO’s research drew an explicit parallel: the concentration of enthusiasm in AI and semiconductor names today mirrors the narrow TMT leadership of the late 1990s, and the valuation discipline that looked wrong during the bubble phase was vindicated over a 3-5 year horizon.

Morningstar’s Dan Lefkovitz showed in June 2025 research that from 2000-2024, US consumer staples delivered materially lower volatility and shallower drawdowns than technology, producing attractive risk-adjusted returns. Wilsons Advisory confirmed the pattern in the Australian context, noting that ASX consumer staples outperformed the broader market during both the 2000-2002 tech bust and the 2008-2009 GFC.

For investors nervous about moving against the current consensus, the historical record offers a clear message: similar moves were rewarded in prior cycles, though the timing of mean reversion required patience.

The practical question is not whether consumer defensives will outperform next quarter. It is whether a portfolio heavily weighted toward technology and AI-exposed equities has adequate exposure to sectors trading at cyclically depressed valuations.

The ASX consumer staples sector underperformance over the past five years, a cumulative drag of approximately 1.17% per annum against a broader market returning over 4% annually, is precisely the kind of extended relative weakness that creates the entry conditions contrarian managers identify as attractive, provided the underlying competitive positions remain intact.

Australia’s largest superannuation funds have begun framing the question in similar terms. AustralianSuper’s March 2025 member update described defensive sector exposure as “ballast against potential reversals in the tech trade.” Sam Sicilia, Chief Investment Officer of Hostplus, noted in May 2025 that “history suggests such concentration does not persist indefinitely,” with the fund maintaining exposure to value and defensive sectors to capture potential re-rating. JP Morgan Asset Management’s Guide to the Markets for Q2 2025 (Australia edition) observed that “consumer staples valuations are at a 15-year low relative to tech.”

Morningstar has framed the contrarian case as a “3-5 year risk-adjusted return argument” rather than a short-term trade. That time horizon matters, because the mean reversion that drives contrarian returns can take longer than most investors expect.

A few questions worth asking of any equity portfolio:

Global consumer staples names such as Nestlé, Coca-Cola, Procter & Gamble, and Diageo require currency management for Australian dollar investors. Hedged fund vehicles offer one approach; accepting AUD/USD or AUD/CHF exposure is another, with different return and risk profiles.

ASX-listed consumer staples offer direct exposure without currency risk but are concentrated in two or three names, primarily Woolworths and Coles. Internationally diversified managed fund or ETF vehicles provide broader access to the global opportunity set, though they introduce currency and fee considerations.

The contrarian case, if persuasive, still requires translating a macro thesis into a concrete allocation, and portfolio construction for Australian investors in this environment involves decisions about how to balance the CGT implications of repositioning, the role of hedged versus unhedged international vehicles, and the mechanics of adding defensive exposure without simply duplicating existing superannuation allocations.

The contrarian thesis for consumer defensives is not without material risks, and a balanced assessment requires stating them directly.

Morningstar’s own analysis acknowledged that the semiconductor sector reacted to genuine demand signals, including agent-based AI deployment and GPU requirements, rather than pure speculation. Dennis Li’s observation was that AI productivity benefits are uncertain in timeline, not that they will never materialise.

Contrarian positioning requires a genuine multi-year time horizon, because the mean reversion that drives returns can take considerably longer than most investors expect. The strategy’s discomfort is its edge, but it is also its cost.

The contrarian case for consumer defensives is not a call against AI or a prediction about short-term market direction. It is a valuation-disciplined observation: capital concentration has created a relative opportunity in sectors with durable competitive positions and depressed multiples.

Three pillars support the thesis. First, the valuation gap created by AI enthusiasm has left consumer defensives trading at discounts to long-run fair value. Second, historical precedent from the dot-com bust and the GFC shows that defensive outperformance in similar moments rewarded patient capital over 3-5 year horizons. Third, the live Australian macro context has depressed sentiment without collapsing staples fundamentals, creating a gap between what the market prices and what the data shows.

For Australian investors, the question is not whether to choose between AI and baked beans, but whether their portfolio reflects a genuine view about relative value or simply mirrors the current consensus.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A contrarian investing strategy involves deliberately targeting assets where market sentiment is most negative, on the premise that pessimism has driven prices below what the underlying business is actually worth, allowing patient investors to capture returns as sentiment normalises.

Consumer staples have been de-rated primarily because capital has rotated aggressively into AI and semiconductor names, not because of material deterioration in business quality; Morningstar has characterised global consumer defensives as trading at a median discount of 10-15% to fair value as a result.

Orbis Investments and GMO have both drawn explicit parallels between today's narrow AI and semiconductor leadership and the TMT concentration of 1999-2000, noting that investors who rotated into out-of-favour defensives before the dot-com bust avoided drawdowns exceeding 50% and generated positive returns over a 3-5 year horizon.

Key risks include the possibility that AI capital expenditure proves durable and supports current tech valuations, that Australian consumer weakness is structural rather than cyclical, and that the ASX consumer staples index is heavily concentrated in Woolworths and Coles, limiting diversification.

Australian investors can access global consumer staples such as Nestle, Coca-Cola, Procter and Gamble, and Diageo through internationally diversified managed funds or ETFs, though these introduce currency and fee considerations; ASX-listed names like Woolworths and Coles offer direct exposure without currency risk but are concentrated in just two or three companies.