Why Your ETF Portfolio May Be Less Diversified Than You Think

50 mins ago

An ETF investor who built a $100,000 portfolio over the last decade could accumulate approximately $26,000 less in after-tax wealth under the rules taking effect from 1 July 2027, according to modelling published by Stockspot. That is not a marginal adjustment. It is a structural change to how long-term investing is taxed in Australia.

On 12 May 2026, the Australian Federal Government handed down the 2026-27 Federal Budget and announced the most significant overhaul of the capital gains tax framework since the 50% discount was introduced in 1999. The centrepiece: abolition of that discount and its replacement with CPI-based cost indexation plus a 30% minimum effective tax rate on real capital gains. The changes take effect from 1 July 2027, giving investors just over 13 months to understand, prepare, and take professional advice where needed.

This article explains how the new capital gains tax system in Australia works, walks through the transitional split-period rules that apply to assets held before and after the switch date, quantifies the real-dollar impact on ETF and share investors, and assesses which investment structures come out ahead or behind under the new settings.

For 27 years, the rule was straightforward. An individual who held an asset for longer than 12 months included only 50% of the capital gain in their assessable income. Introduced on 21 September 1999, the discount replaced an earlier indexation model and became one of the defining features of the Australian tax system for investors.

The Government’s stated rationale for replacing it rests on two arguments. Treasury’s position is that the fixed 50% discount systematically overcompensated some asset classes for inflation, particularly established housing, while undercompensating others in certain periods, distorting how capital flows through the economy.

Treasury analysis concluded that the 50% discount frequently overcompensated established housing for inflation, contributing to capital allocation distortions and housing affordability pressures across multiple market cycles.

The Government’s two stated policy objectives and the two principal criticisms line up as follows:

Understanding the policy rationale matters because it signals which directions future adjustments might take. This is a structural change with identifiable winners and losers, not an arbitrary revenue measure.

From 1 July 2027, the cost base of an asset is adjusted upward for inflation (CPI) before the taxable gain is calculated. In practice, this means only the real gain, the amount by which an asset’s value has grown above and beyond inflation, is assessable.

The reform applies to individuals, trusts, and partnerships. Companies were never eligible for the 50% discount and are unaffected.

Where the old system halved the nominal gain regardless of what inflation actually was, the new system uses actual CPI data to strip out inflation. In a high-inflation environment, that produces generous cost base adjustments. In a low-inflation environment, the adjustments are modest, and the tax bill on a given nominal gain can be materially higher than under the old discount.

Both Pitcher Partners and Baker McKenzie have published analysis on the mechanical operation of the new framework, drawing on official Budget materials.

The 2026-27 Federal Budget tax reform documentation confirms the policy intent to tax only real capital gains, with the 50% discount replaced by CPI indexation and a 30% minimum effective rate applying from 1 July 2027 across individuals, trusts, and partnerships.

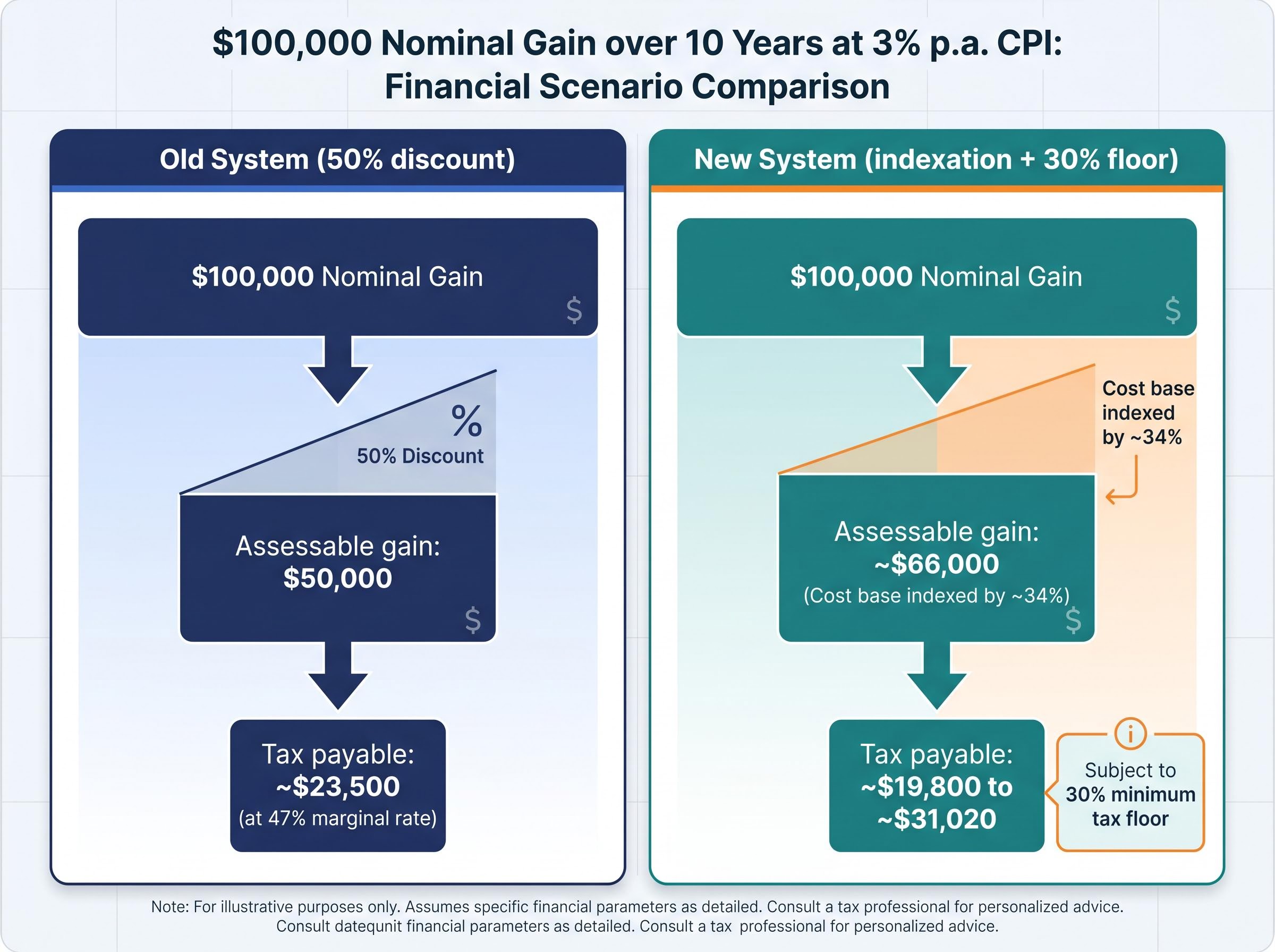

The following worked example illustrates the difference. It assumes a $100,000 nominal gain on an asset held for 10 years with average annual CPI of 3%.

| Scenario | Old system (50% discount) | New system (indexation + 30% floor) |

|---|---|---|

| Nominal gain | $100,000 | $100,000 |

| Inflation adjustment | None (flat 50% discount applied) | Cost base indexed by ~34% (CPI over 10 years at 3% p.a.) |

| Assessable gain | $50,000 | ~$66,000 (real gain after indexation) |

| Minimum effective tax rate | None (taxed at marginal rate on $50,000) | 30% floor on real gain |

| Tax payable (at 47% marginal rate) | ~$23,500 | ~$19,800 (30% of $66,000) to ~$31,020 (47% of $66,000) |

The interaction between indexation and the minimum rate produces different outcomes depending on inflation levels, holding periods, and the investor’s marginal tax rate. Getting the mechanics right matters before any portfolio decision is made.

The CGT reform mechanics, including the precise interaction between CPI indexation, the 30% minimum tax floor, and the split-period calculation for assets held across the transition date, are covered in full in our dedicated guide to Australia’s new CGT rules from 1 July 2027, which also walks through the retirement income-timing strategy that the 30% floor effectively closes off.

The 30% floor is not a flat tax. It is a minimum. A high-income investor on a 47% marginal rate paid an effective rate of approximately 23.5% on a qualifying gain under the old system (47% applied to the 50% discounted gain). Under the new system, that investor pays their full marginal rate on the real gain, which at 47% is well above the floor.

The floor bites hardest for investors whose marginal rate would otherwise produce an effective rate below 30% on the old discounted gain. Under the new system, these investors also hit the 30% minimum, meaning the floor applies across the income spectrum, not only at the top.

The change is prospective. Only gains accruing after 1 July 2027 fall under the new rules. Gains accrued before that date retain eligibility for the 50% discount.

That principle is straightforward. Implementing it is not. For any asset held across the boundary date, the total gain on disposal must be apportioned between two periods, each with different tax treatment. Two options are available to taxpayers:

The compliance burden is real. Investors must be able to separate pre- and post-transition gains across all relevant assets, including shares, ETF units, managed fund units, and real property. As of mid-May 2026, no draft legislation has been introduced, and the split-period apportionment methodology awaits confirmation through the parliamentary process.

Assets acquired before 20 September 1985 have historically been entirely exempt from capital gains tax. Under the new framework, that blanket exemption no longer covers gains accruing after 1 July 2027. Any growth from that date forward becomes taxable for the first time.

This is a particularly significant development for long-held family assets, investment properties, and business interests acquired before the original CGT regime was introduced in 1985. The pre-CGT status is preserved for gains accrued up to 1 July 2027, but from that date forward, the new indexation and 30% minimum tax rules apply.

The compliance implication is immediate: holders of pre-CGT assets who have never needed to track cost base information will now need to establish a baseline value as at 1 July 2027.

The compliance implication of pre-1985 asset valuation extends beyond record-keeping logistics: holders of long-held family farms, rural properties, and business interests built before the original CGT regime have never needed to track market values, and establishing a credible deemed cost base as at 1 July 2027 involves both formal valuation risk and potential disputes with the ATO over methodology.

Stockspot modelling indicates a $100,000 ETF portfolio growing over ten years could accumulate approximately $26,000 less in after-tax wealth under the new CGT settings compared to the old 50% discount framework.

That figure is not a worst-case projection. It reflects a realistic passive ETF portfolio. The impact on more active or higher-turnover strategies could be materially larger.

Even modest increases in annual tax drag compound significantly over long holding periods. A seemingly small percentage-point increase in effective tax rate, applied to realised gains year after year, produces disproportionate dollar differences over a decade. This is the compounding penalty of higher tax drag.

Passive ETFs, because they have low portfolio turnover, generate fewer realised capital gains annually compared to active strategies. That structural feature partially offsets the new regime’s impact relative to higher-turnover alternatives. The three channels through which ETF investors are affected operate simultaneously:

No public statements from Vanguard Australia, BlackRock iShares, or BetaShares regarding the CGT changes and their implications for ETF structures have been located as of mid-May 2026.

Index ETFs rebalance periodically. Index reconstitution events, dividend reinvestment management, and redemption processing can all crystallise gains within the fund that are then distributed to unitholders. Under the new rules, these distributed gains are subject to indexation and the 30% minimum tax for the post-1 July 2027 component.

This matters for buy-and-hold investors who assumed they were deferring all CGT by not selling their units. The fund’s internal activity can trigger taxable events the investor did not choose to initiate, and the after-tax cost of those distributions rises under the new framework.

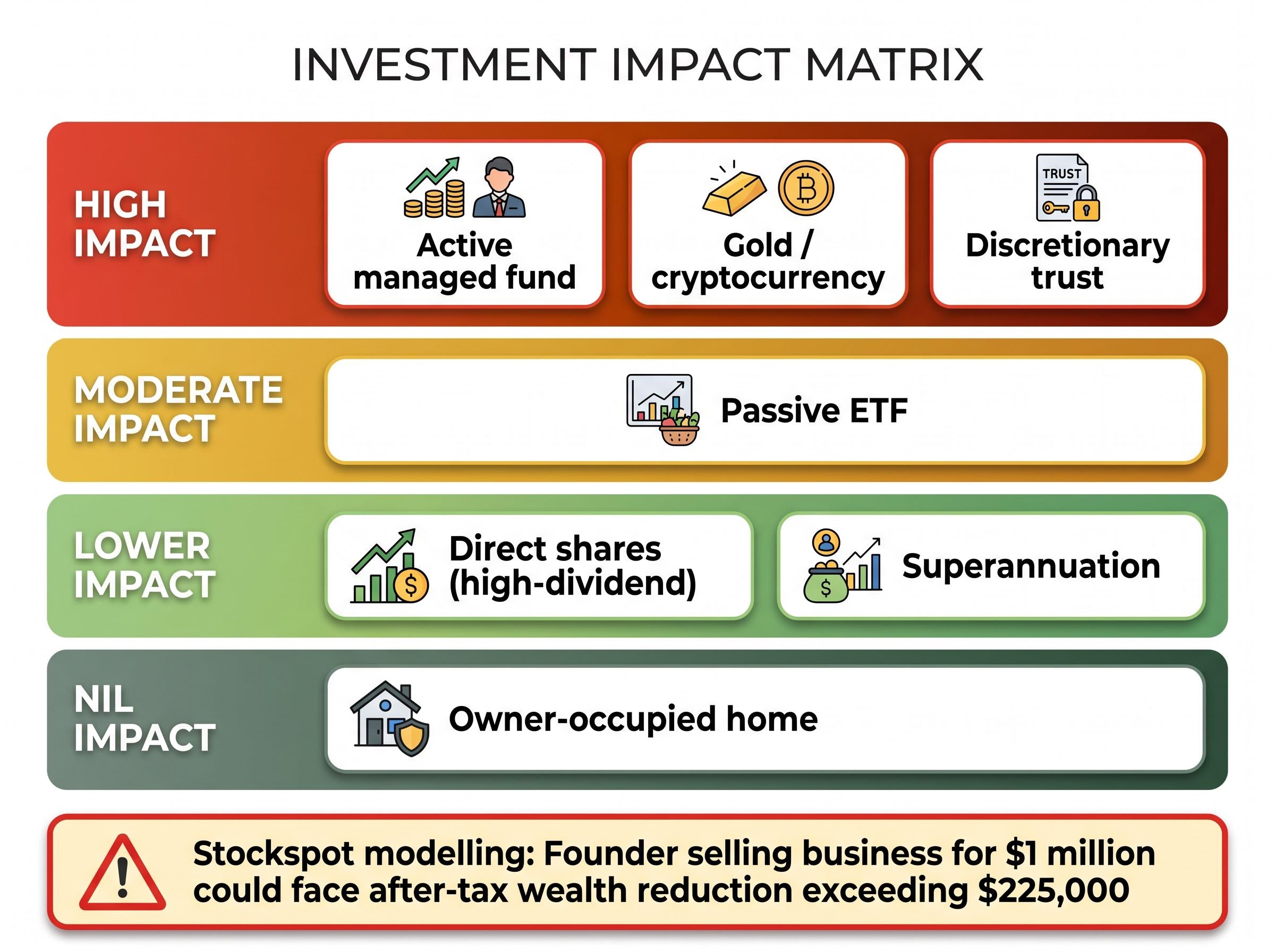

Not every portfolio is equally exposed. The following table maps the relative CGT impact across common investment structures.

| Investment structure | Key return driver | Relative CGT impact | Notes |

|---|---|---|---|

| Passive ETF | Capital + income | Moderate | Low turnover defers taxable events; partially offsets higher rates |

| Active managed fund | Capital + income | High | Frequent distributed gains amplify the new regime’s impact |

| Direct shares (high-dividend) | Primarily income | Lower | Franking credits deliver return as income, reducing reliance on capital gains |

| Gold / cryptocurrency | Capital appreciation only | High | No income component; entire return subject to CGT on disposal |

| Discretionary trust | Capital + income | High | Subject to 30% minimum trust distribution tax under new rules |

| Superannuation | Capital + income | Lower | Concessional tax treatment; constrained by contribution caps and access rules |

| Owner-occupied home | Capital appreciation | Nil | Retains full CGT exemption |

Superannuation’s relative attractiveness increases, but annual contribution caps and the fact that younger investors accumulating wealth outside super face the full effect of the new rules limit its utility as a complete solution. Stockspot modelling suggests a founder selling a business for $1 million could face an after-tax wealth reduction exceeding $225,000 under the new framework.

A secondary effect deserves attention: as effective tax rates on capital gains rise, investors face stronger incentives to defer realisation, reducing capital mobility and potentially slowing reallocation to more productive assets. Negative gearing restrictions (limited to newly constructed residential properties) compound the property investment impact alongside the CGT changes.

The sectoral rotation toward franked dividends is already being flagged by advisers as a predictable consequence of raising effective CGT rates: banks, telcos, utilities, infrastructure, and A-REITs on the ASX deliver a higher proportion of total return as fully franked income rather than capital appreciation, improving their relative after-tax position for individual investors under the new framework.

The lock-in effect on capital mobility is a secondary consequence that the Government’s stated policy objective of redirecting capital toward productive uses may partially contradict: as effective tax rates on realised gains rise, rational investors hold assets longer to defer tax, reducing the reallocation that the reform was designed to encourage.

The 13-month window between the Budget announcement and the transition date is not a crisis period, but it is a planning window. Four near-term actions are appropriate:

The reforms announced on 12 May 2026 still require full parliamentary passage. Final legislative details, including the split-period apportionment methodology, may shift during the parliamentary process. Investors are encouraged to monitor developments rather than act on the announcement alone.

Platform providers such as Stockspot have indicated they intend to update tax reporting systems once final legislative details are confirmed.

The replacement of the 50% discount with CPI indexation and a 30% minimum tax on real capital gains is the most significant structural change to Australia’s capital gains tax framework in 27 years. For ETF investors, long-term shareholders, and holders of pre-CGT assets, the dollar consequences are real and quantifiable.

Genuine uncertainty remains. Draft legislation has not been introduced. The split-period apportionment methodology is unconfirmed. The interaction with MIT and AMIT structures awaits legislative detail. The political path through Parliament has yet to play out.

The appropriate response is preparation, not alarm. Establishing clean records, reviewing portfolio structure, and engaging professional advice where complexity warrants it are the highest-value uses of the next 13 months. Passive, low-turnover investing retains its structural advantages under the new system, even if the absolute after-tax return profile is lower than under the old regime.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The legislative framework described in this article is based on the 2026-27 Federal Budget announcement and official Budget materials; final details are subject to change through the parliamentary process.

From 1 July 2027, the 50% CGT discount that has applied since 1999 is replaced by CPI-based cost indexation plus a 30% minimum effective tax rate on real capital gains, applying to individuals, trusts, and partnerships.

Stockspot modelling indicates a $100,000 ETF portfolio held over ten years could accumulate approximately $26,000 less in after-tax wealth under the new rules compared to the old 50% discount framework, with passive low-turnover ETFs faring better than high-turnover active strategies.

The change is prospective, so gains accrued before 1 July 2027 retain eligibility for the 50% discount, while gains accruing after that date fall under the new indexation and 30% minimum tax rules; investors must apportion the total gain between the two periods using either a formal valuation or an ATO formula.

Investors should establish asset valuations and cost base records as at 1 July 2027, avoid making major structural changes before draft legislation is finalised, review portfolio turnover, and seek professional tax advice if they hold assets in trusts, pre-1985 assets, or complex structures.

Owner-occupied homes retain a full CGT exemption, superannuation benefits from concessional tax treatment, and high-dividend direct shares are partially sheltered because franking credits deliver returns as income rather than capital gains, reducing reliance on the CGT discount.