The $275,000 Cost of Australia’s New Investment Tax Rules

30 mins ago

When semiconductor stocks surge faster than the earnings revisions that should justify them, the gap between price and proof becomes the story. In the week of 12 May 2026, Morningstar Investment Management flagged precisely this concern, warning that chipmaker valuations had climbed on artificial intelligence agent adoption narratives that have yet to translate into verifiable application-layer profitability. Semiconductor stocks including AMD, Micron, and Samsung posted sharp gains in the weeks leading into mid-May, driven by a narrative shift within AI: from model training toward AI agent deployment, a use case requiring substantially more persistent compute and memory infrastructure. The move lifted valuations well ahead of consensus earnings revisions, prompting rare public caution from an institutional manager not known for reflexive pessimism. What follows is an examination of what is actually driving the rally, where the valuation assumptions are most vulnerable, and what Australian investors holding semiconductor exposure through Nasdaq-100 ETFs or global technology funds should be weighing right now.

The rally’s internal logic is coherent. AI agent deployment, unlike model training, demands always-on compute infrastructure that runs continuously rather than in intensive but episodic bursts. Where training clusters spin up, process, and release capacity, agent infrastructure stays persistently active, consuming GPUs, CPUs, and memory chips around the clock. That distinction implies a step-change in the duration, not just the volume, of semiconductor demand.

AMD’s Q1 2026 earnings illustrated just how significant the shift is: the company raised its server CPU total addressable market growth forecast from 18% to 35% annually after identifying agentic AI workloads as a structural driver in procurement data, with 35-45% of inference tasks estimated to be CPU-bound rather than GPU-dependent.

The supply gap relative to these elevated expectations amplified investor sentiment across the sector. AMD, Micron, and Samsung all saw share price appreciation in the weeks prior to mid-May 2026, with broad sector participation suggesting the market was pricing in a structural demand shift rather than company-specific catalysts.

The key infrastructure demand drivers behind the AI agent thesis include:

Dennis Li, Associate Portfolio Manager at Morningstar Investment Management, framed the rally’s logic in 12 May 2026 commentary: the market is pricing AI agent infrastructure as a multi-year hardware upgrade cycle in which each successive generation of models requires substantially more compute and memory.

Training-phase AI workloads are intensive but episodic. A large language model trains over weeks or months, consuming vast GPU clusters, then releases that capacity once training completes. Agent-phase workloads operate differently. An AI agent that monitors, decides, and acts on behalf of a user or enterprise requires persistent compute, always running, always drawing on memory.

This distinction matters for semiconductor revenue duration. Training demand creates lumpy, project-based purchasing cycles. Agent demand, if it scales as proponents expect, creates recurring infrastructure consumption closer to a utility model. That is why the market repriced chipmakers higher: the demand story shifted from cyclical to structural.

Morningstar Investment Management was explicit. Dennis Li stated in the firm’s 12 May 2026 commentary that semiconductor stocks are not particularly attractive at current valuations. The concern is not that AI lacks potential; it is that two specific uncertainties sit upstream of the revenue assumptions already embedded in chip stock prices.

Morningstar Australia has noted a broader valuation reassessment across AI-sensitive sectors, framing the situation plainly: “After a mass downgrade from Morningstar analysts, the question is whether AI is changing the rules of investing.”

The firm identified two core vulnerabilities:

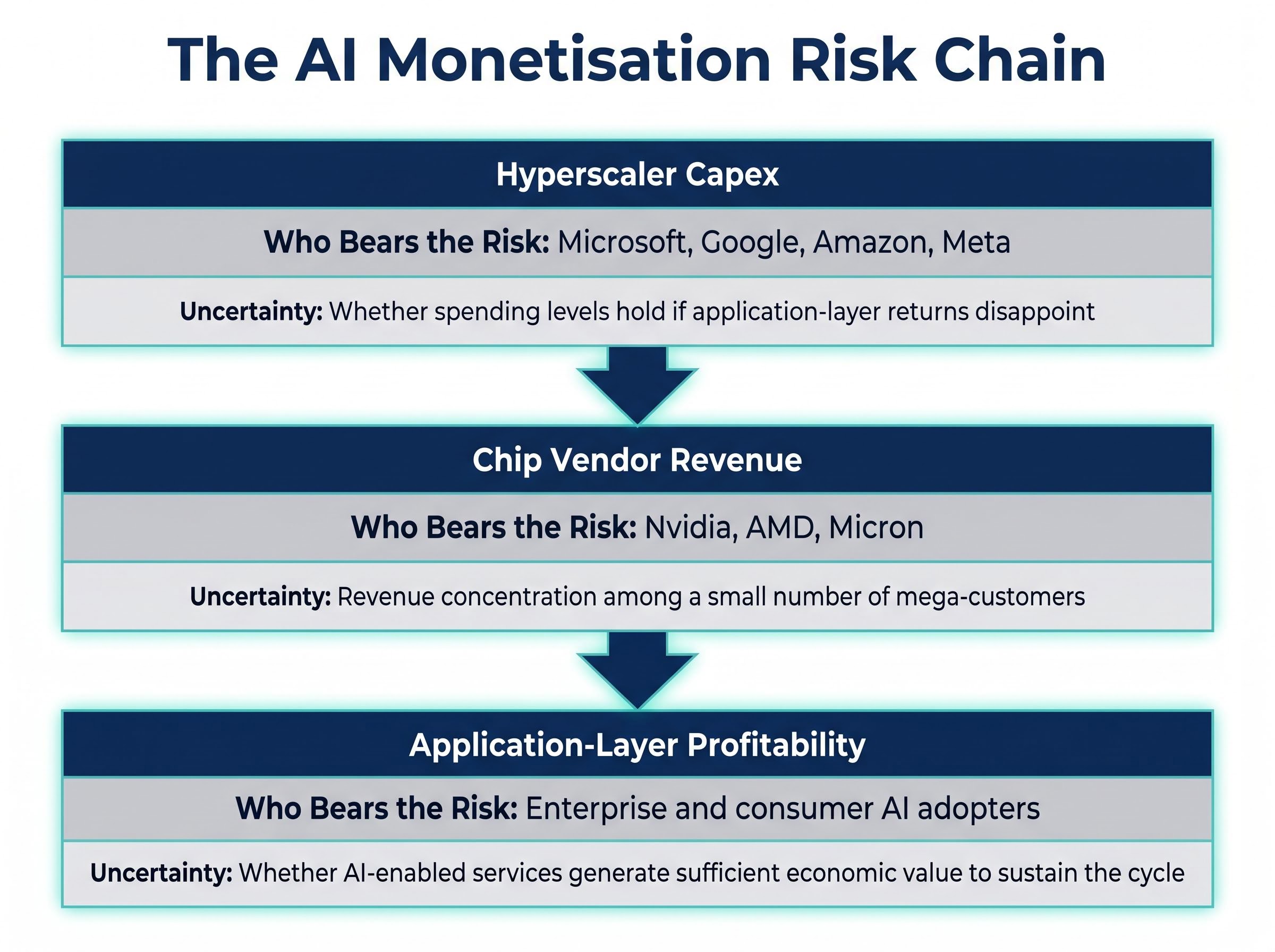

Both uncertainties are structurally upstream of semiconductor revenue. Chip vendors depend on hyperscalers buying hardware. Hyperscalers depend on application-layer companies generating returns from AI. Application-layer companies depend on end users paying for AI-enabled services. If any link in that chain fails to deliver at the pace valuations assume, chipmaker revenue growth faces a ceiling the market has not priced in.

Morningstar’s positioning reinforces the point. The firm currently prefers out-of-favour consumer sectors, including beverages and branded household goods, over elevated-sentiment technology names. That is not contrarianism for its own sake. It reflects a disciplined view that valuation still matters, even when the underlying technology is real.

The bulk of AI capital expenditure originates from four companies: Microsoft, Google, Amazon, and Meta. Their multi-year capex commitments are firm, and management teams have consistently cited AI agents and generative AI services as the rationale for sustained infrastructure spending into 2026 and beyond. On earnings calls, the language has been emphatic.

Hyperscaler capex commitments for 2026 reached approximately $725 billion across Amazon, Microsoft, Alphabet, and Meta combined, with Q1 2026 alone accounting for $130 billion; Microsoft’s annualised AI revenue run rate surpassing $37 billion at 123% year-over-year growth provides the strongest commercially verified case for why those budgets have held.

That emphasis, however, is not the same as proof. The monetisation logic requires a chain of events, and each link carries distinct risk.

| Stage | Who Bears the Risk | Key Uncertainty |

|---|---|---|

| Hyperscaler capex | Microsoft, Google, Amazon, Meta | Whether spending levels hold if application-layer returns disappoint |

| Chip vendor revenue | Nvidia, AMD, Micron | Revenue concentration among a small number of mega-customers |

| Application-layer profitability | Enterprise and consumer AI adopters | Whether AI-enabled services generate sufficient economic value to sustain the cycle |

Nvidia’s data-centre revenue concentration illustrates the risk concretely. A small number of hyperscaler customers account for an outsized share of AI accelerator purchases. Analysts have noted that Nvidia’s gross margins on AI accelerators may represent a peak-cycle phenomenon, supported by tight supply conditions rather than durable competitive positioning alone.

For the current capex cycle to become self-reinforcing, companies deploying AI agents at the application layer must generate measurable returns on that deployment, and those returns must be visible enough to justify hyperscalers maintaining or increasing their infrastructure budgets. If application-layer profitability stalls or arrives more slowly than expected, hyperscaler capex guidance faces downward revision, and chip vendor revenue growth decelerates regardless of how real the underlying technology is.

Historical precedent offers a cautionary reference. Enterprise technology build-outs have repeatedly seen infrastructure spending precede demonstrated application returns by multiple years. The fibre-optic build-out of the late 1990s and early cloud computing infrastructure investments both followed this pattern: real technology, real demand, but a monetisation timeline that lagged the capital deployed to build it.

Semiconductor companies are capital-intensive, cyclical businesses sensitive to inventory and demand cycles in ways that make standard valuation multiples difficult to apply. Chip fabrication requires billions in upfront investment, production lead times stretch across quarters, and demand shifts can move from shortage to oversupply faster than most industries.

The standard semiconductor cycle moves through three broad stages:

Pro-AI commentators argue that traditional cyclical frameworks, including mid-cycle P/E multiples and mean-reversion assumptions, underestimate the structural shift AI workloads represent. Higher sustainable returns on invested capital and faster growth, they contend, justify persistently higher multiples than previous semiconductor cycles warranted.

The counter-argument is familiar from prior technology cycles: the claim that “this time is different” has accompanied every major infrastructure build-out. AI may indeed represent a structural shift rather than a cyclical peak, but historical precedent suggests the burden of proof sits with the bulls, not the bears.

Arm trades at 85x forward P/E and 45x price-to-sales, valuations within the range of dot-com era semiconductor pricing, while the S&P 500 Shiller CAPE sits at approximately 40-41, the second-highest reading in 155 years of data, figures that put the ‘this time is different’ argument under significant historical pressure.

Nvidia’s CUDA developer ecosystem and InfiniBand networking integration provide the strongest case for margin durability. Developer lock-in makes it structurally difficult for large customers to migrate quickly. Against that, in-house chip efforts by Google (TPUs) and Amazon (Trainium) represent margin compression risks over time, as hyperscalers seek to reduce dependence on a single vendor.

Morningstar’s broader framework applies here: AI may change how investors think about semiconductor demand, but valuation discipline still applies.

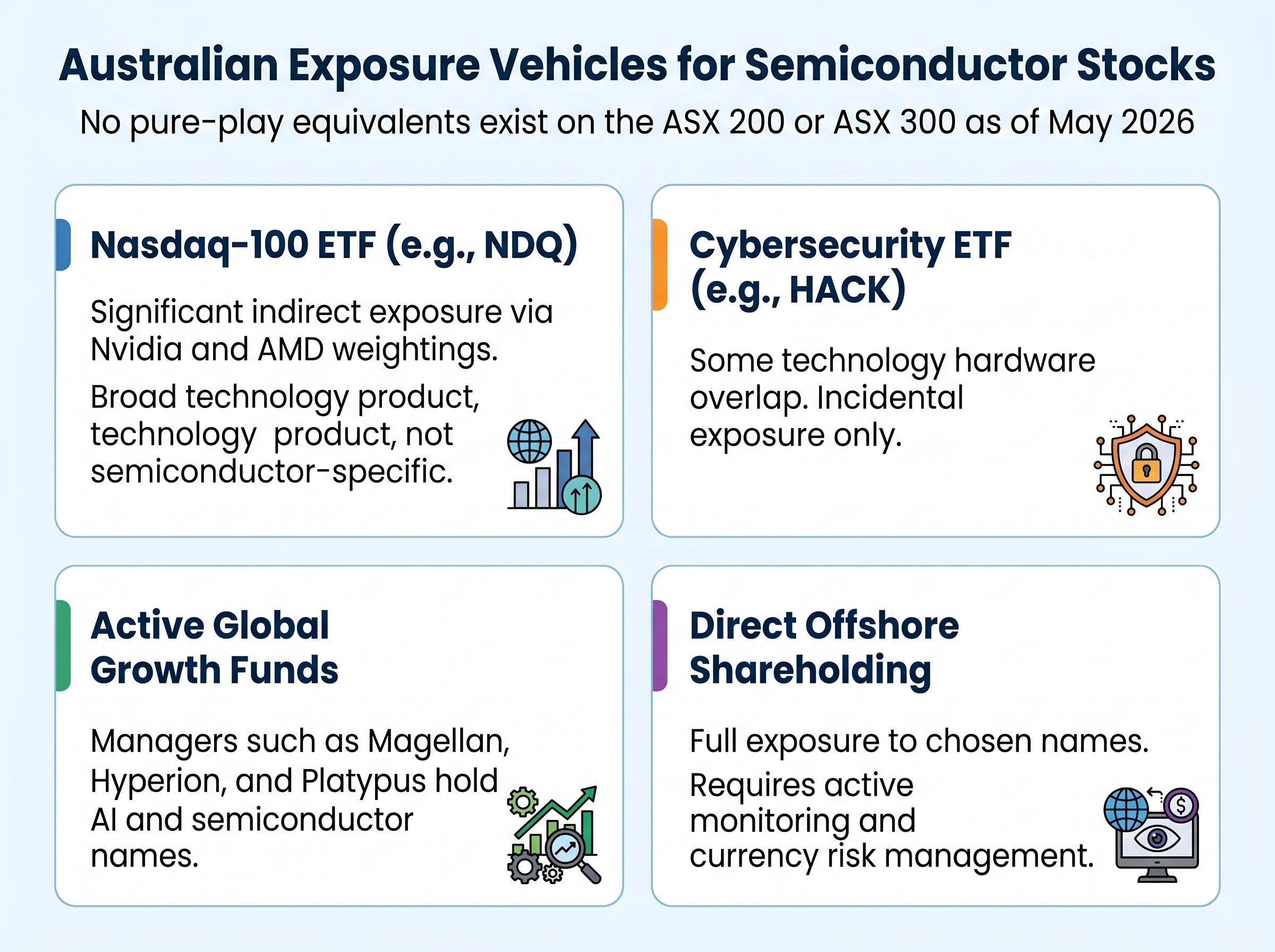

Australian equity indices carry minimal direct semiconductor exposure. The ASX 200 and ASX 300 contain no pure-play equivalent to Nvidia, AMD, or Micron. No pure-play semiconductor ETF exists on the ASX as of May 2026.

Most Australian investors access this theme indirectly, through products they may regard as broadly diversified rather than semiconductor-concentrated.

Domestic technology ETF exposure through vehicles like the BetaShares ATEC fund carries a less obvious composition than its label implies: only 56% of the underlying index constituents are formally classified as technology companies under GICS, with the remainder spread across industrials, communications, and healthcare, a structural characteristic that affects how semiconductor sector corrections transmit into Australian portfolios.

| Exposure Vehicle | Semiconductor Concentration | Key Limitation |

|---|---|---|

| Nasdaq-100 ETF (e.g., NDQ) | Significant indirect exposure via Nvidia and AMD weightings | Broad technology product, not semiconductor-specific |

| Cybersecurity ETF (e.g., HACK) | Some technology hardware overlap | Not semiconductor-focused; incidental exposure only |

| Active global growth funds | Varies; managers such as Magellan, Hyperion, and Platypus hold AI and semiconductor names | Semiconductor risk may not be clearly disclosed in top-10 holdings summaries |

| Direct offshore shareholding | Full exposure to chosen names | Requires active monitoring and currency risk management |

Concentration risk warning: Market-cap-weighted Nasdaq-100 ETFs carry outsized Nvidia weighting. A correction in AI chip valuations would transmit more forcefully into Australian portfolios than investors holding these products as “diversified technology exposure” may expect.

The most actionable insight for Australian investors is that semiconductor valuation risk may already be embedded in products held as part of a diversified allocation, making Morningstar’s caution directly relevant even without deliberate chip-sector positioning.

Rather than prescribing a single answer, the following questions provide a framework Australian investors can apply to their own portfolios immediately:

Morningstar’s contrarian positioning offers a useful reference point. The firm has identified beverages and branded household goods as sectors where valuations reflect overly pessimistic expectations, a stark contrast with the optimism currently embedded in semiconductor prices.

The key swing variables for the remainder of 2026 that should inform ongoing monitoring include:

The two Morningstar uncertainty frames, the productivity timeline and the monetisation conversion, serve as monitoring checkpoints. When evidence emerges that addresses either question with specificity, semiconductor valuations will reprice accordingly. Until then, the gap between narrative and proof remains the defining feature of this rally.

The structural case for AI-driven semiconductor demand is credible. AI agents represent a genuine shift in compute requirements, hyperscaler commitments are firm, and the supply constraints supporting current pricing are real. Credibility, however, is not the same as current valuations being justified.

Two unresolved questions sit upstream of the revenue assumptions already embedded in chip stock prices: how quickly AI agents deliver measurable productivity improvements, and whether those improvements convert into profitability sufficient to sustain the infrastructure spending cycle. Until both questions find answers in reported financial results rather than earnings call commentary, the rally remains a bet on a timeline the market cannot yet verify.

Australian investors can control one thing: whether they hold that exposure knowingly, with a clear understanding of the conditions under which the thesis holds and the signals that would indicate it is breaking down.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Semiconductor stocks are shares in companies that design and manufacture chips such as GPUs, CPUs, and memory used in computing infrastructure. They are highly sensitive to AI investment cycles because hyperscalers like Microsoft, Google, Amazon, and Meta purchase large volumes of chips to build AI infrastructure, meaning any slowdown in that spending transmits directly into chip vendor revenue.

The rally was driven by a narrative shift within AI from model training toward AI agent deployment, a use case requiring persistent, always-on compute and memory infrastructure rather than episodic bursts. Investors repriced chipmakers higher on the expectation that agent infrastructure would create recurring, utility-like demand rather than lumpy project-based purchasing cycles.

Morningstar Investment Management's Dennis Li stated in May 2026 commentary that semiconductor stocks are not particularly attractive at current valuations because two key uncertainties remain unresolved: how quickly AI agents will deliver measurable productivity improvements at enterprise scale, and whether those improvements will convert into profitability sufficient to sustain hyperscaler infrastructure spending.

Australian investors gain indirect exposure through Nasdaq-100 ETFs, active global growth funds from managers such as Magellan, Hyperion, and Platypus, and domestic technology ETFs, with market-cap-weighted products carrying significant Nvidia weighting that can transmit a chip sector correction more forcefully than investors holding them as diversified technology exposure may expect.

Investors should track hyperscaler capex guidance revisions during upcoming earnings cycles, competitive dynamics between Nvidia and alternatives including AMD, Google TPUs, and Amazon Trainium, HBM and advanced packaging supply trajectories, and US export control developments affecting AI chip sales to China, as these variables will determine whether the monetisation chain that underpins current semiconductor valuations holds.