How a Medtech Stock Beat Every Miner on the ASX 200 in FY2026

1 hr ago

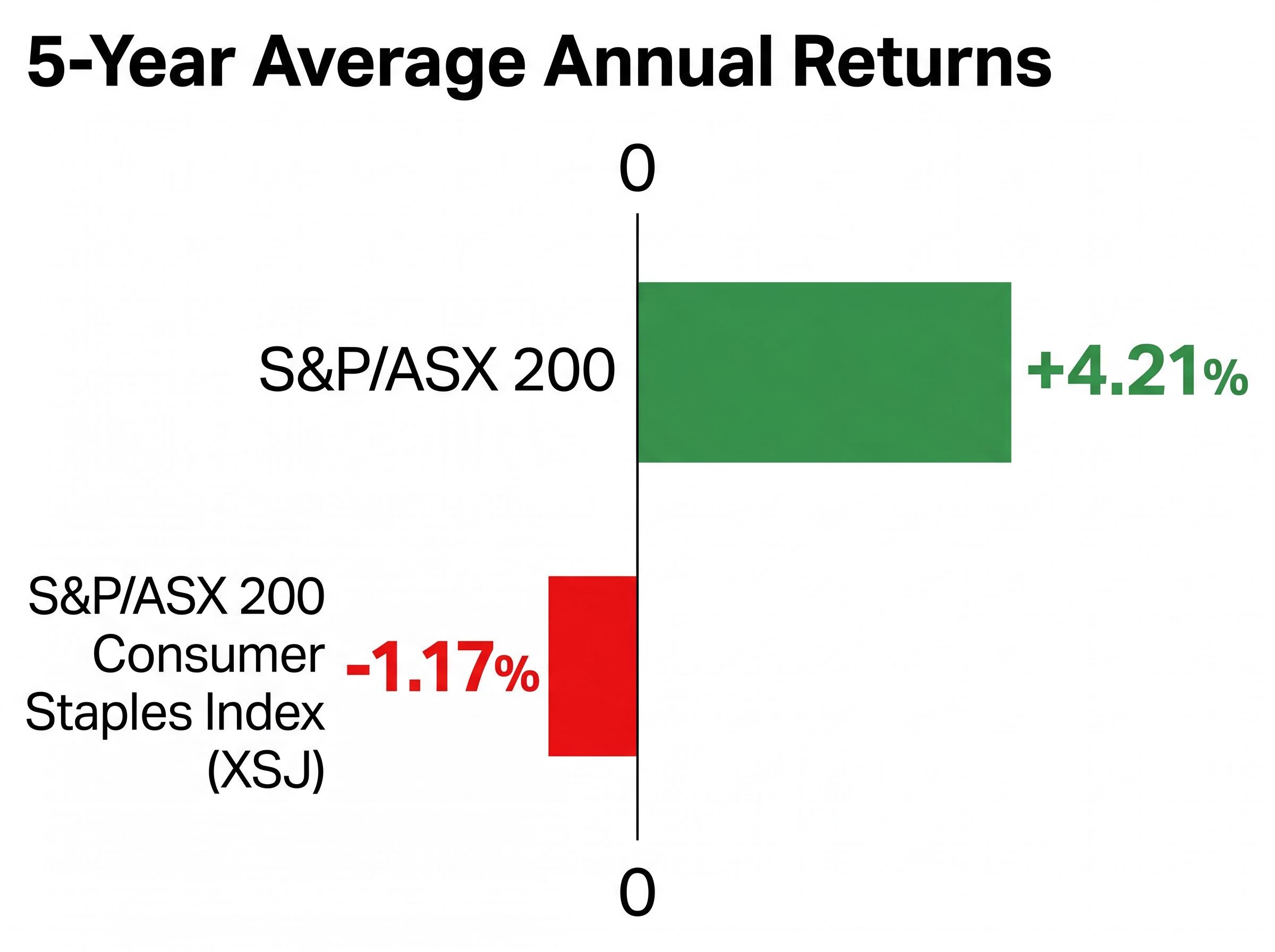

The S&P/ASX 200 Consumer Staples Index has delivered average annual returns of -1.17% over five years. Over the same period, the broader ASX 200 returned +4.21% per year. Investors holding the sector have not simply missed the market; they have gone backwards in real terms, with inflation compounding the damage.

Consumer staples has long occupied the role of the reliable, unexciting anchor in an Australian equity portfolio. Woolworths and Coles are household names. Grocery demand does not disappear in a recession. The dividend cheques keep arriving. Yet the five-year return record directly challenges that narrative, and mid-2026 brings a fresh set of questions about whether the calculus is finally shifting. What follows is a diagnosis of why the sector has underperformed so persistently, an examination of the structural forces holding it back, and a framework for determining when owning ASX consumer staples still makes sense in a diversified portfolio.

The gap is not subtle. Over five years, the S&P/ASX 200 Consumer Staples Index (XSJ) has returned an average of -1.17% annually, while the ASX 200 delivered +4.21% per year. That is a cumulative shortfall measured in thousands of dollars for any investor with meaningful sector exposure.

-1.17% average annual return for the XSJ, versus +4.21% for the ASX 200 over five years.

The calendar 2025 result confirmed this was no one-year anomaly. XSJ posted a price return of just +1.43%, ranking 8th of the 11 ASX 200 sectors. The Materials sector, by comparison, gained +31.71% in the same year, illustrating the opportunity cost of parking capital in defensives at the wrong point in a cycle.

The sector rotation away from consumer-facing names into materials and commodities was not abstract in 2025: three lithium stocks, Liontown Resources, Pilbara Minerals, and Mineral Resources, dominated the list of new 52-week highs in the same week that consumer and health care names filled the annual lows list, illustrating in real time the opportunity cost that XSJ holders absorbed.

The year-to-date 2026 picture, as at 13 May 2026, introduces a partial counterpoint. XSJ has returned +1.7%, compared with a near-flat +0.064% for the ASX 200. The sector is outperforming, but from a low base, and over a short window.

| Index / Sector | 5-Year Avg Annual Return | Calendar 2025 Return | YTD 2026 (13 May) |

|---|---|---|---|

| XSJ (Consumer Staples) | -1.17% | +1.43% | +1.7% |

| S&P/ASX 200 | +4.21% | ~+10.2% (FY2025) | +0.064% |

| Materials | N/A | +31.71% | N/A |

The numbers leave little room for reassuring interpretation. The sector has delivered negative real returns over a full market cycle, and even its best recent stretch barely registers against what other sectors have produced.

Consumer staples companies produce or retail goods that households purchase regardless of economic conditions. In Australia, the sector is dominated by supermarket operators, food manufacturers, and animal nutrition businesses. The XSJ index carried a total market capitalisation of AU$93.5 billion as at 13 May 2026, generating AU$170.8 billion in revenue and AU$2.1 billion in earnings.

Three structural characteristics have historically underpinned the sector’s appeal to investors:

These characteristics explain why the sector trades at undemanding multiples: a PE ratio of 14.6x and a price-to-sales ratio of 0.5x as at 13 May 2026. The market is not pricing consumer staples for earnings growth. It is pricing them for stability and income.

The sector’s long-run total return case rests more heavily on dividends than on capital gains. Investors who own staples typically do so for the income stream, accepting lower growth in exchange for consistency.

Not every constituent fits this profile, however. A2 Milk (ASX: A2M), classified within the sector, has delivered an average dividend yield of just 0.28% over five years and recorded a -31% price decline from the start of 2025 to May 2026. It serves as a reminder that sector-level generalisations do not apply uniformly across all constituents.

The underperformance has not been caused by a single event. It reflects a layered set of pressures that have compounded over several years, each reinforcing the others.

Three headwind categories have dominated:

The ACCC Supermarkets Inquiry 2024-25, which delivered its final report in March 2025, examined supermarket pricing practices at WOW and COL in detail, providing the formal regulatory basis for the ongoing headline risk that has weighed on investor sentiment toward both companies.

The XSJ index is heavily weighted toward two supermarket chains, which amplifies regulatory risk relative to global staples benchmarks.

The RBA cash rate, unchanged at 4.35% since November 2023, has sustained mortgage repayment pressure on Australian households, feeding the trading-down behaviour that compresses supermarket margins.

This is not an exclusively Australian story. US consumer staples underperformed the S&P 500 in 2025 for related but distinct reasons: AI-driven capital flows drew investment away from defensives, and concerns about GLP-1 weight-loss drugs raised questions about long-term demand for certain food categories. The global pattern suggests a broad rotation away from defensive sectors rather than a problem unique to the Australian market.

The Australian version of the problem, however, is amplified by concentration. The XSJ index is dominated by WOW and COL, meaning the regulatory, margin, and competitive pressures facing those two companies flow directly into index-level returns in a way that more diversified global staples indices can absorb.

In April 2026, on a session where the ASX 200 fell 92 points, consumer staples advanced nearly 2%, making them the best-performing sector on the exchange that day.

On a single April 2026 session, staples gained nearly 2% while the ASX 200 dropped 92 points.

That episode captures, in miniature, the entire case for holding staples in a diversified portfolio. The sector’s value is not measured in average annual returns during bull markets. It is measured in what it does on the days everything else falls. Owning an asset that moves in the opposite direction to the rest of a portfolio during selloffs reduces overall volatility, even if it drags on returns during periods of broad market strength.

Defensive positioning in 2026 carries an additional complication that has undermined even conventional safe havens: supply-driven stagflation causes bonds and equities to fall together, meaning the traditional role of defensive equity sectors as portfolio anchors is being tested by a macro environment where the standard diversification logic has broken down.

The year-to-date 2026 data supports this framing. XSJ has returned +1.7% versus the ASX 200’s +0.064% as at 13 May 2026, a period of relatively muted broader market performance where defensives have quietly outperformed.

Three conditions could shift consumer staples from laggard to outperformer in 2026. RBA rate cuts, widely expected but not yet delivered, would ease household mortgage pressure and support consumer spending. Fiscal support targeting middle-income households could provide a further tailwind. And rotation from growth sectors, as their valuations compress after several years of dominance, could redirect capital toward neglected defensives.

Fidelity’s global 2026 outlook identifies a more favourable environment for consumer staples, driven by rate easing, fiscal support, and mean-reversion potential from compressed valuations. Australian commentators, including Talking Wealth and Motley Fool AU, have positioned the sector as “forgotten” and due for rotation attention.

These are theses, not confirmed outcomes. The timing of RBA rate cuts remains uncertain, and there is no guarantee that growth-sector valuations will compress on a timeline that benefits staples. The setup is more constructive than it has been, but that is a relative statement, not a prediction.

The index-level underperformance conceals meaningful dispersion among individual constituents. The XSJ is heavily weighted toward the supermarket duopoly of WOW and COL, meaning their margin and regulatory headwinds dominate index returns. Smaller names, with different business models and risk profiles, have delivered very different outcomes.

Key distinctions between the large-cap index heavyweights and smaller constituents:

Two names illustrate the opportunity.

Inghams Group (ASX: ING) has declined approximately 55% over the year to May 2026, yet carries a grossed-up dividend yield estimated at 6.1%-7.1%. The TradingView consensus price target sits at approximately AU$2.23, compared with a recent price near AU$1.82, implying roughly 22% potential upside.

Ridley Corporation (ASX: RIC) reported FY25 EBITDA of AU$97.8 million, up 8.6% year-on-year. Its one-year price change to May 2026 stands at approximately +16.67%, with a consensus price target of AU$3.30 from a recent price near AU$2.67, implying roughly 23% potential upside.

A2 Milk (ASX: A2M), by contrast, trades at a price-to-sales ratio of 3.65x versus a five-year average of 3.44x. Despite a -31% price decline from the start of 2025, it is not obviously cheap on fundamentals, a reminder that not every beaten-down staples name represents value.

Applying multiple share valuation methods matters particularly when assessing beaten-down names like Inghams and Ridley: a low price-to-sales ratio can create an illusion of cheapness while masking debt levels and margin compression, and anchoring to a single metric, whether dividend yield, consensus price target, or EV/EBITDA, risks a conviction error that a structured multi-method approach would surface.

| Company | 1-Year Price Change | Forward Yield | Consensus Target | Implied Upside |

|---|---|---|---|---|

| Inghams (ING) | ~-55% | ~6.1%-7.1% (grossed-up) | AU$2.23 | ~22% |

| Ridley (RIC) | ~+16.67% | N/A | AU$3.30 | ~23% |

| A2 Milk (A2M) | ~-31% (from start 2025) | ~0.28% (5-yr avg) | N/A | Modest premium to historical PS |

The dispersion makes the sector-level verdict incomplete. Investors who dismiss the sector entirely may be overlooking specific names where company-level fundamentals diverge sharply from the index-level story.

The sector has delivered negative real returns over five years. That is the established fact, and it cannot be argued away. The productive question is not whether consumer staples has underperformed; it is whether the sector still serves a portfolio purpose and under what conditions.

Two legitimate uses remain. Consumer staples exposure can reduce overall portfolio volatility through defensive ballast, the kind of protection demonstrated in the April 2026 episode. And selective exposure to high-yielding names trading below assessed fair value can provide income generation that the broader index does not capture.

The conditions under which adding or maintaining staples exposure is most justified:

Owning the XSJ via a passive ETF means accepting the index’s heavy concentration in the supermarket duopoly, along with all of the cost, competitive, and regulatory pressures those companies face. Selective exposure to individual names such as Inghams or Ridley allows investors to access the sector’s income and value characteristics without the same concentration risk. Neither approach is inherently superior; the choice is a risk-calibration decision tied to portfolio size, conviction, and tolerance for single-stock exposure.

Investors seeking defensive characteristics without committing to the XSJ’s concentrated supermarket exposure have an alternative pathway in quality factor investing, which screens for high return on equity, low financial leverage, and stable earnings growth rather than sector classification, and which outperformed the MSCI World ex Australia Index by 105 basis points in November 2025 precisely during a period of elevated market stress.

The sector trades at a PE of 14.6x and price-to-sales of 0.5x, multiples that are not pricing in meaningful disappointment and offer some downside support. The mean-reversion thesis for 2026, shared by Fidelity globally and several Australian commentators, provides a reason to review the sector rather than dismiss it, without overstating certainty about timing or magnitude.

The five-year return of -1.17% annually versus +4.21% for the ASX 200 has real compounding costs. Investors who need capital appreciation to meet financial goals should be clear-eyed about what consumer staples can and cannot deliver. The sector is not uninvestable. It is, however, a deliberate portfolio construction choice, not a default one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The ASX consumer staples sector covers companies that produce or retail goods households purchase regardless of economic conditions, including supermarket operators Woolworths and Coles, food manufacturers, and animal nutrition businesses. The sector is tracked by the S&P/ASX 200 Consumer Staples Index (XSJ), which had a total market capitalisation of AU$93.5 billion as at 13 May 2026.

The sector has faced a combination of sustained cost inflation squeezing operating margins, household trading-down behaviour shifting spending toward private-label and discount competitors, and ongoing regulatory scrutiny of supermarket pricing practices by the ACCC. The index is also heavily concentrated in Woolworths and Coles, meaning those two companies' specific headwinds dominate index-level returns.

Three key conditions could support a shift: RBA interest rate cuts easing household mortgage pressure, fiscal support targeting middle-income consumers, and rotation from growth sectors as their valuations compress after years of dominance. These remain theses rather than confirmed outcomes, and the timing of RBA cuts is still uncertain.

There is significant dispersion within the sector. Ridley Corporation (ASX: RIC) posted approximately +16.67% price growth over one year to May 2026 with a consensus target implying around 23% further upside, while Inghams Group (ASX: ING) declined roughly 55% but carries a grossed-up dividend yield estimated at 6.1%-7.1%. A2 Milk, despite a -31% price fall, does not appear obviously cheap on a price-to-sales basis.

Consumer staples can still provide two legitimate portfolio functions: reducing overall volatility through defensive ballast, as demonstrated in April 2026 when the sector gained nearly 2% on a day the ASX 200 fell 92 points, and generating income through selective exposure to high-yielding names trading below assessed fair value. The sector is most appropriate when capital preservation is a priority or when a portfolio is already heavily concentrated in growth or cyclical sectors.