Why Your ETF Portfolio May Be Less Diversified Than You Think

9 mins ago

Australia’s 50% capital gains tax discount, a fixture of the tax system since 1999, is set to disappear. The 2026-27 Federal Budget announced its replacement with a system most investors have never encountered: inflation indexation paired with a 30% minimum tax floor on real capital gains, effective 1 July 2027. The change represents the most significant structural reform to Australia’s CGT framework in nearly three decades, yet clear explanations of how the new system actually works remain scarce. This article sets out the core mechanics of both systems side by side, explains how inflation levels directly shape outcomes under the new rules, details what transitional arrangements mean for gains already accrued, identifies who is most exposed, and outlines the record-keeping shift that lies ahead. The goal is a working understanding of the reform before it takes effect.

The government’s stated rationale centres on a specific problem: the current 50% discount taxes nominal gains rather than real gains, which Treasury argues was never the original intent of the CGT system. Under the existing rules, an investor who holds an asset for more than 12 months pays tax on only half the nominal gain, regardless of how much of that gain was simply inflation eroding the value of money.

“The Government will replace the 50 per cent Capital Gains Tax (CGT) discount with a discount based on inflation and introduce a minimum 30 per cent tax on gains from 1 July 2027.”

— Budget 2026-27 Tax Reform page, Australian Government, Department of the Treasury, May 2026

The reform is not without historical precedent. Before 1999, Australia operated an indexation-based CGT system. The flat 50% discount replaced it. What the Budget proposes is, in structural terms, a return to that older approach, with one significant addition: a 30% minimum tax on real gains that did not exist in the pre-1999 framework.

The Budget announcement that saw the CGT discount abolished on 12 May 2026 also introduced a 30% minimum tax on net capital gains above $20,000 for individuals, a threshold detail that did not appear prominently in the original Treasury release but carries meaningful implications for investors close to that gain level.

The Australian Treasury Budget 2026-27 tax factsheet confirms that the replacement of the 50% discount with cost base indexation and a 30% minimum tax rate on capital gains applies from 1 July 2027, and that the reform is intended to ensure investors pay tax only on real gains rather than nominal ones.

This is a philosophical shift, not a technical tweak. And it carries a qualification that matters: as at mid-May 2026, the reform remains announced Budget policy. No draft Bill, no ATO technical guidance, and no Treasury exposure draft have been released. The measures will require legislation before they take effect on 1 July 2027.

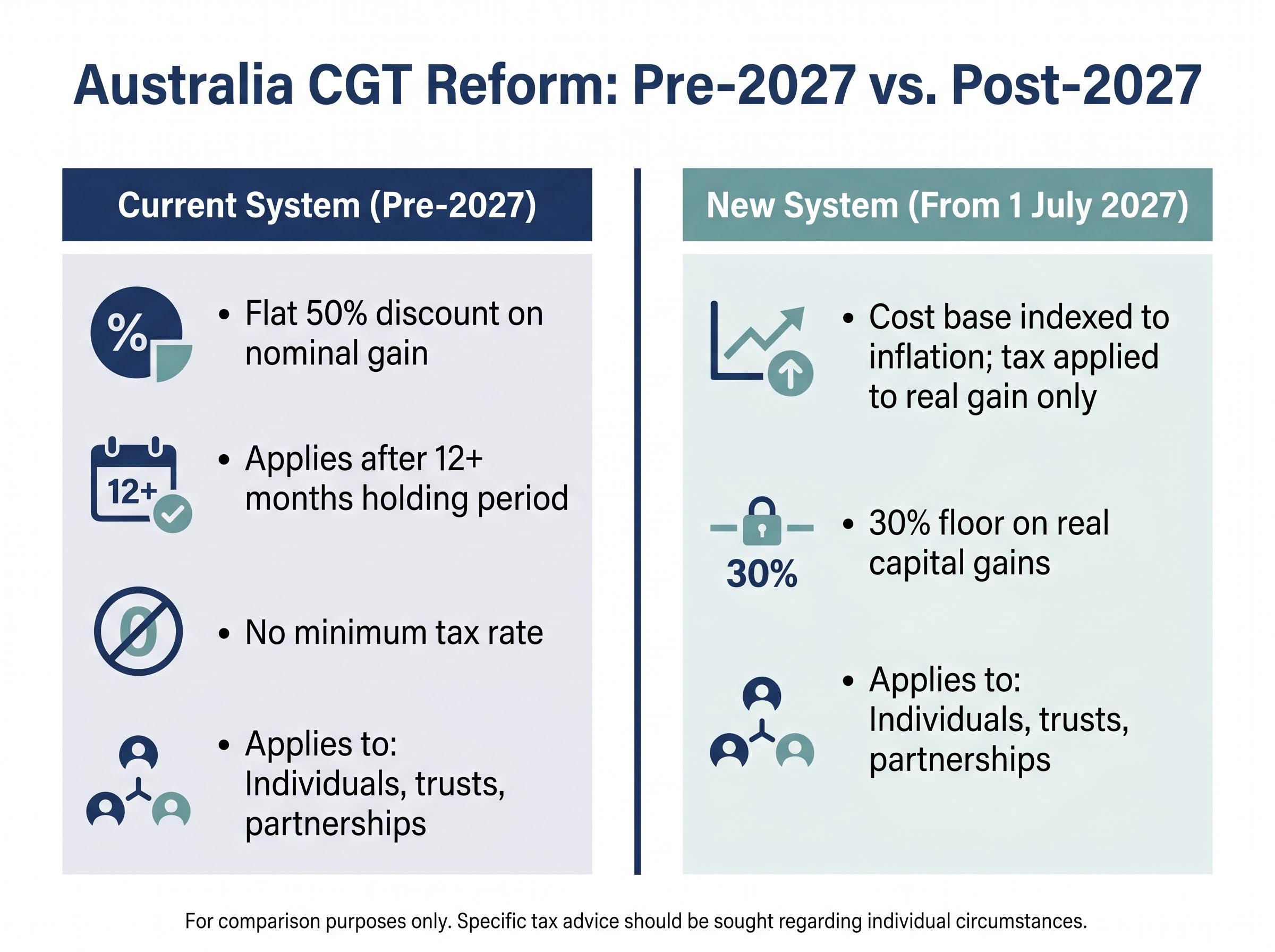

Under the outgoing system, the calculation is straightforward. An individual, trust, or partnership that holds a CGT asset for more than 12 months applies a flat 50% discount to the nominal gain. Half the gain is taxable; half is not. Inflation plays no role in the calculation. Whether consumer prices rose 1% or 5% a year during the holding period, the discount is the same.

The replacement system works differently. From 1 July 2027, the asset’s cost base is adjusted upward by inflation before the taxable gain is calculated. Only the real, above-inflation gain is subject to tax. As the Budget documentation frames it, the reform aims to ensure investors “will only pay tax on their real capital gain, restoring the original intent of the CGT arrangements.”

Sitting on top of the indexation mechanism is the 30% minimum tax floor. Regardless of an investor’s marginal tax rate, the effective CGT rate on the real gain cannot fall below 30%. This floor is the feature that prevents the new system from being straightforwardly more generous than the old one.

The reform applies broadly. According to Clayton Utz, it covers “all CGT assets held by individuals, trusts and partnerships,” including shares, ETFs, investment property, and business assets, not only residential property.

| Feature | Current system (pre-2027) | New system (from 1 July 2027) |

|---|---|---|

| How the taxable gain is calculated | Flat 50% discount on nominal gain | Cost base indexed to inflation; tax applied to real gain only |

| Asset classes covered | All CGT assets held 12+ months | All CGT assets held by individuals, trusts, partnerships |

| Minimum tax rate | None (taxed at investor’s marginal rate on discounted gain) | 30% floor on real capital gains |

| Who it applies to | Individuals, trusts, partnerships | Individuals, trusts, partnerships |

The headline promise of the new system sounds reassuring: investors will only pay tax on real gains. In practice, the outcome depends almost entirely on one variable that no investor controls: inflation.

Two scenarios illustrate how sharply the results can diverge.

Clayton Utz notes that the 30% minimum tax “will mean that, for some investors, effective tax rates will rise compared with the current 50%-discount system, especially when inflation is low and real gains make up a larger share of nominal gains.”

The compounding effect over time amplifies this divergence. Modelling across 10, 20, and 30-year investment horizons, as analysis from Stockspot illustrates, shows that even modest annual differences in inflation produce materially different after-tax outcomes.

Concrete modelling of after-tax wealth outcomes across different holding periods shows that the compounding effect of the new rules is non-linear: a $100,000 ETF portfolio growing at 8% annually could accumulate approximately $26,000 less over a decade under the new regime compared with the 50% discount, a gap that widens substantially at the 20-year and 30-year horizons.

Current inflation provides useful context. According to the Australian Bureau of Statistics, annual CPI inflation was 4.6% in the 12 months to March 2026. At that level, indexation relief is meaningful. Should inflation moderate toward 2% or below in coming years, the calculus shifts materially against investors who rely on indexation to offset the 30% floor.

The ABS Consumer Price Index data to March 2026 recorded annual CPI inflation at 4.6%, a level at which indexation relief under the new system would be meaningful, though any moderation toward the 2% target band in coming years would reduce that relief substantially.

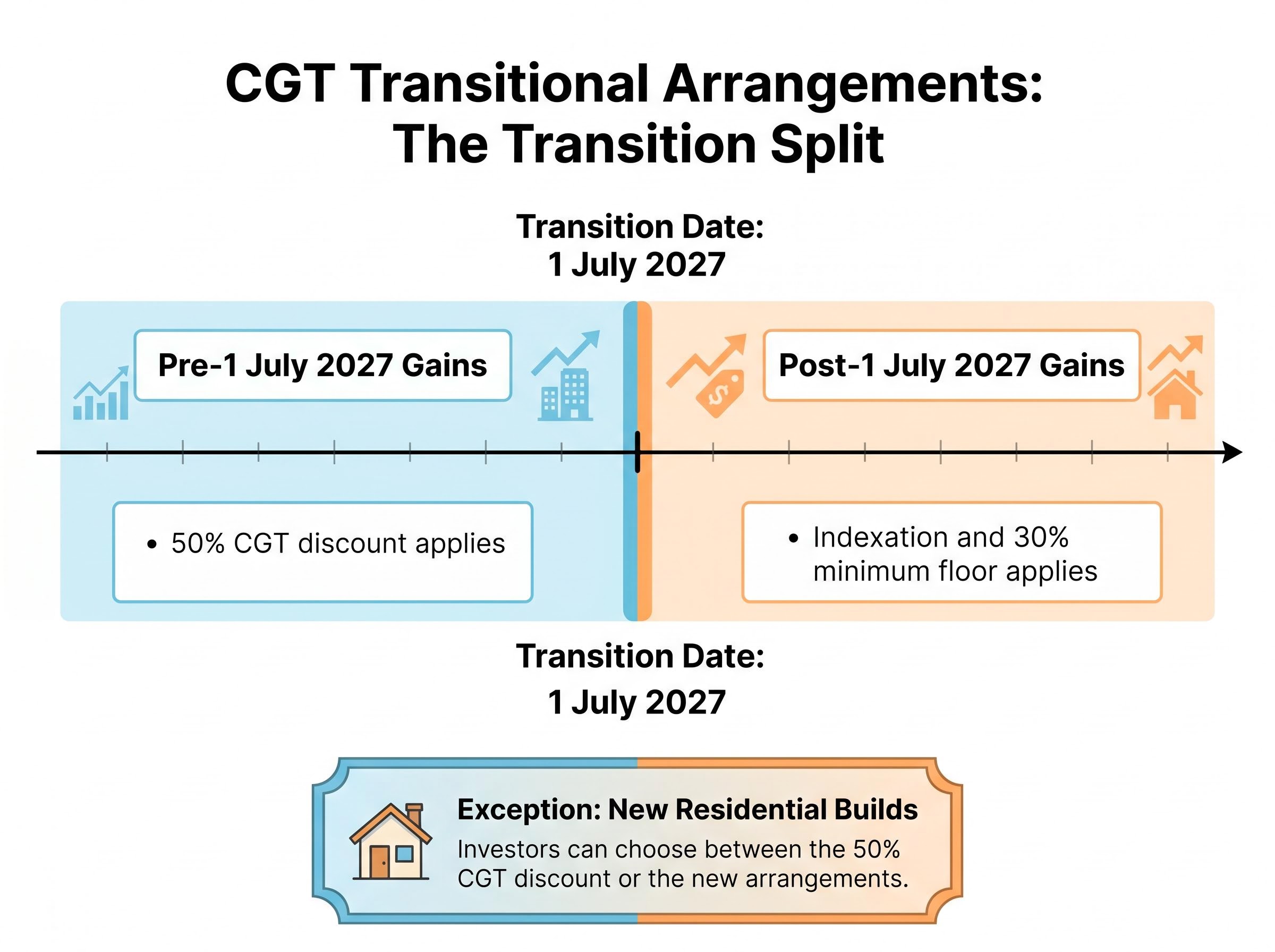

Most investors considering this reform are not starting from zero. They hold assets purchased months, years, or decades ago, with unrealised gains already accumulated under the existing rules. The transitional framework determines how those gains are treated.

The core principle is confirmed in Budget documentation: the CGT reforms apply only to gains arising after 1 July 2027. For assets held across the transition date, Clayton Utz provides the clearest available description of how the split works:

While the principle of splitting gains at 1 July 2027 is established, the precise methodology for doing so has not been published. No draft Bill, ATO technical guidance, or Treasury exposure draft on CGT reform had been released as at mid-May 2026.

One significant detail the Budget documentation introduces but the transitional framework discussion often overlooks is the end of the pre-1985 CGT exemption: assets acquired before 19 September 1985 will enter the CGT net from 1 July 2027 using a deemed cost base equal to market value on the transition date, creating a valuation exposure that is acute for holders of long-held family properties and rural land.

The practical questions are significant. How will the pre-2027 and post-2027 portions of a gain be calculated in practice? Will market valuations at the transition date be required? Will investors have election options? These details remain to be legislated, and investors should monitor Treasury and ATO releases as the reform moves through the parliamentary process.

For any investor holding assets with unrealised gains, the transitional rules are not an abstract policy detail. They determine the actual split of tax treatment when those assets are eventually sold.

The reform does not affect all investors equally. The gap between winners and losers under the new system is wide enough that locating oneself in the picture matters.

Clayton Utz specifically highlights “high-net-worth individuals and family investment structures” who have relied on the 50% discount and discretionary trusts as the most exposed group. Long-term share, ETF, and property investors on higher marginal tax rates face a structural increase in effective CGT rates, particularly in low-inflation environments where indexation provides limited relief.

Established property investors are doubly affected. They lose the full 50% CGT discount and, separately, face new negative gearing restrictions on established properties from 1 July 2027. Stockspot notes that startup founders and business owners face heightened exposure because long-term financial returns are often concentrated in a single capital gain event at the time of business sale.

At the other end of the spectrum, lower-income investors whose marginal tax rate is already at or near 30% may see limited change, since their effective rate under the current system was already close to the new floor. Clayton Utz commentary (published 14 May 2026) states that income support recipients, including Age Pensioners, are explicitly exempt from the 30% minimum tax on real capital gains, though this exemption does not appear in official Budget documentation.

The treatment of complying superannuation funds under the new rules has not been confirmed in publicly available Budget or ATO materials as at mid-May 2026.

| Investor profile | Likely impact under new rules | Key reason |

|---|---|---|

| High-income share/ETF investor | Higher effective CGT rate likely | Loss of 50% discount; 30% floor bites in low-inflation periods |

| Established property investor | Significant increase in tax burden | Loss of 50% discount combined with negative gearing restrictions |

| Business owner/startup founder | Heightened exposure on exit events | Returns concentrated in a single capital gain at sale |

| Lower-income investor (marginal rate near 30%) | Limited material change | Effective rate under current system already near the new floor |

| Income support recipient/Age Pensioner | Protected (exempt from 30% minimum) | Explicit exemption per Clayton Utz commentary |

| Superannuation fund investor | Uncertain | Treatment not confirmed in Budget or ATO materials |

Under the outgoing system, the CGT calculation for most individual investors was simple: hold an asset for more than 12 months, apply the 50% discount, and pay tax on half the nominal gain. The arithmetic could fit on the back of an envelope.

The new system demands more. Investors will need to track the indexed cost base of each asset over the full holding period, source reliable inflation data for each year, and check the outcome against the 30% minimum floor. Clayton Utz identifies three specific compliance burdens: tracking indexed cost bases over time, apportioning gains between pre- and post-reform periods, and checking outcomes against the 30% minimum tax rate.

For assets held across the 1 July 2027 transition date, the complexity compounds. Each sale requires a split calculation: the pre-2027 gain portion under old rules, and the post-2027 portion under new rules.

No ATO guidance or detailed compliance manual from professional bodies had been published as at mid-May 2026. The final legislation may refine the mechanics. Regardless of how the final rules are written, certain foundational records will be needed:

Latitude Accountants notes that individual investors will likely need more detailed records of acquisition costs and dates, access to reliable inflation data for indexation, and professional advice when selling assets held across the transition date. The reform is widely expected to increase reliance on tax agents, accounting software, and professional advisers, particularly for investors managing portfolios across multiple assets, brokers, or structures.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The new CGT framework targets a genuine equity problem. Taxing inflationary gains as if they were real returns was a structural flaw in the 50% discount model. In that narrow sense, indexation is fairer: it distinguishes between wealth that was created and wealth that was merely nominal.

That fairness carries a cost. The 30% minimum floor means the system is not purely generous to investors. The increased administrative complexity means the simplicity of the old framework is gone. And the outcomes are not fixed; they move with inflation, holding period, and marginal tax rate in ways that the flat 50% discount never did. Forward planning under the new system is inherently more demanding.

The reform remains announced policy, not yet law. The window before 1 July 2027 is the period for investors to seek professional tax advice, review holding structures, and begin building the records that will be needed when the new rules take effect.

Investors who want to move from understanding the reform to acting on it will find our comprehensive walkthrough of CGT planning strategies before 2027 covers low-turnover ETF structuring, superannuation contribution capacity, buy-only rebalancing, and a worked example showing how the terminal wealth gap exceeds $100,000 over a 30-year horizon at common portfolio sizes.

One consideration is worth holding onto through the noise: diversification, investment discipline, and long-term compounding remain the fundamentals of sound investing. Reacting to tax changes by making poorly considered structural decisions, rushing to sell assets or restructuring portfolios without professional guidance, is itself a risk. The rules are changing. The principles of disciplined investing are not.

These statements reflect announced government policy as at May 2026. The measures are subject to change based on the legislative process and further regulatory guidance. Past performance does not guarantee future results.

From 1 July 2027, Australia's 50% capital gains tax discount will be replaced with a system that indexes the cost base of assets to inflation, meaning only the real gain above inflation is taxable, and a 30% minimum tax floor will apply to those real gains regardless of the investor's marginal tax rate.

For assets held across the 1 July 2027 transition date, the existing 50% CGT discount continues to apply to the portion of any gain accrued up to that date, while only gains accruing from 1 July 2027 onward are subject to the new indexation and 30% minimum tax rules.

High-income investors holding shares, ETFs, or investment property, established property investors who also face new negative gearing restrictions, and business owners or startup founders realising a single large capital gain at the time of sale are identified as the most exposed groups under the new rules.

Investors will need to maintain acquisition dates and cost bases for every CGT asset, records of any capital improvements and transaction costs, and holding period details relative to the 1 July 2027 transition date, as the indexed cost base calculation will be required for every future disposal.

Higher inflation increases the indexed cost base adjustment, reducing the taxable real gain and potentially making the new system comparable to or lighter than the old 50% discount; in low-inflation environments, however, the cost base barely moves, exposing a larger share of the nominal gain to the 30% minimum tax floor.