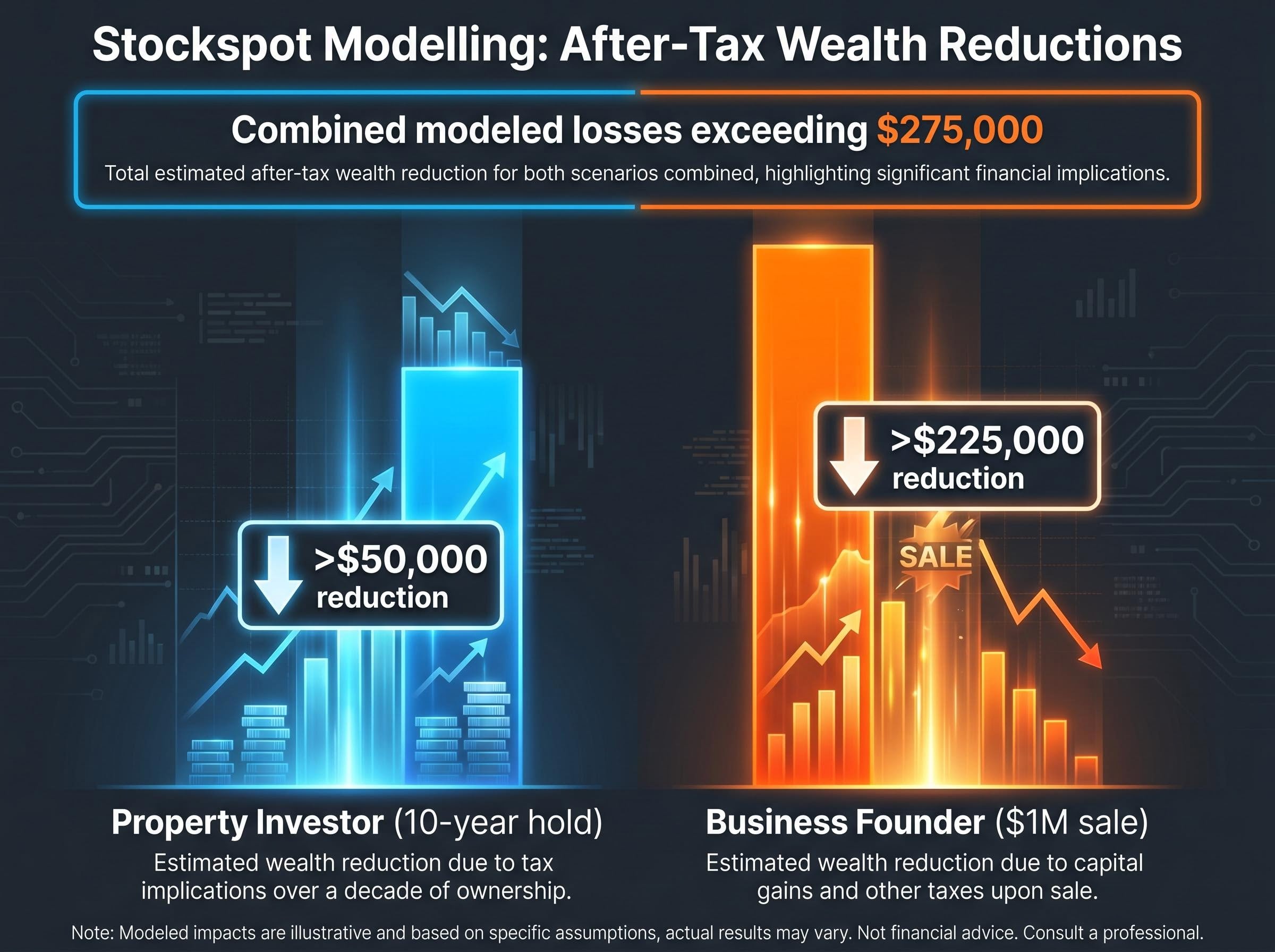

A landlord purchasing an existing investment property after Budget night and a founder selling a private company they built over a decade face combined after-tax losses exceeding $275,000 under scenarios modelled from the same reform package. Both figures stem from the 2026-27 Federal Budget, delivered on 12 May 2026, which paired two structural investment tax changes into a single announcement framed as improving economic fairness. The first restricts negative gearing to new residential builds from 1 July 2027. The second replaces the longstanding 50% capital gains tax (CGT) discount with cost-base indexation and a 30% minimum effective tax rate on real gains. For exchange-traded fund holders, the impact is measurable but diffuse. For property investors carrying leveraged positions and business owners approaching a sale, the arithmetic is immediate. What follows models the dollar cost for each, surfaces the unresolved policy contradiction between encouraging entrepreneurship and taxing its upside more heavily, and assesses what the combined changes signal for rental supply and Australia’s startup ecosystem.

How the two reforms interact to change investment economics

For more than two decades, the 50% CGT discount functioned as a blunt inflation proxy. Any asset held longer than 12 months received a flat halving of the nominal gain at disposal. In practice, this often overcompensated holders of high-growth assets, particularly detached housing, where nominal appreciation significantly outpaced inflation across much of the 2000s and 2010s. Treasury’s stated rationale for reform targets this overcompensation directly.

The 2026 Federal Budget tax reforms span three distinct pillars, covering capital gains tax, negative gearing, and discretionary trust distributions, with a combined revenue impact estimated at $77 billion over the decade and transition windows that differ across each measure.

The replacement mechanism works differently. Cost-base indexation adjusts the original purchase price by Consumer Price Index (CPI) movement over the holding period. Tax is then calculated only on the real gain, the portion of appreciation that exceeds inflation. In a high-inflation environment, this can be generous. In a low-inflation environment, the adjustment is small and the taxable gain remains large.

The 30% minimum effective rate operates as a floor, not a ceiling. Investors on a 47% marginal rate see a modest reduction in their effective CGT rate. But investors on marginal rates below 30%, including many retirees and part-time workers with investment portfolios, are pulled up to 30% on their real capital gains regardless. This is the design feature that changes the distributional profile of the tax.

| Feature | Old treatment (50% discount) | New treatment (indexation + 30% floor) |

|---|---|---|

| Discount applied | Flat 50% on nominal gain | No discount; cost base indexed by CPI |

| Inflation adjustment | None (discount acts as proxy) | CPI indexation of purchase price |

| Effective rate at 47% marginal | 23.5% | 30% (floor applies) |

| Effective rate at 30% marginal | 15% | 30% (floor pulls rate up) |

Gains attributable to the pre-1 July 2027 period may retain partial access to the 50% discount. Post-commencement gains fall under the new framework. Taxpayers have two options for apportioning the split:

- The ATO’s standard apportionment formula, which uses a time-based pro-rata calculation

- An independent valuation of the asset as at 1 July 2027, establishing a market-value baseline for the split

The choice between these two methods is itself a planning decision that requires professional advice before disposal.

The ATO’s CGT calculation guidance sets out the precise mechanics for applying cost-base indexation and the conditions under which the 50% discount was available, establishing the baseline against which the new 30% floor and CPI indexation framework represents a direct structural change for long-term asset holders.

When big ASX news breaks, our subscribers know first

What the reforms cost a leveraged property investor: a concrete scenario

The scenario starts with a common profile: an investor on a 47% marginal tax rate purchases an existing residential property after 7:30pm AEST on 12 May 2026 (Budget night) and holds for ten years. Under the new rules, this investor faces two distinct cost layers.

The negative gearing loss on existing property

From 1 July 2027, annual interest costs on a non-new-build residential investment can no longer be offset against salary or other income. For an investor carrying a typical loan balance, this removes a cash-flow subsidy that materially supported the economics of leveraged property investment for decades.

Body corporate fees, depreciation, and maintenance deductions remain available. The change targets the net rental loss, the gap between rental income and total holding costs, that investors previously offset against their taxable income from other sources. For existing-property acquisitions made after Budget night, that offset disappears.

The CGT cost at disposal

Layer the capital gains change on top. The calculation follows three steps:

- Annual cash-flow impact: The loss of negative gearing deductibility reduces after-tax returns each year of the holding period, compounding over a decade.

- Accumulated holding-period impact: Over ten years, the foregone deductions and their opportunity cost accumulate into a material wealth difference versus the prior regime.

- Disposal tax: At sale, the investor now pays tax on the real gain at the 30% floor rate rather than on half the nominal gain at their marginal rate. In a low-inflation decade, the indexation adjustment is small, and the gap between the old and new after-tax proceeds widens.

Stockspot modelling projects an after-tax wealth reduction exceeding $50,000 over a ten-year horizon for a property investor scenario under the new framework.

One critical distinction shapes near-term decisions. Properties held before 7:30pm AEST on 12 May 2026 retain full negative gearing deductibility, creating a measurable asset-value bifurcation between grandfathered and post-Budget stock. Meanwhile, investors who purchase newly constructed residential properties after Budget night retain negative gearing eligibility, redirecting the investment calculus toward off-the-plan and new-build markets.

For existing investors weighing whether to hold, sell before 1 July 2027, or pivot to new builds, the dollar-figure difference between these pathways is the central decision variable.

What the reforms cost a business founder selling their company

A property investor’s loss is spread across years of holding costs and a final tax bill. A founder’s loss is compressed into a single transaction: the sale of a business built over years of risk, labour, and forgone income. The emotional and financial stakes are structurally different.

Consider a founder who sells a private company for $1 million after a decade of building. Under the prior regime, the 50% CGT discount applied to the nominal gain, and Division 152 small-business CGT concessions (under the Income Tax Assessment Act 1997) could further reduce or eliminate the tax liability entirely. These concessions were specifically designed to facilitate business succession and retirement funding:

- 15-year exemption: Full CGT exemption if the asset was held for at least 15 years and the owner is retiring or permanently incapacitated

- 50% active asset reduction: An additional 50% reduction on the capital gain for qualifying active business assets

- Retirement exemption: Up to $500,000 lifetime CGT exemption directed toward superannuation

- Rollover relief: Allows deferral of CGT if sale proceeds are reinvested in a replacement active business asset

The unresolved question is whether Division 152 concessions survive the 30% minimum effective rate floor or are partially overridden by it. Draft legislation has not yet been released, and this interaction is the single most consequential unknown in the entire reform package for business owners approaching succession or retirement.

Stockspot modelling indicates a founder selling a business for $1 million could face an after-tax wealth reduction exceeding $225,000 under the new CGT framework.

| Scenario ($1M sale, 47% marginal rate) | Old treatment | New treatment (if Div 152 overridden) |

|---|---|---|

| CGT discount / indexation | 50% discount applied | CPI indexation of cost base |

| Div 152 concessions | Fully available | Interaction with 30% floor unconfirmed |

| Estimated after-tax proceeds | Higher (concessions stack) | Potentially $225,000+ lower |

Chris Brycki, chief executive of Stockspot, noted in commentary published in The Australian that Treasury’s stated goal of redirecting capital toward productive business investment sits in direct tension with raising the effective tax cost of the exit event that rewards entrepreneurs for taking that risk. The contradiction is not rhetorical. It is arithmetic.

Why restricting negative gearing to new builds may tighten rents before it eases them

The policy logic: redirecting demand toward new construction

The new-build carve-out is designed as a supply stimulus. By removing negative gearing eligibility from existing properties while preserving it for new residential construction, the policy redirects investor demand toward the segment of the housing market that adds to total dwelling stock. In theory, this increases construction activity over time and eases affordability pressure.

Whether it works as intended depends on factors external to the tax reform itself: construction financing conditions, planning approval timelines, and developer willingness to bring projects to market in an environment where input costs remain elevated.

The timing risk: when does the supply actually arrive?

The policy’s long-run logic may hold. The near-term sequencing is the problem. The supply adjustment unfolds in three stages:

- Investor demand shifts away from existing stock as post-Budget purchasers face weaker economics without negative gearing

- New-build purchases increase, but construction lags of 18-36 months between off-the-plan purchase and occupancy apply

- New supply arrives and begins to ease rental market pressure

The gap between stage one and stage three is where rental markets tighten. Existing landlords who exit reduce available rental stock before new dwellings are completed. The grandfathering provision partially insulates the existing rental stock, since landlords holding properties acquired before Budget night retain full deductibility. This moderates, but does not eliminate, the near-term exit pressure.

Research from market analysis suggests reduced speculative demand may dampen property values over time but could simultaneously shrink rental stock, particularly in capital city markets with already-tight vacancy rates. Post-Budget vacancy rate data from SQM Research and dwelling value signals from CoreLogic will be the leading indicators to watch as the transition period unfolds.

The startup and venture capital contradiction the Budget does not resolve

How the 30% floor compresses startup portfolio economics

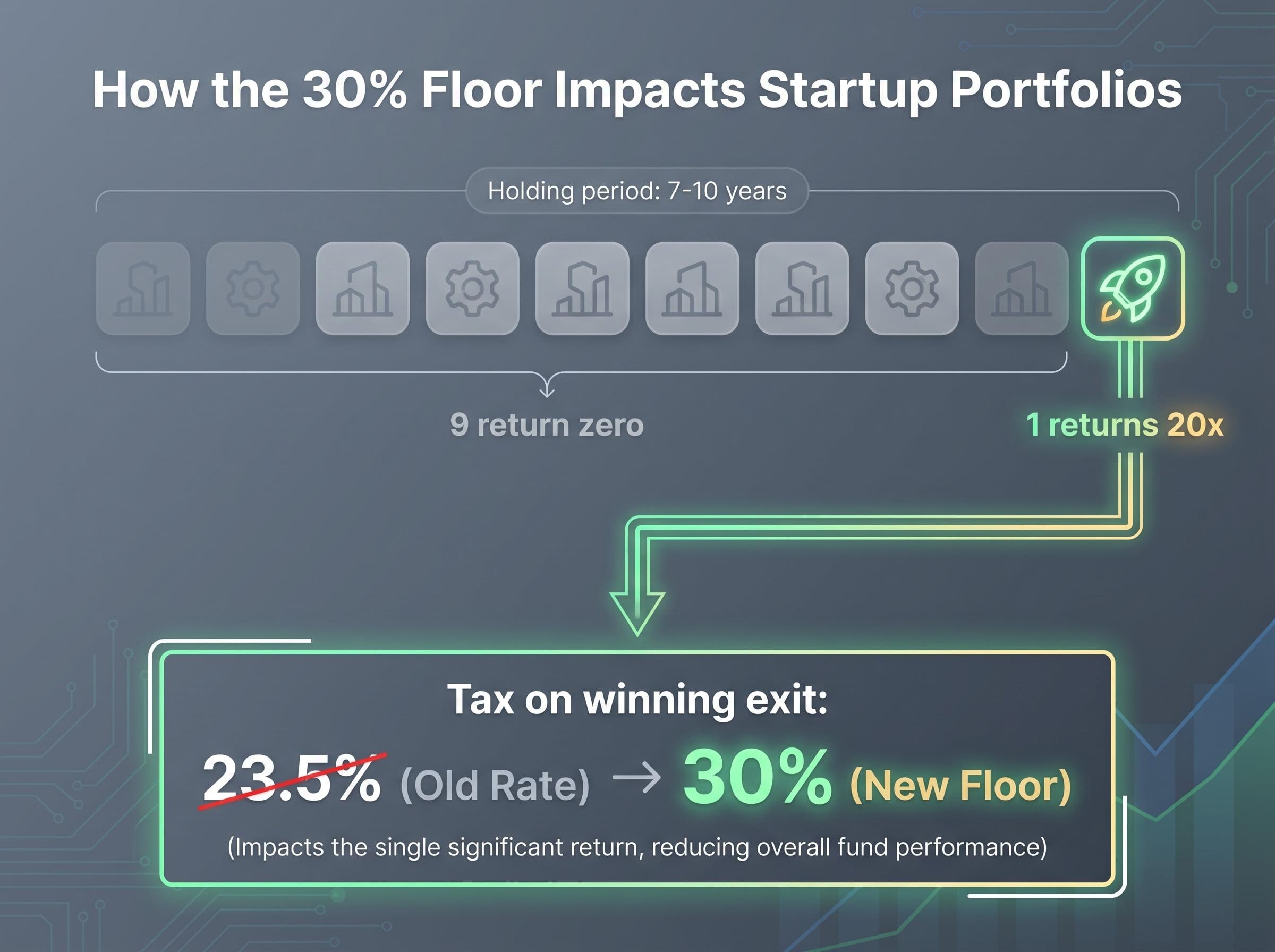

Startup and venture capital investing differs structurally from property or ETF investing. Failure rates are high. Holding periods typically stretch 7-10 years before exit. Returns concentrate in a small number of large wins that must compensate for the majority of total losses across a portfolio.

In a simplified illustration: an angel investor deploys capital across ten early-stage companies. Nine return zero. One returns 20x the original investment. Under the old 50% CGT discount, the winning exit was taxed at an effective rate of 23.5% for a top-rate taxpayer. Under the new 30% floor, that effective rate rises. The compression is most severe for investors on marginal rates below 30%, who are pulled up to the floor rather than benefiting from their lower rate.

The net effect is a reduction in the expected after-tax return that justifies investing in the nine losers. For angel investors and early-stage venture funds, this changes the portfolio mathematics.

Chris Brycki observed in The Australian that Australia already faces weak productivity growth and slowing business dynamism, and that disincentivising long-term risk-taking through higher effective CGT rates may reinforce those patterns rather than reverse them.

The CGT lock-in effect, where higher effective rates reduce the incentive to sell and reallocate capital, may partially undermine the Government’s stated goal of redirecting investment toward productive uses, since investors who would otherwise have sold and redeployed into new builds or business assets instead hold existing positions to avoid the tax event.

The employee share ownership plan (ESOP) dimension adds a further layer. If employee equity gains face the 30% floor, the attractiveness of equity compensation as a recruitment tool for startups competing against established-company salaries is reduced.

Three investor types face the sharpest impact:

- Founders at exit, where years of deferred compensation crystallise in a single taxable event

- Angel investors on early-stage equity, where portfolio return economics depend on favourable treatment of winning positions

- Employees holding ESOP equity, where the compensation advantage of equity over salary narrows

What this means for Australia’s position as a startup destination

Australia competes for founder talent and early-stage capital against jurisdictions with more favourable CGT treatment for startup equity. The reforms widen that gap. Confirmed post-Budget commentary from the Australian Investment Council and the Tech Council of Australia was not yet available as of 16 May 2026, four days after Budget night, but their responses will shape the sector’s formal position on the reforms.

ESOP tax treatment intersects with the competitiveness question and requires specific legal advice as draft legislation emerges.

The decisions that cannot wait until the legislation is final

Some decisions have already crystallised. Negative gearing eligibility for property acquisitions made before versus after 7:30pm AEST on 12 May 2026 is fixed. The question now is whether to hold grandfathered properties through the transition or dispose of assets before 1 July 2027 under the old CGT treatment.

Other decisions depend on legislative detail that has not yet been released. The Division 152 interaction with the 30% floor cannot be planned around until Treasury publishes draft legislation. Business owners should prepare scenario models now but hold execution until that clarity arrives.

| Decisions already crystallised | Decisions requiring legislative confirmation |

|---|---|

| Negative gearing eligibility (pre/post Budget night) | Division 152 interaction with 30% CGT floor |

| Grandfathered status of existing holdings | ESOP treatment under the new framework |

| New-build eligibility for post-Budget purchases | ATO apportionment formula detail for split-period gains |

Stockspot and other advisory firms have explicitly cautioned against rushed decisions based on early announcements. The reforms have not yet passed parliament, and final details may shift through consultation. Three categories of professional advice are worth engaging now:

- Tax adviser: CGT scenario modelling under old versus new treatment for specific asset holdings

- Property lawyer: Contract timing and settlement scheduling relative to the 1 July 2027 transition

- Business or succession lawyer: Division 152 interaction analysis and contingency structuring

The gap between announcement and legislation is itself a strategic window. It allows scenario modelling and conditional planning without premature execution.

Australia’s investment landscape has structurally shifted, but the map is still being drawn

The combined effect of the negative gearing restriction and the 30% CGT floor does not fall evenly. Property investors acquiring existing stock after Budget night face the sharpest immediate arithmetic. Business founders approaching a sale face the largest single-transaction impact. Grandfathered property holders and new-build buyers sit in a structurally different position, with the prior rules or the carve-out preserving much of their existing economics.

The relative tax positioning across asset classes shifts materially under the new settings, with passive ETFs, dividend-paying equities, and superannuation structurally better placed than leveraged direct property and discretionary trust structures, a comparison that informs how investors might reweight portfolios during the transition window.

The unresolved contradiction sits at the policy’s centre. The new-build carve-out provides a mechanism for redirecting property capital toward supply-generating investment. No equivalent mechanism exists for startup equity. The reforms are designed to encourage productive capital allocation, yet the 30% floor taxes the entrepreneurial exit that is the direct reward for that risk-taking. Until draft legislation clarifies whether Division 152 concessions survive the floor, this tension remains structurally unaddressed.

Investors, property owners, and business founders should consult a tax adviser or financial planner with specific scenarios before the 1 July 2027 transition date and monitor Treasury’s draft legislation release for resolution of the Division 152 question.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.