How to Value a Transition-Stage Stock Using Tesla as a Case Study

16 mins ago

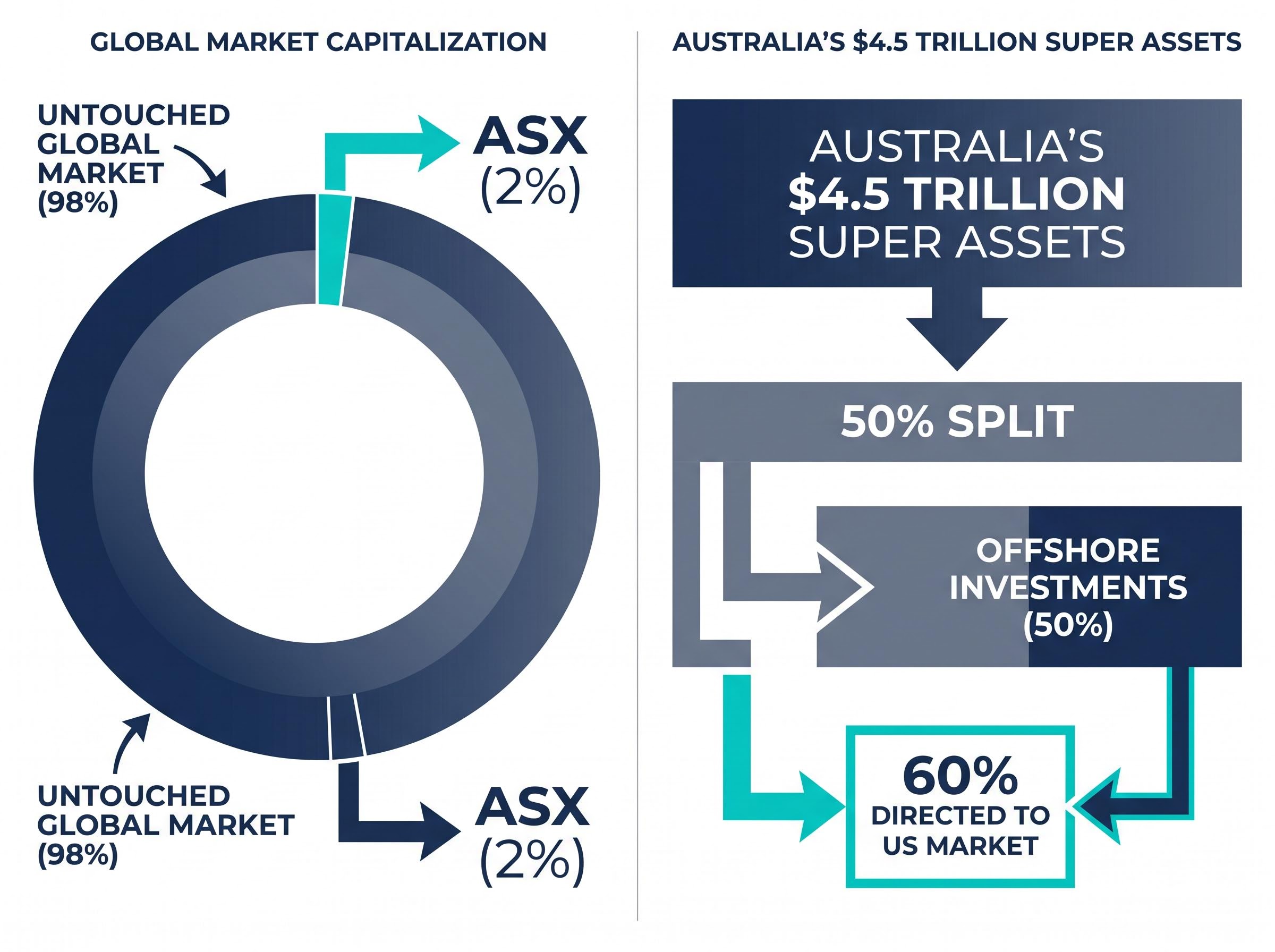

Australia’s superannuation system has quietly crossed a significant threshold: 50% of the nation’s $4.5 trillion in super assets now sits in offshore investments. Yet most self-directed investors are still doing the opposite, building portfolios dominated by the same four banks and two miners. The ASX represents approximately 2% of global market capitalisation, which means a domestic-only portfolio leaves 98% of the world’s listed companies untouched.

Two Vanguard ETFs available on the ASX, V500 and VAE, offer a direct solution for investors who want meaningful exposure to US technology and Asian growth without the complexity of stock-picking or managing multiple accounts. This guide explains what each ETF holds, why they complement each other, how to combine them practically, and what currency and tax considerations Australian investors need to understand before buying. The result is a clear, actionable two-fund framework that can be implemented through any standard ASX broker.

The ASX is a concentrated market. Its sector composition leans heavily toward a narrow set of industries, and that concentration creates a structural gap for investors relying on it as their sole equity exposure.

Australia’s share of global market capitalisation sits at approximately 2%. That single figure is the mathematical case for looking beyond domestic borders.

The concentration problem runs deeper than sector weights alone: ASX stock performance against the index over a 15-year period shows that only 36% of Australia’s 210 largest listed companies beat the ASX 300, with the median individual stock returning 6.73% annually against the index’s 8.62%, and the gap widens further once survivorship bias is accounted for.

50% of Australia’s $4.5 trillion in superannuation assets is now invested offshore.

Institutional investors have already acted on this reality. Of that offshore allocation, 60% is directed to the US market. Super funds managing retirement savings for millions of Australians have structurally shifted away from domestic-only portfolios, and the trend has been accelerating since approximately 2023. Self-directed investors building portfolios through ASX brokers face the same concentration problem, but many have yet to make the same adjustment.

ASFA’s superannuation offshore investment data shows that international allocations have risen from around 35% to approximately 50% of total fund assets over the past decade, driven primarily by international listed equities and a structural shift away from domestic-only mandates.

The diversification case is not abstract. It rests on two specific gaps in the ASX that, left unaddressed, leave Australian portfolios structurally underexposed to the sectors driving long-term global returns.

Global technology and healthcare companies of significant scale are largely absent from the ASX. When these sectors outperform over extended periods, as technology has for much of the past decade, domestic-only portfolios miss the compounding effect entirely. V500 provides access to the full breadth of the S&P 500, including US-listed technology, healthcare, consumer discretionary, communications, and industrials companies that have no meaningful ASX equivalent.

A second gap exists that US-only exposure does not fill. Asia’s growth story is distinct from the American one: semiconductor manufacturing concentrated in Taiwan, digital platform economies in China and India, consumption-led growth across South Korea, and electric vehicle supply chain companies spread across the region. VAE provides access to these markets through the FTSE Asia ex-Japan index. Broad international ETFs such as VGS (Vanguard’s developed-market fund) offer global coverage but do not carve out dedicated Asia ex-Japan weight at the same level.

VAE is one of three main Asian ETF options on the ASX available to Australian investors: IAA carries a lower MER of 0.29% per annum and a concentrated 50-stock large-cap tilt, while ASIA allocates 34.2% to semiconductors and holds roughly two-thirds of its weight in Taiwan and South Korea, making it a targeted technology supply chain play rather than a broad regional fund.

This is not an argument against holding Australian shares. It is a case for adding what the ASX structurally cannot provide.

| Sector | ASX representation | Available via V500 or VAE |

|---|---|---|

| Technology | Minimal | V500 (US mega-cap tech) |

| Healthcare | Limited mid-cap | V500 (US pharma, biotech) |

| Semiconductors | Negligible | VAE (Taiwan, South Korea) |

| Digital platforms | Negligible | VAE (China, India) |

| EV supply chain | Negligible | VAE (China, South Korea) |

With the gaps identified, the next step is understanding the two products designed to fill them. Both are index-tracking ETFs with straightforward structures, but the details matter.

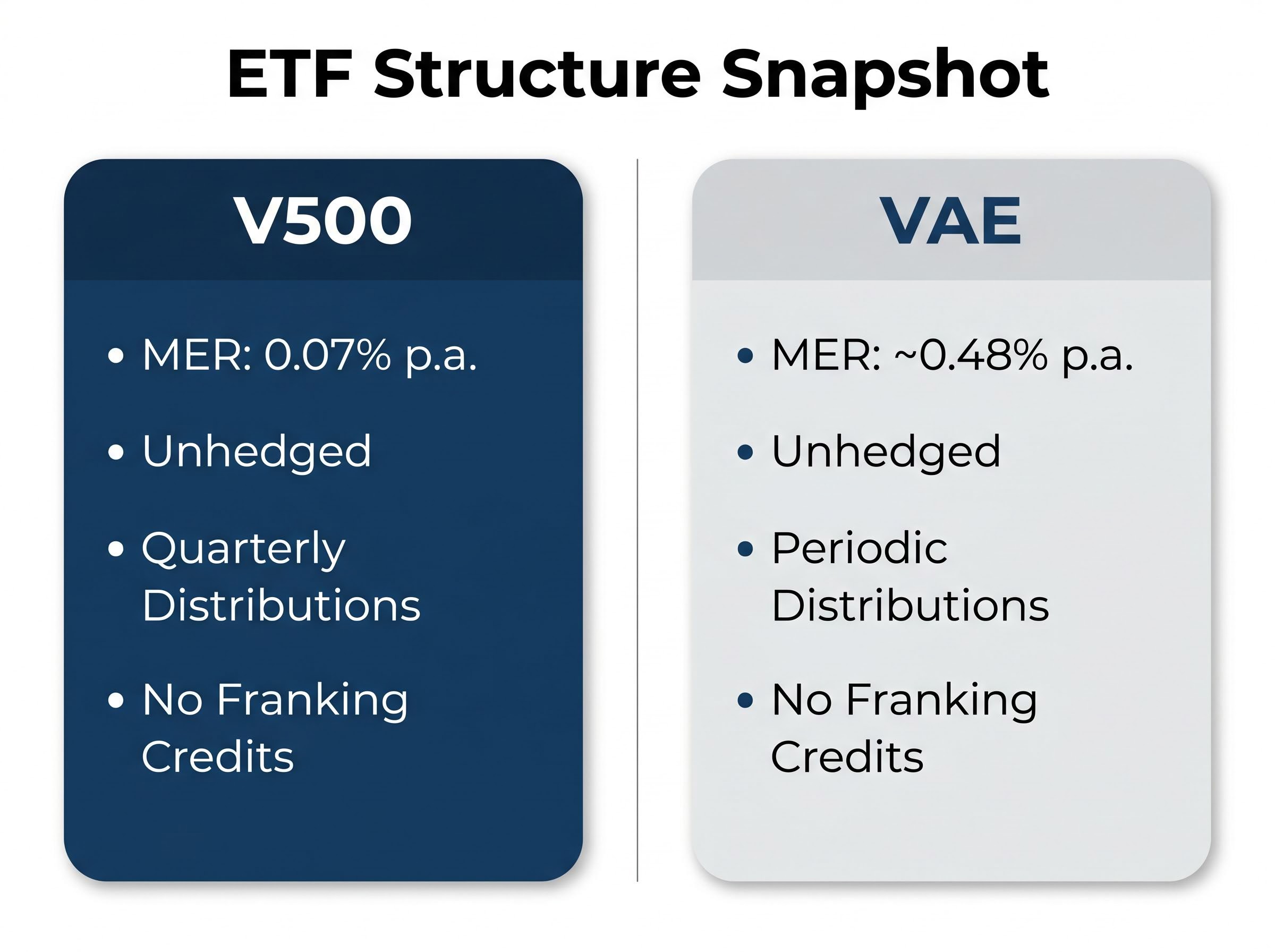

V500 tracks the S&P 500 Net Total Return AUD Index, covering approximately 500 of the largest US-listed companies. It launched on 3 March 2026 with trading commencing on the ASX the following day. Its management expense ratio (MER) is 0.07% p.a., placing it among the lowest-cost ETFs available on the ASX. As of early May 2026, assets under management stood at approximately $64.41 million. Distributions are paid quarterly, and a dividend reinvestment plan (DRP) is available. The fund is unhedged, meaning AUD/USD currency movements directly affect returns.

Given its recent launch, V500 has no meaningful performance history yet. Early performance tracks the S&P 500 benchmark in AUD terms, as expected for an index fund.

V500 is not the only ASX-listed product tracking the S&P 500; S&P 500 ETF alternatives such as IVV carry a MER of approximately 0.04% and significantly larger AUM, which matters to investors who weigh fund size and track record alongside cost when selecting between otherwise structurally similar index products.

VAE tracks the FTSE Asia ex-Japan index, with approximate country weightings of China (35-40%), India (20%), Taiwan (20%), and South Korea (15%). Its MER has historically been approximately 0.48% p.a., though investors should verify the current figure on Vanguard Australia’s product page before purchasing. VAE is also unhedged, exposing holders to a basket of Asian currencies relative to the Australian dollar.

Reader alert: Some third-party sources, including Morningstar Australia and the ASX ETP page, incorrectly label V500 as hedged. This is a labelling error. Vanguard Australia’s official product page confirms V500 is unhedged. Always verify fund details at the issuer’s website.

| Feature | V500 | VAE |

|---|---|---|

| Index tracked | S&P 500 Net Total Return AUD | FTSE Asia ex-Japan |

| MER | 0.07% p.a. | ~0.48% p.a. (verify current) |

| Hedging status | Unhedged | Unhedged |

| Primary geographic exposure | United States | China, India, Taiwan, South Korea |

| Distribution frequency | Quarterly (DRP available) | Periodic |

Understanding each ETF individually is one thing. Knowing how they work together as a portfolio building block is the step that turns research into a plan.

The logic is straightforward: V500 anchors the international allocation given the scale, liquidity, and sectoral depth of US equity markets. VAE provides a targeted tilt toward Asia’s longer-term growth potential, accessing markets and sectors that even a full S&P 500 allocation cannot reach. This mirrors the institutional approach; Australian super funds direct 60% of their offshore allocation to the US, with the remainder spread across other regions.

Several variables influence whether an investor tilts toward V500 or VAE. An existing portfolio heavy in resources and financials has less overlap with V500’s technology and healthcare exposure, which may argue for a larger V500 allocation. An investor with a 15-20 year time horizon may see VAE’s higher-growth, higher-volatility profile as appropriate for a meaningful allocation. Risk appetite matters: Asian markets can experience sharper drawdowns than the S&P 500, and the currency exposure adds a second layer of variability.

This two-fund approach sits alongside, not in place of, an Australian equities holding such as VAS.

Both V500 and VAE are purchased exactly like ordinary ASX shares through any standard brokerage account, including CommSec, Stake, SelfWealth, and CMC Markets. No minimum investment applies beyond the cost of one unit plus brokerage. V500 offers a DRP option for automatic reinvestment of distributions. Vanguard Australia’s product pages provide current fees, factsheets, and country breakdowns for both funds.

Three practical considerations separate international ETFs from their domestic equivalents, and understanding them upfront prevents surprises at tax time or when reading quarterly statements.

Both V500 and VAE are unhedged. For V500, this means a weaker Australian dollar relative to the US dollar boosts reported AUD returns, while a stronger Australian dollar reduces them. For VAE, the exposure is to a basket of Asian currencies (CNY, INR, TWD, KRW) relative to AUD. This currency effect is a feature of the structure. Over long holding periods, currency movements tend to average out, but in any given year they can meaningfully amplify or dampen returns.

The franking credit difference is the most commonly misunderstood aspect for Australian investors. ASX equities, including those held through VAS, often carry franking credits that reduce an investor’s tax liability. V500 and VAE distributions carry no franking credits because the underlying dividends are foreign-sourced. This does not make international ETFs inferior, but it does change the after-tax arithmetic.

The ATO guidance on ETF tax treatment confirms that distributions from foreign-domiciled funds must be declared as foreign income and may attract withholding tax, with a foreign income tax offset available to prevent double taxation on the same earnings.

ASX ETF tax treatment involves several layers that interact differently depending on holding period and investor structure: units held for at least 12 months qualify for the 50% CGT discount, ETF assets are held in a legally separate unit trust outside the issuer’s balance sheet, and using limit orders and checking the intraday net asset value before trading are the execution practices that protect returns at the point of purchase.

For investors who specifically want to remove USD currency risk from their US equity exposure, VGAD (Vanguard’s hedged international shares ETF) is the relevant alternative available on the ASX.

V500’s MER of 0.07% p.a. is among the lowest-cost ETFs available on the ASX. VAE’s higher MER of approximately 0.48% p.a. reflects the added complexity and cost of accessing Asian markets. Both figures should be verified on Vanguard Australia’s product pages before purchasing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The ASX’s 2% share of global market capitalisation means domestic-only investing leaves the vast majority of global growth untouched. V500 and VAE together address the two largest gaps, US technology and healthcare, and Asian growth markets, in a straightforward, low-cost structure.

The practical simplicity is the point. Both ETFs are accessible through any ASX broker, require no minimum investment beyond one unit, and are managed passively. Investors are not depending on active stock-selection skill or timing calls. They are buying broad, diversified exposure to the parts of the global economy the ASX does not cover.

This is a strategy for investors with multi-year time horizons who want to build wealth systematically. Both funds will experience periods of underperformance. The value comes from consistent, long-term accumulation rather than attempting to pick the right entry point. Before making any investment decision, investors should visit Vanguard Australia’s official product pages for current fees, factsheets, and country breakdowns for both V500 and VAE.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

V500 is a Vanguard ETF listed on the ASX that tracks the S&P 500 Net Total Return AUD Index, providing exposure to approximately 500 of the largest US-listed companies at a management expense ratio of just 0.07% per annum. It launched in March 2026 and is unhedged, meaning AUD/USD movements directly affect returns.

VAE tracks the FTSE Asia ex-Japan index, with approximate country weightings of 35-40% China, 20% India, 20% Taiwan, and 15% South Korea, providing exposure to semiconductor manufacturers, digital platform companies, and electric vehicle supply chain businesses across the region.

No, neither V500 nor VAE distributions carry franking credits because the underlying dividends are foreign-sourced. Australian investors must declare these distributions as foreign income, though a foreign income tax offset is available to prevent double taxation.

Investors can use V500 as the anchor of their international allocation to capture US technology and healthcare exposure, then add VAE for a targeted tilt toward Asian growth markets, mirroring the approach used by Australian superannuation funds that direct roughly 60% of offshore allocations to the US and the remainder to other regions.

The ASX represents only approximately 2% of global market capitalisation, with heavy concentration in financials and materials and minimal technology or semiconductor exposure. International ETFs such as V500 and VAE provide access to the 98% of listed companies and sectors that a domestic-only portfolio leaves untouched.