JPMorgan Says Cyber Risk Leaves Bank Valuations Dangerously Exposed

9 mins ago

Not all AI spending is created equal. When four of the world’s largest technology companies reported Q1 2026 earnings in the final days of April 2026, each disclosed rising capital expenditure on artificial intelligence. Yet markets delivered starkly different verdicts. Alphabet surged nearly 10% in after-hours trading while Meta shed close to the same amount. Amazon edged higher; Microsoft drifted lower despite a cloud beat. The divergence landed in the same week that Australian inflation came in above forecasts and the Reserve Bank of Australia raised rates on 5 May 2026, sharpening local investor focus on which offshore equity positions are genuinely earning their keep. Big Tech earnings have become a live referendum on whether AI investment is converting into revenue or merely accumulating on balance sheets. What follows unpacks why Alphabet and Amazon were rewarded, why Microsoft and Meta were not, and what the split signals for Australian investors evaluating global tech exposure.

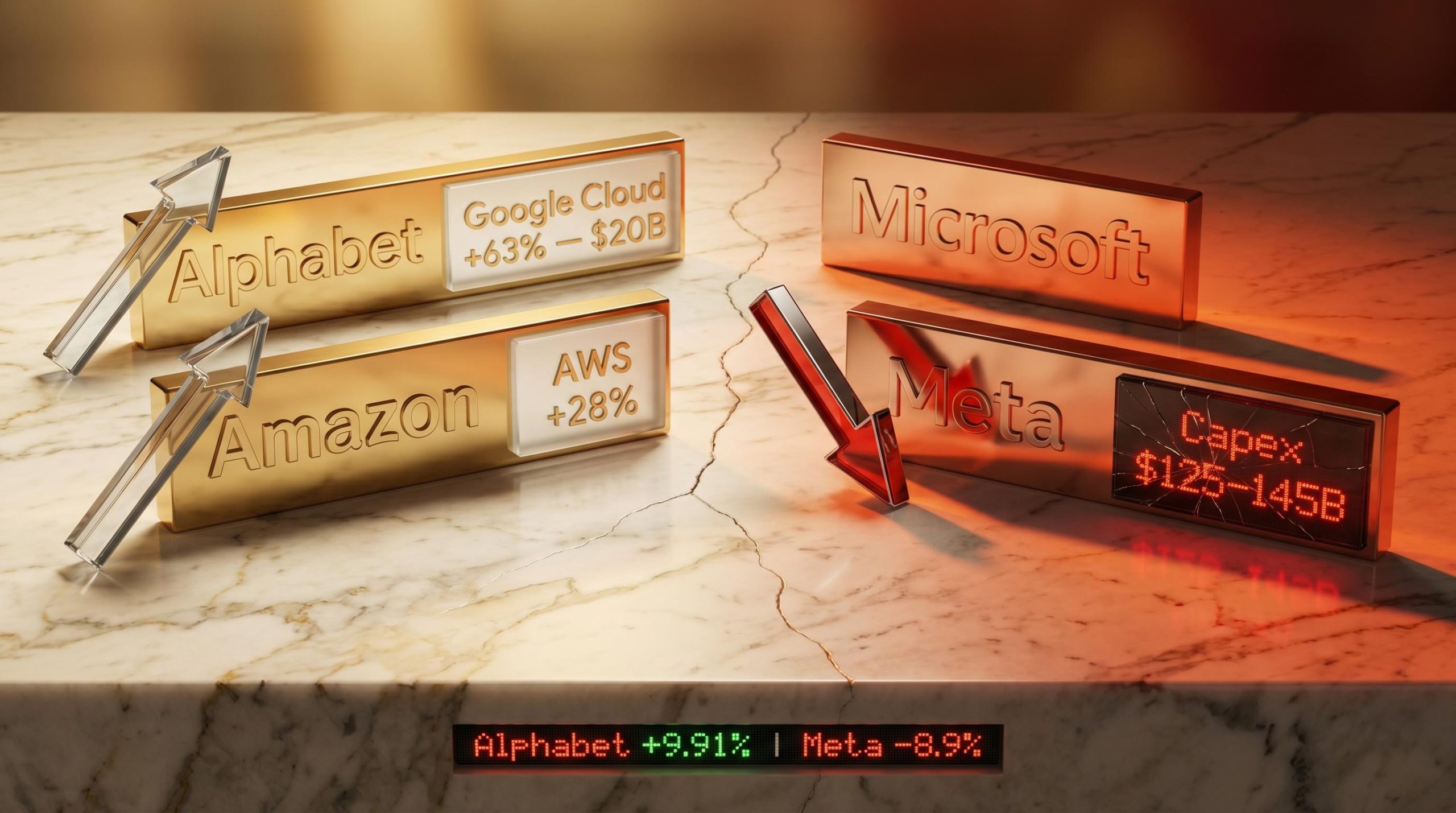

Alphabet gained approximately 9.91-10% after hours. Meta fell approximately 8.9-10%. Between those two reactions sits a nearly 20-percentage-point gap, and it did not come from revenue misses.

All four companies beat or met headline estimates. All four disclosed increasing AI capital expenditure. The market’s verdict was not about top-line performance; it was about which companies could show AI spending translating into visible returns.

All four hyperscalers beat or met consensus revenue estimates. The divergence in share price reactions reflects a market now applying a returns-evidence filter, not a revenue filter, to AI spending.

| Company | Q1 Revenue Result | After-Hours Price Move | AI Capex Direction |

|---|---|---|---|

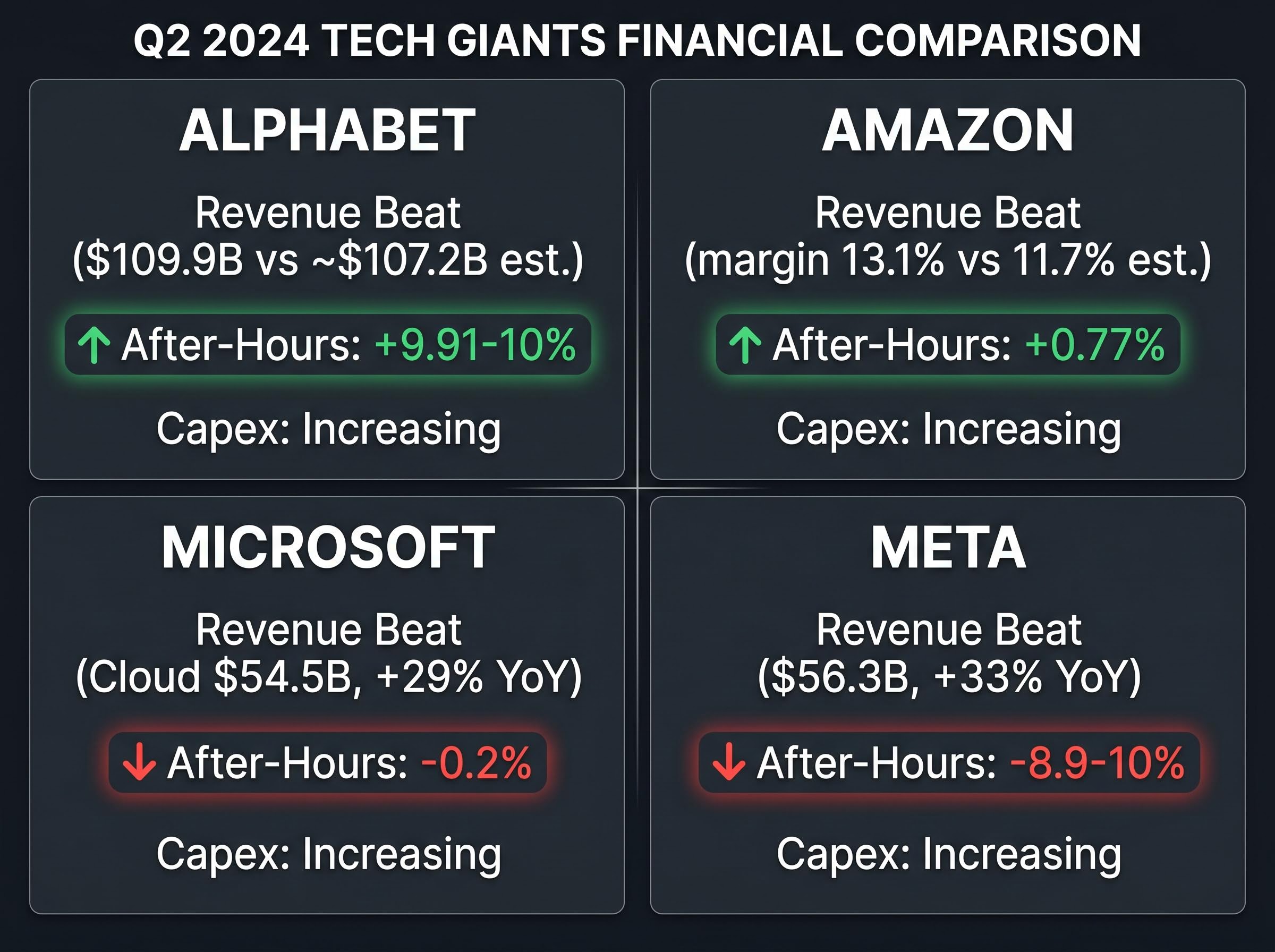

| Alphabet | Beat ($109.9B vs ~$107.2B est.) | +9.91-10% | Increasing |

| Amazon | Beat (operating margin 13.1% vs 11.7% est.) | +0.77% | Increasing |

| Microsoft | Beat (Cloud $54.5B, +29% YoY) | -0.2% | Increasing |

| Meta | Beat ($56.3B, +33% YoY) | -8.9-10% | Increasing |

The puzzle this earnings season posed was straightforward: if everyone beat, why did only half get rewarded?

The answer sat inside the cloud revenue lines. Both Alphabet and Amazon delivered AI spending that was already converting into measurable revenue growth, within this quarter, not deferred to a future reporting period.

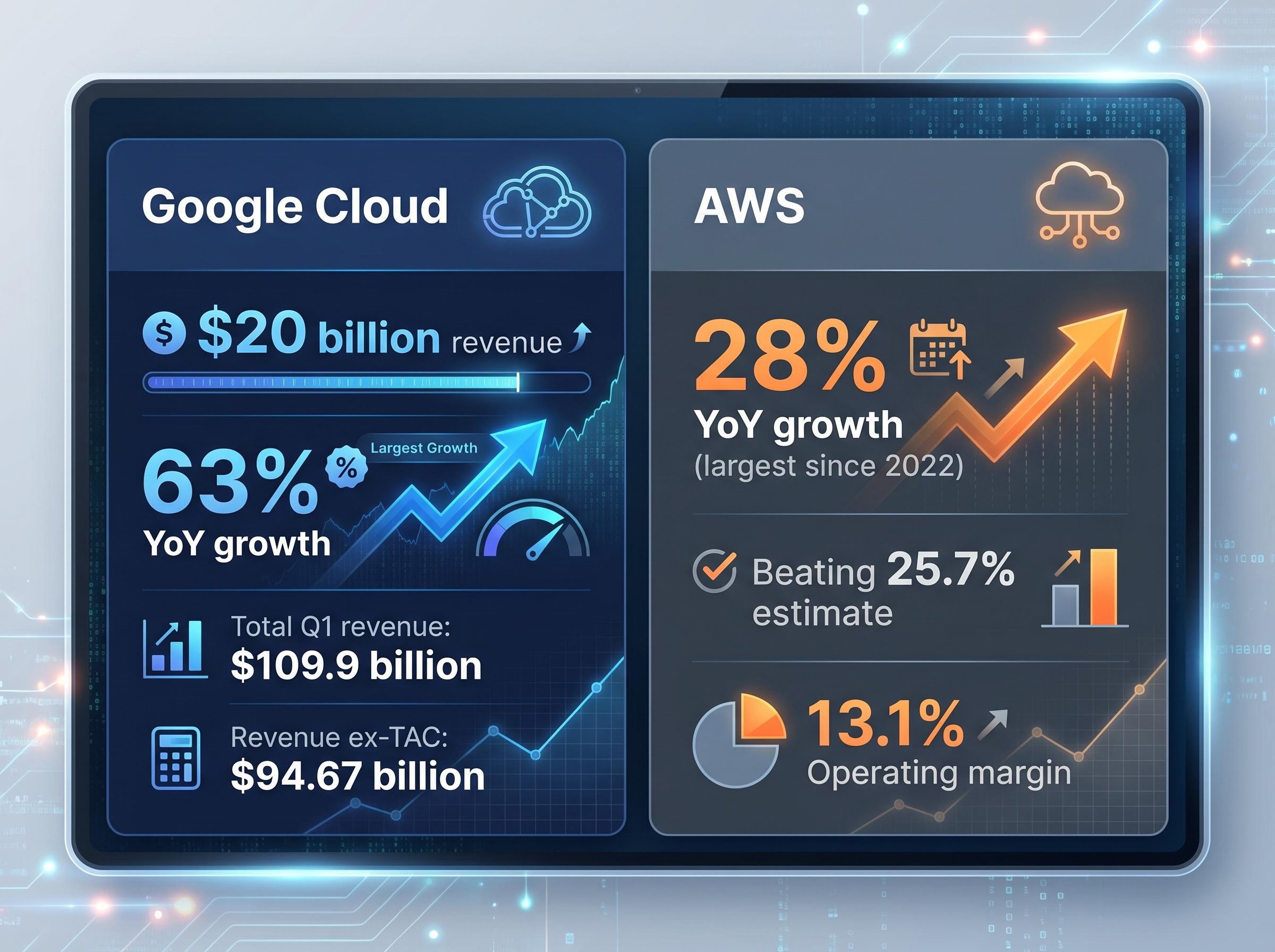

Google Cloud revenue grew 63% to $20 billion, the strongest cloud growth since the AI boom began. That figure did the persuasive work on its own.

Enterprise AI spending powered the result. The beat was not confined to cloud; it extended across the business, reinforcing the argument that Alphabet’s AI investment is generating returns at scale.

AWS cloud revenue rose 28% year-over-year, beating the consensus estimate of 25.7% and marking the largest growth since 2022. Operating margin came in at 13.1% versus a forecast of 11.7%.

The partnership layer mattered. Where Alphabet demonstrated organic enterprise demand, Amazon showed deal-making with the leading AI model developers translating into measurable cloud revenue. Both companies provided evidence of capex-to-revenue conversion within a visible timeframe, not a promise.

The market’s reward for Alphabet and Amazon rested on a specific mechanism that Australian investors can apply to every future earnings cycle: cloud infrastructure has become the primary channel through which AI capital expenditure converts into visible revenue.

When a hyperscaler spends billions on data centres, chips, and networking equipment, the revenue signal investors look for is growth in the cloud business that sits on top of that infrastructure. If a company’s cloud unit is growing faster than expected, the market reads that as evidence the spending is working. If the cloud unit is growing at or below expectations despite rising capex, the market reads the spending as accumulating without a clear return path.

Bloomberg coverage from 29-30 April 2026 captured the investor mood: markets now require “something coming out of the other side” of AI spending.

Early AI spending gains are beginning to extend beyond technology companies. Caterpillar has captured demand-side benefits from AI infrastructure construction, illustrating that the investment thesis has downstream effects in industrials and utilities.

The hardware supply chain sits at the intersection of both the rewarded and penalised earnings stories from this quarter: semiconductor equities capturing hyperscaler procurement budgets have delivered material year-to-date gains regardless of whether the end hyperscaler itself passed the market’s returns-evidence filter, illustrating that the AI investment thesis distributes unevenly across the tech ecosystem.

Two phases now define how the market evaluates AI capex:

Understanding the distinction helps Australian investors move beyond surface-level earnings headlines and assess whether a tech holding’s AI spending is generating returns or still building towards them.

The AI infrastructure investment cycle now demands that investors separate operating cash margins from capex headlines; Wall Street’s working expectation as of Q1 2026 is that companies must demonstrate concrete monetisation within a twelve-month window, a threshold that Alphabet and Amazon cleared this quarter and that Microsoft and Meta did not.

Neither Microsoft nor Meta delivered a bad quarter in absolute terms. The issue was a gap between what the results showed and what the market now demands.

Microsoft Cloud revenue reached $54.5 billion, up 29% year-over-year (25% in constant currency). By any prior standard, that is a strong result, and it beat estimates.

The cloud number alone would have been celebrated a year ago. In Q1 2026, investors treated it as insufficient because the broader AI investment narrative lacked the near-term return clarity that Alphabet and Amazon provided.

Meta reported Q1 revenue of $56.311 billion, up 33% year-over-year. The headline beat did not matter.

The capex increase without an accompanying return roadmap was the specific trigger. Investor patience for deferred AI returns is eroding; a strong revenue quarter no longer provides cover for an AI spending strategy that lacks near-term return visibility.

The Q1 results exposed a structural tension that extends beyond any single company’s quarter. The scale of planned AI infrastructure spending across the hyperscalers is enormous, and the market’s willingness to fund it without visible returns is narrowing.

Meta’s confirmed guidance of $125-145 billion for 2026 is the clearest data point. Analyst estimates based on Q1 trends suggest Amazon’s 2026 capex could approach approximately $200 billion, though no official guidance range has been confirmed. Microsoft and Alphabet did not disclose specific full-year figures.

| Company | 2026 Capex Figure | Guidance Status |

|---|---|---|

| Meta | $125-145 billion | Confirmed guidance |

| Amazon | ~$200 billion | Analyst estimate (unconfirmed) |

| Microsoft / Alphabet | Not disclosed | No full-year figure provided |

No confirmed consensus aggregate 2026 capex figure across all four companies has been published. The absence of a clear total itself reflects the opacity that is driving investor concern.

Bloomberg coverage from 29-30 April 2026 noted resolute underlying demand but flagged growing investor pressure for tangible outcomes. The divergence seen this quarter is not a one-off. It marks the beginning of a sustained market discipline applied to hyperscaler AI spending, where opacity about returns will be penalised and visibility rewarded.

The AI returns debate is not an abstract US story. Australian superannuation funds and exchange-traded funds with global equity mandates hold these companies. The market’s new returns-evidence filter directly affects the valuations within those portfolios.

The domestic backdrop raises the stakes. The RBA raised rates on 5 May 2026, a decision broadly anticipated after inflation data released the prior week came in above forecasts. In a higher-rate environment, the opportunity cost of holding offshore equity positions rises, making it more consequential to distinguish between AI spending that is converting and AI spending that is accumulating.

Market concentration risk compounds the returns question for Australian ETF holders: advanced computing stocks account for approximately 13% of US equity valuations in April 2026, surpassing dot-com era levels, which means a sector-wide repricing of AI capex expectations would transmit through broad index products rather than staying contained within individual stock positions.

The RBA’s May 2026 monetary policy decision confirmed the increase in the cash rate target to 4.35 per cent, citing above-forecast inflation as a key factor, a move that raised the opportunity cost of holding offshore equity positions across Australian superannuation and ETF portfolios.

Vesna Peroska of Morningstar Australia has observed that investor attention remains concentrated on the AI investment narrative as a driver of equity market support, underscoring how closely Australian portfolio outcomes are tied to whether that narrative delivers.

Three steps can help Australian investors evaluate global tech holdings through the lens this earnings season established:

The split between Alphabet and Amazon on one side, and Microsoft and Meta on the other, serves as the practical case study for applying this framework.

Q1 2026 earnings established that markets are no longer treating AI capital expenditure as uniformly positive. Evidence of conversion is now the price of admission for a premium valuation. The divergence between Alphabet and Amazon on one side, and Microsoft and Meta on the other, could narrow or widen depending on what Q2 2026 results reveal.

The AI spending story is entering a more demanding phase. Companies that demonstrate visible returns from their infrastructure investment will be rewarded; those that cannot will face growing scepticism regardless of headline revenue performance. Morningstar’s broader coverage of global tech valuations and the AI infrastructure investment theme offers ongoing analysis for investors tracking this shift.

Investors wanting to stress-test whether the market’s new returns-evidence filter represents rational repricing or the beginning of a broader correction will find our deep-dive into AI stock bubble frameworks, which applies Minsky, Kindleberger, Sharma’s four O’s, and the Shiller CAPE ratio to the current AI spending cycle, with the CAPE standing at 40.11 as of 1 May 2026 and the four frameworks delivering split verdicts on whether a bubble has formed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Q1 2026 Big Tech earnings showed that markets are no longer treating rising AI capital expenditure as uniformly positive. Companies like Alphabet and Amazon were rewarded because their cloud units showed measurable revenue growth from AI investment, while Meta and Microsoft faced selling pressure despite strong headline results because their AI spending lacked clear near-term return signals.

Alphabet surged roughly 10% after hours because Google Cloud revenue grew 63% to $20 billion, providing concrete evidence that AI infrastructure spending was converting into revenue. Meta fell approximately 9-10% because the company raised full-year 2026 capex guidance to $125-145 billion without accompanying near-term return signals, which the market treated as accumulation rather than conversion.

Conversion mode means a company's AI spending is producing visible revenue growth within the current reporting period, as seen with Google Cloud and AWS in Q1 2026. Accumulation mode means AI capital expenditure is rising but revenue conversion remains unclear or deferred, the pattern investors penalised at Meta and, to a lesser extent, Microsoft this quarter.

Australian superannuation funds and ETFs with global equity mandates hold Alphabet, Amazon, Microsoft, and Meta, meaning the market's new returns-evidence filter directly affects portfolio valuations. With the RBA raising rates to 4.35% in May 2026, the opportunity cost of holding offshore equity positions has also increased, making it more important to distinguish between AI spending that is converting and spending that is still accumulating.

Investors can identify the company's primary AI revenue channel (typically the cloud business for hyperscalers), check whether recent results show growth in that channel ahead of analyst estimates, and assess whether rising capex guidance is accompanied by near-term return signals. A cloud beat signals conversion; rising spending without a visible return roadmap is the pattern the market penalised in Q1 2026.