Citi Puts Memory Supply Above Chip Design in AI Stock Rankings

45 mins ago

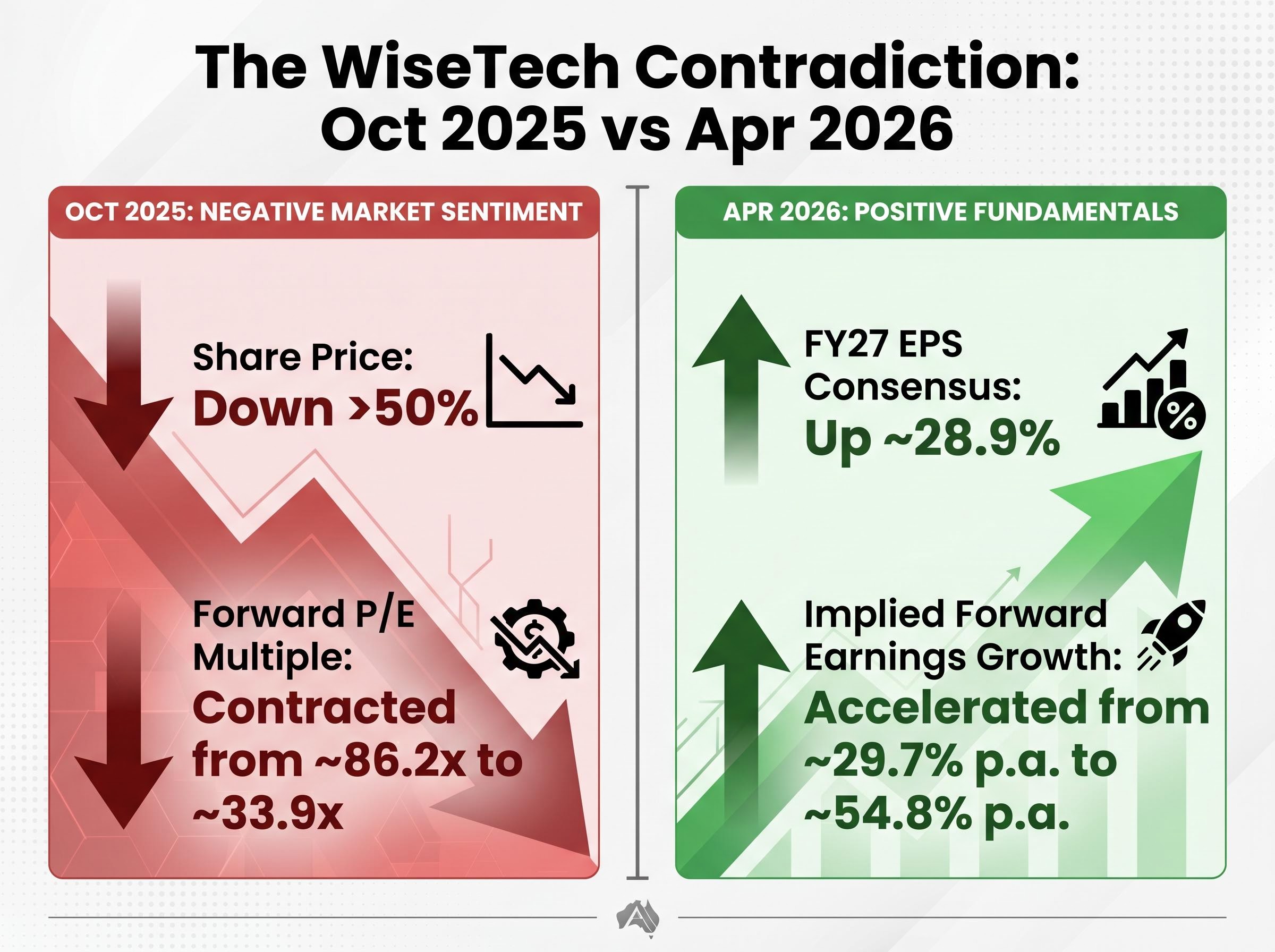

Between October 2025 and April 2026, WiseTech Global’s consensus earnings forecasts for FY27 rose 28.9%. Its share price fell more than 50%. That contradiction is the entire story of what happened to ASX growth stocks during the so-called SaaSpocalypse.

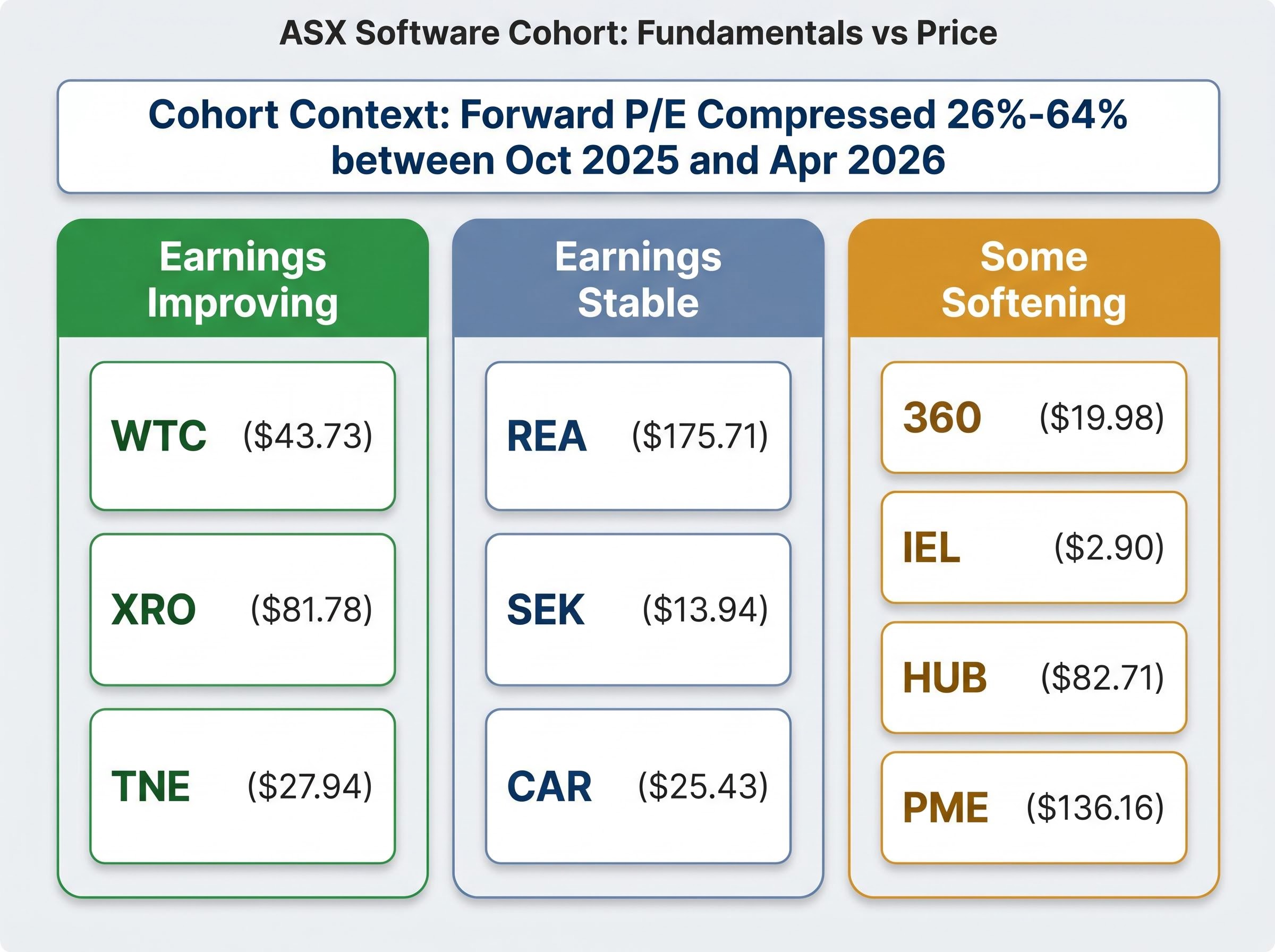

A wave of AI coding tools arriving from the second half of 2025 spooked global equity markets into repricing every software stock as if the SaaS business model itself was broken. The sell-off erased an estimated $1-2 trillion in global software market capitalisation. On the ASX, ten of the most prominent growth stocks saw forward price-to-earnings (P/E) multiples compress between 26% and 64%, even as underlying earnings held firm or improved across most of the cohort.

What follows unpacks what actually happened: the mechanics of multiple compression, the specific data showing sentiment did the damage rather than fundamentals, the case for why vertically embedded ASX software businesses are more defensible than the sell-off implied, and what broker consensus says about the recovery runway from here.

Growth stocks carry elevated P/E multiples because investors are paying for future earnings expansion, not just current profits. The higher the multiple, the longer the payback period the market is willing to accept. When that tolerance contracts, the arithmetic is unforgiving.

The mechanism works in three steps:

A stock trading at 80x earnings at $80 per share re-rated to 40x trades at $40. The business earned the same 100 cents per share throughout. The price halved purely because investor sentiment shifted.

This is not a theoretical exercise. Across the ten-stock ASX cohort, forward P/E multiples compressed 26%-64% between October 2025 and 30 April 2026. In all but one stock, consensus forward earnings estimates remained positive throughout the period. The mechanism has historical precedent: it preceded both permanent value destruction during the dot-com bust in 2000 and a full recovery after the 2022 rate cycle compression, depending on whether the fundamental threat turned out to be real.

The RBA’s March 2026 Financial Stability Review flagged the potential for sharp corrections in global equity markets driven by the AI investment cycle, providing an independent macroprudential lens on exactly the kind of sentiment-driven repricing that ASX growth stocks experienced across this period.

Understanding this mechanism is the prerequisite for evaluating whether the sell-off was rational. Without it, a 60% price decline looks like evidence of a broken business. With it, it may look like evidence of a mispriced one.

The fear was specific, and at its strongest, it was credible. Cursor 2.0, released in October 2025, demonstrated the capacity to auto-generate full applications. Anthropic’s Claude 3.5, released in June 2024, enabled no-code replication of basic SaaS functionality. GitHub Copilot-class tools demonstrated approximately 40% developer productivity gains. Together, these tools raised a pointed question for enterprise software investors: if customers could replicate or replace SaaS tools internally, what was the recurring subscription actually paying for?

The global market answered with indiscriminate selling. An estimated $1-2 trillion in software market capitalisation evaporated. Outcome-based pricing now accounts for approximately 40% of new enterprise contracts, up from approximately 15% previously, evidence that leading SaaS businesses were adapting pricing models rather than watching them collapse. The sell-off, however, made little distinction between the businesses genuinely exposed and those that were not.

The ASX sell-off did not occur in isolation; the global software repricing that erased an estimated $2 trillion in US market capitalisation through early 2026 accelerated the indiscriminate selling, pulling vertically embedded businesses down alongside the horizontal per-seat platforms that faced genuine displacement risk.

That distinction matters. Horizontal per-seat SaaS, where the product is a general-purpose tool sold per user, faces genuine displacement risk from AI coding platforms. Vertical systems of record, where the software is embedded in industry-specific workflows, regulatory frameworks, and proprietary data ecosystems, present a fundamentally different risk profile.

| Business Type | SaaS Model | AI Disruption Risk | ASX Examples | Moat Source |

|---|---|---|---|---|

| Horizontal per-seat SaaS | General-purpose, per-user pricing | High | Limited direct ASX exposure | Scale and brand; replicable by AI tools |

| Vertical systems of record | Industry-specific, embedded workflows | Low to moderate | WTC, XRO, PME, REA, TNE | Proprietary data, regulatory lock-in, network effects |

The ASX cohort’s competitive moats rest on four categories that AI coding tools cannot replicate:

The sell-off was partly rational and partly indiscriminate. Identifying which businesses sit in which category is where the investment analysis begins.

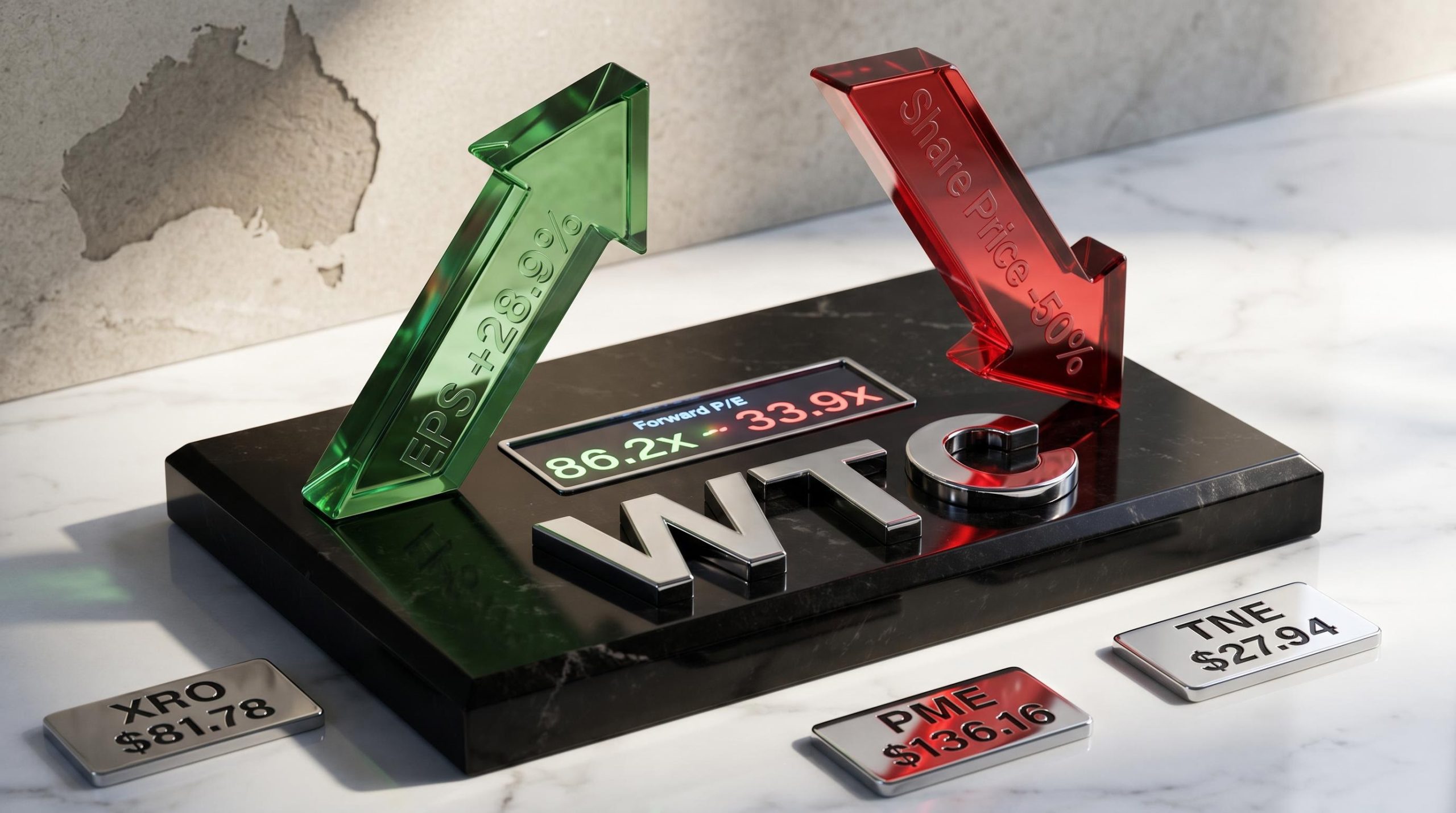

WiseTech Global (ASX: WTC) provides the clearest illustration in the cohort. The numbers tell the story without embellishment.

Between October 2025 and April 2026, consensus FY27 earnings per share estimates were revised upward by approximately 28.9%. Over the same period, the WTC share price fell more than 50%. The forward P/E multiple contracted from approximately 86.2x to approximately 33.9x.

Consensus earnings forecasts rose 28.9% while the share price more than halved. The implied forward earnings growth rate accelerated from approximately 29.7% per annum to approximately 54.8% per annum. The market was pricing in more pessimism at exactly the moment the earnings outlook was brightening.

| Metric | October 2025 | April 2026 |

|---|---|---|

| Share price direction | Pre-decline | Down more than 50% |

| Forward P/E | ~86.2x | ~33.9x |

| FY27 EPS consensus direction | Baseline | Up ~28.9% |

| Implied forward earnings growth rate | ~29.7% p.a. | ~54.8% p.a. |

CEO Zubin Appoo, appointed in July 2025, flagged AI-enhanced CargoWise features in an April 2026 trading update as supporting second-half FY26 revenue performance. As of early May 2026, the WTC share price stood at $43.73.

WiseTech’s AI transformation programme, which included a planned reduction of up to 2,000 roles and a structural shift toward transaction-based pricing, was announced alongside 76% revenue growth in 1H26, providing an early signal that management was using AI to deepen its operational moat rather than defending against displacement.

The WiseTech case illustrates precisely why understanding the source of a price decline matters. A 50% fall caused by multiple compression is a fundamentally different investment situation from a 50% fall caused by an earnings collapse. In WiseTech’s case, the earnings trajectory moved in the opposite direction to the share price across the entire period.

WiseTech was not an outlier. Across all ten stocks, forward P/E multiples compressed between 26% and 64% from October 2025 to 30 April 2026. The sell-off was sector-wide. The question is whether it was uniformly justified.

Technical analysis signals preceded the price declines. The ChartWatch model flagged downtrend conditions in nine of ten stocks between September and December 2025, well before the worst falls materialised. Subsequent declines from downtrend designation ranged from approximately 18% (HUB24) to approximately 82% (IDP Education), averaging approximately 51%. As of early May 2026, only Technology One (ASX: TNE) had returned to an uptrend designation.

| Stock | ASX Code | May 2026 Price (AUD) | Forward P/E Compression (Oct 2025 to Apr 2026) | Fundamental Verdict |

|---|---|---|---|---|

| WiseTech Global | WTC | $43.73 | ~61% | Earnings improving |

| Xero | XRO | $81.78 | Compressed | Earnings improving |

| REA Group | REA | $175.71 | Compressed | Earnings stable |

| Seek | SEK | $13.94 | Compressed | Earnings stable |

| CAR Group | CAR | $25.43 | Compressed | Earnings stable |

| Technology One | TNE | $27.94 | Compressed | Earnings improving |

| Life360 | 360 | $19.98 | Compressed | Some softening |

| IDP Education | IEL | $2.90 | Compressed | Some softening |

| HUB24 | HUB | $82.71 | Compressed | Some softening |

| Pro Medicus | PME | $136.16 | Compressed | Some softening |

Six stocks, WTC, XRO, REA, SEK, CAR, and TNE, maintained stable or improved near-term earnings per share and forward growth trajectories throughout the compression window. The multiple contraction for these names was therefore predominantly sentiment-driven.

Xero reported verified annual recurring revenue (ARR) of approximately $2.7 billion, up approximately 26% year-on-year, with AI-powered automated reconciliation features cited as supporting customer retention. Technology One reported FY26 year-to-date revenue growth of approximately 25%, with AI-embedded enterprise resource planning (ERP) winning local government contracts. REA Group’s Australian and New Zealand listings were up approximately 15% at its April 2026 trading update.

Four stocks showed some earnings trajectory softening, meaning the multiple compression was not entirely disconnected from fundamentals, even if its magnitude appeared disproportionate.

Long-run return concentration on the ASX is extreme: a Morningstar study found that Pro Medicus alone generated approximately 27% of all wealth created across the 210 largest listed companies over 15 years, which helps explain why even disproportionate multiple compression in a single quality compounder produces outsized portfolio consequences.

All ten cohort stocks held a consensus buy rating as of 6 May 2026. Eight of the ten qualified as strong buys under consensus methodology; IDP Education and Technology One were the exceptions.

Consensus 12-month price target upside ranged from approximately 12% for TNE to approximately 132% for IEL. Morgan Stanley reiterated a Buy rating on Xero with a $130 price target.

Institutional consensus points to 12%-132% upside across the cohort as of 6 May 2026, with all ten stocks rated buy.

Global signals provide additional context. In the United States, Salesforce and Workday were down approximately 29%-39% year-to-date, while Atlassian sat approximately 80% below its all-time high. UK-listed Darktrace had recovered approximately 25% on an AI pivot narrative.

On the ASX, only TNE had returned to a technical uptrend as of early May 2026. WTC, Life360, Seek, and HUB24 were still appearing on downtrend scans in the most recent ten trading sessions.

The recovery case is not without risk. Three unresolved factors could prevent or delay multiple re-expansion:

Consensus buy ratings and double-digit upside targets do not guarantee outcomes. They confirm that institutional investors who have stress-tested these businesses against the AI disruption thesis are not abandoning the cohort. The gap between current prices and price targets is the market’s way of pricing unresolved uncertainty, not confirmed permanent damage.

The majority of the ASX SaaS sell-off from October 2025 to April 2026 was driven by multiple compression rooted in sentiment, not by fundamental earnings deterioration. Six of ten stocks maintained stable or improving earnings trajectories. Four showed some softening, though the degree of multiple compression appeared disproportionate to the fundamental changes in each case.

Genuine uncertainty remains. AI disruption risk for horizontal SaaS is real. Technical signals suggest not all stocks have completed their bottoming process. The pricing model transition introduces near-term earnings visibility challenges.

For investors assessing individual stocks within the cohort, two questions matter most: does the business function as a system of record with proprietary data, regulatory embedding, or network effects? And has the multiple compression been proportionate to any actual change in the earnings trajectory?

The answers will vary stock by stock. The data presented here provides the foundation for that assessment.

For investors ready to act on the analysis presented here, our dedicated guide to pre-researched watchlist construction explains how to build a prioritised buy list with pre-calculated intrinsic value estimates and margin-of-safety thresholds, the mechanism that converts a compression thesis into a structured entry process when sentiment shifts.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Multiple compression occurs when investors reduce the price-to-earnings ratio they are willing to pay for a stock, causing the share price to fall even if earnings remain unchanged. For high-multiple ASX growth stocks, even a modest sentiment shift can produce dramatic price declines without any deterioration in the underlying business.

The sell-off was triggered by AI coding tools such as Cursor 2.0 and Anthropic's Claude 3.5, which raised fears that customers could replicate or replace SaaS products internally, prompting indiscriminate selling that erased an estimated $1-2 trillion in global software market capitalisation and compressed ASX growth stock multiples by 26%-64%.

Six of the ten cohort stocks, including WiseTech Global, Xero, REA Group, Seek, CAR Group, and Technology One, maintained stable or improving earnings trajectories throughout the compression window, meaning their price declines were predominantly driven by sentiment rather than fundamental deterioration.

Vertical systems of record are embedded in industry-specific workflows, regulatory frameworks, and proprietary data ecosystems that AI coding tools cannot easily replicate, unlike horizontal per-seat SaaS products which face genuine displacement risk from general-purpose AI platforms.

As of 6 May 2026, all ten cohort stocks held a consensus buy rating, with 12-month price target upside ranging from approximately 12% for Technology One to approximately 132% for IDP Education, though unresolved risks including prolonged AI disruption and macroeconomic softening remain.