Citi Puts Memory Supply Above Chip Design in AI Stock Rankings

57 mins ago

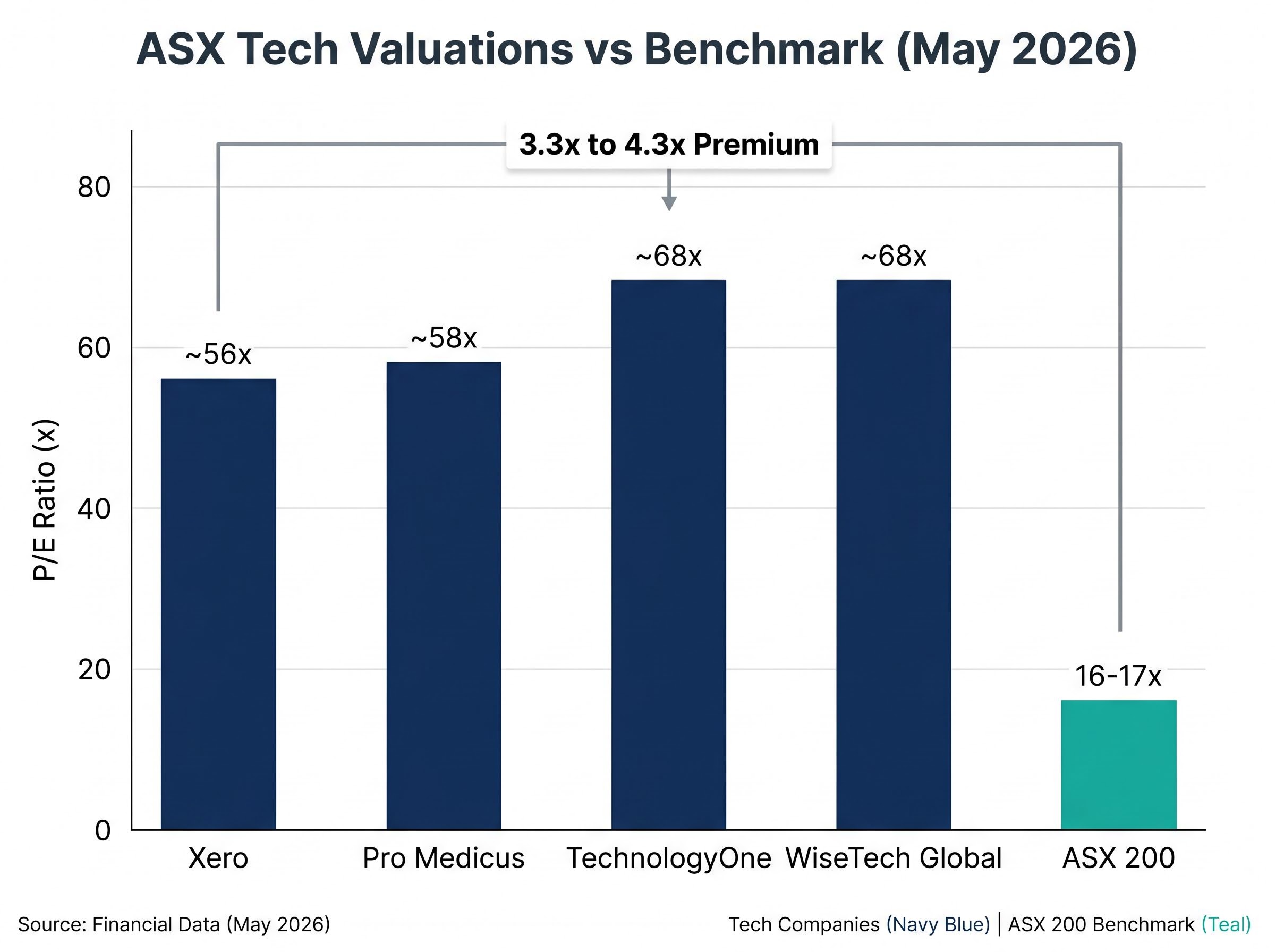

Four of the ASX’s most closely watched technology companies, Pro Medicus, WiseTech Global, TechnologyOne, and Xero, are trading at 56 to 68 times trailing earnings as of early May 2026. That is after a bruising stretch of multiple compression that included a broad ASX tech selloff in November 2025 and an AI-driven panic in January 2025. The premium these stocks command over the broader ASX 200, which trades at a forward price-to-earnings ratio of roughly 16-17x, has narrowed but not closed. Whether that remaining gap reflects fair compensation for genuine quality or a valuation trap dressed in strong earnings is the question Australian investors keep circling. This analysis examines the verified earnings results, the AI disruption episode, and the structural debate around premium multiples to give readers a framework for reaching their own answer rather than borrowing someone else’s.

The numbers as they stand in early May 2026 are straightforward. Pro Medicus (ASX: PME) trades at approximately 58x trailing earnings. WiseTech Global (ASX: WTC) and TechnologyOne (ASX: TNE) both sit near 68x. Xero (ASX: XRO) comes in at roughly 56x, the lowest of the four, though still more than three times the broader market’s forward multiple.

The ASX 200 forward P/E sits at approximately 16-17x as of early May 2026, making the gap between these four companies and the benchmark a factor of 3.3x to 4.3x.

| Company | ASX Code | Current TTM P/E | Approximate Premium vs ASX 200 |

|---|---|---|---|

| Pro Medicus | PME | ~58x | ~3.5x |

| WiseTech Global | WTC | ~68x | ~4.1x |

| TechnologyOne | TNE | ~68x | ~4.1x |

| Xero | XRO | ~56x | ~3.4x |

Two distinct events compressed these multiples from what appear to have been substantially higher 2024 peaks, though exact peak figures remain difficult to verify independently. The November 2025 selloff, reported by the Australian Financial Review and the Sydney Morning Herald, hit the sector broadly and sent TechnologyOne shares down approximately 17%. Months earlier, the emergence of DeepSeek in January 2025 triggered a market-wide reassessment of software business models.

The compression was real. Yet the gap that remains is striking. Paying three to four times the market multiple demands justification, and that justification starts with what these businesses actually earned.

Let the revenue figures arrive before the interpretation.

| Company | Period | Revenue | Revenue Growth |

|---|---|---|---|

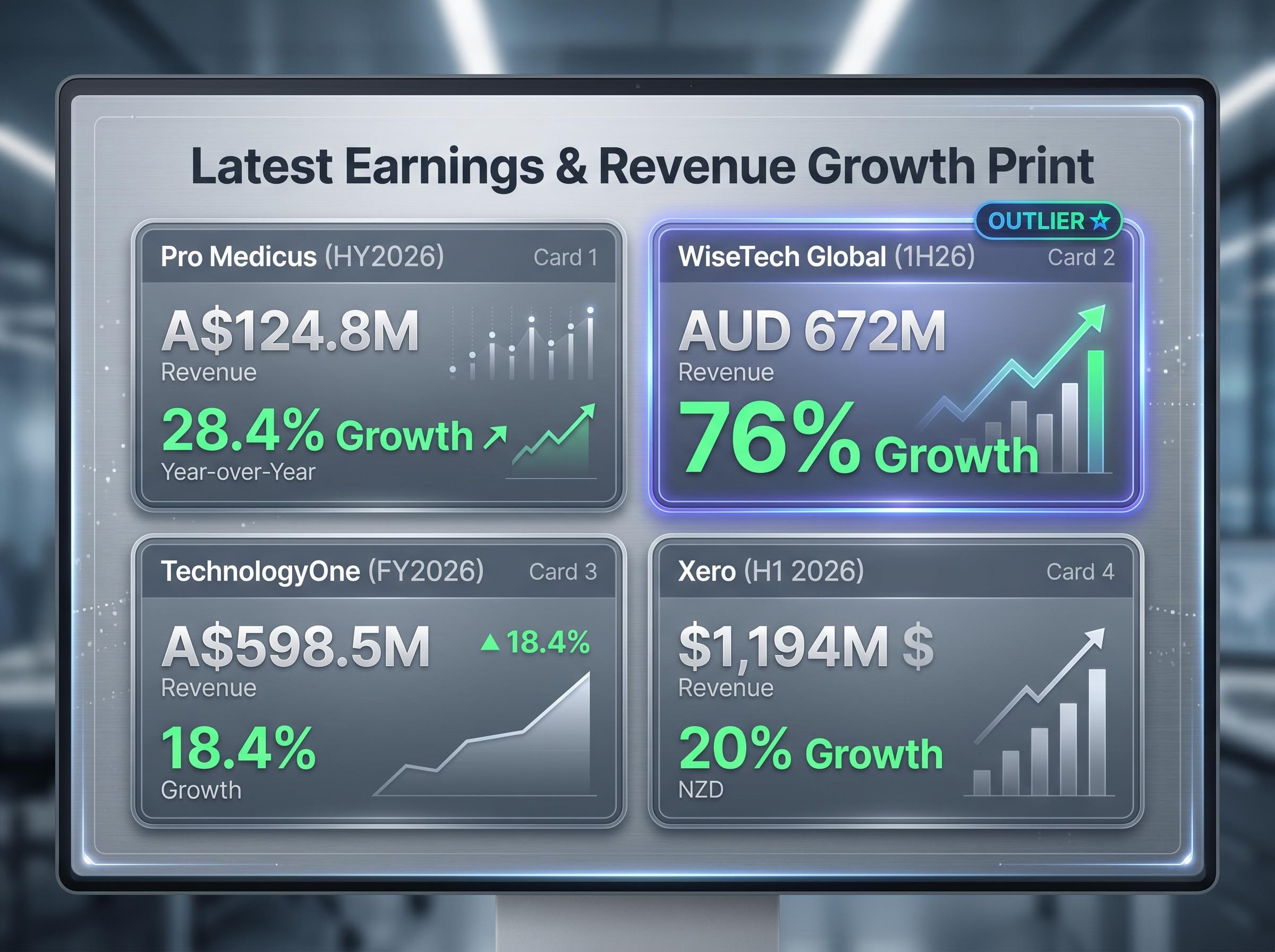

| Pro Medicus | HY2026 | A$124.8 million | 28.4% |

| WiseTech Global | 1H26 | AUD 672 million | 76% |

| TechnologyOne | FY2026 (full year) | A$598.5 million | 18.4% |

| Xero | H1 2026 | $1,194 million | 20% |

All four companies delivered genuine top-line growth. None of the recent share price recoveries relied on multiple expansion alone; the earnings underneath expanded meaningfully.

WiseTech Global’s first-half 2026 revenue of AUD 672 million, representing 76% year-on-year growth, stands apart. For a logistics software business that had been framed as vulnerable to AI-driven disruption just months earlier, the result was difficult to square with the bearish narrative. The scale of the beat, verified via WiseTech’s 25 February 2026 ASX release, made it the strongest revenue growth print in the group by a wide margin.

Pro Medicus at 28.4% and Xero at 20% delivered results consistent with high-quality SaaS growth trajectories. TechnologyOne’s 18.4% full-year growth was the most moderate of the four, though still comfortably above the ASX 200’s aggregate revenue growth.

These are not speculative businesses burning cash in pursuit of scale. They are profitable, growing, and generating the earnings that the premium multiples theoretically price in.

When DeepSeek emerged in January 2025, the initial market response treated it as a structural threat to any software business built on recurring revenue and proprietary workflows. The logic was immediate: if open-source AI models could replicate SaaS functionality at a fraction of the cost, the switching cost moats that justified premium valuations would erode. ASX tech stocks sold off sharply alongside global peers.

The November 2025 selloff was broader and arguably more damaging to sentiment. Per the Australian Financial Review (5 November 2025) and the Sydney Morning Herald (19 November 2025), the sector fell on a combination of valuation fatigue and macro caution, with TechnologyOne dropping approximately 17%.

The January 2025 selloff is increasingly framed by institutional analysts as a sentiment overcorrection rather than a fundamental reassessment, validated by the earnings results that followed.

What happened next told a different story. Each of the four businesses demonstrated that AI integration was enhancing, not undermining, their competitive positions:

The earnings data that followed, particularly WiseTech’s 76% revenue growth, made the January selloff look less like a structural repricing and more like a fear trade that outran its evidence. Businesses with deeply embedded workflows, high switching costs, and recurring revenue proved more resilient than the market had priced in during the panic.

That does not mean the AI competitive question is resolved permanently. It means the first test arrived, and these four businesses passed it.

A P/E ratio of 68x looks, on the surface, like investors have lost touch with reality. The instinct to dismiss it is understandable. But the mechanics of how growth stocks are valued explain why high multiples can be rational, even if they are never comfortable.

The logic works in three steps:

The PEG ratio, which divides the P/E by the earnings growth rate, offers a rough practical lens. A PEG of 1.0x is often treated as fair value for a growth stock. Pro Medicus at approximately 58x with 28.4% growth implies a PEG near 2.0x, suggesting the market is pricing in sustained growth beyond what the latest half-year result alone justifies. WiseTech at 68x with 76% first-half growth presents a different picture, though the PEG framework has limitations: it assumes growth rates are sustainable, and it ignores balance sheet risk entirely.

The P/E ratio does not capture execution risk, competitive disruption, or interest rate sensitivity. Growth stocks are long-duration assets, meaning their valuations are more sensitive to changes in discount rates than lower-growth businesses. When interest rates rise or rate-cut expectations are pushed back, the present value of distant future earnings falls, and high-P/E stocks absorb disproportionate price declines.

The November 2025 selloff illustrated this asymmetry concretely. TechnologyOne fell approximately 17% on sector sentiment, not on a fundamental earnings shock. At high multiples, the margin for error is thin: even a modest earnings miss or a shift in macro conditions can produce a sharp price response.

The analytical observation is clear. All four businesses delivered strong earnings. All four trade at steep premiums. The question that remains is how an individual investor should weigh those two facts against each other.

Several variables matter when evaluating whether a premium multiple is justified:

Broker views on these four stocks reflect genuine disagreement. Directional research suggests Pro Medicus carries a broadly constructive Buy consensus. WiseTech draws mixed views, with Citi reported as constructive and UBS more cautious on relative valuation. Xero is generally characterised as fairly valued, with its AI accounting copilot cited as a potential upsell catalyst. These assessments are directional and sourced from broker commentary that has not been independently verified; investors should consult current broker platforms for live consensus data.

Institutional activity paints a similarly divided picture. The net lean following the November 2025 and January 2025 compression events appears to favour holding or adding, but meaningful pockets of profit-taking persist. Fund managers with long-duration mandates and those with shorter-term valuation discipline reach different conclusions about the same stocks, which is itself informative.

The structural bear argument is straightforward. At 56-68x earnings, even modest earnings disappointments or upward shifts in interest rate expectations can trigger disproportionate share price falls, regardless of whether the underlying business remains operationally strong. Growth stocks are long-duration assets; their valuations carry greater sensitivity to discount rate changes than lower-multiple value stocks.

The November 2025 episode provided a live demonstration. A sector-wide sentiment shift, not a deterioration in any individual company’s fundamentals, was sufficient to send TechnologyOne down approximately 17%. At lower multiples, the same sentiment event would have produced a smaller price impact. The premium amplifies both upside and downside, and that asymmetry is the risk that P/E ratios alone do not convey.

The verified earnings data supports the quality thesis for all four companies. Pro Medicus, WiseTech Global, TechnologyOne, and Xero are growing revenue at 18-76%, integrating AI into their product suites, and retaining the recurring revenue structures that underpin premium valuations. The DeepSeek panic and November 2025 selloff provided a live case study in how external forces can compress premium multiples even when fundamentals remain intact.

Whether that quality justifies paying 56-68x trailing earnings depends on variables this analysis cannot resolve for the reader: individual time horizon, risk tolerance, and forward growth assumptions. If revenue growth rates sustain or accelerate, the multiples compress naturally over time. If growth disappoints or macro conditions tighten, the asymmetric downside of high multiples becomes the dominant risk.

Investors evaluating these stocks may benefit from focusing on the quality criteria outlined above, revenue consistency, switching costs, margin trajectory, and competitive durability, before anchoring on the P/E figure alone. The multiple is the price of admission. The business underneath determines whether it was worth paying.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

All verified data used throughout this article reflects conditions as of early May 2026. Multiples shift continuously, and investors should verify current figures before acting.

A price-to-earnings (P/E) ratio compares a company's share price to its earnings per share, giving investors a measure of how much they are paying for each dollar of profit. For ASX tech stocks like Pro Medicus and WiseTech Global, high P/E ratios of 56-68x reflect the market pricing in strong future earnings growth rather than just current profitability.

Pro Medicus, WiseTech Global, TechnologyOne, and Xero trade at 3.3x to 4.3x the ASX 200 forward multiple because investors pay a scarcity premium for businesses with durable competitive advantages, high switching costs, and recurring revenue structures that are rare on the Australian market.

The PEG ratio divides a company's P/E ratio by its earnings growth rate, with a reading of 1.0x often treated as fair value for a growth stock. Pro Medicus at roughly 58x earnings and 28.4% revenue growth implies a PEG near 2.0x, suggesting the market is pricing in sustained growth beyond what the latest result alone justifies.

The emergence of DeepSeek in January 2025 triggered a sharp selloff in ASX tech stocks on fears that open-source AI would erode software switching cost moats, but the earnings results that followed showed each of the four companies integrating AI as a product enhancer rather than suffering competitive damage.

At 56-68x earnings, even modest earnings disappointments or rising interest rate expectations can trigger disproportionate share price declines because growth stocks are long-duration assets sensitive to changes in discount rates. The November 2025 selloff, which sent TechnologyOne down approximately 17% on sentiment alone rather than any fundamental deterioration, illustrated this asymmetry concretely.