The Memo That Halved Meta’s AI Infrastructure Cost Estimate

4 hrs ago

On 27 January 2025, Nvidia shed $589 billion in market capitalisation in a single session, the largest single-day loss in corporate history. Thousands of kilometres away, ASX-listed data centre stocks absorbed a simultaneous blow. DigiCo Infrastructure REIT fell 11%. NextDC dropped as much as 9.4% intraday.

The trigger was DeepSeek-R1, a Chinese-built AI model that reportedly cost less than $6 million to train and performed competitively with models built on hardware costing orders of magnitude more. For investors who had backed ASX data centre and AI infrastructure stocks on the premise that the AI boom required ever-greater compute capacity, the question was immediate: if AI gets dramatically cheaper, does the infrastructure thesis collapse?

What followed over 16 months provides one of the clearest case studies available for evaluating how competitive disruption events propagate through the ASX’s AI infrastructure cohort, why the initial selloff misread the underlying economics, and what the recovery teaches investors about positioning in the sector.

DeepSeek-R1 was released on 20 January 2025. The global market reaction concentrated on Monday, 27 January 2025, when the scale of the destruction became visible within hours of the US open.

The market logic driving the selloff was specific: if AI training and inference become dramatically cheaper, the capital expenditure supercycle driving data centre demand could slow, making infrastructure investment look over-capitalised. DeepSeek-V3 had reportedly been trained for under $6 million. DeepSeek-R1 was reported to be 20-50x cheaper to operate than OpenAI equivalents. The implication, as markets read it in real time, was that the billions being spent by hyperscalers on compute infrastructure might not be necessary at the scale being planned.

The key global market moves on 27 January 2025:

Marc Andreessen posted on X (formerly Twitter) on or around 27 January 2025: “DeepSeek R1 is AI’s Sputnik moment,” a framing widely interpreted as acknowledging a serious competitive and geopolitical shift in AI development.

The panic was real. Whether the logic behind it was sound is what the subsequent 16 months would test.

The ASX reaction was not random contagion. It reflected real investor logic about AI capital expenditure, and it hit the sector’s most prominent names in sequence.

NextDC (NXT) fell up to 9.4% intraday on 27 January 2025 before partially recovering. Goodman Group (GMG) experienced downward pressure across 27-28 January. DigiCo Infrastructure REIT (DGT) dropped 11% on 28 January 2025, the sharpest single-day move among the three.

Australian financial media, including Reuters and ABC News, covered the selloff in real time. The framing from analysts, however, was not uniformly bearish from day one.

| Stock | Intraday move | Approx. stabilisation | Initial analyst call |

|---|---|---|---|

| NextDC (NXT) | Down 9.4% | March 2025 | IG Australia: positive sector outlook maintained |

| Goodman Group (GMG) | Down (pressure 27-28 Jan) | March 2025 | Constructive longer-term view from brokers |

| DigiCo (DGT) | Down 11% | March 2025 | UBS: buy, 32% upside target |

UBS issued a buy recommendation on DigiCo on 28 January 2025, citing 32% upside. The call was made within 24 hours of the selloff, making it one of the earliest named broker recommendations to frame the dislocation as an opportunity rather than a signal.

Daniel Morgan, Senior Portfolio Manager at Synovus Trust Company, argued on or around 27 January that DeepSeek competed with ChatGPT for consumer use cases, not with data centre infrastructure. The distinction mattered. Professional capital was already reassessing the thesis before the week was out.

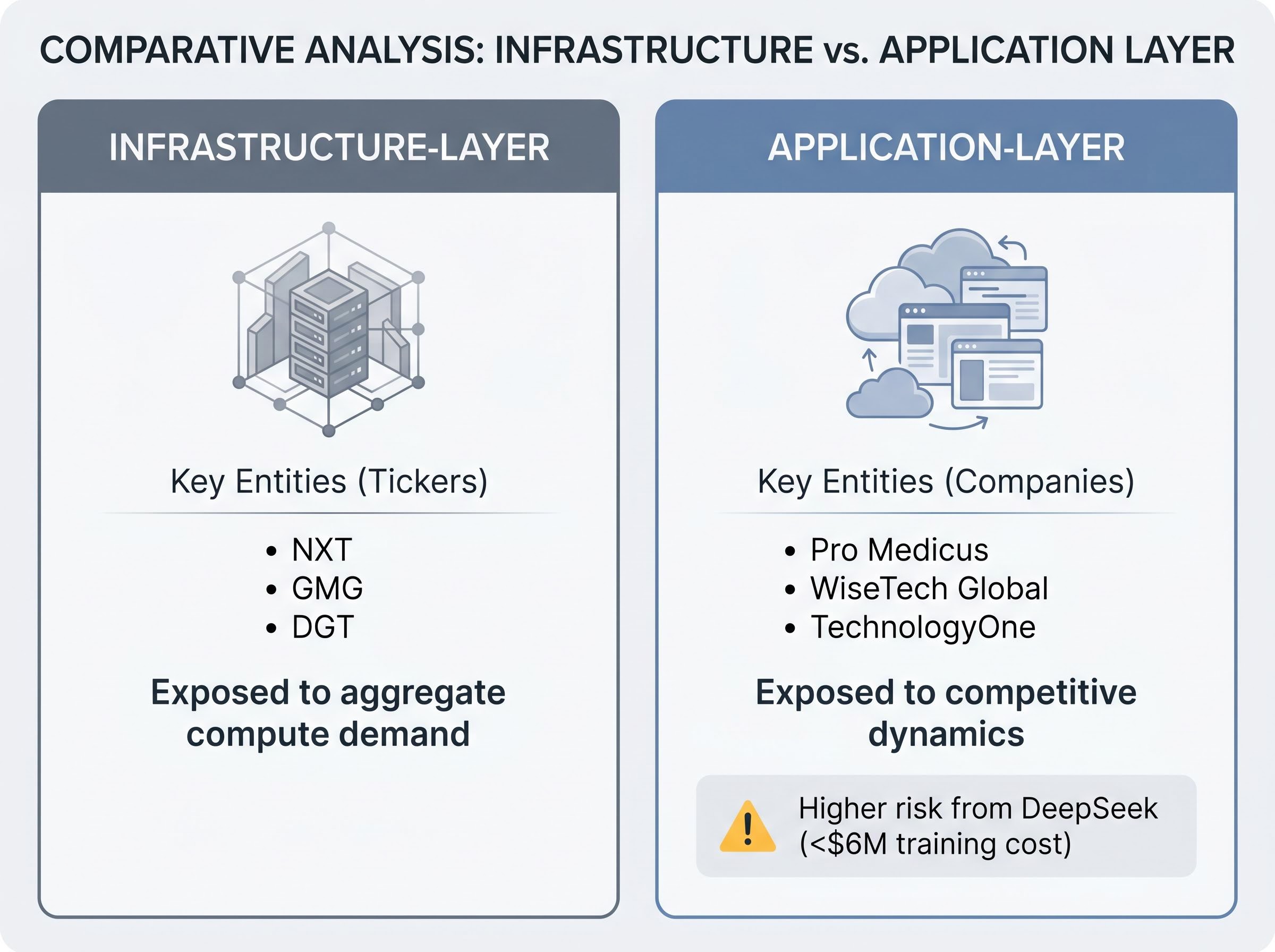

The selloff treated all AI-adjacent stocks as though they faced the same risk. They did not. The difference lies in where a company sits in the AI supply chain.

The “picks and shovels” investment concept holds that regardless of which AI model or platform ultimately wins market share, the physical infrastructure enabling all of them, including data centres, power, connectivity, and cooling, must be built and maintained. A gold rush rewards the people selling shovels whether the miners strike gold or not.

The structural context for ASX AI infrastructure investment extends beyond any single disruption event: Australia’s data centre capacity is projected to more than double from 1,350 MW to 3,100 MW between 2024 and 2030, requiring an estimated A$26 billion in new capital, a buildout that was already committed and contracting before DeepSeek entered the picture.

Applied to the ASX, the distinction separates two groups:

DeepSeek’s training cost of under $6 million, compared to the billions spent by US hyperscalers on comparable model development, was a competitive threat to model developers. It was not, by the same logic, a threat to the physical facilities those models run on.

The Jevons Paradox describes a pattern observed since the 19th century: when a technology becomes more efficient and cheaper to use, total consumption of that technology typically increases rather than decreases. Efficiency gains expand the pool of users and use cases rather than shrinking demand.

Applied to DeepSeek: a 20-50x reduction in inference cost means AI becomes viable for vastly more applications, businesses, and consumers. More adoption means more queries, more processing, more data, and more demand on the physical infrastructure that handles all of it.

This argument was present in analyst commentary from late January 2025 and was cited extensively in retrospective analysis through 2026. The efficiency that spooked markets was, by this logic, the very force that would accelerate infrastructure demand.

FAccT ’25 research on Jevons Paradox rebound effects in AI systems provides an academic grounding for this argument, demonstrating that efficiency-driven cost reductions in technology historically expand total consumption rather than contracting it, a pattern directly applicable to the inference cost dynamics DeepSeek introduced.

The evidence arrived in stages. By March 2025, ASX AI infrastructure stocks had largely stabilised. Through the remainder of 2025 and into 2026, the trajectory turned upward.

DigiCo provided the most concrete corporate signal that operators themselves were not pulling back. The company announced the US$750 million sale of CHI1, its Chicago data centre asset, with proceeds directed to the SYD1 expansion in Australia. This was not a defensive retrenchment; it was a capital recycling decision that committed significant resources to domestic growth in the wake of the panic.

DigiCo’s CHI1 sale for US$750 million was confirmed in May 2026 alongside CDC Data Centres signing the largest data centre contract in Australian history at 555MW, a pairing of announcements that made the same week one of the most consequential for Australian digital infrastructure capital allocation since the sector’s ASX listing cycle began.

Goodman Group reported increased data centre leasing rates in the months following the selloff. NextDC continued expansion in Sydney and Melbourne, with infrastructure buildout maintained despite the January volatility. Government energy policy and data sovereignty requirements provided structural tailwinds for facilities in Canberra and Brisbane.

| Company | Approx. performance (post-shock to mid-2026) | Key catalyst |

|---|---|---|

| DigiCo (DGT) | ~23% gain | CHI1 sale (US$750M), SYD1 expansion |

| NextDC (NXT) | Recovery and expansion | Continued Sydney/Melbourne buildout |

| Goodman Group (GMG) | Recovery and expansion | Increased data centre leasing rates |

Retrospective analysis from Livewire Markets and Wealth Within framed 27 January 2025 as a buying opportunity for ASX data centre names, with DigiCo’s approximately 23% gain to mid-2026 cited as a key data point supporting the thesis.

By 2026, NXT, GMG, and DGT appeared as top picks in both domestic and international sector outlooks. The performance data, rather than commentary alone, confirmed what the contrarian thesis had argued within hours of the selloff.

The core investor error on 27 January 2025 was conflating competitive disruption at the model layer with structural risk at the infrastructure layer. DeepSeek threatened AI software economics. It did not threaten the demand for physical compute capacity; it arguably accelerated it.

A supply-chain mapping discipline can prevent that conflation from recurring. Three steps apply to any future disruption event:

Step one applied to NextDC, Goodman Group, or DigiCo immediately redirects the analytical question. These are infrastructure-layer companies. The question is not “which AI model wins?” but “does aggregate compute demand grow?”

Step two: DeepSeek did not create a substitute for data centre capacity. No AI model runs without physical infrastructure, regardless of how cheaply it was trained.

Step three: cheaper inference costs expand adoption. More users, more queries, more demand on the underlying infrastructure. The demand direction pointed upward.

Contrast this with an ASX SaaS name such as TechnologyOne (TNE), which fell approximately 17% during the ASX technology sector selloff around November 2025. Application-layer companies face genuine substitution risk when cheaper competitors emerge. The analytical conclusion differs at step two, and the investment response should differ accordingly.

The software repricing dynamics that DeepSeek accelerated extended well beyond January 2025, culminating in a $2 trillion wealth destruction event across US legacy software markets in early 2026 as AI-native alternatives threatened to commoditise per-unit licensing models, a trajectory that ran in the opposite direction to infrastructure-layer performance over the same period.

CNBC observed on 6 January 2026 that DeepSeek’s 2025 shock did not cause a repeat investor frenzy when new AI developments emerged, attributing this to a more sophisticated market understanding of AI infrastructure demand dynamics. The framework, in other words, was already propagating through professional capital.

The 27 January 2025 selloff functioned as an involuntary stress test. It imposed a sudden, severe sentiment shock on infrastructure stocks whose underlying demand fundamentals were, by the subsequent evidence, intact.

DigiCo’s approximately 23% recovery to mid-2026, NextDC and Goodman Group’s continued expansion, and UBS’s 28 January buy call being validated over the following months collectively confirm the picks-and-shovels logic in specific, measurable terms, not as a vague thematic narrative.

The efficiency-adoption argument that emerged in analyst commentary from late January 2025, consistent with the Jevons Paradox, held that competitive disruption events in AI modelling are more likely to increase than decrease long-run infrastructure demand. The subsequent 16 months bore that argument out.

Three durable takeaways from the episode:

Global outlook pieces from Seeking Alpha, Yahoo Finance, and domestic research through 2026 continued to flag Australian data centre operators as beneficiaries of sustained AI capital expenditure. The question that separates investors who will benefit from future disruption events from those who will not remains the same one the DeepSeek episode posed: does this development accelerate or decelerate total AI adoption?

The DeepSeek shock was a sentiment-driven reprice of infrastructure stocks, not a fundamental signal. The subsequent 16 months confirmed that distinction through stock performance, corporate capital allocation, and the sustained expansion of ASX data centre operators.

The picks-and-shovels thesis held because infrastructure demand is a function of aggregate AI adoption, not of which model leads. The Jevons Paradox held because efficiency gains expanded the user base rather than contracting it.

AI model competition will intensify. Future efficiency breakthroughs are probable. The analytical framework developed from the DeepSeek episode, mapping supply chain position, assessing substitutability, and tracing demand direction, transfers directly to evaluating those events. The case study is resolved. The tools it produced are not time-limited.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

ASX AI infrastructure stocks are companies such as NextDC, Goodman Group, and DigiCo Infrastructure REIT that own or operate physical data centre assets, power, and connectivity facilities that enable AI computing, regardless of which AI model or platform leads the market.

Markets initially feared that DeepSeek's low training cost (under $6 million) signalled a slowdown in hyperscaler capital expenditure on compute infrastructure, causing investors to sell AI-adjacent stocks including NextDC, Goodman Group, and DigiCo before the underlying demand logic was reassessed.

Historical evidence and the Jevons Paradox suggest the opposite: when AI becomes cheaper to run, more businesses and consumers adopt it, increasing the total number of queries and processing tasks and therefore raising aggregate demand on the physical infrastructure that handles them.

DigiCo recovered approximately 23% from its post-shock lows to mid-2026, supported by the US$750 million sale of its CHI1 Chicago data centre and the commitment of those proceeds to its SYD1 expansion in Australia.

Investors should identify whether the company operates at the infrastructure layer (data centres, power, connectivity) or the application layer (software, platforms, AI models), because infrastructure-layer stocks are exposed to aggregate compute demand while application-layer stocks face direct substitution risk from cheaper AI alternatives.