Westpac’s FY25 full-year dividend of $1.53 per share translates to a trailing yield of 3.98% at the current share price of $38.43, a materially better entry point than the highs above $41 that WBC.AX touched in 2025. For income investors, the question is not whether the yield looks acceptable today, but whether the dividend trajectory through FY27 and FY28 justifies a long-term position.

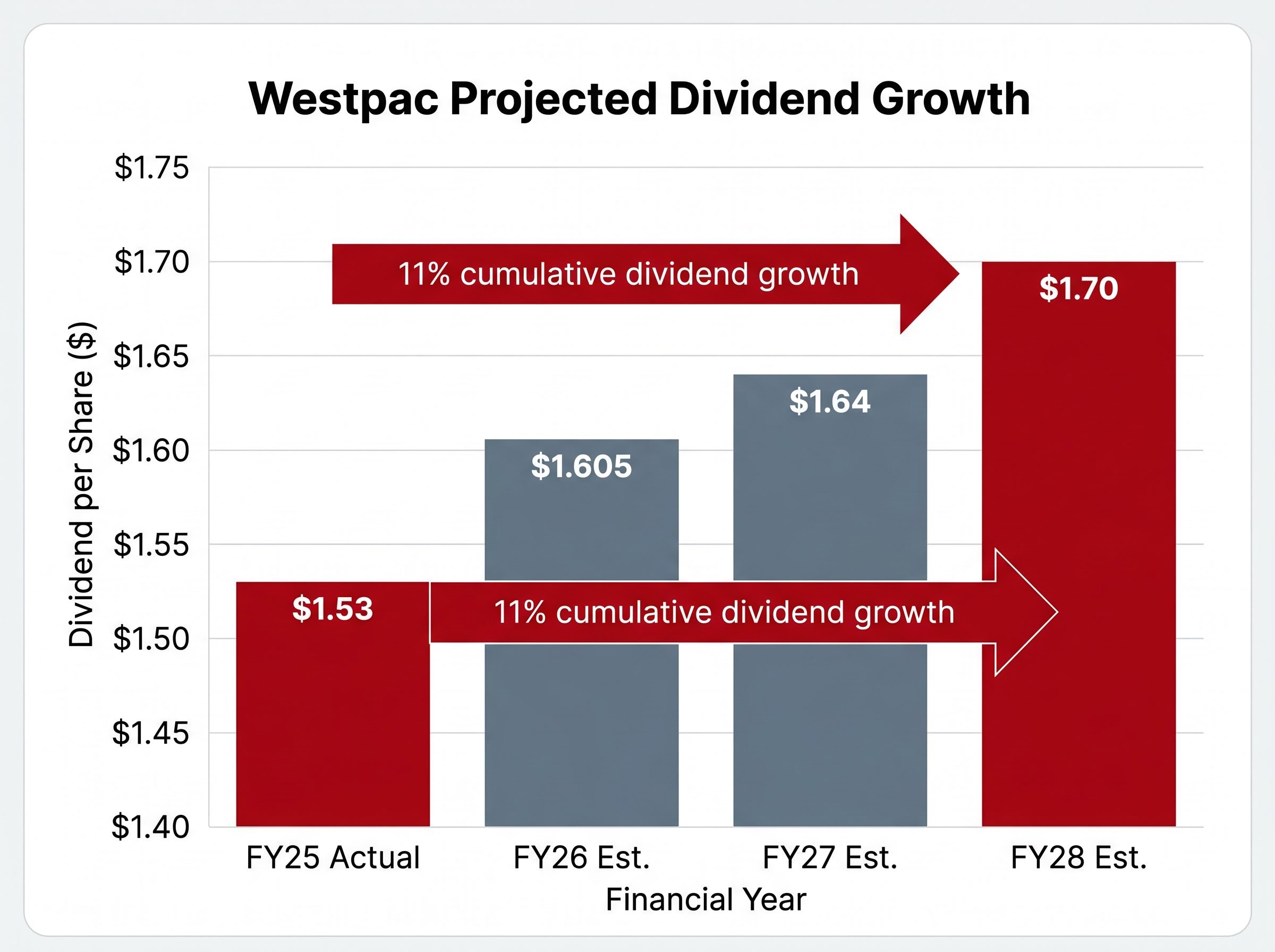

Analyst projections point to $1.605 per share in FY26, $1.64 in FY27, and $1.70 in FY28. These numbers sit inside a fast-moving environment: RBA rate decisions expected through mid-2026, an ongoing technology transformation programme with rising costs, and one of the most competitive mortgage markets in the bank’s recent history. The FY26 half-year results due on 5 May 2026 will provide the first formal read on whether Westpac’s current trajectory supports or complicates those forecasts.

What follows works through each layer of that question systematically, giving income-focused investors a structured framework for evaluating Westpac’s dividend reliability through to FY28, including what to watch, what could go wrong, and how franking credits change the effective return calculation.

Where Westpac’s dividend stands today: yield, franking, and the May 5 catalyst

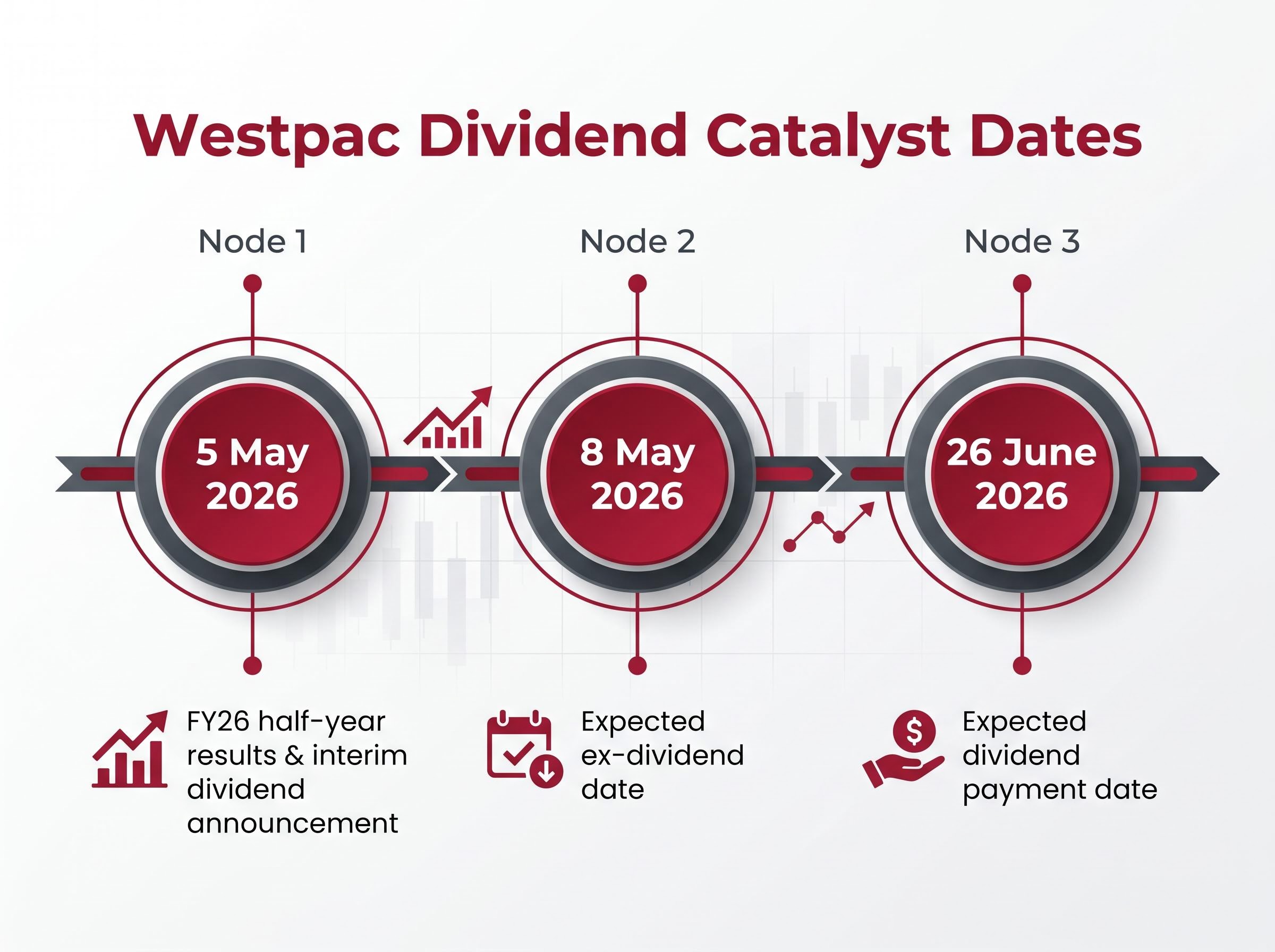

The income picture starts with confirmed numbers. Westpac closed at $38.43 on 30 April 2026, and its FY25 full-year dividend of $1.53 per share produces a trailing yield of 3.98%. The bank pays dividends semi-annually (interim plus final), and the FY26 interim dividend is expected at approximately $0.82, pending confirmation at the half-year results announcement on 5 May 2026.

Three dates matter in the near term:

- 5 May 2026: FY26 half-year results and interim dividend announcement

- 8 May 2026: Expected ex-dividend date

- 26 June 2026: Expected dividend payment date

That 3.98% headline yield, however, materially understates the return for a large segment of the Australian investor base. Westpac dividends are fully franked, meaning the 30% corporate tax already paid by the bank flows to eligible shareholders as a franking credit.

For eligible Australian investors, Westpac’s fully franked dividends translate to a grossed-up yield in the range of 4.1% to 6%, depending on individual tax circumstances.

For self-managed super fund (SMSF) trustees in pension phase, the effective return sits at the upper end of that range. The 5 May announcement is the single most important near-term catalyst for confirming whether FY26 is tracking to plan.

When big ASX news breaks, our subscribers know first

What analyst forecasts say about FY26, FY27, and FY28

The FY26 consensus from late 2025 clusters in the $1.55-$1.58 per share range, based on estimates compiled by CommSec and DivvyDiary. CMC Invest’s projection sits higher at $1.605, a figure that should be weighed with the understanding that it exceeds the broader consensus.

Looking further out, CMC Invest projects $1.64 for FY27 and $1.70 for FY28. At the current share price of $38.43, these translate into a rising forward yield profile.

| Financial Year | Projected Dividend (per share) | Forward Yield at $38.43 | Grossed-Up Yield (est.) |

|---|---|---|---|

| FY25 (actual) | $1.53 | 3.98% | ~5.7% |

| FY26 (CMC Invest) | $1.605 | ~4.18% | ~5.97% |

| FY27 (CMC Invest) | $1.64 | ~4.27% | ~6.1% |

| FY28 (CMC Invest) | $1.70 | ~4.43% | ~5.7% |

The trajectory from $1.53 to a projected $1.70 represents approximately 11% cumulative dividend growth across three years. That is modest but consistent, and meaningful when layered on top of franking credit returns. Supporting the near-term picture, Westpac’s Q1 FY26 quarterly profit came in at $1.9 billion, reflecting 5%-6% growth compared to the second-half FY25 average.

Westpac’s Q1 FY26 operating performance, including $22 billion in lending growth and $12 billion in deposit inflows during the quarter, provides the most recent evidence that core franchise momentum has continued into the current financial year, even as the share price has given up its gains since the start of 2026.

How much confidence should investors place in these numbers?

There is a material distinction between the FY26 consensus range (compiled from multiple broker estimates) and the FY27-FY28 figures, which rely on a single source. No independently verified FY27 or FY28 forecasts from institutional brokers such as Morgan Stanley, UBS, Macquarie, or Citi were publicly available at the time of writing.

The 5 May 2026 half-year results will be the first opportunity to calibrate whether FY26 is tracking toward the lower consensus or the higher CMC projection. Investors seeking institutional views should consult post-May 5 research publications.

How Australian interest rates will shape Westpac’s earning power through FY28

The mechanism is straightforward: when the RBA raises rates, the spread between what Westpac pays for deposits and what it charges on loans tends to widen. That spread, the net interest margin (NIM), is the primary engine of bank profitability, and profitability determines how much the board can sustainably pay in dividends.

As of 30 April 2026, the RBA cash rate sits at 4.10% following a 25 basis point hike in March. The expected path forward involves three further increases:

Australia’s inflation trajectory sits at the centre of the rate outlook: headline CPI reached 4.6% in March 2026, nearly double the top of the RBA’s 2-3% target band, with trimmed mean inflation at 3.3% suggesting the acceleration is partly driven by volatile energy prices rather than a uniform deterioration in underlying conditions.

- May 2026: 25bps hike to 4.35%

- June 2026: 25bps hike to 4.60%

- August 2026: 25bps hike to approximately 4.85% (peak, per Westpac’s economics team projection)

Rate cuts are not anticipated before 2027.

On paper, this is a tailwind for bank margins. In practice, Westpac’s FY25 result complicates the picture. Net profit fell to $6.99 billion, with fierce mortgage price competition cited as a contributing factor. The bank is lending at tighter margins to defend market share, which limits how much of the rate benefit reaches the bottom line.

While higher rates expand the spread between Westpac’s deposit costs and lending returns, the competitive mortgage market limits how much of that expansion flows through to profit and dividends.

For the FY27-FY28 dividend projections to hold, Westpac needs the rate tailwind to outweigh competitive margin compression. That balance is the single most important variable in the earnings outlook.

What franking credits actually mean for Australian income investors

Most Australian investors understand that franking credits are beneficial. Fewer can quantify exactly how they change the return on a specific holding. The mechanics are worth working through with real numbers.

When Westpac pays a fully franked dividend, the 30% corporate tax the bank has already paid on those earnings is attached as a credit. Eligible shareholders can use that credit to offset their own tax liability on the dividend income. For the FY25 dividend of $1.53 per share, the grossed-up value is calculated as $1.53 / (1 – 0.30) = approximately $2.19 per share.

At a share price of $38.43, that grossed-up figure produces a yield of approximately 5.7%, well above the 3.98% cash yield. The benefit, however, is not uniform.

Grossed-up yield by investor type

The same $1.53 dividend translates to different effective yields depending on the holder’s tax position:

- SMSF in pension phase (0% tax): Receives the full franking credit as a cash refund, producing the highest effective yield in the ~5.7% range

- Investor in the 32.5% marginal bracket: Pays a small top-up tax on the grossed-up amount, but still receives a materially higher after-tax return than the headline yield suggests

- Investor in the 45% top bracket: The franking credit offsets a portion of the tax liability, but the net benefit is smaller; effective yield is closer to the cash dividend yield

For SMSF trustees and retirees building passive income portfolios, the franking credit component shifts Westpac’s headline yield from competitive into genuinely compelling territory, a distinction that raw yield comparisons to term deposits or international equities would miss.

Individual circumstances vary, and readers should seek personal tax advice.

The risks that could derail Westpac’s dividend growth trajectory

The forecast numbers assume a baseline that holds. Three specific mechanisms could break it.

- UNITE programme cost overruns and operational drag: Costs for the single mortgage system component of Westpac’s UNITE technology programme have risen to $285 million, up from a prior $265 million estimate. In Q1 FY26 alone, $195 million was invested, with 57 initiatives still in scope. If costs continue to escalate, the programme absorbs capital that would otherwise support dividend growth.

- Competitive NIM compression in mortgage lending: FY25 net profit of $6.99 billion already reflected margin pressure from mortgage pricing competition. Analysts do not expect this pressure to ease materially through the FY27-FY28 window.

- Credit quality deterioration if RBA hikes exceed expectations: If the cash rate reaches its projected peak of approximately 4.85% and cuts are delayed beyond 2027, mortgage arrears and defaults could rise, creating a credit cost headwind that directly affects dividend capacity.

| Risk Factor | Trigger Condition | Dividend Metric to Watch |

|---|---|---|

| UNITE cost overruns | Programme costs exceed revised $285M estimate | Payout ratio, free capital generation |

| Mortgage margin compression | NIM declines despite rising cash rate | NIM disclosure in half-year results |

| Credit quality deterioration | Cash rate holds above 4.5% into 2027 | Arrears rate, impairment charges |

None of these risks individually makes the dividend forecast implausible. Collectively, they define the conditions under which the $1.64 and $1.70 projections would need to be revised downward, and monitoring them gives investors the earliest possible signal that the thesis is changing.

Broker consensus price targets clustering 8-11% below the current share price represent the most direct challenge to total return assumptions for income investors: a move toward the Morgans price target of A$34.04 would erase multiple years of dividend income, meaning the yield analysis in isolation understates the full risk of holding at current levels.

What Westpac’s dividend record tells income investors about long-term reliability

Zooming out from the near-term risks, Westpac’s historical payout behaviour offers a useful anchor. The bank has maintained a consistent semi-annual dividend cadence for over a decade, with one notable exception: the 2020 cut, driven by the COVID-19 pandemic and regulatory pressure from APRA, not by structural balance sheet weakness.

APRA’s capital adequacy standard for ADIs sets the capital conservation buffer requirements that directly constrain how much of a bank’s earnings can be distributed as dividends, meaning Westpac’s payout decisions operate within a regulatory ceiling that can tighten if capital ratios come under pressure.

Westpac’s 2020 dividend cut was regulator-influenced and pandemic-driven, not a signal of structural earnings weakness. In every other year across the past decade, the bank maintained or grew its payout.

Three structural indicators support the forward reliability of that track record:

- Consistent semi-annual cadence maintained across interest rate cycles and competitive environments

- Fully franked status preserved through downturns, confirming sufficient taxable earnings to support the credit

- Growing direct-channel residential lending origination, which increased for the second consecutive quarter in FY26, a positive signal for margin retention as the bank reduces reliance on broker-originated loans

The share price decline from the 2025 highs above $41 to the current $38.43 has also improved the entry proposition for new buyers. On the same $1.53 dividend, the trailing yield moved from approximately 3.73% at $41 to 3.98% at $38.43. No change in dividend policy was required; the price did the work.

A single dividend cut in over ten years, driven by an unprecedented global event, is the kind of track record income investors in ASX financials evaluate favourably. It does not eliminate risk, but it contextualises the reliability of the forward projections.

Westpac as a passive income holding: what the FY27-FY28 forecasts are really saying

The multi-year picture is straightforward. From the confirmed FY25 base of $1.53, through the FY26 consensus range and the higher CMC projections, to a projected $1.70 in FY28, the trajectory implies approximately 11% cumulative dividend growth across three years. That pace is modest, gradual, and consistent with Westpac’s historical growth rate.

At the current price, the FY28 grossed-up yield reaches approximately 5.7% for eligible Australian investors, a figure that would compare favourably to most fixed-income alternatives if it materialises.

Whether it materialises depends on specific events in the next six months. Investors monitoring this thesis should watch three catalysts:

- 5 May 2026: Half-year results, interim dividend amount, NIM commentary, and UNITE cost update

- May and June 2026 RBA decisions: Confirmation or deviation from the expected rate path to 4.85%

- UNITE programme cost disclosures in the half-year results, particularly whether the $285 million mortgage system estimate holds

Westpac is a structurally sound dividend payer for Australian income investors. The $1.64-$1.70 trajectory, however, assumes competitive pressures do not intensify further and that the UNITE programme delivers its intended efficiency benefits within budget. Income investors do not need certainty to make a position decision; they need a clear picture of what they are buying, what could change it, and when they will know.

For investors comparing yield across the Big Four before allocating fresh capital, our dedicated guide to CBA’s dividend case examines CBA’s fully franked yield, its two-decade uninterrupted payment record, and how the effective gross yield for SMSFs in pension phase compares directly to Westpac’s current income proposition at equivalent entry prices.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.