Australia’s headline inflation rate surged to 4.6% in March 2026, the sharpest monthly acceleration in recent memory and a reading that sits well above the Reserve Bank of Australia’s (RBA) 2-3% target band. The Australian Bureau of Statistics (ABS) released the figures on 29 April 2026, just days before the RBA’s Monetary Policy Board meets on 4-5 May. Markets are now pricing a 62% probability of a further 25 basis point increase, which would lift the cash rate to 4.35% and extend a tightening cycle that delivered its most recent hike as recently as 17 March.

The data lands against a backdrop of energy-driven price pressures, a resilient housing market, and a widening gap between RBA and Federal Reserve policy that is pushing the Australian dollar higher. What follows explains what the March CPI data actually shows, why energy prices are doing so much of the inflation work, what another rate hike would mean for mortgage holders and borrowers, and how the RBA-Fed policy divergence is reshaping the Australian dollar.

Australia’s inflation just hit 4.6%: here is what the March CPI data actually shows

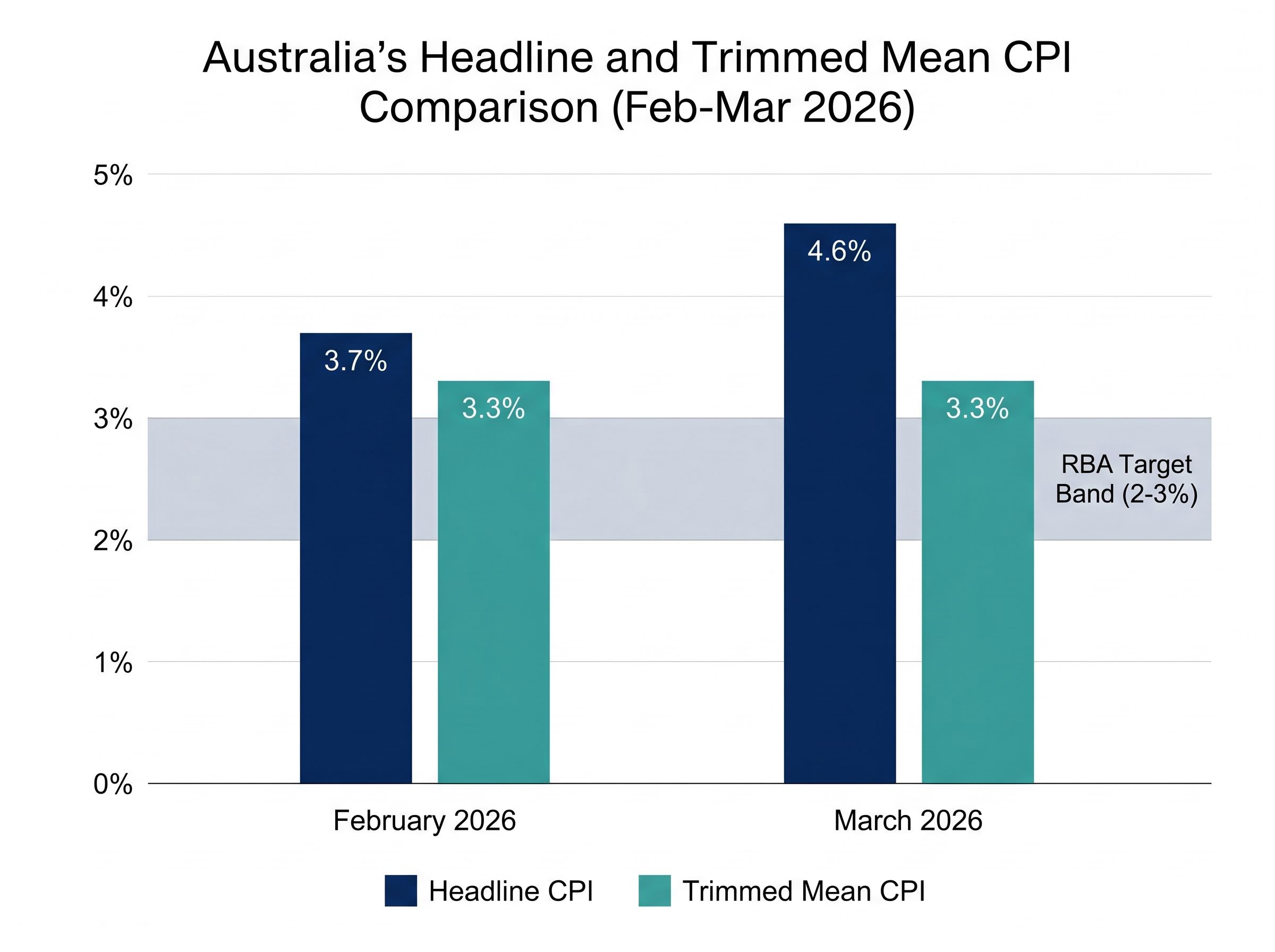

The number that matters most this week is 4.6%. That is Australia’s headline Consumer Price Index for March 2026, up from 3.7% in February, a move of nearly a full percentage point in a single month. It is the widest margin above the RBA’s 2-3% target band in the current cycle.

The complication sits underneath the headline. Trimmed mean CPI, the measure that strips out the most volatile price movements to capture underlying inflation, held steady at 3.3% in March, unchanged from February. That divergence is what makes this release difficult to interpret cleanly: the headline number screams urgency, while the underlying measure suggests the breadth of price pressures has not worsened.

Trimmed mean CPI strips out the most volatile price movements in any given month, including sharp fuel or food swings, to isolate the persistent inflation pressures that monetary policy is best positioned to address; the measure is designed precisely to prevent a single-category spike from distorting the policy signal.

| Measure | February 2026 | March 2026 |

|---|---|---|

| Headline CPI | 3.7% | 4.6% |

| Trimmed Mean CPI | 3.3% | 3.3% |

The RBA’s Monetary Policy Board stated in its March decision that “inflation is likely to remain above target for some time and that the risks have tilted further to the upside.”

Headline CPI is the figure that shapes political pressure, media coverage, and household anxiety. The trimmed mean is the figure the RBA watches most closely for policy calibration. Both are above target. Only one of them just accelerated sharply.

When big ASX news breaks, our subscribers know first

Energy prices are the engine driving inflation higher

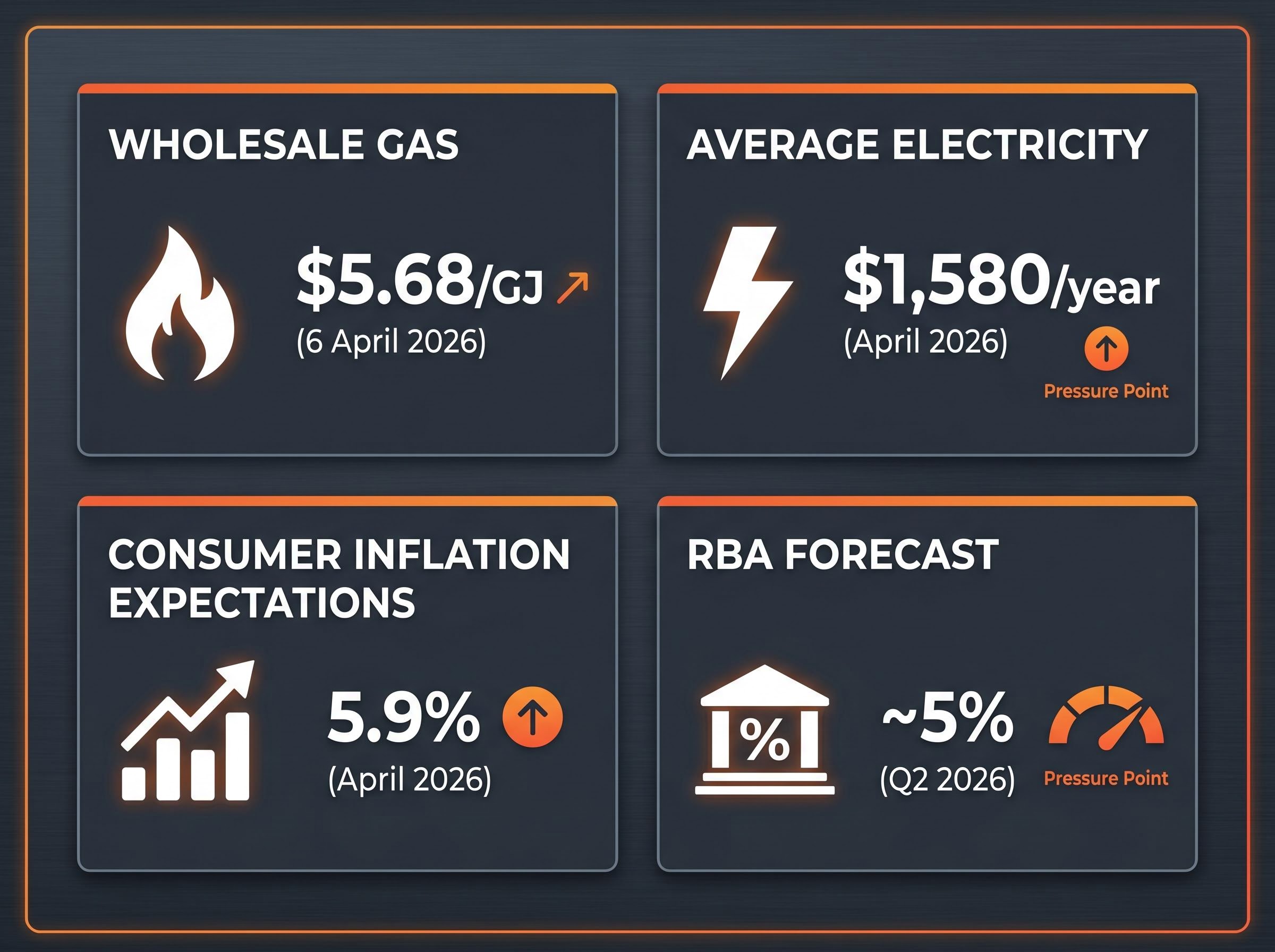

The gap between headline and trimmed mean CPI points directly at volatile items, and energy sits at the centre. The RBA’s own Q2 2026 forecasts project headline inflation reaching approximately 5%, with fuel and energy costs doing much of the work.

The domestic pricing data reinforces that picture:

- Wholesale gas prices stood at $5.68/GJ as of 6 April 2026

- National average electricity costs reached $1,580 per year in April 2026

- The RBA’s Q2 2026 headline inflation forecast sits at approximately 5%, driven substantially by energy inputs

Global oil market pressures, particularly tensions in the Middle East, are feeding directly into Australian fuel costs. Deputy Governor Andrew Hauser, speaking in New York, characterised the situation as an “oil crisis” causing a “big income shock” for Australian households.

Deputy Governor Hauser warned of a potential “nightmare” stagflation scenario, with inflation remaining too high for too long while economic growth slows.

This is the structural difficulty the RBA faces. Energy inflation is not something higher interest rates can cure directly; monetary policy can only suppress broader demand to prevent energy costs from feeding into wages and services prices. The tool is necessary but blunt, and the March CPI data shows it has not yet contained the headline figure.

Oil futures backwardation, where near-term contracts trade above longer-dated ones, signals that institutional capital views the current supply disruption as temporary; if the market is right, the energy-driven gap between headline and trimmed mean CPI would narrow materially over the following two to three quarters without requiring additional tightening from the RBA.

What the RBA cash rate is and why it matters for every Australian borrower

The RBA cash rate is the interest rate on overnight loans between commercial banks. It is the single most influential lever in Australian monetary policy because it determines the cost of wholesale funding for the entire banking system. When the RBA raises the cash rate, banks face higher borrowing costs, and those costs flow through to retail lending rates, including variable-rate mortgages, personal loans, and business credit.

The current cash rate is 4.10%, set at the board meeting on 17 March 2026. That decision was not a one-off; it extended a sustained tightening cycle aimed at returning inflation to the 2-3% target band. Consumer inflation expectations in April 2026 reached 5.9%, according to survey data, a level that risks becoming self-fulfilling if households and businesses begin setting prices and wages based on those expectations.

The RBA’s 2-3% inflation target band is the formal framework that governs how the board interprets CPI data and calibrates the cash rate, with the November 2025 Statement on Monetary Policy confirming that the board will maintain tightening pressure until underlying inflation returns sustainably within that range.

Markets are pricing a 62% probability that the board will deliver another 25 basis point increase at its 4-5 May meeting, which would take the cash rate to 4.35%.

How the RBA cash rate flows through to your mortgage

The transmission from an RBA decision to a household repayment change follows a predictable sequence:

- The RBA raises the cash rate at its board meeting

- Commercial banks reprice their wholesale funding costs to reflect the new rate

- Banks adjust variable mortgage rates, typically within days to weeks of the decision

- Monthly repayments increase for borrowers on variable-rate products

Not all lenders pass through rate changes at identical speed or magnitude. Some major banks adjust within days; smaller lenders and non-bank providers may take longer. The practical effect for a borrower on a variable rate is that each 25 basis point increase adds to the monthly repayment burden, compounding across the multiple hikes already delivered in this cycle.

May 4-5 is the date: what markets and economists expect the RBA to do

The 62% market probability of a hike captures genuine division, not a consensus with a small margin of doubt. The arguments on both sides carry weight, and the board’s decision will depend on how it weighs headline severity against underlying stability.

The case for hiking

- Headline CPI at 4.6% is now nearly double the top of the RBA’s target band, and the Q2 forecast of approximately 5% suggests the peak has not yet arrived

- Consumer inflation expectations at 5.9% risk becoming embedded in wage negotiations and price-setting behaviour, a self-reinforcing dynamic the RBA is determined to prevent

- Deputy Governor Hauser stated that rates “will have to go to a level that bring[s] inflation back to target” if needed, signalling the board’s willingness to act

The case for holding

- Trimmed mean CPI remained unchanged at 3.3%, suggesting the headline surge reflects volatile energy prices rather than a broadening of underlying inflation

- The 17 March hike has not yet fully transmitted through the financial system; raising again before assessing its effect risks overtightening

- The inflation driver is substantially supply-side (energy and fuel costs), which monetary policy addresses only indirectly by suppressing demand broadly

The tension between these two cases is real. A board that hikes is responding to headline severity and expectation anchoring. A board that holds is trusting the trimmed mean signal and respecting transmission lags. Both positions are defensible, which is precisely why the 62% figure reflects a genuine debate rather than a foregone conclusion.

The rate hike cycle peak may arrive sooner than current pricing implies, with Oxford Economics modelling pointing to potential back-to-back quarterly GDP contractions in June and September 2026, a growth shock that historically causes central banks to pivot from tightening to cutting within a 6-12 month window of the inflation peak.

The Australian dollar is surging as the RBA and Fed head in opposite directions

Interest rate differentials are among the most direct drivers of currency movements. When one central bank tightens while another holds, capital flows toward the higher-yielding currency. That dynamic is playing out now between the RBA and the US Federal Reserve.

The RBA is expected to consider a further rate increase on 4-5 May, while the Fed is anticipated to hold US rates steady during the same week, widening the policy gap between the two economies.

The AUD/USD rate stood at 0.7119 as of 30 April 2026. According to analysis from Morningstar’s Matt Wilkinson, the Australian dollar has appreciated against multiple major currencies in late April 2026:

- USD: A stronger AUD reduces the cost of US-denominated imports but weighs on Australian exporters earning in US dollars

- Euro: Cheaper European goods and travel for Australians, with reduced competitiveness for Australian exports to the eurozone

- British pound: Similar import relief, with implications for Australian companies with UK operations

- Japanese yen: Benefits Australian travellers and importers of Japanese goods

The dual-edged nature of a stronger dollar is worth noting. A firmer AUD provides partial relief on import costs, including some energy inputs priced in US dollars. It also compresses returns for Australian investors holding offshore assets denominated in weaker currencies. US inflation remains significantly more subdued than Australia’s, reinforcing the expectation that the policy divergence will persist.

Beyond May: what persistent inflation means for Australian households in 2026

The May decision, whichever way it falls, is not the end of this rate cycle. Deputy Governor Hauser’s warning that rates will go as high as needed to return inflation to target frames an outlook where further hikes remain possible if the data does not improve.

Despite the current rate environment, national house prices rose 0.7% in March 2026 and 2.1% over the quarter. Homebuyer sentiment increased 3.5% in April 2026 but remains soft by historical standards. The housing market’s resilience suggests that monetary policy transmission to property prices remains incomplete, with supply constraints partially offsetting the effect of higher borrowing costs.

Analysis from UNSW (published in February 2026) suggested that persistent inflation could necessitate further cash rate increases through 2026, adding to the cumulative burden on variable-rate mortgage holders.

Investors exploring how to construct a portfolio that can weather both sustained inflation and a faster-than-expected rate reversal will find our comprehensive walkthrough of ASX inflation portfolio positioning, which covers scenario-balanced allocations across VBND, CRED, VGS, QUAL, AAA, and ISEC, with analysis of how each instrument performs under the two most likely 2026 macro outcomes.

What to watch for the rest of 2026

Australian borrowers, savers, and investors should monitor several indicators that will determine whether the May hike, if delivered, is the last or part of a continuing series:

- Monthly CPI releases: The next several readings will show whether the headline surge was a one-month spike or the beginning of a sustained move toward 5%

- RBA board meeting dates: Each meeting through the second half of 2026 is a potential decision point

- AUD/USD movements: Continued appreciation could ease import cost pressures; depreciation would compound them

- Fixed-rate mortgage repricing timelines: Borrowers rolling off fixed rates into the current variable environment face materially higher repayments

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A 4.6% inflation print and a rate cycle that is not finished yet

A headline CPI of 4.6%, energy-driven pressures feeding a Q2 forecast near 5%, and an RBA that has explicitly signalled its willingness to raise rates further all point toward the 4-5 May meeting being an active decision rather than a formality. The 62% market probability reflects genuine uncertainty, not confidence; the trimmed mean’s stability at 3.3% introduces a legitimate counterargument that the board will weigh seriously.

For Australians on variable mortgages, in the property market, or holding AUD-denominated assets, the practical response is the same regardless of whether May produces a hike or a hold: prepare for a range of outcomes. Review variable-rate exposure, assess refinancing options before the decision, and recognise that the trajectory of Australian inflation in 2026 will be shaped by energy markets and global conditions that no single board meeting can resolve.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.