Kevin Warsh Takes Over the Fed as Inflation Hits 3.8%

1 hr ago

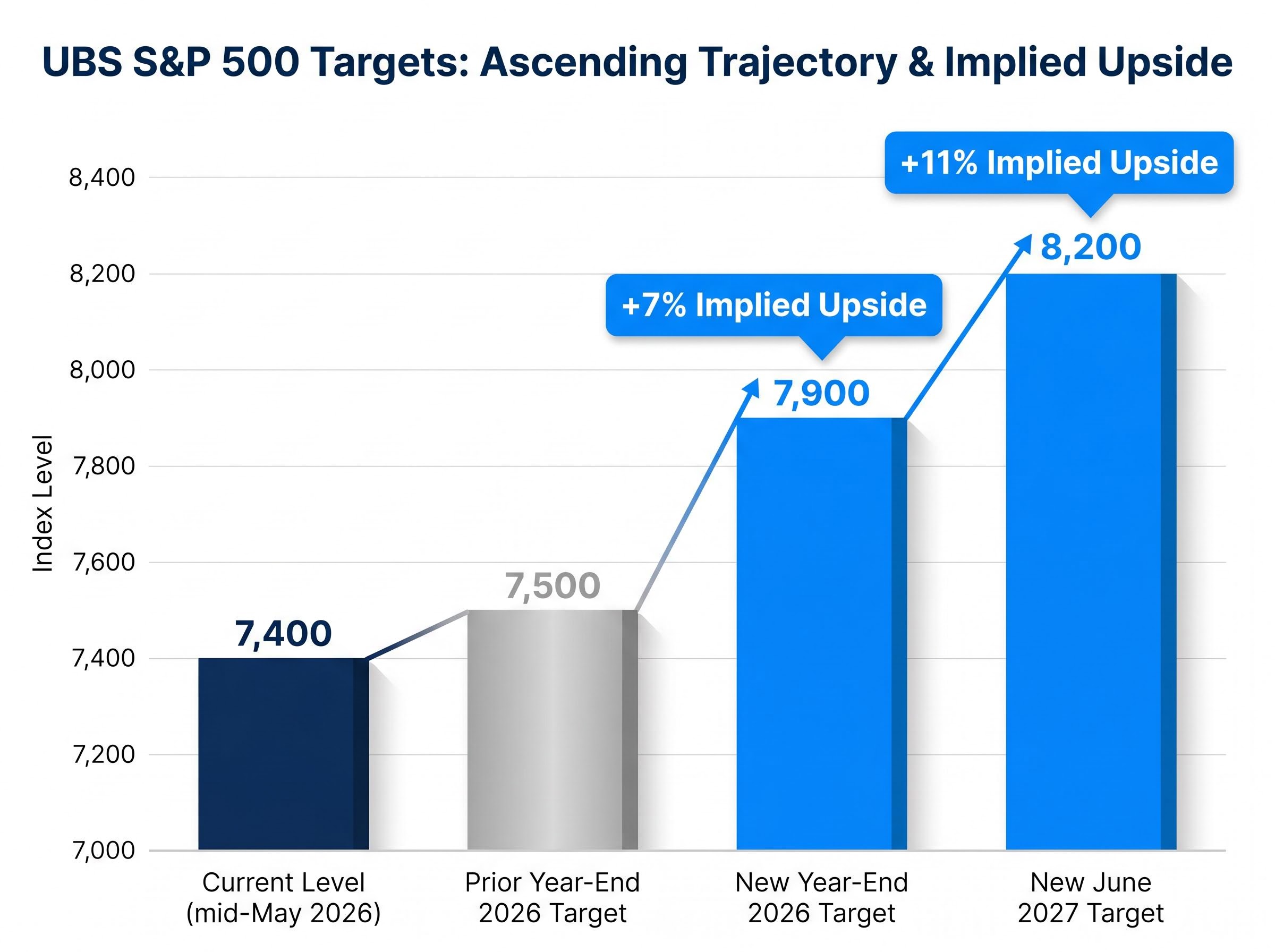

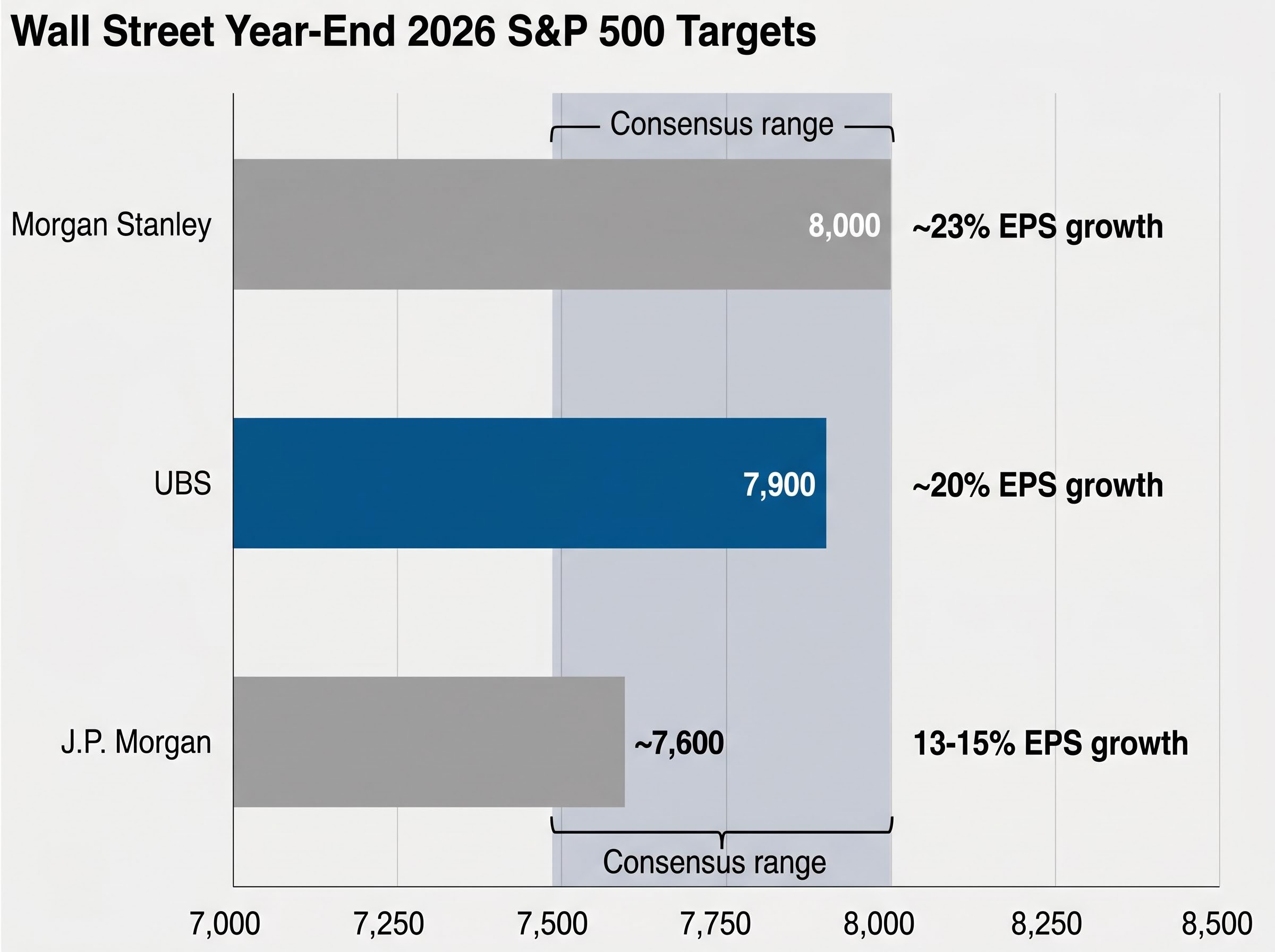

UBS has raised its S&P 500 year-end 2026 price target to 7,900 and introduced a June 2027 target of 8,200, both anchored to earnings upgrades that place 2026 earnings per share at $335, a figure implying roughly 20% profit growth for the index. The revision, published in a client note on 22 May 2026, arrives with the S&P 500 trading near 7,400, meaning UBS sees approximately 7% additional upside to year-end and further room into 2027. It lands against a backdrop of near-universal Wall Street bullishness: Morgan Stanley holds a year-end 2026 target of 8,000, J.P. Morgan sits around 7,600, and the broadest consensus band runs 7,500-8,000, placing UBS toward the upper-middle of the current major-bank range. What follows breaks down exactly what changed in the firm’s model, why semiconductors and energy drove most of the EPS revision, what UBS says investors need to watch, and how the call stacks up against the broader Wall Street consensus.

UBS raised its year-end 2026 S&P 500 target from 7,500 to 7,900 and introduced, for the first time, a June 2027 target of 8,200. The firm retained its “Attractive” designation for U.S. equities alongside the numerical upgrade, a signal that the revision reflects structural conviction rather than a short-term tactical tweak.

With the index trading near 7,400 as of mid-May 2026, the key numbers break down as follows:

UBS raised its S&P 500 year-end 2026 target from 7,500 to 7,900, introducing a June 2027 milestone of 8,200.

The size of the revision, 400 index points on the year-end target alone, places UBS above J.P. Morgan’s approximately 7,600 and modestly below Morgan Stanley’s 8,000. For institutional and retail investors alike, the retention of “Attractive” on U.S. equities as an asset class indicates the firm’s guidance is to maintain equity exposure, not merely chase a near-term level.

The most consequential detail in the UBS note is what drives the higher target. The firm attributed the revision principally to improved profit forecasts rather than any expansion in price-to-earnings multiples. That distinction carries weight: an earnings-driven price target is anchored to actual corporate profitability, not to investors paying more for the same earnings stream.

The EPS trajectory tells the story:

The Q1 2026 earnings season delivered a blended S&P 500 growth rate of 27.1%, nearly double the 13.1% analyst forecast from quarter-end, with an aggregate earnings surprise of 20.7% that was almost three times the five-year average, providing the empirical foundation on which UBS and its peers built their upgraded EPS assumptions.

| Year | Prior EPS Estimate | Revised EPS Estimate | Implied Growth |

|---|---|---|---|

| 2026 | $310 | $335 | ~20% |

| 2027 | N/A (new estimate) | $375 | ~12% (from revised 2026 base) |

The sector composition of the EPS revision is concentrated rather than broad:

Understanding where the earnings momentum is concentrated tells investors which portfolio exposures are most aligned with, or most dependent on, the UBS thesis holding.

AI-related capital spending has become the single largest driver of S&P 500 earnings revisions in 2026, yet the transmission mechanism from data centre investment to index-level EPS is worth understanding in concrete terms. It operates in three steps:

UBS revised its data centre capital spending estimates upward for 2026 before lifting its broader earnings forecasts, confirming this is the operative causal channel in the firm’s model. The sequence matters: spending drives demand, demand drives pricing power, and pricing power drives profit.

Independent data supports the earnings upgrade cycle UBS is projecting forward. According to Fidelity Investments, as of 11 May 2026 with 453 S&P 500 companies having reported, 84% beat Q1 2026 profit estimates. S&P 500 operating margins reached approximately 16%, described as an all-time high.

Earnings outperformance was broad-based across sectors, not confined to technology, which supports the multi-sector nature of the UBS revision. J.P. Morgan projects 13-15% S&P 500 earnings growth for at least two years, driven by AI-related forces spreading into utilities, banks, healthcare, and logistics. Investors who understand this transmission mechanism are better positioned to evaluate whether the earnings upgrade cycle has legs, or whether it depends on capital spending holding at elevated levels.

FactSet Q1 2026 earnings data confirms that the blended net profit margin for the S&P 500 reached 14.7% for the quarter, reinforcing the operating margin strength that underpins the earnings upgrade cycle multiple banks are now projecting forward.

UBS did not publish a bullish revision without conditions. The firm named three specific risks that could interrupt the path from 7,400 to 7,900 and beyond.

UBS indicated that a restoration of energy shipments through the Strait of Hormuz would likely be necessary to support the next phase of market appreciation.

The three named risks:

The Hormuz supply normalisation timeline extends well beyond a ceasefire announcement: with Saudi Aramco’s CEO warning that supply recovery could extend into 2027 and the IEA’s 400 million barrel emergency release covering only approximately four weeks of the weekly supply deficit, the energy precondition UBS named for the next leg of market appreciation may not be satisfied on a schedule that supports the year-end 7,900 target.

For calibration, J.P. Morgan assigns a 35% probability of a U.S. and global recession in 2026, while Morgan Stanley describes the energy supply shock from the Iran conflict as generating ongoing uncertainties. The Hormuz condition, in particular, gives investors a concrete watchpoint: if energy supply normalises, the bull case strengthens. If disruption persists, the earnings outlook faces pressure from rising input costs and potential central bank tightening.

For investors who need to model the interest rate path behind UBS’s earnings assumptions, our deep-dive into the 2026 Fed rate outlook examines how the most fractured FOMC vote in over 30 years, spanning both hawkish and dovish dissents, makes forward guidance less reliable and raises the risk of a rate surprise that could compress the earnings multiples on which targets like 7,900 depend.

UBS’s revised target does not exist in isolation. Placing it within the current Wall Street range gives investors context for judging conviction level.

Morgan Stanley’s mid-2026 investment outlook sets a year-end 2026 S&P 500 target of 8,000 alongside a mid-2027 forecast of 8,300, with approximately 23% EPS growth as the central earnings assumption underpinning both figures.

| Firm | Year-End 2026 Target | Key Earnings Growth Assumption |

|---|---|---|

| Morgan Stanley | 8,000 | ~23% EPS growth in 2026 |

| UBS | 7,900 | ~20% EPS growth in 2026 |

| J.P. Morgan | ~7,600 | 13-15% EPS growth for two years |

| Consensus range | 7,500-8,000 | Mid-teens EPS growth broadly expected |

The most bullish calls, from Oppenheimer and Deutsche Bank, reached approximately 8,200 earlier in 2026, according to Carnegie Investment Counsel’s January summary. That figure matches UBS’s new June 2027 horizon target, suggesting the firm sees the most aggressive year-end calls as achievable on a slightly longer timeline.

All three major banks share a common three-pillar thesis:

Not every major bank reads the same $335 EPS forecast as a buy signal: Bank of America raised its 2026 EPS estimate to $335 while holding its year-end price target at 7,100, a deliberate argument that 22% earnings growth is earnings already priced in at a forward P/E of 21.4x, roughly 20% above the 10-year historical average.

Where UBS distinguishes itself is in naming a specific precondition, Hormuz resolution, for the next leg of appreciation. Neither Morgan Stanley nor J.P. Morgan frame the energy risk as an explicit gate for their targets in the same conditional terms.

The UBS upgrade is, at its core, an earnings revision story. The path from 7,400 to 7,900 by year-end and 8,200 by mid-2027 rests on the firm’s conviction that S&P 500 EPS can reach $335 in 2026 (roughly 20% growth) and $375 in 2027 (roughly 12% growth). The sustainability of that trajectory depends on whether AI-driven profit momentum continues and whether two conditions resolve favourably: energy supply through the Strait of Hormuz and the Federal Reserve’s rate path.

UBS retained its “Attractive” rating on U.S. equities, meaning the firm’s guidance is to stay engaged with the market rather than reduce risk exposure, while monitoring the named risks.

For investors calibrating their positioning, the call offers a concrete framework: earnings, not sentiment, are doing the work, and the conditions under which the thesis holds or breaks are explicitly stated.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

UBS raised its year-end 2026 S&P 500 price target from 7,500 to 7,900, implying roughly 7% upside from the index level of approximately 7,400 as of mid-May 2026.

UBS forecasts S&P 500 earnings per share of $335 for 2026, implying approximately 20% profit growth, with semiconductors accounting for roughly 50% of the EPS revision and energy contributing around 25%.

UBS sits in the upper-middle of the current major-bank range: Morgan Stanley holds the highest year-end 2026 target at 8,000, UBS is at 7,900, J.P. Morgan is at approximately 7,600, and the broad consensus band runs 7,500-8,000.

UBS named three key risks: ongoing disruption to energy shipments through the Strait of Hormuz, a Federal Reserve rate reversal driven by persistent energy-related inflation, and volatility in semiconductor equities given their recent sharp gains.

UBS attributed the target upgrade to improved corporate profit forecasts rather than multiple expansion, meaning the higher target reflects actual earnings growth expectations rather than investors paying more for the same earnings stream.