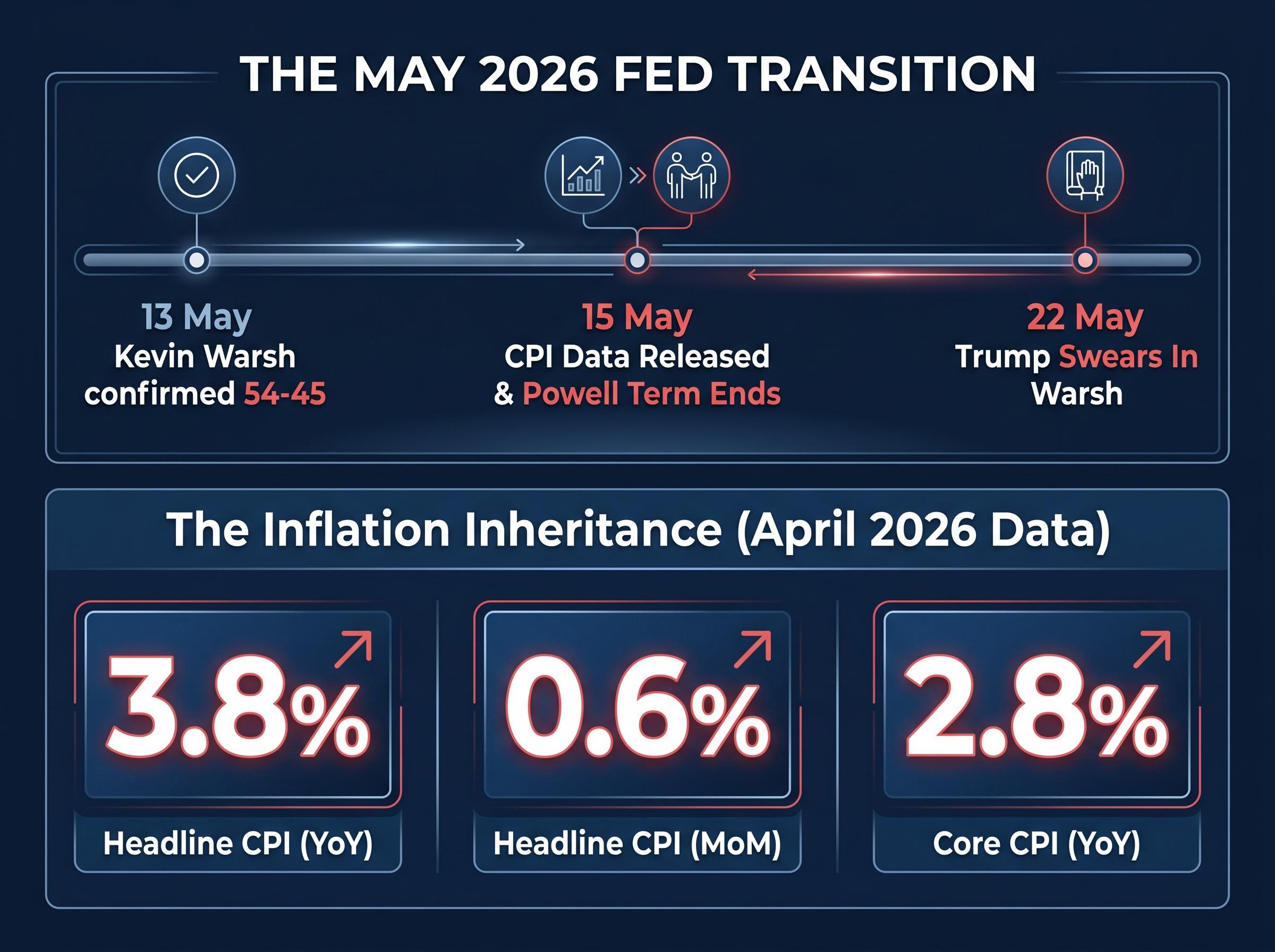

On 22 May 2026, President Donald Trump stood in the ceremonial room, looked at his newly installed Federal Reserve Chair, and told him not to listen to the president. The instruction was remarkable precisely because it was necessary. Kevin Warsh, confirmed 54-45 by the Senate on 13 May 2026 and now the 17th Chair of the Federal Reserve, inherits the institution at a moment when the independence of central banking in the United States has become a live market variable rather than a settled question. With headline inflation running at 3.8% year-over-year and the administration’s prior conduct toward outgoing Chair Jerome Powell still fresh, the gap between ceremony and substance is where the real analysis begins.

What follows is an examination of what political pressure on the Fed actually means for institutional independence, why that independence matters for markets and ordinary Americans, and what investors should watch as the Warsh era opens into a second half of 2026 defined by persistent inflation and unresolved political tension.

The ceremony that said the quiet part loud

Trump presided over the swearing-in on 22 May 2026, one week after Powell’s term as chair concluded on 15 May. The ceremony itself was unremarkable in format. The substance was not.

Trump instructed Warsh to operate independently and not be influenced by the president or others, describing the Federal Reserve as “the most consequential central bank in the world.”

That statement, offered publicly by the same president who spent years calling Powell derogatory names, demanding rate cuts, and authorising a formal government inquiry into Fed renovation spending, carries its own analytical weight. A president publicly affirming central bank independence at the precise moment he installs his handpicked successor is not reassurance. It is evidence that the question of independence required addressing at all.

The contradiction needs no editorial commentary to be visible. Trump chose Powell’s replacement after years of documented dissatisfaction with Powell’s rate decisions. He then told the replacement, in front of cameras, to ignore him. The instruction acknowledged the pressure. Whether the instruction will hold is the subject of everything that follows.

When big ASX news breaks, our subscribers know first

Why central bank independence is not just an abstract principle

The phrase “central bank independence” appears frequently in financial commentary, often without explanation of what it protects against. In operational terms, it means the Federal Reserve sets interest rates and manages the money supply free from direct political instruction. The goal is to keep inflation stable and employment high over the long term, even when short-term political incentives push in the opposite direction.

The mechanism by which inflation erodes purchasing power operates silently across savings accounts, fixed-income holdings, and wage contracts, compounding the cost of any policy delay and explaining why even a modest overshoot above the Fed’s 2% target carries meaningful long-run consequences for household wealth.

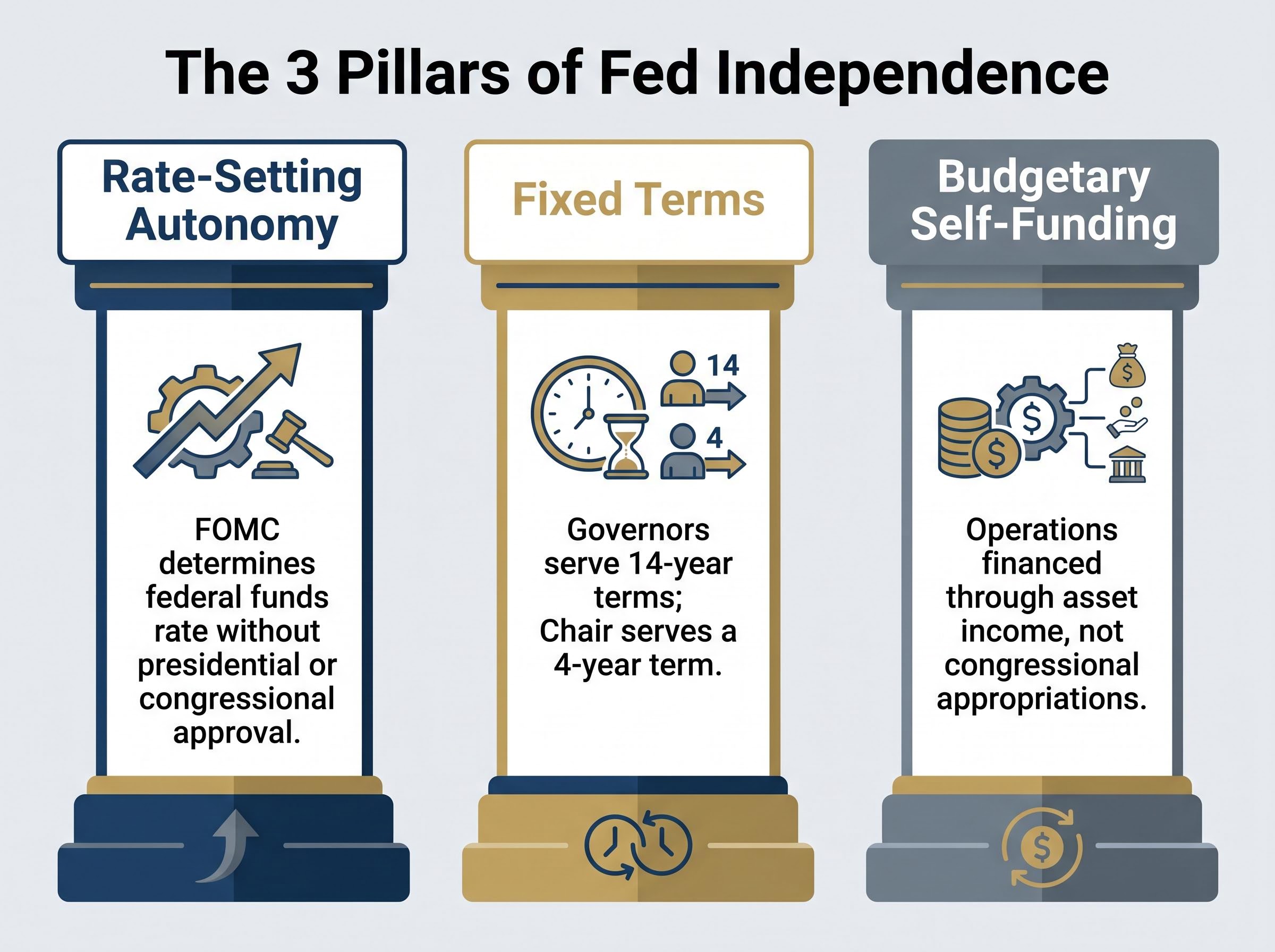

Three structural features underpin this independence:

- Rate-setting autonomy: The Federal Open Market Committee determines the federal funds rate without requiring approval from the president or Congress.

- Fixed terms: Fed governors serve 14-year terms, and the chair serves a four-year term, designed to outlast electoral cycles and insulate decision-making from campaign pressures.

- Budgetary self-funding: The Fed finances its operations through income on its asset holdings, not through congressional appropriations, removing the most direct lever of political control.

The Federal Reserve Board governance structure establishes that governors serve 14-year terms and the chair serves a four-year term, timelines deliberately calibrated to outlast presidential cycles and reduce the leverage any single administration holds over the institution’s direction.

These are not abstract governance features. They are the specific mechanisms that prevent a sitting president from calling the Fed and dictating rate policy.

What today’s inflation data makes the stakes concrete

The April 2026 Consumer Price Index, released by the Bureau of Labor Statistics on 15 May 2026, reported headline inflation of 3.8% year-over-year and 0.6% month-over-month. Core CPI, which strips out food and energy, came in at 2.8% year-over-year.

These figures illustrate the tension in real time. A Fed pressured to cut rates into 3.8% headline inflation would risk entrenching price pressures and losing the credibility that anchors long-term inflation expectations. The timing of the Warsh transition, directly into this inflationary environment, means his earliest policy signals will carry disproportionate weight. Any perception that the new chair might ease prematurely in response to political pressure could itself accelerate inflation expectations before a single rate decision is made.

Trump’s pressure campaign on Powell: what actually happened

The independence concern surrounding the Warsh appointment does not rest on speculation. It rests on a documented pattern of presidential conduct toward the Fed during Trump’s second term.

That pattern escalated through three distinct phases:

- Public criticism of rate decisions. Trump repeatedly called on the Fed to lower borrowing costs, framing Powell’s rate stance as an obstacle to economic growth. These statements, made through public channels, became a recurring feature of the administration’s economic messaging through to the May 2026 transition.

- Derogatory rhetoric directed at the chair personally. Beyond policy disagreement, Trump used derogatory nicknames for Powell in public statements, a tactic that personalised the conflict and signalled to markets that the president viewed the Fed chair as an adversary rather than an independent institutional leader.

- A formal government inquiry into Fed renovation spending. This represented the most structurally significant escalation. Unlike rhetorical criticism, the renovation inquiry deployed a formal government mechanism against the institution itself, raising concerns about whether administrative tools could be used to pressure or destabilise Fed leadership.

The renovation spending inquiry stands apart from the public rhetoric because it moved the pressure from words to institutional action, a distinction that markets and governance observers treated as qualitatively different.

Despite this sustained pressure, Powell did not publicly alter monetary policy decisions in response to Trump’s demands. His term concluded on 15 May 2026 without a capitulation on rates. That outcome is itself evidence: the structural independence mechanisms functioned under strain. The question the Warsh era poses is whether those mechanisms will continue to hold under a chair who owes his appointment to the president who tested them.

FOMC internal divisions were already visible before Warsh took the oath, with four dissenting votes recorded at the April 28-29 meeting, the most at any single Federal Reserve meeting since 1992, and an active Supreme Court challenge to Fed independence adding a legal dimension to the institutional pressure the incoming chair now faces.

The Nixon-Burns lesson the Fed was built to prevent

The tension between a president who wants lower rates and a Fed chair who resists is not new. Its most consequential historical precedent is the relationship between President Richard Nixon and Fed Chair Arthur Burns in the early 1970s.

Burns accommodated Nixon’s desire for loose monetary policy ahead of the 1972 presidential election, keeping rates lower than the inflationary environment warranted. The result was not abstract: it contributed directly to the inflation spiral that defined the decade, with consumer prices rising at double-digit annual rates by the mid-1970s. The economic damage took years and a severe recession under Paul Volcker’s chairmanship to reverse.

The Nixon tapes evidence on Burns, preserved and analysed through the Federal Reserve’s archival research system, documents in granular detail how private presidential persuasion translated into monetary policy accommodation, providing the empirical foundation for the consensus that institutional independence requires structural protection rather than personal resolve alone.

The modern consensus on central bank independence, and the structural features of the Federal Reserve Act that protect it, were built in direct response to the Burns failure. They are not theoretical safeguards. They are institutional scar tissue.

| Feature | Nixon-Burns (1970s) | Trump-Powell-Warsh (2025-2026) |

|---|---|---|

| Pressure type | Private persuasion, political alignment | Public criticism, formal institutional inquiry |

| Fed chair response | Accommodation of political preference | Powell resisted; Warsh era untested |

| Inflationary context | Rising inflation, pre-election loosening | Headline CPI at 3.8%, energy-driven pressures |

| Outcome | Decade of stagflation | To be determined |

Warsh comes from the institutional tradition that takes the Burns lesson seriously. His 2006-2011 tenure as a Fed Governor placed him inside the institution during and after the global financial crisis, a period when the Fed’s independence and credibility were tested by different but equally intense pressures. That professional formation matters. Whether it proves sufficient against the specific pressures of this presidency remains the open question.

What markets are actually pricing when they price Fed independence

When markets price threats to Fed independence, the transmission runs through three specific channels.

The bond market is the most direct. Inflation expectations embedded in the yield curve reflect investor confidence that the Fed will act to contain prices. If that confidence erodes, long-term yields rise as bondholders demand higher compensation for the risk that inflation will not be controlled. The dollar is the second channel: reserve currency credibility depends in part on the perception that U.S. monetary policy is set by technocrats, not politicians. The third is equity valuations, where discount rate certainty affects how investors value future corporate earnings. Uncertainty about whether the Fed will follow its mandate or accommodate political pressure widens the range of possible rate paths, compressing valuation multiples.

Bond market pressure has emerged as the primary forcing mechanism on White House economic decisions in 2026, with the 10-year Treasury yield at 4.66%-4.67% and the 30-year pushing 5.18%, meaning the Fed’s credibility is being priced in real time through yield levels that simultaneously tighten mortgage rates, corporate borrowing costs, and federal debt servicing.

As of the swearing-in, reporting indicated traders were pricing in at least one 25 basis point rate increase before the end of 2026, reflecting the inflationary environment rather than any expectation of immediate policy accommodation under the new chair. Middle East conflict-driven energy price surges have been cited as a significant driver of the current inflationary backdrop, adding supply-side complexity to the rate outlook.

Signals to watch under the Warsh Fed

Investors can monitor several concrete signals to assess whether the new chair is operating independently:

- Yield curve response to Fed communications. If long-term yields spike after Warsh speeches or press conferences, it may signal that markets perceive his messaging as insufficiently hawkish for the inflation environment.

- Dollar index reaction. A weakening dollar following dovish Fed signals in a high-inflation context would suggest credibility erosion.

- Divergence between Fed and White House rate rhetoric. If Fed communications and administration public statements on rates converge rather than maintain institutional distance, markets will notice.

- Rate futures shifts after Trump public statements. If fed funds futures move meaningfully in response to presidential commentary on rates, it indicates markets believe the commentary carries policy weight.

These are not theoretical indicators. They are observable in real time and will provide the earliest evidence of whether the Warsh Fed is maintaining the independence that Trump, at the ceremony, publicly instructed it to preserve.

For investors wanting to translate the independence question into a concrete portfolio monitoring framework, our dedicated guide to Warsh’s policy framework and market signals examines the five specific indicators — including Brent crude relative to $100, short-dated Treasury yield direction, and Warsh’s first press conference stance on easing bias — that will provide the earliest empirical evidence of how the new chair navigates the dual pressure of hot inflation and political scrutiny.

Independence is a credibility stock, not a fixed asset

The framing that matters going forward is not whether the Fed is independent or not. Independence is not a binary condition. It is a credibility stock: accumulated through consistent, data-driven behaviour and depleted through perceived accommodation of political pressure.

The 54-45 Senate confirmation margin places Warsh in office with a narrow mandate and a politically charged appointment history. Trump’s ceremony statement, instructing the new chair toward independence and calling the Fed “the most consequential central bank in the world,” signals that even the administration recognises the credibility cost of visible interference. The statement is a deposit into the credibility account. Whether subsequent conduct matches it will determine whether the balance grows or erodes.

The empirical test is straightforward. With headline inflation at 3.8%, any early Warsh policy moves should be assessed against the data. If rate decisions align with the inflation trajectory and the Fed’s dual mandate, the credibility stock holds. If policy pivots appear to track presidential preferences rather than economic conditions, markets will reprice accordingly, and the repricing will be visible in the channels identified above.

The Warsh era begins with the words right. The question, as it always is with independence, is whether the actions follow.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Fed policy direction are speculative and subject to change based on economic developments and institutional decisions.