On 22 May 2026, Kevin Warsh placed his hand on the Bible, took the oath of office from Justice Clarence Thomas at a White House ceremony, and became the 17th Chair of the Federal Reserve. Jerome Powell’s tenure is over. The most consequential leadership transition in central banking since 2018 is now official.

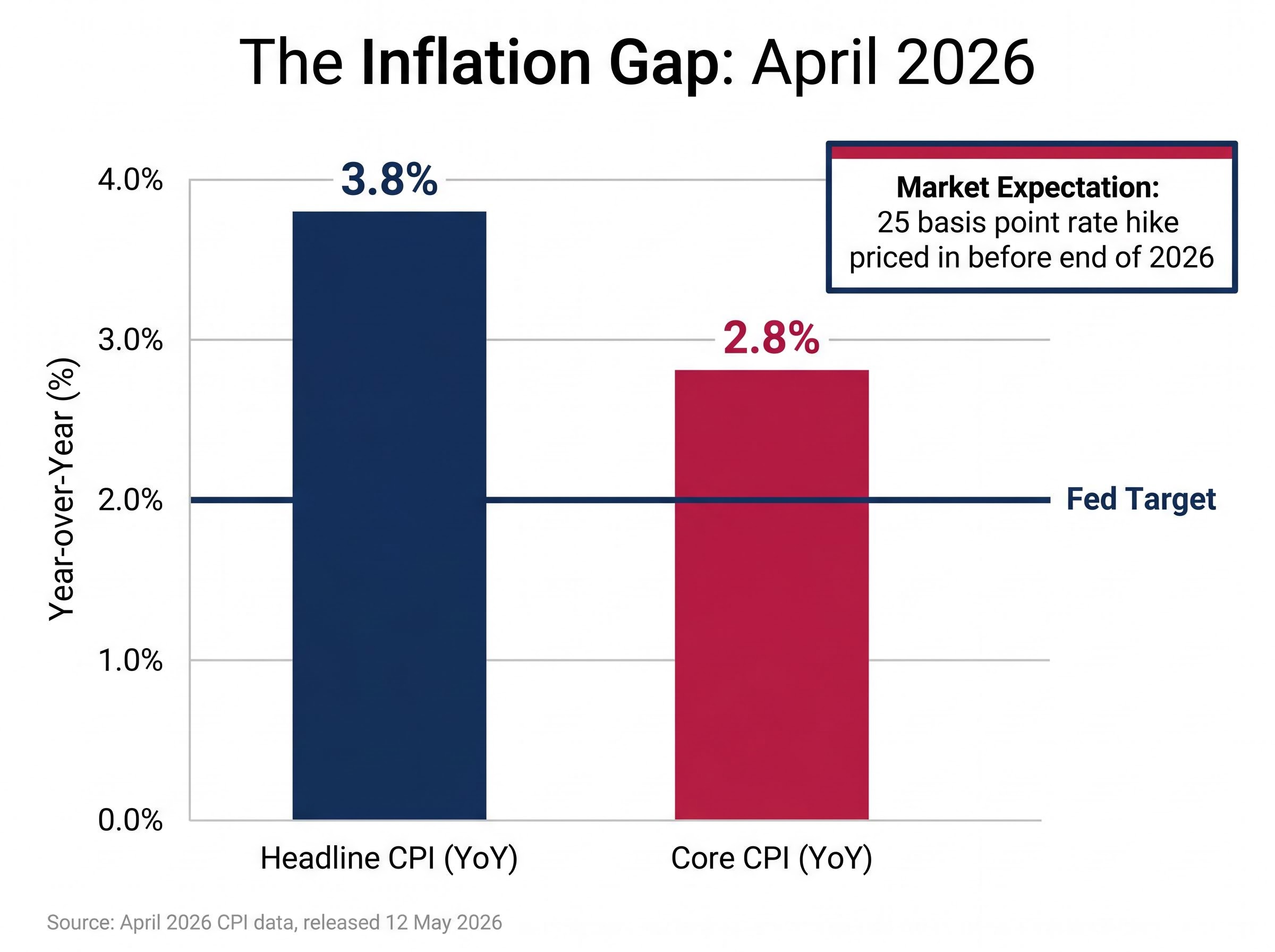

The timing is not incidental. Just ten days before the swearing-in, the Bureau of Labor Statistics published April 2026 Consumer Price Index data showing headline inflation running at 3.8% year-over-year, with core prices at 2.8%, both well above the Fed’s 2% target. Warsh inherits an inflation problem that is already shaping market expectations: traders have moved to price in a 0.25 percentage point rate hike before year-end. His policy philosophy, documented across a decade of public speeches and commentary, leans hawkish, pre-emptive, and sceptical of the accommodative tools his predecessor favoured. What follows is an account of how Warsh arrived at the Fed’s top job, what he believes, the economic conditions waiting on his desk, the independence question hovering over the appointment, and what investors should watch from here.

From governor to chair: how Kevin Warsh arrived at the Fed’s top job

The path from nomination to oath took roughly two months. The procedural sequence unfolded in four steps:

- Nomination: President Trump formally nominated Kevin Warsh as Federal Reserve Chair.

- Senate Banking Committee hearing: Warsh appeared before the committee on 21 April 2026.

- Senate confirmation vote: The full Senate confirmed Warsh on 13 May 2026 by a vote of 54-45.

- Swearing-in: Justice Clarence Thomas administered the oath at a White House ceremony on 22 May 2026.

The 54-45 confirmation vote split almost entirely along party lines, the narrowest margin for a Fed Chair confirmation in recent memory.

That margin matters. It signals both the political capital the administration spent on the appointment and the degree of opposition Warsh’s candidacy generated in the Senate. For context, Powell was confirmed to his first term by a 84-13 vote in 2018.

The Senate confirmation vote carried its own signal: near-unanimous Democratic opposition centred on Fed independence concerns, and the 54-45 margin reflects how politically freighted this appointment became in the weeks between nomination and oath.

Warsh is not, however, an outsider. He previously served as a Federal Reserve governor, giving him institutional familiarity that most incoming chairs lack. He knows the building, the staff, and the internal dynamics of the Federal Open Market Committee (FOMC), the body that sets interest rate policy. The question is not whether he understands the institution. It is what he intends to do with it.

When big ASX news breaks, our subscribers know first

What Warsh actually believes about monetary policy

The clearest window into Warsh’s thinking remains his public record from the post-financial-crisis era. His 7 October 2016 speech at the Manhattan Institute, titled “The New Malaise,” laid out a policy philosophy that challenged the Federal Reserve’s approach under both Ben Bernanke and Janet Yellen.

In that speech and in subsequent op-eds, Warsh argued that quantitative easing (where the central bank purchases large quantities of government bonds and other assets to push down long-term interest rates) had outlived its usefulness and was creating financial-stability risks. He advocated for a smaller Fed balance sheet. He warned that keeping rates near zero for years encouraged excessive risk-taking in financial markets rather than productive economic activity.

His approach favours rule-based, pre-emptive tightening. Where the Powell-era Fed waited for data to confirm inflation before acting, Warsh’s documented preference is to move before the data forces the Fed’s hand.

Warsh’s documented view that the economy operates with a structurally higher neutral rate than the post-2008 consensus assumed has direct implications for how far rates need to rise before policy is genuinely restrictive, a threshold that sits considerably above where the federal funds rate currently sits.

Warsh’s documented hawkish policy record extends back to the post-2008 deflationary cycle, when he raised concerns about excessive inflation risk at a time when most policymakers were focused on the opposite problem, a track record that gives his pre-emptive tightening philosophy a longer history than a single 2016 speech.

The Powell contrast

Jerome Powell governed as a data-dependent gradualist, particularly during the 2022-2024 rate cycle. He waited for inflation readings to confirm trends before adjusting policy, and he tolerated periods of uncertainty with patience rather than pre-emptive action. The philosophical gap between the two is visible across several dimensions.

| Policy Dimension | Kevin Warsh (Documented) | Jerome Powell (Recent Practice) |

|---|---|---|

| QE stance | Sceptical; views large-scale asset purchases as a financial-stability risk | Deployed aggressively in 2020; wound down gradually |

| Balance sheet preference | Smaller; favours faster reduction | Accepted a large balance sheet; slow runoff |

| Tightening style | Pre-emptive and rule-based | Data-dependent; moved after confirmation |

| Inflation response | Act early to prevent entrenchment | Tolerate transitory readings; act on persistence |

This is not a subtle distinction. It represents a different theory of when and how a central bank should act.

The inflation problem waiting on Warsh’s desk

The Bureau of Labor Statistics released April 2026 CPI data on 12 May 2026, ten days before the swearing-in. Warsh did not need to wait for his first briefing to understand the scale of the problem. The numbers were public:

- Headline CPI (year-over-year): +3.8%

- Headline CPI (month-over-month, seasonally adjusted): +0.6%

- Core CPI, excluding food and energy (year-over-year): +2.8%

- Core CPI (month-over-month, seasonally adjusted): +0.4%

(Source: U.S. Bureau of Labor Statistics, CPI news release, published 12 May 2026)

Headline inflation at 3.8% year-over-year sits nearly double the Fed’s 2% target, the widest gap a new Fed chair has inherited since the post-pandemic surge.

The headline figure captures what consumers feel at the checkout. The core figure, which strips out volatile food and energy prices, is the reading the Fed treats as a more reliable signal of persistent inflation pressure. At 2.8%, core CPI remains meaningfully above target.

According to Investing.com reporting, traders have fully priced in a 25 basis point rate hike before the end of 2026. That expectation amounts to a market bet that the new chair will tighten, not ease, in his opening months.

For a chair whose documented instincts favour pre-emptive action against inflation, the data does not present an ambiguous case. The first FOMC meeting under Warsh’s leadership will be a direct test of whether his stated philosophy translates into policy.

Federal Reserve independence: what Trump said at the swearing-in, and why it matters

At the White House ceremony, President Trump publicly instructed Warsh not to be influenced by the president or others in making monetary policy decisions. He described the Federal Reserve as a foundational institution of global finance and the most consequential central bank in the world.

The remarks were notable for their content, and for their context. Trump’s prior conduct toward the Fed has included repeated public calls for rate cuts, derogatory public criticism of Jerome Powell by name, and what Investing.com reporting described as a formal administration inquiry into Fed renovation expenditures during Powell’s tenure (though this inquiry has not been independently confirmed by other outlets at the time of writing).

The gap between the ceremony’s rhetoric and the administration’s recent history creates an unresolved question that markets will price in real time.

Why central bank independence is a market variable

An independent central bank is a credibility signal. When bond investors believe the Fed sets rates based on economic conditions rather than political pressure, long-term inflation expectations stay anchored, and Treasury yields remain stable. If that belief erodes, investors demand higher yields to compensate for the risk that monetary policy will be compromised. The same dynamic applies to the U.S. dollar’s reserve currency status. Independence is not a governance abstraction; it is a variable that moves yields and exchange rates.

What to watch now that Warsh is in charge

The appointment is confirmed. The inflation data is published. What remains is execution. Four specific signposts will tell investors how the Warsh era is shaping up:

- First FOMC meeting as chair: The initial meeting Warsh presides over will reveal whether his pre-emptive, hawkish instincts translate into policy action or whether the committee’s consensus moderates his approach.

- Balance sheet signalling: Any communication suggesting an acceleration of quantitative tightening or faster asset runoff would confirm that Warsh’s documented balance-sheet-reduction preference is moving from speech to practice.

- Press conference tone and forward guidance language: The specific words Warsh uses in his first post-meeting press conference will set the market’s baseline for how fast and how far rate moves could go; precision or ambiguity in that language will move Treasury yields in real time.

- White House and Fed divergence: Any gap between administration statements on rates and FOMC decisions will signal whether the independence norm proclaimed at the ceremony is holding under live policy conditions.

The scale of FOMC dissents Warsh inherits is without modern precedent: four members voted against the April 28-29 statement, the most at any single meeting since 1992, and the 30-year Treasury yield reached 5.14% on May 18, the highest level since before the 2008 financial crisis, tightening financial conditions independently of any rate decision Warsh makes.

With April CPI at 3.8%, a 25 basis point hike already priced in by markets, and a new chair whose documented views lean toward acting before the data deteriorates further, the baseline expectation is for a tighter policy stance. The signposts above will confirm or complicate that expectation.

A new era at the Fed, and what it costs to get it wrong

This is not a routine leadership change. The shift from Powell to Warsh represents a different theory of central banking: when to act, how aggressively to manage the balance sheet, and how much weight to place on pre-emption versus patience.

What remains genuinely unknown is how Warsh will manage FOMC consensus across a committee he did not build, whether his documented hawkishness will survive contact with a slowing economy if one materialises, and whether the administration’s public commitment to Fed independence will hold through a politically inconvenient tightening cycle.

The conditions are specific. Inflation at 3.8%. A rate hike already priced in. A chair whose instincts, on paper, align with the direction markets expect. If the alignment holds, the transition may be orderly. If the variables shift and Warsh’s independence is tested rather than assumed, the repricing could be significant.

For investors recalibrating their portfolios in response to the Warsh era’s likely policy direction, our comprehensive walkthrough of defensive investing during rate hikes covers sector rotation toward high-margin, low-debt equities, the case for dollar-cost averaging in volatile rate environments, and specific screening criteria for identifying companies with the pricing power to absorb tighter financial conditions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Federal Reserve policy are speculative and subject to change based on economic developments and institutional dynamics.