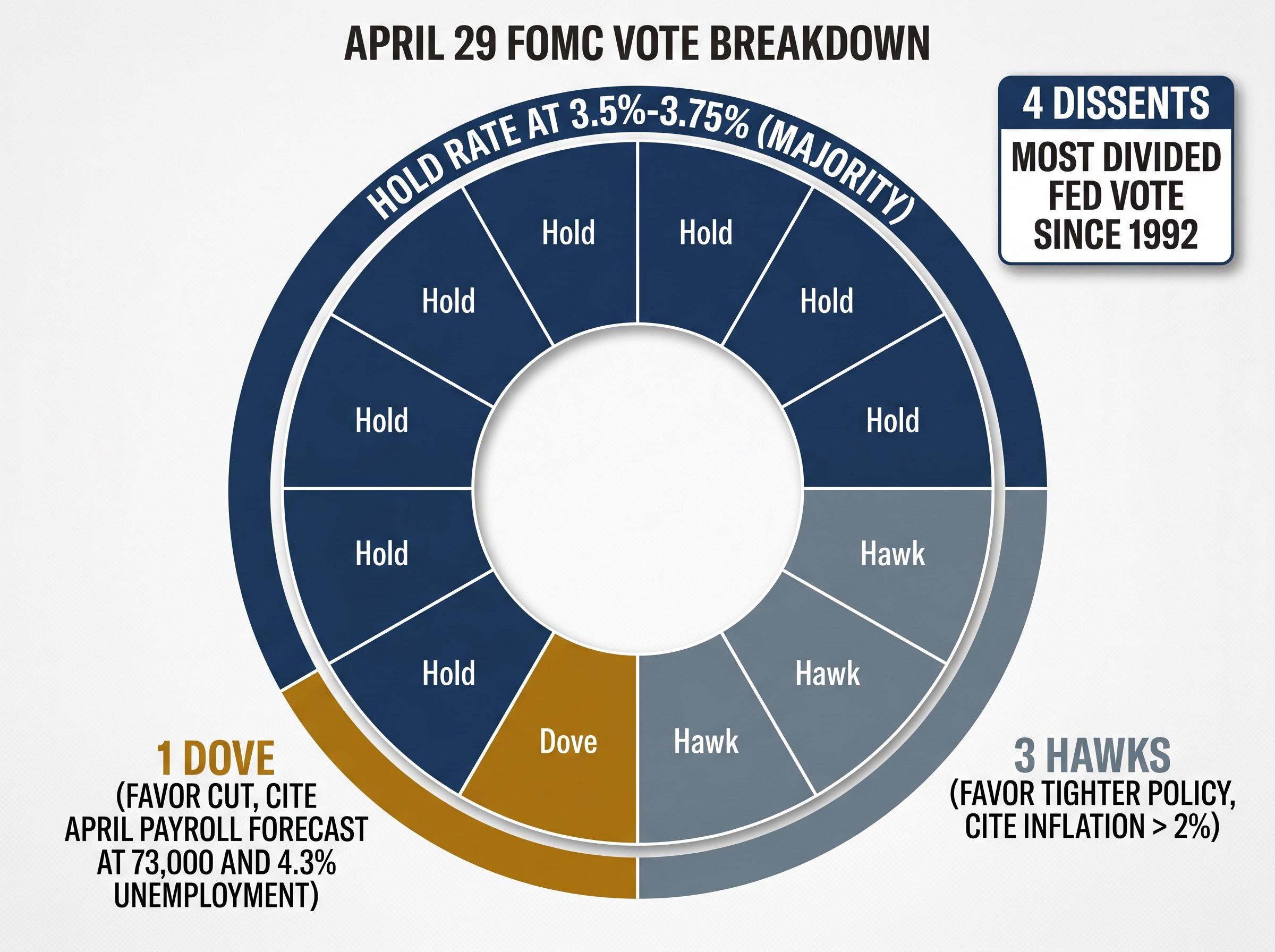

The Federal Reserve’s April 29 meeting produced four dissents, the most fractured policy vote in over three decades, and yet the rate-hold headline alone understates how much changed at the central bank in a single afternoon. The decision to hold the federal funds rate at 3.5%-3.75% arrived alongside internal disagreement spanning both directions: three hawks pushing for tighter policy and one dove pushing for a cut. Simultaneously, Jerome Powell confirmed he will remain on the Fed Board as a governor after his chairmanship ends on May 15, a move without modern precedent that complicates the transition to Trump’s designated successor, Kevin Warsh. What follows is an analysis of what the dissent pattern reveals about the Fed’s actual policy trajectory, why Powell’s board decision matters for institutional dynamics, how to read the wave of Fed speaker appearances scheduled this week, and what all of it means for rate-sensitive assets.

Four dissents, one fractured committee: what the April 29 FOMC vote actually signals

The Federal Open Market Committee (FOMC) prizes consensus. Most meetings produce unanimous or near-unanimous votes. The April 29 decision broke that pattern in a way the institution has not seen in over 30 years.

The April 29 FOMC statement confirmed the hold at 3.5%-3.75% and characterised risks as broadly balanced, with Powell indicating the next move would more likely be a cut while explicitly ruling out hikes as a base case.

Four dissents at the April 29 FOMC meeting: the most divided Fed vote since 1992.

The fracture split in two directions, and the asymmetry is the story. The dissenting positions break down as follows:

- Three hawkish dissenters opposed the hold, favouring tighter policy on the basis that current rates remain insufficiently restrictive given persistent inflation above the 2% target.

- One dovish dissenter pushed for an immediate cut, citing employment risks as justification, particularly with April payrolls forecast at approximately 73,000 (a sharp deceleration from March’s 178,000) and unemployment projected at 4.3%.

- The majority voted to hold at 3.5%-3.75%, maintaining the status quo.

Some sources cite three dissents rather than four; official minutes will confirm the precise count when released. Regardless, the signal is the same.

This is not a committee divided about timing. It is a committee divided about direction. Hawks and the lone dove are reading the same economic data, March payrolls at 178,000 (above expectations), slowing forward indicators, inflation still above target, and arriving at opposing conclusions about what the Fed should do next. For investors, a fractured committee means forward guidance carries less weight because there is no reliable consensus view on the next move.

The dual-mandate conflict sitting beneath the April 29 vote is sharper than the headline hold suggests: PCE inflation running at 3.5% against a 2% target cannot be addressed with the same rate tool designed to ease pressure on an unemployment rate approaching 4.3%, and the committee’s internal fracture reflects that irresolvable tension.

When big ASX news breaks, our subscribers know first

Why the Fed holds its benchmark rate, and how dissent actually works

The FOMC consists of 12 voting members: the seven members of the Board of Governors (when fully seated), the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents on a rotating basis. The chair sets the agenda. Policy decisions are reached by majority vote.

The federal funds rate target band, currently 3.5%-3.75%, is the rate at which banks lend reserves to each other overnight. It anchors borrowing costs across the economy, from mortgage rates to corporate debt pricing to credit card interest.

A dissent is not a casual aside. It is a formal, named disagreement entered into the official record.

How a Fed dissent enters the official record

The process follows a specific sequence:

- The FOMC votes on the policy decision at the conclusion of the meeting.

- Dissenting votes are recorded alongside the majority decision.

- Fed staff draft the official minutes, incorporating dissenters’ names and specific rationales.

- Minutes are published approximately three weeks after the meeting.

That three-week lag matters. In the period between the meeting and the minutes release, markets operate with the post-meeting statement and press conference as their only official sources. The dissenters’ names and detailed reasoning from the April 29 meeting will not be confirmed until the minutes are published; this is a date worth marking.

The last time the FOMC produced a comparable level of disagreement was 1992. Understanding that dissents reshape the minutes, influence expectations, and signal where the committee may move next makes the vote record a leading indicator, not background noise.

Jerome Powell’s decision to remain as governor, and what it means for the Warsh handover

Every modern Fed chair has left the Board cleanly. Janet Yellen departed entirely in February 2018 when her chair term concluded. Powell has chosen a different path.

His announcement that he will remain on the Board as a governor after May 15, 2026, citing legal concerns and transition considerations, breaks with that precedent. Under the Federal Reserve Act, the chair appointment is a four-year term, but the underlying governor seat carries a 14-year term. The two are legally distinct.

Federal Reserve Act Section 10 establishes the legal architecture that makes Powell’s decision possible: governor appointments carry a 14-year term that is legally distinct from the four-year chair appointment, meaning a departing chair retains full board membership and voting rights unless they choose to resign entirely.

The Federal Reserve Act permits a governor to serve a 14-year term independent of the four-year chair appointment. Powell’s decision to exercise that right is legally permissible but institutionally unprecedented in the modern era.

| Chair | Term End Date | Remained on Board | Successor | Transition Complexity |

|---|---|---|---|---|

| Janet Yellen | February 2018 | No | Jerome Powell | Low: clean departure |

| Jerome Powell | May 15, 2026 | Yes (as governor) | Kevin Warsh (designated) | High: former chair retains vote |

The implications are specific. Powell retains a vote, participates in deliberations, and is constitutionally protected from removal. Kevin Warsh, Trump’s designated successor expected to bring a different policy orientation, may struggle to build the internal consensus that gives Fed communications their market-calming power. That dynamic matters directly for bond market volatility and forward guidance reliability.

The Warsh confirmation mechanics are more constrained than the designation announcement implied: as a holder of one of 12 FOMC votes, his personal policy preferences do not automatically translate into committee decisions, and market data from the confirmation advance itself showed rising Treasury yields and a flat S&P 500 rather than the dovish relief rally some anticipated.

What the wave of Fed speaker appearances this week signals to markets

After the most divided vote in a generation, every public statement from a Fed official carries heightened weight. This week’s speaker calendar is not background noise; it is a live intelligence-gathering exercise.

| Official | Role | Scheduled Appearance | What to Watch |

|---|---|---|---|

| John Williams | New York Fed President | Monday | Permanent voter; inflation characterisation |

| Michelle Bowman | Fed Governor | Tuesday | Hawkish lean; employment risk weighting |

| Michael Barr | Fed Governor | Tuesday | Regulatory focus; any rate path signals |

| John Williams | New York Fed President | Thursday | Second appearance; potential shift in tone |

| Additional officials | Various | Later in the week | Breadth of dissent sentiment |

Williams’s two appearances are particularly significant. As New York Fed president, he holds a permanent FOMC vote. Deutsche Bank analysts have flagged this week as an opportunity to assess where each speaker positions relative to the committee’s centre, given Powell’s characterisation of the FOMC as moving toward a more neutral posture.

No post-April 29 public statements from Williams, Bowman, or Barr have been confirmed as of May 4; the Fed speeches archive at federalreserve.gov is the appropriate source for updates. Three signals investors should monitor in each appearance:

- How each speaker characterises current inflation trajectory

- Whether employment risks receive equal, greater, or lesser weighting than inflation concerns

- Any reference to the pace or conditions for future rate adjustments

Where markets are pricing the Fed, and what the 83-87% hold probability means for portfolios

Fed funds futures price an 83%-87% probability of no rate change through end-2026.

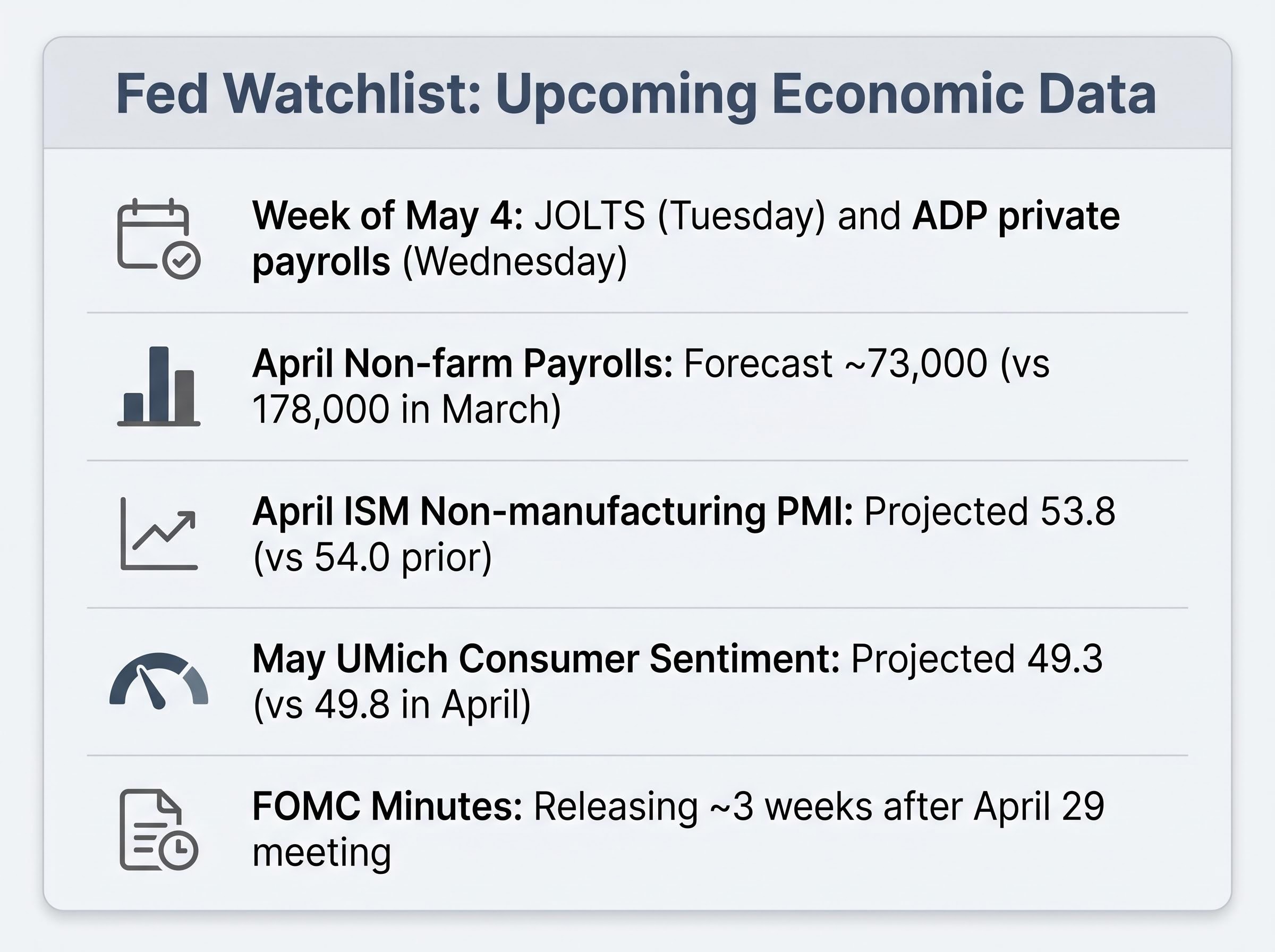

That is a strong consensus. Bond yields, REIT valuations, and rate-sensitive sector performance are all calibrated to an extended hold environment at 3.5%-3.75%. March dot plot projections indicated one projected cut in 2026, though April-specific Summary of Economic Projections (SEP) data has not been confirmed; CME FedWatch and the Fed’s SEP releases at federalreserve.gov remain the recommended sources for updated projections.

Powell ruled out rate hikes as any base case after the April 29 meeting. Incoming economic data reinforces the hold narrative for now: the ISM non-manufacturing PMI for April is projected at 53.8 (versus 54.0 prior), and the University of Michigan May preliminary consumer sentiment reading is projected at 49.3 (versus 49.8 in April), both signalling modest deterioration rather than a sharp move in either direction.

GDP growth blocking rate cuts is the often-overlooked third dimension of the Fed’s current dilemma: Q1 2026 GDP at 2.0% annualised with jobless claims at multi-decade lows removes the recessionary urgency that historically provides political and institutional cover for easing, leaving the committee with inflation above target and no compelling growth argument for moving.

The gap that matters is between market consensus and institutional uncertainty. Futures are pricing certainty. The Fed’s internal dynamics suggest the path is far less settled. Three rate-sensitive asset categories face the most exposure if that consensus unravels:

- Long-duration Treasuries, which would reprice sharply on any shift in the rate trajectory

- REITs, whose valuations are anchored to the assumption of stable borrowing costs

- Utilities, which attract yield-seeking capital that could rotate quickly if cut expectations revive or evaporate

A 83%-87% hold probability sounds reassuring until accounting for the possibility that a Warsh-led Fed with Powell as a dissenting governor reshapes the committee’s direction.

The next major ASX story will hit our subscribers first

A Fed in flux: what investors should watch through mid-2026

Three interlocking uncertainties define the rate outlook from here: the direction of the next rate move, the shape of the Warsh-Powell institutional dynamic, and the incoming economic data that will drive the Fed’s next decision.

The specific releases and events to monitor, in approximate chronological order:

- JOLTS job openings release, scheduled Tuesday (week of May 4)

- ADP private payrolls, scheduled Wednesday (week of May 4)

- April non-farm payrolls, forecast at approximately 73,000 (versus March’s 178,000)

- ISM non-manufacturing PMI for April, projected at 53.8

- April 29 FOMC minutes release (approximately three weeks post-meeting), which will confirm dissenter names and rationales

The University of Michigan May preliminary consumer sentiment reading, projected at 49.3, and elevated oil prices linked to Strait of Hormuz tensions remain live inflation risk variables. The Fed has not yet formally addressed the geopolitical supply chain disruption in official policy communications, making it an unresolved factor that could shift the committee’s calculus.

The Warsh variable: what his confirmation hearing could signal

Kevin Warsh’s Senate confirmation hearings will offer the clearest early signal of his policy orientation. His public testimony on the pace of cuts, the Fed’s independence from political pressure, and his approach to consensus-building will shape market expectations before he casts a single vote. Until he is confirmed and his stance clarified, institutional uncertainty at the Fed remains elevated. His working relationship with Powell as a fellow board member, should Powell remain, will be a defining dynamic once he is seated.

Investors wanting to model the full scope of policy risk under a Warsh-led Fed will find our deep-dive into Warsh’s balance sheet strategy covers the three market-moving questions beyond the fed funds rate: accelerated quantitative tightening that could steepen the yield curve even as short rates hold, bank capital deregulation, and a proposed communication overhaul that would eliminate the dot-plot and reduce press conference frequency.

Investors who build a monitoring framework around these data points and institutional events will be better positioned to anticipate shifts than those relying solely on futures pricing, which currently underweights the disruption risk embedded in the leadership transition.

The fracture beneath the headline, and why it matters more than the rate decision itself

The hold at 3.5%-3.75% was the least surprising element of April 29. The dissent pattern, the statement language shift signalling greater uncertainty on future cuts, and the Powell board announcement are the developments that carry lasting market relevance.

Powell characterised risks as broadly balanced after the meeting, describing the Fed as having provided sufficient insurance against employment risks while keeping rates at neutral to weigh on inflation. He ruled out hikes as a base case and indicated the next move would more likely be a cut, but offered no commitment on timing.

Those reassurances are complicated by the committee’s internal fracture. A chair who says risks are balanced speaks with less authority when four of his colleagues formally disagreed with the decision in the same meeting.

Fed funds futures continue to price an 83%-87% probability of no change through year-end. That may prove correct. But a fragmented Fed is a Fed whose communications carry less market-calming power, and the leadership transition ahead has no modern playbook. Positioning in rate-sensitive assets should account for the possibility that guidance reliability will deteriorate through the second half of 2026, regardless of which direction rates ultimately move.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.