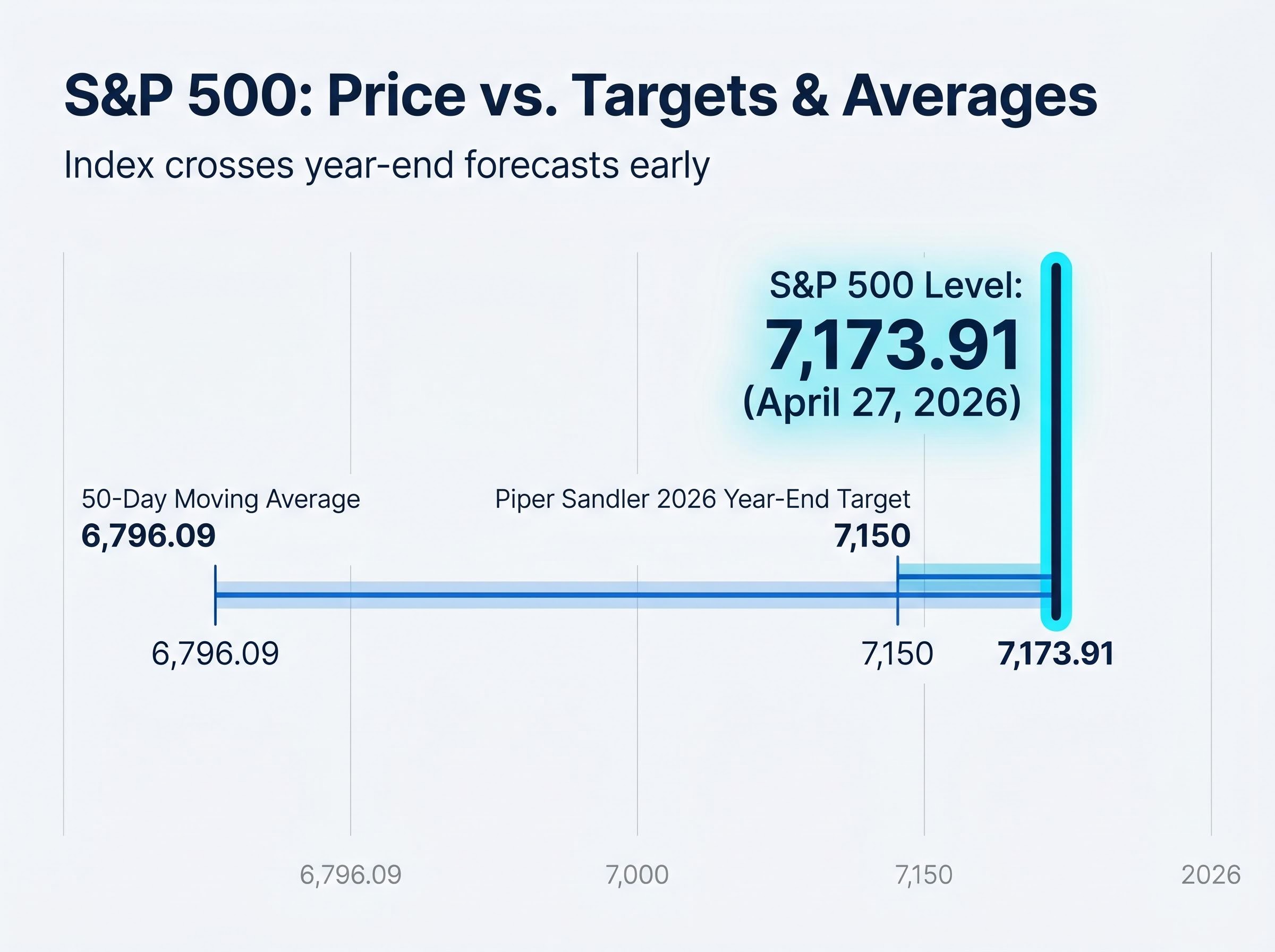

While the S&P 500 closed at 7,173.91 on April 27, 2026, hitting Piper Sandler‘s full-year target with eight months remaining, one of Wall Street’s most-watched technicians is not celebrating. US equity markets have climbed to record highs even as WTI crude trades near $100 per barrel and the Strait of Hormuz remains disrupted.

Institutions from Morningstar to Morgan Stanley are flagging a systematic underpricing of stock market risk across asset classes. The contradiction between price action and underlying geopolitical conditions is the central tension of this moment.

This analysis unpacks Craig Johnson’s warnings and the psychological mechanics driving retail complacency. It details the concrete geopolitical catalysts that could reprice markets quickly and what history says happens when investors ignore these signals long enough.

The market has already hit its year-end target, and that is part of the problem

The mathematics of the current rally present an immediate structural challenge. Johnson’s initial 2026 forecast set a year-end S&P 500 target of 7,150, representing roughly 5%-6% upside from earlier in the year. The index crossed that threshold in late April, compressing the remaining forecasted upside into zero.

Johnson structured his 2026 outlook around a “jump, slump, and pump” pattern, anticipating a difficult middle period that the market may now be entering. He views current conditions as a rotational bull market rather than a broad-based advance. Weak conviction in current momentum indicators argues against buying dips automatically.

This rotational environment is further complicated by growing corporate energy risks, as approximately two-thirds of large companies have already flagged rising input costs in their first-quarter earnings reports.

Investors assuming record highs confirm absolute safety must reconcile those highs with cooling participation beneath the surface. Johnson is monitoring three specific technical warnings:

S&P 500 target fulfillment, removing structural support for continued upward momentum The index trading dangerously far above its 50-day moving average of 6,796.09 as of April 27, 2026 * Deteriorating conviction signals that suggest the rally is narrowing

“We still believe a washout low is ahead of us amid mounting global tensions.”

The fulfillment of a bullish target in April forces a critical evaluation of what drives the next leg higher.

When big ASX news breaks, our subscribers know first

Why retail investors turned bullish at exactly the wrong moment

Market sentiment often moves inversely to concrete geopolitical threats. According to reports, the American Association of Individual Investors (AAII) sentiment survey showed bullish retail positioning rising to nearly 50% in mid-April 2026. This represents a sharp climb from approximately 33% just before the US-Iran conflict escalated.

This surge in optimism happened alongside the conflict, suggesting a wilful dismissal of external threats. According to Johnson, this reflects a well-documented psychological pattern where participants systematically ignore variables they cannot directly price.

Investors often set aside unquantifiable geopolitical risks when underlying price momentum remains strong, prioritising the immediate trend over the abstract threat.

This retail complacency directly contradicts macroeconomic indicators. Bank of America data shows consumer expenditure climbing, despite elevated energy costs compressing household budgets.

Consumer confidence vs. investor confidence: a widening split

The divergence between retail equity optimism and broader economic anxiety is widening. While AAII bullish readings approach 50%, consumer sentiment has fallen to record lows. This split represents an unstable equilibrium. Spending is currently being sustained by savings drawdowns rather than wage growth, creating a fragile foundation for the equity optimism observed in the AAII data.

Recent University of Michigan consumer surveys reveal a growing wealth gap where confidence gains among stock owners are completely offset by declining optimism among households without equity exposure.

What the geopolitical risk actually looks like in practice

The abstract threat of conflict translates into portfolio loss through very specific mechanical pathways. The US-Iran conflict remains locked in a prolonged limbo phase, with a blockade of Iranian ports and intermittent threats to close the Strait of Hormuz. Iran announced a brief reopening on April 17, 2026, only to reverse the decision the following day. By April 19, 2026, the US seized an Iranian-flagged vessel, cementing the disruption.

According to reports, the Strait of Hormuz handles roughly 20% of global oil trade, making it the primary artery for energy markets. Estimates suggest clearing the strait for safe commercial shipping could take six months once peace is achieved. Consequently, WTI crude traded at approximately $99-$100 per barrel as of April 29, 2026, embedding inflation pressure directly into corporate cost structures.

The US Energy Information Administration analysis confirms this maritime chokepoint accommodates over one quarter of total global seaborne petroleum trade, leaving international supply chains highly exposed to prolonged blockades.

Morningstar stated on April 20, 2026, that markets have become “too complacent” amid these price spikes.

| Risk Factor | Current Status | Market Implication |

|---|---|---|

| US-Iran Conflict | Ongoing, intermittent Hormuz closures | Prolonged supply chain disruption |

| WTI Crude Oil | ~$99-$100/barrel (April 29, 2026) | High inflation passthrough risk |

| Brent Crude Oil | ~$112/barrel (mid-April 2026) | Elevated global energy input costs |

| Analyst Sentiment | Flagging high market overvaluation | Underpriced systematic portfolio risk |

Johnson highlighted three specific catalysts that could force an immediate repricing:

- Broader economic fallout from sustained Middle East hostilities

- Additional direct disruptions to the Strait of Hormuz

- A widening of the conflict to involve neighbouring oil producers

What history says about markets that ignore geopolitical shocks

Financial history offers a clear pattern regarding delayed reactions to geopolitical crises. The record shows that the variable separating brief volatility from painful drawdowns is whether markets had already priced in the risk before escalation. Morgan Stanley characterises the current environment as a “tightrope” due to stretched expectations and unpriced political vulnerabilities.

JPMorgan and LPL Research note that while markets historically absorb short-term shocks, prolonged disruptions compound existing valuation pressures.

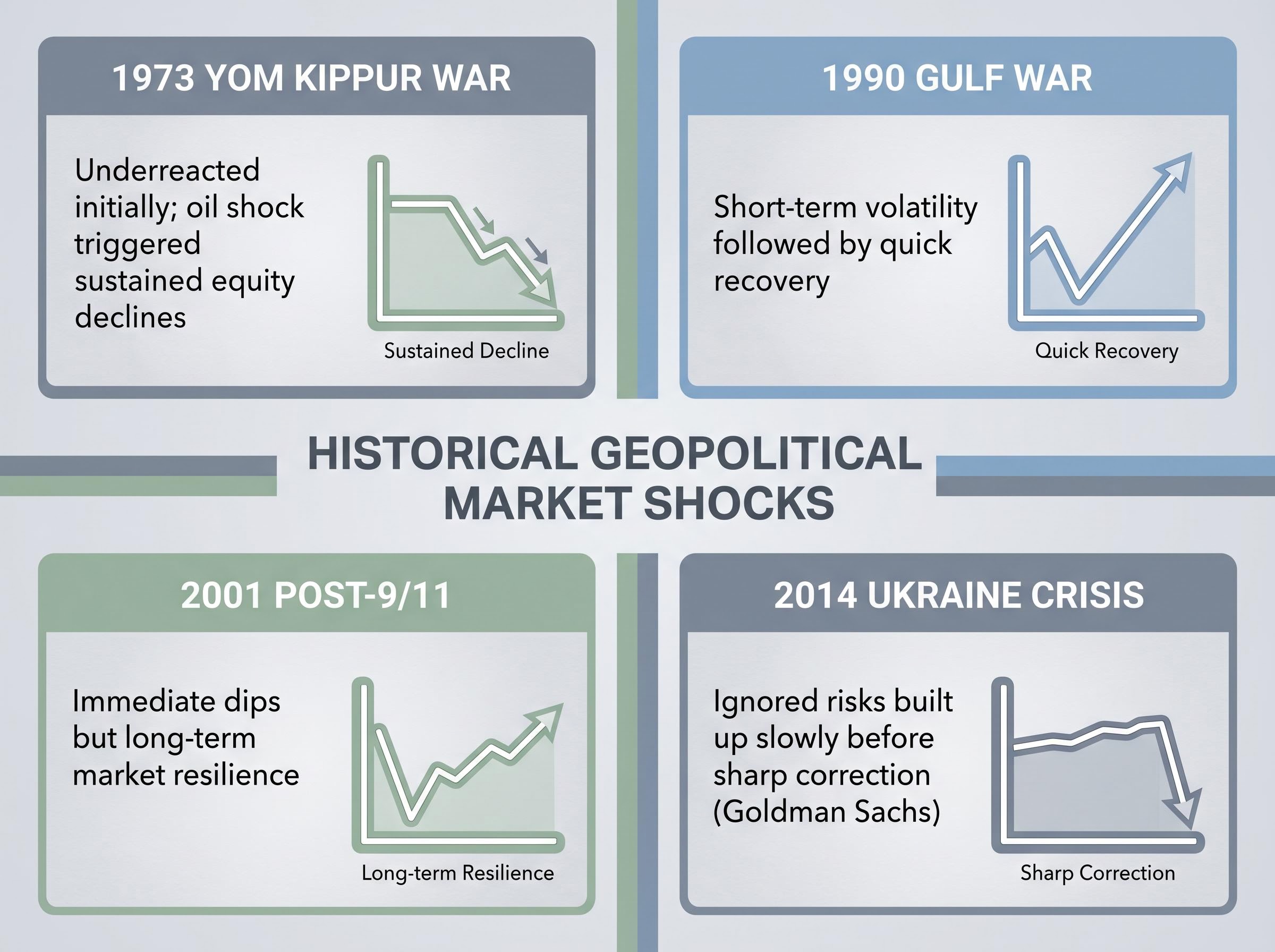

Four key historical precedents illustrate this dynamic:

1973 Yom Kippur War: Markets underreacted initially before the resulting oil shock triggered significant, sustained equity declines. 1990 Gulf War: Caused short-term volatility followed by a quick recovery, as the conflict timeline remained contained. 2001 Post-9/11: Triggered immediate dips but demonstrated long-term market resilience over varied recovery timelines. 2014 Ukraine Crisis: Ignored risks built up slowly before tipping the market into a sharp correction.

“The 2014 crisis served as an inflection point where previously dismissed regional risks suddenly forced a broad market correction,” according to Goldman Sachs analysis.

The 1973 Yom Kippur War serves as the closest parallel to current oil-driven risks. When geopolitical shocks combine with elevated valuations and inflation, the delayed reckoning is often severe.

For readers wanting to model the downside scenarios if these geopolitical pressures push the economy into contraction, our deep-dive into historical recessionary drawdowns examines past 32% average market declines and how corporate earnings historically reprice.

Underlying economic vulnerabilities: consumer spending and the K-shaped economy

Beneath the headline spending data, structural vulnerabilities are eroding the foundation of the current rally. According to reports, Paul Donovan from UBS argues that developed economies have not yet felt the true weight of elevated oil prices. He suggests the reckoning is deferred rather than cancelled, as households draw down savings to sustain spending amid elevated energy costs.

Aggregate consumer expenditure climbed. However, this headline strength masks a severe K-shaped dynamic.

Three layers of hidden pressure threaten this balance:

Aggressive savings drawdowns masking real demand weakness Income bifurcation separating high-earner resilience from low-earner distress * Direct oil price passthrough to everyday household input costs

Lower-income households are absorbing the shock that markets are ignoring

Elevated gasoline costs consume a disproportionately larger share of lower-income household budgets. Higher-income households are sustaining the aggregate spending data, while lower-income demographics face severe spending compression.

When pump prices cross critical thresholds, the historical impacts of expensive gasoline demonstrate that consumer discretionary spending contracts sharply, a pattern that has consistently weighed on broader equity returns over the subsequent six months.

This lower-income spending compression acts as a leading indicator for broader demand softening. Equity market earnings forecasts generally project sustained margin growth, leaving valuations highly vulnerable if this hidden demand weakness materialises.

Record prices, mounting risks, and what a careful investor actually does now

Navigating this contradiction requires a framework grounded in specific geopolitical tripwires rather than broad index levels. Johnson maintains a long-term bullish stance but advocates near-term caution, advising against rushing to buy S&P 500 dips given the weak internal conviction of the current rally. His characterisation of a rotational bull market suggests investors should focus on selective positioning rather than broad index exposure.

Sarah Breeden, Deputy Governor of the Bank of England, shares this cautious outlook regarding current valuations.

Overvalued equities could be highly vulnerable to a meaningful correction if current macroeconomic and geopolitical risks crystallise.

Analysts at Investing.com assess that market participants are materially underestimating the risks associated with the Middle East conflict. To manage this exposure, investors must monitor three specific escalation signals:

- Strait of Hormuz status: Any definitive closure or prolonged timeline for clearing the shipping lanes.

- Oil price trajectory: WTI crude sustaining levels above $100 per barrel, embedding permanent inflation.

- Conflict scope: Evidence of the US-Iran standoff pulling in additional regional actors.

Focusing on these concrete triggers replaces vague unease with a structured method for evaluating incoming data.

Investors exploring how specific price thresholds might force mechanical market selling will find our detailed coverage of institutional sell triggers, which breaks down the specific commodity levels that major banks project will initiate a widespread equity correction.

The record is real, but the runway is shorter than it looks

Markets trading at record highs are not inherently safe, particularly when those highs have already consumed the forecasted upside for the entire year. The risk environment continues to accumulate, demanding vigilance over complacency. Long-term structural bulls can still hold a near-term posture of caution, as the two positions are not mutually exclusive.

The forward-looking signal is not whether the index holds a specific level today, but whether the Strait of Hormuz resolution and the oil price trajectory begin to align with the market’s optimism.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to volatile market conditions.