Fed Holds Rates but Dot Plot Signals a Hike Before Year-End

3 hrs ago

Starbucks shares jumped approximately 5.16% following the release of the company’s second-quarter fiscal 2026 earnings, but the most significant Wall Street development for any long-term Starbucks stock forecast was quieter. Two separate sell-side firms revised their multi-year profit models, projecting a recovery arc that extends well beyond the immediate quarterly result. The latest figures confirmed that Chief Executive Officer Brian Niccol’s operational turnaround is gaining measurable traction.

Comparable store sales rose 6.2%, non-GAAP earnings per share reached $0.50 to beat the $0.43 consensus, and operating margins expanded across both GAAP and non-GAAP metrics. The company subsequently raised its full-year guidance, establishing a higher baseline for the coming quarters.

For investors evaluating the equity beyond the near-term price movement, the central question revolves around the durability of this multi-year earnings trajectory. This analysis examines the specific frameworks Evercore and Wolfe Research are using to model the company’s profit recovery through fiscal 2028. It outlines where the two firms diverge in their estimates, what conditions must materialise for the bull case to hold, and where structural execution risks remain.

The headline metrics from the second quarter demonstrate a broad operational improvement that stretches beyond simple price increases.

Key second-quarter fiscal 2026 results include: Global comparable store sales: Increased 6.2%, driven primarily by transaction volume growth rather than pricing alone. Consolidated net revenues: Rose 9% year-on-year to $9.5 billion. Earnings per share: Non-GAAP EPS reached $0.50, representing a 16.3% beat against the $0.43 Wall Street consensus, while GAAP EPS grew 32% year-on-year to $0.45. Operating margins: GAAP margins expanded 180 basis points to 8.7%, with non-GAAP margins expanding 120 basis points to 9.4%.

The transaction-led nature of this recovery carries specific implications for margin durability. Volume growth is historically more difficult to sustain than price-led growth, yet it signals a genuine demand recovery rather than a temporary revenue mix shift. This recovery pattern is particularly evident in the domestic market.

The official quarterly earnings release details the exact revenue mix changes that analysts are using to build their revised models. Management’s breakdown of transaction volume versus ticket size provides the core data supporting this qualitative shift.

Evercore Market Analysis “North America same-store sales growth improved by 13 percentage points across the six most recent quarters.”

Following these results, management raised fiscal 2026 guidance, targeting comparable sales growth of 5% or greater and a non-GAAP EPS range of $2.25 to $2.45. This updated guidance provided sell-side analysts with a credible anchor to adjust their multi-year projections upward.

Evercore responded to the second-quarter results by reconstructing its earnings expectations through the end of fiscal 2028. The firm’s outlook is supported by a specific sequence of margin recovery assumptions.

The revised model relies on three primary margin drivers. The company is now lapping its prior periods of heavy labour reinvestment, coffee cost inflation is expected to moderate, and a comprehensive productivity savings programme is beginning to yield measurable financial benefits. Evercore analysts note that profit flow-through is still building and has not yet reached full velocity.

The most analytically striking component of the Evercore thesis centres on domestic profitability. The firm projects North America incremental margins will experience a sharp reversal. If the company can convert more than half of each incremental revenue dollar into profit domestically next year, the earnings compounding effect becomes self-reinforcing.

| Fiscal Year | Previous EPS Estimate | Revised EPS Estimate | Change |

|---|---|---|---|

| FY26 | $2.30 | $2.45 | +$0.15 |

| FY27 | $3.09 | $3.25 | +$0.16 |

| FY28 | $3.92 | $4.00 | +$0.08 |

The upward trajectory in the later years relies heavily on cumulative productivity savings. These accumulated cost reductions function as a structural margin floor for the business. By removing fixed costs from the operational model, the savings reduce the degree to which pure revenue growth must carry the entire earnings recovery burden.

The success of this comprehensive productivity savings program will directly determine if the company can offset persistent labor costs and fund essential store upgrades.

While Evercore anchors its thesis in margin mathematics, Wolfe Research focuses on leading indicators of consumer demand. Two recent strategic initiatives serve as the primary testing grounds for the company’s ability to drive sustained transaction volume.

The company executed a major restructure of the Starbucks Rewards programme in March 2026. Early qualitative commentary surrounding the redesign has been positive, though the market currently lacks verified quantitative data regarding adoption rates or engagement percentages.

Wolfe Research Observation Early indications regarding the restructured loyalty programme appear “promising,” providing initial validation for the strategic pivot.

Simultaneously, the April 2026 launch of the Energy Refresher product line represents a specific test of the company’s ability to expand its addressable market. The initiative attempts to capture consumer occasions beyond traditional coffee visits, with early channel checks suggesting the product is performing in line with or ahead of internal expectations.

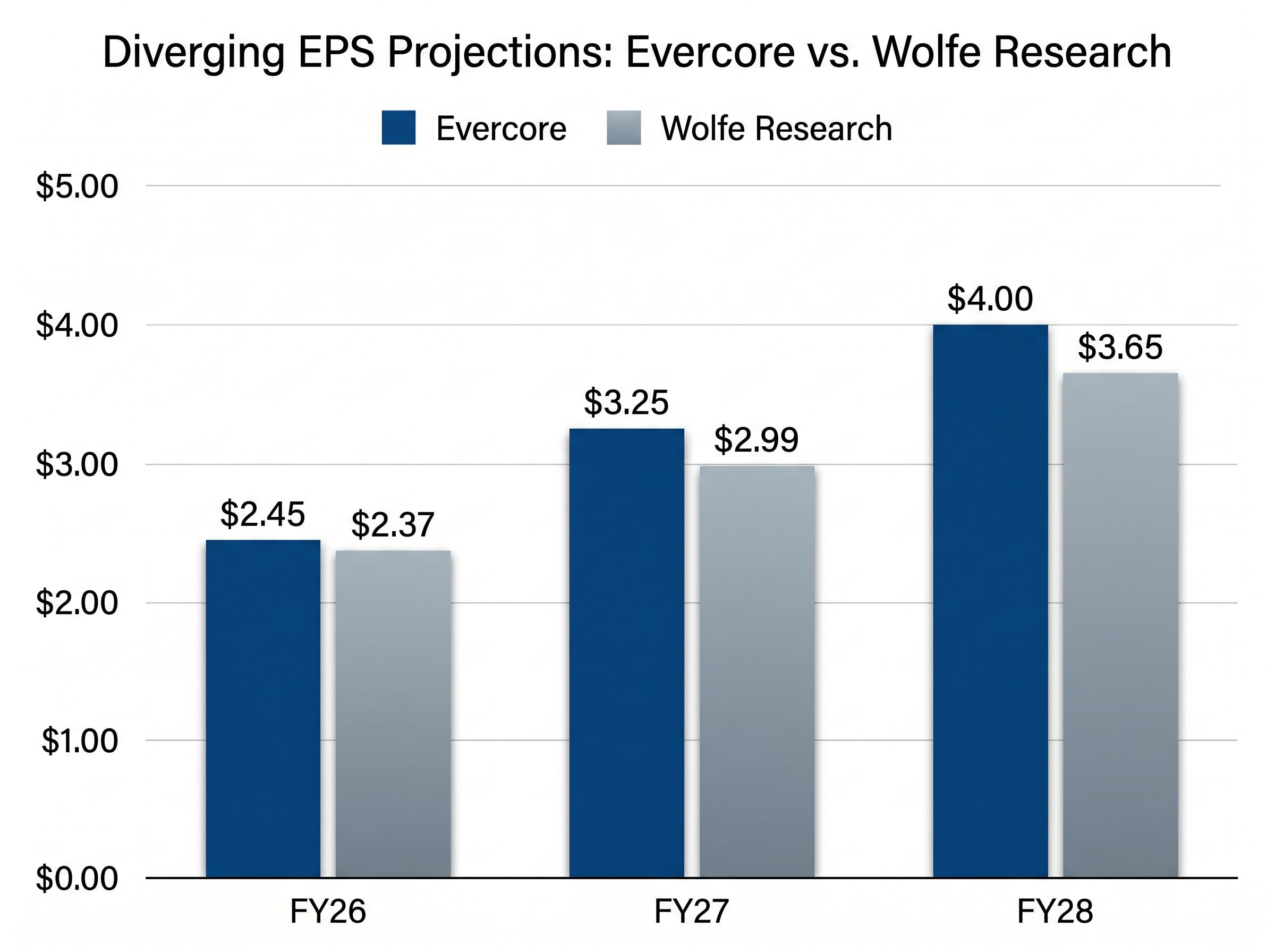

Despite these positive qualitative signals, Wolfe Research maintains a structurally more conservative financial model than Evercore. The firm models a slower margin recovery, creating a meaningful divergence in outer-year earnings projections.

These diverging long-term EPS forecasts highlight a fundamental disagreement over whether peak profitability is a permanent structural relic or an attainable target by 2028.

| Fiscal Year | Evercore EPS Estimate | Wolfe Research EPS Estimate |

|---|---|---|

| FY26 | $2.45 | $2.37 |

| FY27 | $3.25 | $2.99 |

| FY28 | $4.00 | $3.65 |

Investors evaluating these dual frameworks should treat the loyalty and product signals as qualitative leading indicators rather than confirmed financial drivers. Hard engagement metrics in the coming quarters will be necessary to validate either firm’s multi-year earnings model.

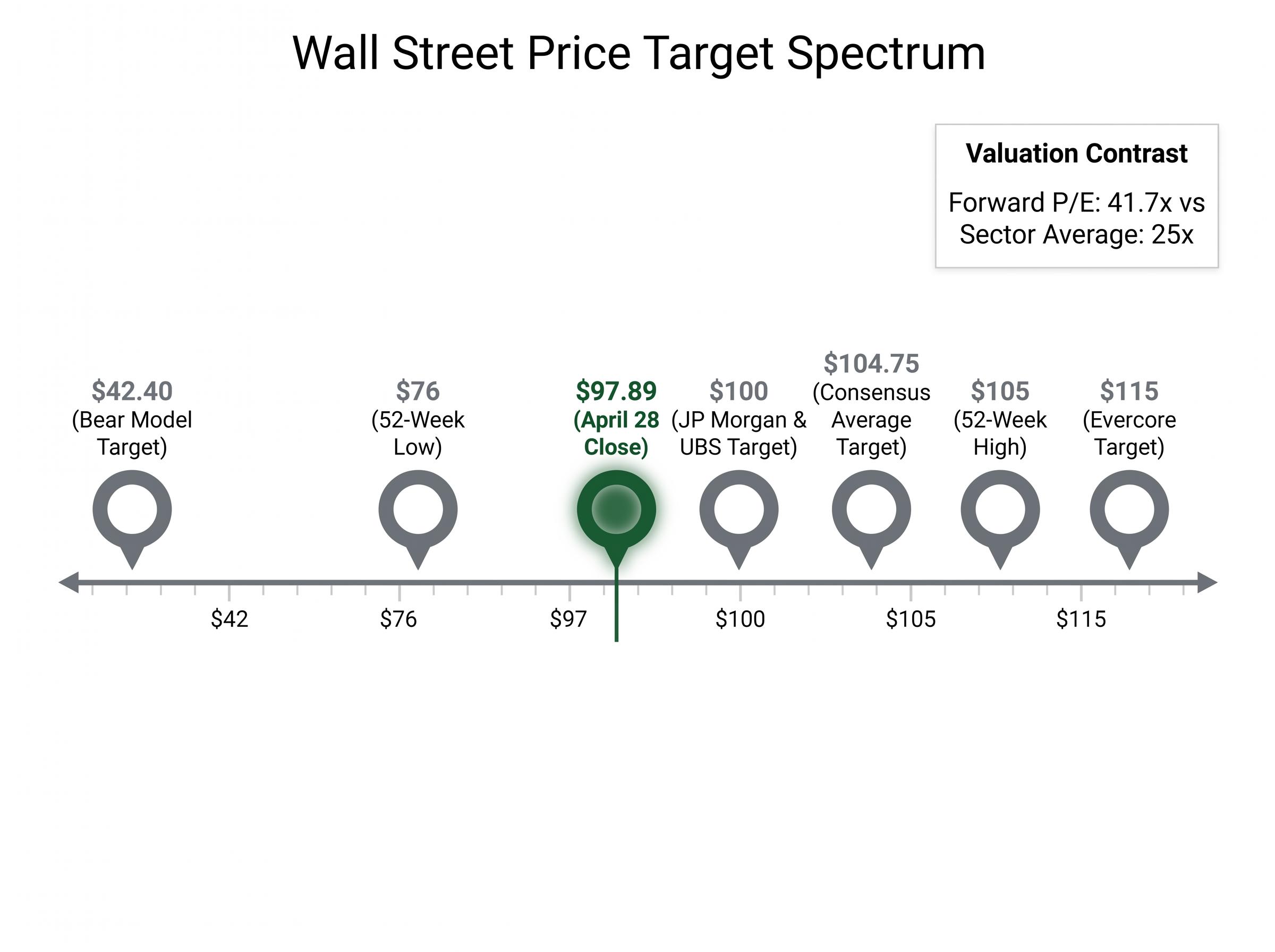

The central tension in the current investment case lies in the price the market is already charging for the recovery. The stock closed at $97.89 on April 28, trading within a 52-week range of $76 to $105. Based on the fiscal 2026 non-GAAP EPS guidance midpoint of $2.35, the company trades at approximately 41.7x forward earnings.

Valuation Contrast The current forward price-to-earnings multiple of 41.7x sits at a substantial premium to the consumer discretionary sector average of approximately 25x.

This premium multiple requires specific conditions to hold over the next three years. It prices in continued earnings compounding toward Evercore’s $4.00 fiscal 2028 estimate and assumes flawless execution of the margin recovery strategy. Any meaningful miss on comparable sales momentum would compress the multiple faster than earnings growth could offset the impact.

Additional upside to this premium valuation could emerge if the recent Chinese joint venture restructuring successfully deconsolidates margin-dilutive international operations by the third quarter.

Current Wall Street consensus reflects this valuation tension. The average analyst price target sits at $104.75, implying approximately 7% upside from the April 28 close.

Notable post-earnings positions from the 39-analyst coverage universe include: JP Morgan: $100 price target (Overweight) UBS: $100 price target (Hold) * Consensus Average: $104.75

Approximately 19 analysts maintain a Hold rating on the equity. Furthermore, short interest sits at 45.28 million shares, representing 3.98% of the float. This split consensus indicates genuine institutional uncertainty regarding whether the fundamental recovery can outpace the current valuation multiple.

The institutional caution surrounding the stock is anchored in specific structural variables that could disrupt the projected earnings trajectory. The bear case does not require the company to fail entirely; it only requires the fundamental recovery to progress slower than the 41.7x multiple demands.

Bearish analysts focus on three primary risk pillars that threaten to invalidate the optimistic multi-year models: Commodity price headwinds: Persistent inflation in coffee commodity costs is expected to pressure margins through at least the first half of fiscal 2026. Labour cost investments: Ongoing wage and operational investments at the store level continue to suppress near-term profitability. * Execution risk: The complex rollout and customer adoption mechanics of the restructured loyalty programme introduce potential friction points.

Wolfe Research previously articulated these concerns last month when downgrading the stock to Peer Perform. While the second-quarter margin expansion demonstrated some resilience against these pressures, bearish analysts maintain that current profitability remains materially below the company’s prior peak margin levels. One independent sell-side model currently carries a Sell rating with a $42.40 price target, driven entirely by long-term labour and inflation assumptions.

Tracking global coffee futures market data reveals how tightly raw material costs correlate with the company’s historical margin compression periods. If these agricultural inputs remain elevated, the planned productivity savings could be largely absorbed by basic supply chain expenses.

The market’s initial reaction to the earnings release requires careful interpretation. The stock jumped approximately 5.16% in pre-market trading today on characteristically thin volume. The 3.98% short float is not elevated enough to trigger a forced short-squeeze dynamic, suggesting the immediate price action reflects sentiment relief rather than high-conviction institutional buying.

The multi-year financial projections provided by Evercore and Wolfe Research establish clear quarterly checkpoints for investors. The recently raised fiscal 2026 non-GAAP EPS guidance of $2.25 to $2.45 sets the immediate operational baseline that the market is now pricing against.

Looking further ahead, the gap between the firms’ projections highlights the central debate over margin recovery speed.

The Critical Margin Pivot “North America incremental margins projected to exceed 50% in FY27.”

To determine which firm’s model is tracking closer to reality, investors should monitor four specific operational metrics in the upcoming quarters:

By tracking these specific variables, market participants will gain earlier visibility into whether the underlying operational recovery can support the current valuation multiple.

Investors exploring these varying projections will find our full explainer on Starbucks margin recovery scenarios highly useful, as it breaks down the exact operational shifts required for both the bull and bear outcomes.

The second-quarter fiscal 2026 results confirm that a genuine operational turnaround is underway. The transaction-driven comparable sales growth and the resulting upward revisions to multi-year analyst estimates provide a credible foundation for the fundamental bull thesis. However, trading at approximately 41.7x forward earnings, the equity has already priced in a near-flawless execution of this recovery strategy.

The valuation leaves little room for operational friction. The significant gap between Evercore’s $4.00 and Wolfe Research’s $3.65 fiscal 2028 earnings estimates perfectly encapsulates the range of potential outcomes that investors must weigh. One model assumes the company can successfully expand domestic margins past historical resistance points, while the other anticipates structural headwinds will persist.

Readers evaluating the company’s long-term prospects should begin tracking North America incremental margin disclosures and loyalty engagement data as their primary validation metrics. The third-quarter fiscal 2026 earnings call will serve as the next scheduled catalyst, providing the specific data necessary to test the durability of these multi-year earnings projections.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Starbucks' Q2 fiscal 2026 results were driven by a 6.2% increase in global comparable store sales, primarily from transaction volume growth, and non-GAAP earnings per share of $0.50, which beat the $0.43 consensus. The company also expanded its operating margins.

Evercore projects Starbucks' fiscal 2028 EPS at $4.00, assuming significant North America incremental margin recovery. Wolfe Research, however, maintains a more conservative forecast of $3.65 EPS for fiscal 2028, anticipating a slower margin expansion.

Investors should closely monitor North America incremental margins, the trajectory of coffee commodity costs, verified adoption rates and engagement frequencies for the restructured Starbucks Rewards program, and sales data for the new Energy Refresher product line.

Starbucks currently trades at approximately 41.7x forward earnings based on its fiscal 2026 guidance, representing a substantial premium to the consumer discretionary sector average. This valuation prices in near-flawless execution of its recovery strategy, leaving little room for error.

Primary risks include persistent commodity price headwinds, ongoing labor cost investments at the store level, and execution challenges associated with the complex rollout and customer adoption of the restructured loyalty program.