The investing playbook that protected Australian portfolios through the GFC, the COVID crash, and the 2022 inflation surge is not working in 2026. Bonds are falling alongside equities. Gold sold off despite surging oil prices. The conventional defence is failing precisely when investors need it most.

The Iran War has created a supply-side shock unlike anything most retail investors have navigated. With Brent crude at $116.62 per barrel, Australian headline inflation at 4.6%, and the RBA cash rate now at 4.1% after two consecutive hikes, portfolios face a dual threat: inflation eroding purchasing power while recession risk clouds equity markets. The traditional response, rotating into bonds and gold, has produced losses rather than safety.

This guide explains why the old playbook has broken down, which assets are actually offering defensible positioning right now, and how Australian investors can construct a practical response using accessible ETFs on the ASX.

Why the crisis playbook is failing Australian investors

For roughly four decades, major economic crises followed a consistent pattern. Growth collapsed, deflationary pressure built, central banks cut rates, and bond prices rose. Investors who rotated into bonds and gold during the GFC or the COVID crash were rewarded because those crises destroyed demand, which is exactly what bonds are designed to hedge against.

The Iran War is not a demand shock. It is a supply shock. The closure of the Strait of Hormuz has disrupted approximately 20% of worldwide oil and LNG supply, pushing energy prices sharply higher without any corresponding collapse in consumer spending. Central banks are raising rates to contain inflation, not cutting them to stimulate growth. That single distinction explains why bonds are losing value alongside equities.

The World Bank energy price outlook projecting the largest surge since 2022 estimated a 24% rise in energy prices for the year, providing an independent institutional benchmark for the scale of the supply disruption that Australian portfolios are currently navigating.

Gold, meanwhile, entered this crisis as an already crowded trade. Three factors are compounding the problem:

- Gold generates no income yield, making it costly to hold when cash rates exceed 4%

- An approximately 80% price appreciation over the two years preceding the conflict had attracted speculative positioning, which reversed when margin calls forced liquidation

- US dollar appreciation has raised the cost of gold for non-USD buyers, suppressing international demand

10-year US Treasury yields have risen to 4.36%-4.42%, up from approximately 4.2% pre-escalation. The 2022 precedent is instructive: pandemic supply disruptions compounded by the Ukraine energy shock caused bonds and equities to fall simultaneously, negating the protection bonds were supposed to provide.

The World Bank has warned the Iran War will trigger the largest energy price surge since 2022, underscoring the severity of the supply-side disruption confronting global markets.

Investors who act on the old assumptions risk compounding losses by rotating into assets that remain under pressure.

The phenomenon of safe haven assets failing in a supply-driven crisis is not unique to the Iran War; Australian long bond rates reaching 5.1% represent a decade-high that makes the mechanism of simultaneous bond and equity losses structurally legible rather than anomalous.

When big ASX news breaks, our subscribers know first

What the supply shock actually means for your money: a framework for 2026

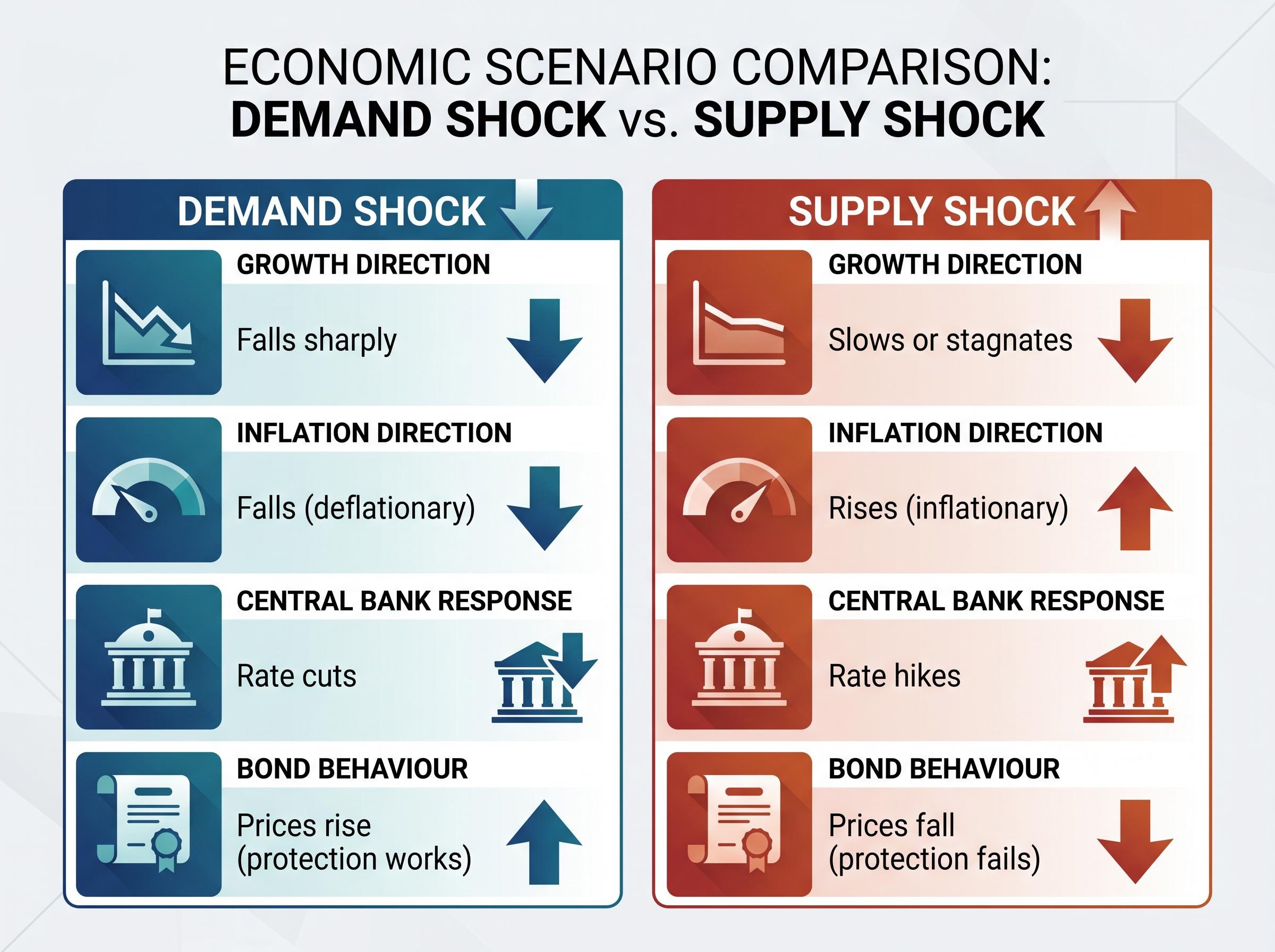

A supply shock and a demand shock look similar on a portfolio statement. Both produce falling equity values and rising anxiety. The difference lies in what is driving the pain, and that difference determines which defences actually work.

A demand shock reduces spending. Consumers and businesses pull back, prices fall, and central banks respond by cutting interest rates. Bonds rally because lower rates push bond prices up. A supply shock does the opposite. The quantity of goods available shrinks, pushing prices higher even as economic activity slows. Central banks are forced to raise rates to contain inflation, which pushes bond prices down.

The result is a condition economists call stagflation: simultaneously low growth, elevated inflation, and restrictive financing costs. It is the worst environment for both bonds and equities at once. The RBA’s decision to raise rates to 4.1% following hikes in both February and March 2026, with Australian headline CPI at 4.6% and Brent crude up approximately 40% since the escalation began, fits this pattern precisely.

The rules of stagflation investing in a supply shock shift materially when the shock is supply-side rather than demand-side: the RBA’s forecast terminal cash rate of 5.00% implies a more prolonged tightening cycle than the current 4.1% rate suggests, which has direct implications for how long duration risk in fixed income portfolios remains elevated.

The RBA monetary policy decision confirming successive rate increases identified inflation picking up materially through the second half of 2025 as the primary driver, placing the cash rate at 4.10% and signalling that the board remains focused on returning inflation to target before considering any easing.

| Dimension | Demand Shock | Supply Shock |

|---|---|---|

| Growth direction | Falls sharply | Slows or stagnates |

| Inflation direction | Falls (deflationary) | Rises (inflationary) |

| Central bank response | Rate cuts | Rate hikes |

| Bond behaviour | Prices rise (protection works) | Prices fall (protection fails) |

The US dollar has emerged as the one traditional safe haven still functioning as expected. US energy self-sufficiency and revised Federal Reserve rate expectations have supported the greenback, pushing the AUD/USD to 0.7183, down approximately 2% amid risk-off sentiment. LNG prices have risen approximately one-third since the war began, adding further inflationary pressure to Australian energy costs.

What history tells us about supply shock recoveries

The 1970s oil embargo remains the closest historical parallel. During that crisis, Australian inflation reached 17.6% and equities fell approximately 40%. The recovery was slow, measured in years rather than quarters.

The 2022 episode offers a more recent reference point. Fuel-driven CPI spikes in Australia demonstrated the lag between energy price increases and broader consumer inflation. Markets eventually recovered, but the path was uneven and tested investor discipline.

One structural difference matters. The current crisis is more narrowly focused on energy than 2022, which involved simultaneous pandemic recovery pressures, supply chain disruptions, and energy shocks. A more singular cause could mean a more singular catalyst for recovery.

The honest case for each asset class right now

Each asset class deserves an honest appraisal rather than a blanket recommendation. The right choice depends on individual circumstances, and the evidence for and against each option is more nuanced than headlines suggest.

Cash and short-duration instruments represent the most straightforwardly defensive option. AAA (BetaShares Australian High Interest Cash ETF) is yielding 3.90% with a year-to-date return of 1.23% and net assets of $5.09 billion. Capital is preserved, and the yield compensates for waiting.

AAA recorded approximately $789 million in inflows in March 2026 alone, a clear signal of where defensive investors are already moving capital.

Floating rate bonds offer a middle path. QPON (BetaShares Australian Bank Senior Floating Rate Bond ETF), with a NAV of $26.23 and five-year annualised performance of 3.64% p.a., provides yield without the duration risk punishing fixed-rate bonds. Its floating rate structure adjusts as the RBA raises rates, protecting rather than eroding value.

Fixed-rate bonds carry a more complicated case. VAF (Vanguard Australian Fixed Interest ETF) offers approximately 4.0% yield, but duration risk remains if further RBA hikes materialise. The income is real; the capital risk is also real.

Gold is up approximately 10% since early 2026 despite the early sell-off, reflecting a partial recovery of safe haven demand. The long-term structural case remains intact. The near-term headwinds from US dollar strength and position unwinding have not fully resolved.

Equities are volatile and under pressure, but the case for quality-factor stocks deserves a hearing. Companies selected for high return on equity, low leverage, and earnings stability tend to show lower earnings sensitivity during stagflationary periods. BlackRock pivoted in mid-April 2026 to overweighting US stocks, concluding that conflict damage is largely contained.

| Asset Class | Representative ETF | Approx. Yield / Return | Key Risk | Suitability |

|---|---|---|---|---|

| Cash | AAA | 3.90% yield | Inflation erosion over time | Near-term defence |

| Floating rate bonds | QPON | 3.64% p.a. (5-yr) | Credit risk if recession deepens | Income with rate protection |

| Fixed-rate bonds | VAF | ~4.0% yield | Duration risk from further hikes | Income seekers with rate view |

| Gold | Gold ETFs | ~10% YTD | USD strength, crowded positioning | Long-term inflation hedge |

| Quality equities | AQLT / QLTY | Volatile | Earnings compression risk | Long-term growth exposure |

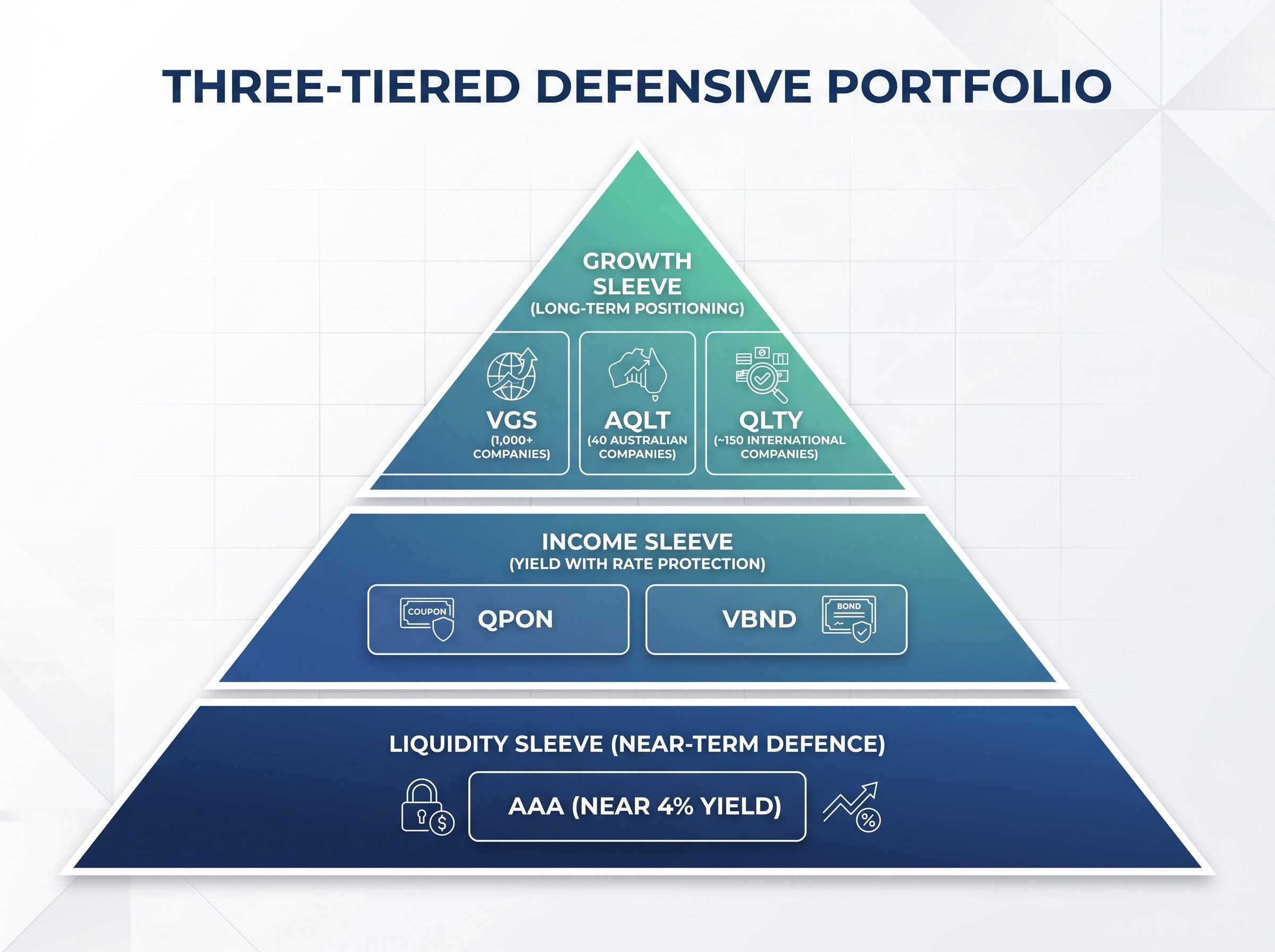

How to build a defensive Australian portfolio without abandoning growth

The evidence points toward a tiered approach rather than a single allocation decision. Three portfolio sleeves, each serving a distinct purpose, provide structure without being prescriptive about individual circumstances.

- Liquidity sleeve (near-term defence): AAA for capital preservation at near 4% yield. This sleeve covers near-term spending needs and provides dry powder if opportunities emerge.

- Income sleeve (yield with rate protection): QPON for floating rate exposure that adjusts with RBA tightening. VBND (Vanguard Global Aggregate Bond Index Hedged ETF) for diversified fixed income exposure with currency risk hedged back to AUD.

- Growth sleeve (long-term positioning): VGS for international equity exposure across 1,000+ large developed-market companies. AQLT (BetaShares Australian Quality ETF) for 40 Australian companies selected on return on equity, low leverage, and earnings stability. QLTY (BetaShares Global Quality Leaders ETF) for approximately 150 international companies selected on quality metrics.

The balance between these sleeves depends on time horizon, near-term spending requirements, and actual risk tolerance rather than current sentiment. Excessive cash allocation forgoes income opportunity. Excessive equity allocation ignores genuine near-term risks.

Australian super funds have consistently urged members not to panic, pointing to historical precedents that support staying invested through geopolitical disruptions.

For investors wanting to implement the growth sleeve with greater sector-level precision, our dedicated guide to investing during rate hikes covers equity selection criteria across power generation, semiconductors, and oil services, with specific guidance on identifying low-debt, high-margin companies that retain pricing power in a capital-constrained environment.

Why staying invested beats waiting for clarity

Markets have historically rebounded from geopolitical conflicts once a credible path toward de-escalation emerges, even without complete resolution. Wars generally produce temporary market impacts, and rate-sensitive assets could appreciate significantly once conflict de-escalation becomes visible.

Systematic investing, making regular contributions regardless of market conditions, removes the market-timing problem from the equation. It allows investors to accumulate at lower prices during periods of volatility and avoids the reinvestment paralysis that traps those who move entirely to cash.

There is also a case that markets may be overestimating how far rates need to rise. The RBA cash rate is already at 4.1%, and further tightening risks tipping the economy into recession, which could prompt a policy reversal sooner than current pricing suggests.

Where the recovery opportunity hides if de-escalation arrives

Defence and opportunity are not mutually exclusive positions. Investors who remain partially allocated to growth assets retain access to a recovery that could arrive faster than the consensus expects.

The asymmetry is worth considering. A fully cashed-out investor locks in current prices and faces reinvestment risk when sentiment shifts faster than they can respond. Rate-sensitive assets, including longer-duration bonds and quality growth equities, are the categories most likely to benefit sharply from a de-escalation signal that causes markets to reprice rate expectations downward.

Vaughan Nelson CIO Chris Wallis has noted that energy price lags are still working through the system, suggesting the current inflation peak may not yet fully reflect subsequent conditions. Once those lags are absorbed, the inflationary pressure easing could be more rapid than gradual.

The recovery timeline could also be accelerated by long-term disinflationary forces operating in parallel with the energy shock: AI-driven efficiency gains and Chinese manufacturing overcapacity are actively suppressing costs in sectors outside energy, which means the inflation peak implied by current RBA pricing may arrive sooner than a pure energy analysis would suggest.

Several signals would indicate a recovery inflection point:

- A ceasefire announcement or formal de-escalation agreement

- Reopening of the Strait of Hormuz to commercial shipping

- The RBA pausing or signalling an end to rate hikes

- Oil prices retreating meaningfully toward pre-war levels

BlackRock pivoted in mid-April 2026 to overweighting US stocks, concluding that conflict damage is largely contained. When one of the world’s largest asset managers shifts from defence to offence, it represents an institutional signal worth considering.

The current crisis is more narrowly focused than 2022, which means the recovery catalyst, whether a ceasefire or the reopening of shipping lanes, is more singular and potentially more rapid in its market impact.

The same market that is testing your patience is setting your next return

The playbook has changed. The fundamental discipline has not. Staying diversified, maintaining liquidity, and remaining invested through volatility are principles that have outlasted every prior crisis, including the ones that felt unprecedented at the time.

The practical framework is straightforward: cash and floating rate instruments for near-term defence, quality equities and diversified bonds for long-term positioning, and systematic contributions to remove market-timing risk from the equation.

The more useful question for most investors is not “where should markets go?” but rather “does my current allocation actually match my time horizon and risk tolerance, or does it simply reflect recent anxiety?” If the answer is the latter, a conversation with a financial adviser may be more valuable than any single trade.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.