Australian long bond rates have hit 5.1%, a decade high. Brent crude is trading between $105 and $120 per barrel after the Iran War closed the Strait of Hormuz, triggering what the International Energy Agency has called the largest oil supply disruption in recorded history. Bonds are falling alongside equities. Gold has sold off. The Australian dollar sits at 0.7113 against the USD as of 30 April 2026, and the Westpac-Melbourne Institute Consumer Sentiment Index has collapsed 12.5% in April alone to 80.1.

The assets most investors reach for in a crisis are doing the opposite of what they should. This guide explains which safe haven assets are still functioning, why others have failed, and how Australian retail investors can reposition across cash, fixed income, and quality equities using specific ASX-listed instruments. The framework that follows is designed to support an informed, unhurried decision rather than a reactive one.

How a supply shock dismantles conventional crisis defences

Most investors carry an assumption into every downturn: bonds go up when equities go down, and gold rises when everything else falls. In demand-collapse crises like the GFC or Covid, that assumption held. Central banks cut rates, bond prices rallied, and gold attracted capital fleeing risk.

A supply-driven shock operates on different mechanics entirely. When the disruption originates in energy supply rather than consumer demand, inflation rises at the same time growth weakens. Central banks cannot cut rates to support growth without accelerating inflation further. The result is that bonds and equities fall together, eliminating the diversification benefit that underpins most portfolio construction.

The stagflation investing rules that apply to a supply-side shock differ fundamentally from those used in demand-driven downturns, because central banks cannot ease policy without accelerating the very inflation they are trying to contain, leaving rate hikes as the only available lever even as growth deteriorates.

BIS research on bond-equity correlation shows that the historically negative relationship between bonds and equities shifts toward positive territory during episodes of high and volatile inflation, meaning the diversification benefit that underpins most retail portfolio construction weakens precisely when investors are most exposed.

The Strait of Hormuz normally facilitates transit of roughly 20% of global oil and LNG supply. It has been effectively closed since the escalation of the Iran War.

The environment this creates has a name: stagflation. Three conditions define it:

- Weak growth: Consumer confidence has collapsed and household spending is under pressure from energy costs and elevated borrowing rates.

- Elevated inflation: Oil prices between $105 and $120 per barrel are feeding directly into transport, manufacturing, and retail costs.

- Restrictive interest rates: The RBA cash rate stands at 4.10%, with markets pricing a 74% probability of a further hike to 4.35% at the May meeting.

This combination, last seen in the 1970s, is the environment where conventional safe haven logic fails most completely. US 10-year Treasury yields have risen well above 4% as of early April 2026, and LSEG data has documented the return correlation between global equities and government bonds shifting during supply shocks, reducing the hedging value of bonds precisely when investors need it most.

Understanding why the usual defences are failing is the first step toward identifying what is actually working.

When big ASX news breaks, our subscribers know first

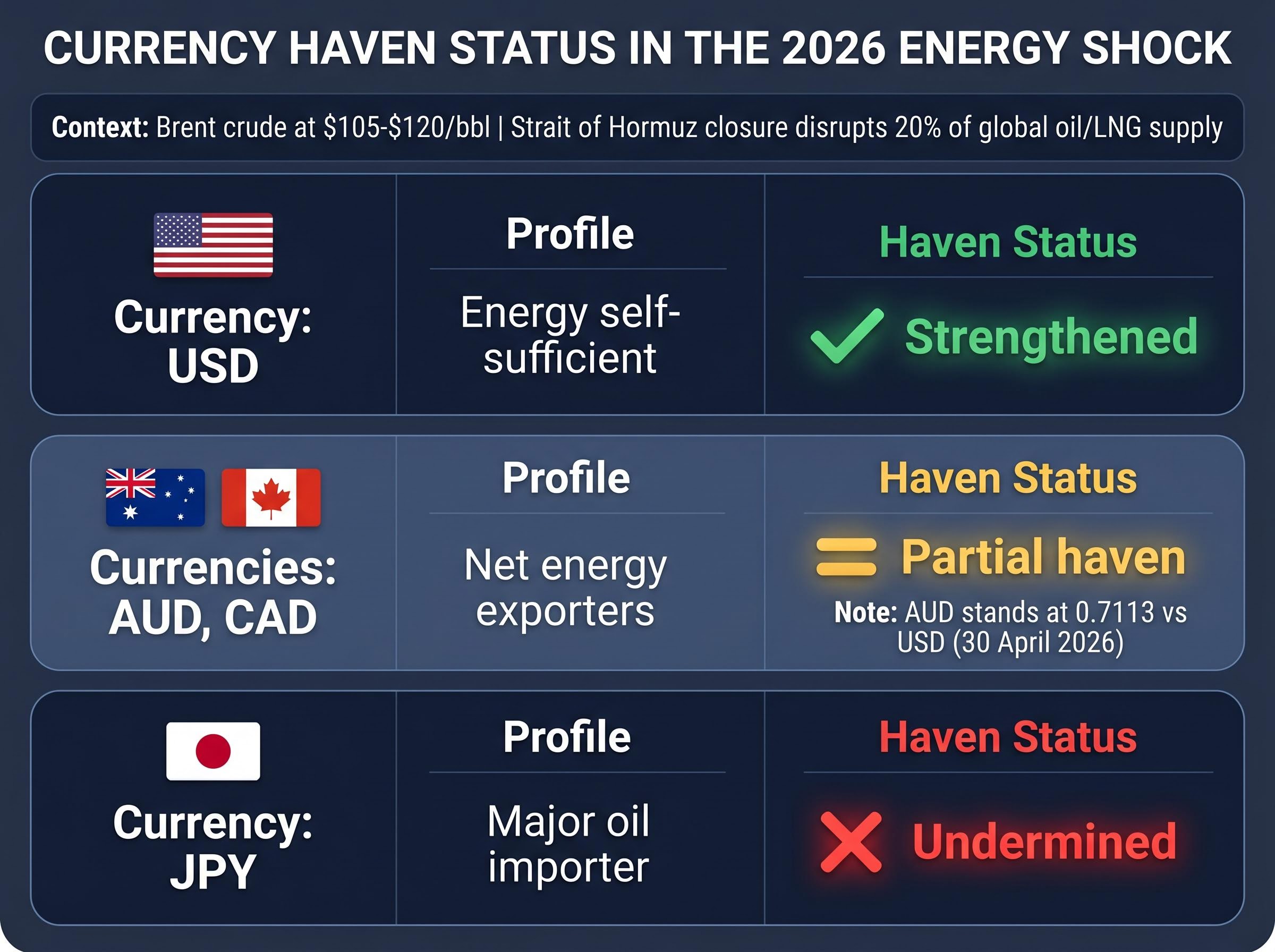

Why energy dependency is now the key driver of currency performance

The US dollar has emerged as the only major currency strengthening through this crisis, and the reason is structural rather than cyclical. American energy self-sufficiency insulates the US economy from the direct cost impact of the Strait of Hormuz closure, while markets are simultaneously pricing in a prolonged period of elevated US interest rates, reinforcing demand for USD-denominated assets.

Japan’s yen, traditionally a haven currency supported by a large trade surplus and substantial overseas investment holdings, has underperformed. The reason is straightforward: Japan imports the vast majority of its oil. The energy cost shock offsets the yen’s structural haven characteristics, leaving it weaker than its historical role would suggest.

For Australian investors, the picture is more nuanced. The AUD and the Canadian dollar have held their ground better than the yen because both economies are associated with net energy-exporting profiles. The AUD’s weakness against the USD (at 0.7113 as of 30 April 2026, according to RBA data) reflects global risk aversion rather than a structural energy-import penalty. Morningstar/Macrobond currency performance data from 17 March 2026 confirmed this pattern, with energy-exporter currencies broadly outperforming energy-importers.

| Currency Group | Energy Profile | Haven Status in Oil Shock | Performance Direction (Current Crisis) |

|---|---|---|---|

| USD | Energy self-sufficient | Strengthened | Appreciating against most majors |

| AUD, CAD | Net energy exporters | Partial haven | Weakened vs USD, outperforming importers |

| JPY | Major oil importer | Undermined | Underperforming despite traditional haven role |

The practical implication is direct: unhedged offshore exposures become more expensive as the AUD weakens, strengthening the relative appeal of domestically denominated assets. Geography-aware positioning is now a portfolio construction variable, not just a macro observation.

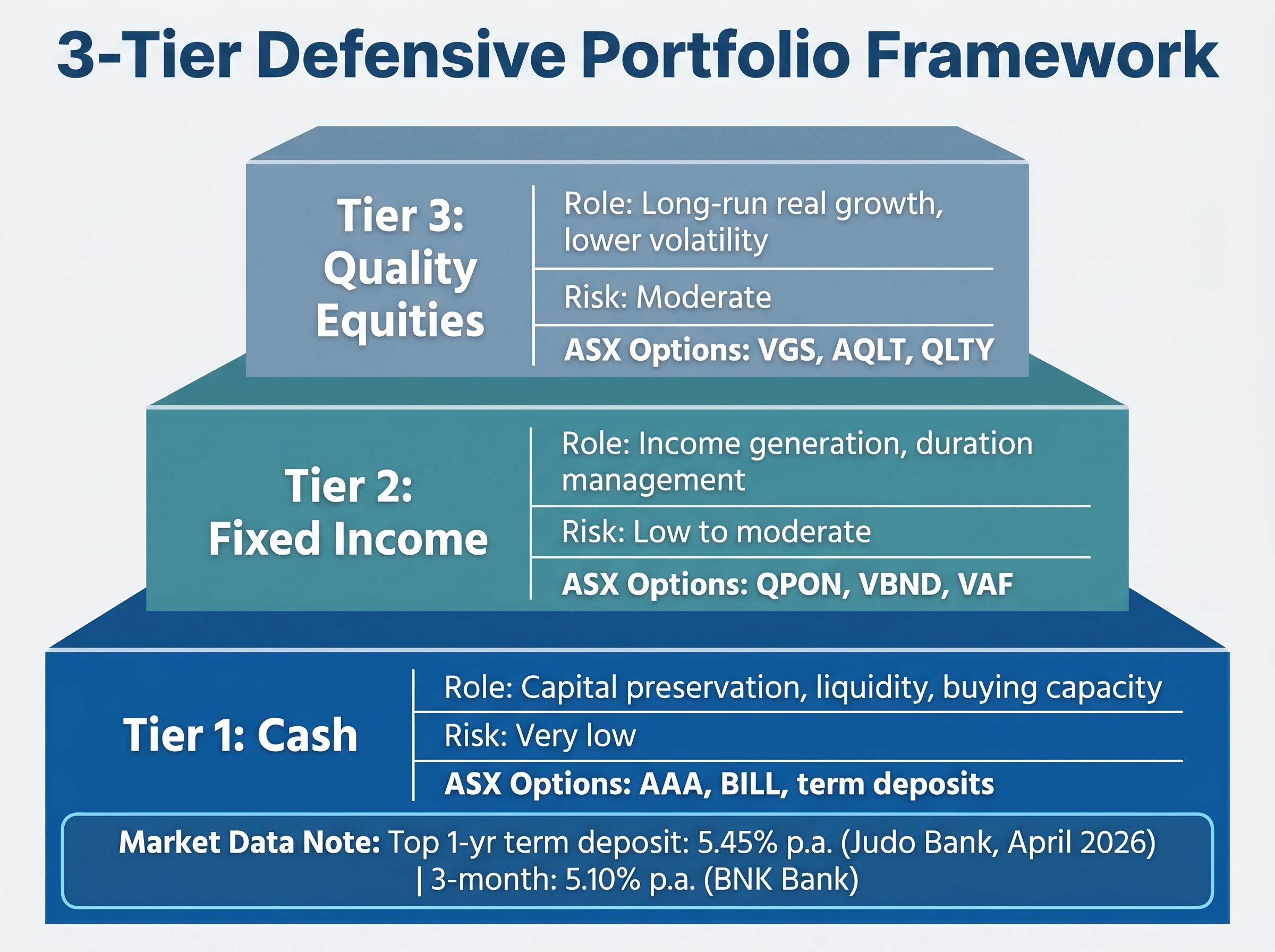

Building a defensive Australian portfolio: cash, fixed income, and quality equities

The defensive framework for this environment has three tiers, each with a distinct role. They function as a coherent system rather than a menu of alternatives.

Cash and cash equivalents serve as the foundation. The role of cash in a stagflationary environment is not passive. It preserves capital, meets near-term spending needs, and creates the capacity to buy undervalued assets when dislocations occur. With the Westpac-Melbourne Institute Consumer Sentiment Index at 80.1 (down 12.5% in April alone), defensive positioning is widely shared across Australian households.

High-interest cash ETFs and term deposits offer meaningfully different characteristics:

- Liquidity: Cash ETFs trade on the ASX and can be sold on any trading day; term deposits lock funds for the agreed period.

- Access: ETFs require a brokerage account; term deposits are opened through a bank.

- Yield comparison: Top 1-year term deposit rates reach 5.45% p.a. (Judo Bank, April 2026), while 3-month rates reach 5.10% p.a. (BNK Bank). Cash ETFs like AAA (priced at $50.20 on 22 April 2026) target competitive yields with daily liquidity.

Excessive cash concentration, however, forfeits higher-yielding income opportunities. Balance is the point.

Quality equities complete the framework. Quality-factor ETFs, those selecting for high return on equity, low financial leverage, and earnings stability, have historically demonstrated lower volatility in stress environments. In a stagflationary period, this makes them a more appropriate equity allocation than broad market index exposure.

Fixed income forms the second tier. Floating-rate bonds reduce duration risk while generating income above cash rates. Short-duration government and investment-grade corporate bonds reduce capital loss exposure relative to long-dated alternatives. In a rising-rate environment, shorter duration is the lever that matters.

| Tier | Role in Portfolio | Risk Profile | Representative ASX Options |

|---|---|---|---|

| Cash | Capital preservation, liquidity, buying capacity | Very low | AAA, BILL, term deposits |

| Quality Equities | Long-run real growth, lower volatility | Moderate | VGS, AQLT, QLTY |

| Fixed Income | Income generation, duration management | Low to moderate | QPON, VBND, VAF |

Eight ASX ETFs for navigating the current environment

| ASX Code | ETF Name | Tier | Key Characteristic | Role in Defensive Portfolio |

|---|---|---|---|---|

| AAA | BetaShares Australian High Interest Cash ETF | Cash | AUD bank deposit accounts | Capital security with income |

| BILL | iShares Core Cash ETF | Cash | Short-term money market instruments | High liquidity, capital preservation |

| QPON | BetaShares Australian Bank Senior Floating Rate Bond ETF | Fixed Income | Senior floating rate bonds from major banks | Monthly income above cash rates |

| VBND | Vanguard Global Aggregate Bond Index Hedged ETF | Fixed Income | Global government and corporate bonds, AUD hedged | Diversified income with currency protection |

| VAF | Vanguard Australian Fixed Interest Index ETF | Fixed Income | Australian government and corporate bonds | Domestic fixed income access |

| VGS | Vanguard MSCI Index International Shares ETF | Equity | 1,000+ developed market large caps | Broad international equity exposure |

| AQLT | BetaShares Australian Quality ETF | Equity | 40 Australian quality-screened companies | Domestic quality equity exposure |

| QLTY | BetaShares Global Quality Leaders ETF | Equity | 150 global companies ranked on ROE and cash flow | International quality equity exposure |

Cash and cash-equivalent ETFs (AAA, BILL)

Both AAA and BILL serve the same tier but differ in mechanics. AAA targets income through AUD bank deposit accounts and was priced at $50.20 on 22 April 2026, consistent with its capital-stable design. BILL holds short-term money market instruments and bank deposits, prioritising maximum liquidity. For investors choosing between them, the distinction is yield profile versus immediate access; both preserve capital.

Fixed income ETFs (QPON, VBND, VAF)

Duration is the differentiator here. QPON holds senior floating-rate bonds from major Australian banks, meaning its coupon resets with rate movements, reducing the price sensitivity that punishes longer-duration holdings. VAF provides broad Australian government and corporate bond exposure across a range of maturities. VBND offers diversified global bond exposure with AUD currency hedging, a feature specifically relevant for Australian investors given current AUD weakness, as it eliminates the currency risk on international bond holdings.

Quality equity ETFs (VGS, AQLT, QLTY)

In a stagflationary environment, the relevant equity lens is quality-factor selection rather than broad market index exposure. AQLT screens 40 Australian companies on return on equity, low financial leverage, and earnings stability. QLTY applies the same logic globally across 150 non-Australian companies ranked on return on equity and cash flow generation. VGS provides broader developed-market exposure across more than 1,000 large-cap companies for investors who prefer wider diversification.

ETF prices and yields change daily. The data referenced reflects April 2026 conditions, and readers should verify current pricing before acting.

What bonds are actually doing right now, and why income still matters

Bond investors opening their statements this month are seeing red. Capital losses on fixed income holdings have been material, and the instinct to sell is understandable. But the price movement tells only half the story.

The mechanics are sequential:

- Rate expectations rise. The RBA has lifted the cash rate to 4.10%, and markets are pricing a 74% probability of a further increase to 4.35% at the May 2026 meeting (based on ASX 30 Day Interbank Cash Rate Futures as of 24 April 2026).

- New bond yields increase. Newly issued bonds offer higher coupons to reflect the changed rate environment.

- Older bond prices fall. Existing bonds with lower coupons become less attractive by comparison, so their market price drops to compensate buyers for the lower income stream.

The RBA March 2026 monetary policy decision raised the cash rate target to 4.10%, with the Board citing persistent domestic inflation and the pass-through effects of global energy prices as the primary factors driving the tightening stance.

Australian long bond rates have reached 5.1%, the highest level in over a decade.

Short-duration bonds are less exposed to this dynamic because their remaining life is shorter, meaning less time for rate changes to compound against them. Long-dated bonds carry more risk because markets are also anticipating higher government borrowing needs if the conflict proves prolonged.

Why the income component changes the calculation

The coupon payments on bonds continue flowing regardless of what happens to the price before maturity. For an investor holding a bond ETF through a volatile period, the income component acts as a performance anchor, offsetting a portion of the capital loss and contributing to total return even when the price on screen is falling.

This distinction between price return and total return is where most retail investors lose the thread. Major institutional investors have reportedly adopted a more constructive view on bonds as yields rise, precisely because the income component is now objectively better than at any point in the past decade. The 10-year Australian government bond yield stood at approximately 4.31% as of 16 April 2026.

Elevated yields represent compensation for holding duration risk. For income-focused investors with appropriate time horizons, the current environment may represent a more attractive entry point than any seen in recent years. Bonds are complex right now, not broken.

For investors wanting to model the bond recovery scenario in more depth, our full explainer on the RBA rate hike cycle examines oil futures backwardation as a signal that the inflationary impulse may be time-limited, applies the Taylor Rule to current RBA settings, and reviews historical supply shock cycles to estimate when the pivot from hikes to cuts has typically arrived.

How systematic investing converts market volatility into a structural advantage

Dollar-cost averaging (DCA) is the practice of investing a fixed dollar amount at regular intervals regardless of market conditions. The mechanical result is straightforward: more units are purchased when prices are low, fewer when prices are high, and the average cost per unit tends to fall below the average market price over time.

The current environment is specifically well-suited to this approach for investors with sufficient risk appetite and long enough time horizons. Elevated volatility creates meaningful price variation between each investment interval. The historical pattern of markets recovering once conflict de-escalation becomes visible suggests the current downturn is unlikely to be permanent.

Markets have tended to recover quickly from geopolitical conflicts once a resolution path becomes visible, even without full settlement.

There is also a plausible upside scenario. The current crisis is more narrowly focused on energy than 2022 (which compounded energy shocks with pandemic supply chain disruptions). Rates are already restrictive. Rate-sensitive assets, including bonds, could rebound sharply once conflict resolution looks plausible. Markets may be overestimating how far rates need to rise.

The four-step DCA process:

- Set the investment amount (a fixed dollar figure appropriate for the investor’s budget).

- Set the frequency (weekly, fortnightly, or monthly).

- Select the instrument or instruments from the defensive framework.

- Automate the transfer to remove the temptation of timing.

With the ANZ-Roy Morgan index showing a partial rebound of approximately 3.5 points to 62.3 in early April, some stabilisation is emerging at depressed levels. Volatile conditions are also the right moment to check whether current allocations genuinely reflect investment objectives, risk tolerance, time horizon, and near-term liquidity needs, rather than making reactive changes driven by sentiment.

For investors ready to implement a DCA programme rather than just understand the concept, our dedicated guide to dollar-cost averaging covers the specific automation features available on Australian platforms including Interactive Brokers and Betashares Direct, the record-keeping requirements for Capital Gains Tax compliance, and the behavioural mechanisms that make automation more effective than manual periodic investing.

When the playbook breaks, the discipline holds

The Iran War has disrupted the conventional safe haven hierarchy. Bonds have not protected. Gold has not rallied. The yen has not strengthened. But the underlying principles of defensive portfolio construction, liquidity, income, diversification, and discipline, remain intact and actionable for Australian retail investors.

The three-tier framework provides a structure that functions across multiple scenarios: cash for liquidity and capital preservation, fixed income for income generation and a rising-yield entry point, and quality equities for long-run participation with lower volatility characteristics.

Tactical inflation allocation frameworks that incorporate Treasury Inflation-Protected Securities, REITs with strong rent escalation clauses, and a systematic 10-15% cash buffer extend the defensive toolkit beyond the ASX-listed instruments covered here, particularly for investors managing cross-border portfolios or seeking sector-level pricing power plays.

Genuine uncertainty remains. The Strait of Hormuz is still closed. Ceasefire talks are stalled. The RBA may hike again in May. Investors do not need certainty to act; they need a framework robust enough to function regardless of which scenario unfolds.

The most productive next step is to review current allocations against the three-tier model, identify the largest gap, and address it with one deliberate step rather than a wholesale portfolio overhaul.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. Investors should conduct their own research and consult with a licensed financial adviser before making investment decisions.