Brent Hits $110 as Hormuz Closure Fuels 10% Inflation Risk

1 hr ago

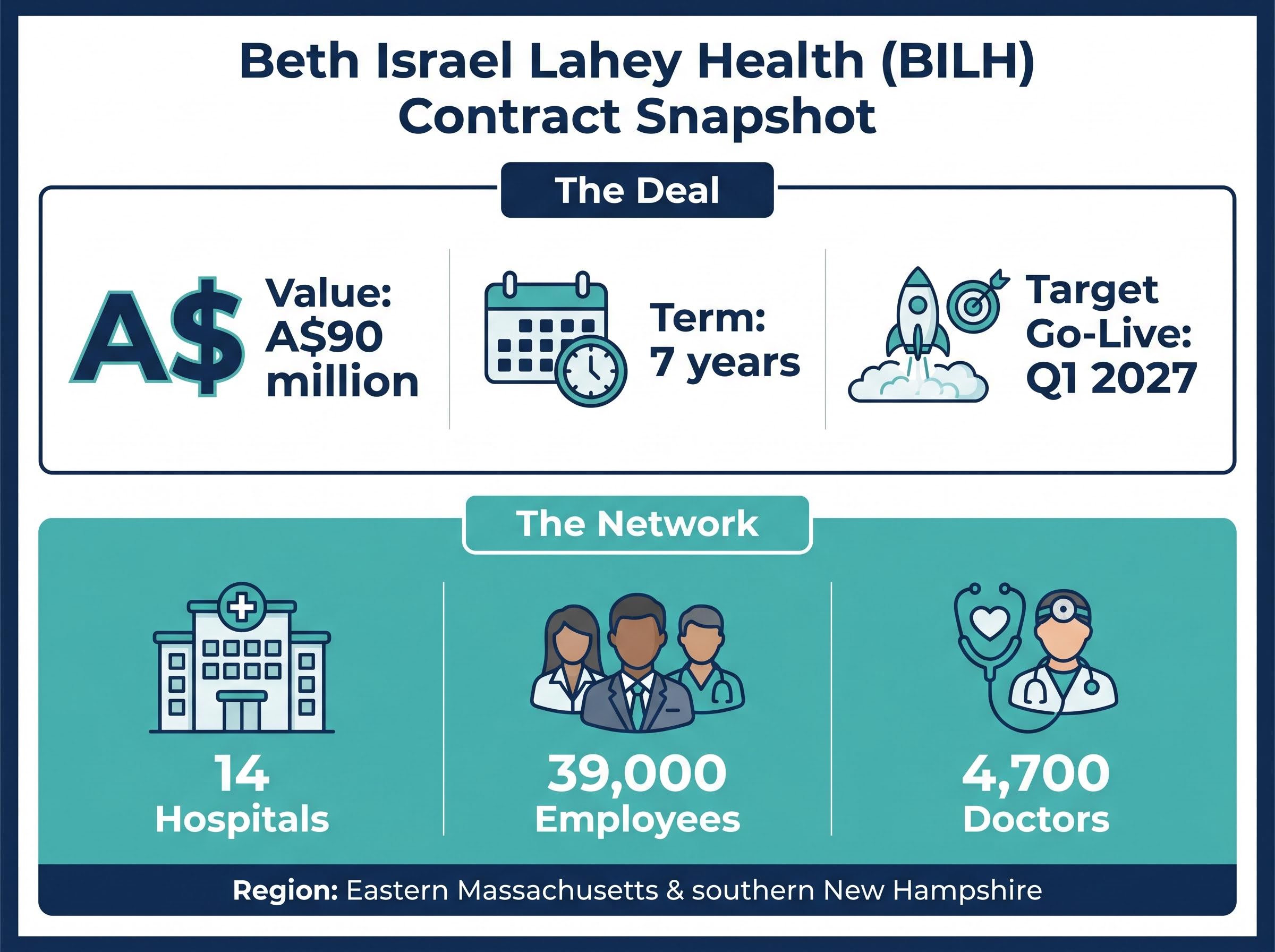

Pro Medicus has added another A$90 million US hospital contract to its books, this time with one of Boston’s largest and most complex integrated health systems. The deal with Beth Israel Lahey Health (BILH), announced to the ASX on 18 May 2026, is a seven-year agreement covering a full deployment of the Visage 7 Enterprise Imaging Platform across a 14-hospital network with roughly 39,000 staff.

For investors tracking Pro Medicus’s North American contract pipeline, the announcement reinforces a pattern of large, multi-year wins that has defined the company’s growth narrative through 2026. What follows breaks down exactly what was agreed, who the client is, when the revenue begins flowing, and what the deal signals for those assessing the PME share price trajectory and long-term contract momentum.

The commercial terms are straightforward: A$90 million over seven years, covering a full-suite deployment of the Visage 7 Enterprise Imaging Platform across BILH’s entire hospital network. Deployment planning commenced immediately following the ASX announcement on 18 May 2026, with the go-live targeted for Q1 calendar year 2027.

What distinguishes this deal from a narrower module purchase is the breadth of the deployment. BILH has contracted for all three core Visage 7 products:

Together, the three modules replace what would typically be a fragmented patchwork of legacy systems with a single, consolidated diagnostic imaging environment. The cloud-based implementation model means BILH avoids a large upfront infrastructure build, instead accessing the platform as a hosted service.

CEO Commentary CEO Dr Sam Hupert characterised the deal as further evidence that cloud-hosted platforms are becoming the benchmark in North American healthcare IT, with health systems increasingly seeking unified imaging environments over legacy alternatives.

BILH is a not-for-profit integrated health system spanning eastern Massachusetts and southern New Hampshire. The network’s scale makes it one of the larger and more complex imaging environments in the northeastern United States.

| Attribute | Detail |

|---|---|

| Hospitals | 14 |

| Employees | Approximately 39,000 |

| Physician network | Approximately 4,700 doctors |

| Geographic footprint | Eastern Massachusetts and southern New Hampshire |

| Institution types | Academic medical centres, teaching hospitals, community and specialty hospitals |

The organisational mix matters. Academic medical centres generate high imaging volumes with complex study types, while community hospitals require simpler but consistent access to the same platform. Deploying a single enterprise imaging solution across that range of clinical complexity is a meaningful operational challenge, and a successful rollout here strengthens Pro Medicus’s reference credentials for similarly large integrated delivery networks across the US.

The BILH deal is not an isolated event. It follows a pattern of large, multi-year contract wins that raises a more consequential question for investors: is this momentum cyclical or structurally driven?

Visage 7 is an enterprise imaging platform, meaning it replaces the multiple separate systems a hospital traditionally uses to view, manage, and store diagnostic images. The Viewer lets clinicians display and manipulate medical scans. Workflow manages how imaging studies move through the reading and reporting process across departments and sites. Open Archive stores all imaging data in a single cloud-based repository rather than in separate on-premise servers at each facility.

The critical differentiator from legacy systems is architecture. Older Picture Archiving and Communication Systems (PACS), the technology hospitals have used for decades to store and retrieve medical images, were typically installed on local servers at individual sites. Visage 7 is cloud-native, meaning it was designed from the ground up to run as a hosted service rather than being retrofitted for the cloud after the fact.

KLAS Research enterprise imaging findings consistently place cloud-native platforms ahead of legacy PACS alternatives on metrics including clinician satisfaction, cross-site accessibility, and total cost of ownership, providing independent market validation for the procurement shift that health systems like BILH are acting on.

Large US health systems are in the middle of a multi-year replacement cycle, moving from fragmented, modality-specific PACS toward consolidated enterprise imaging. Three primary drivers are accelerating adoption:

The enterprise imaging market that Pro Medicus is consolidating is projected to grow at a 12% compound annual rate to US$4.1 billion by 2030, a structural tailwind that has attracted competing platform launches from smaller ASX-listed players attempting to carve out positions in the same health system replacement cycle, though none yet operating at the contract scale or client complexity that characterises Pro Medicus’s recent wins.

Dr Hupert noted that BILH joins a growing roster of clients selecting the fully cloud-hosted platform and that the deal pipeline remains robust across all market segments.

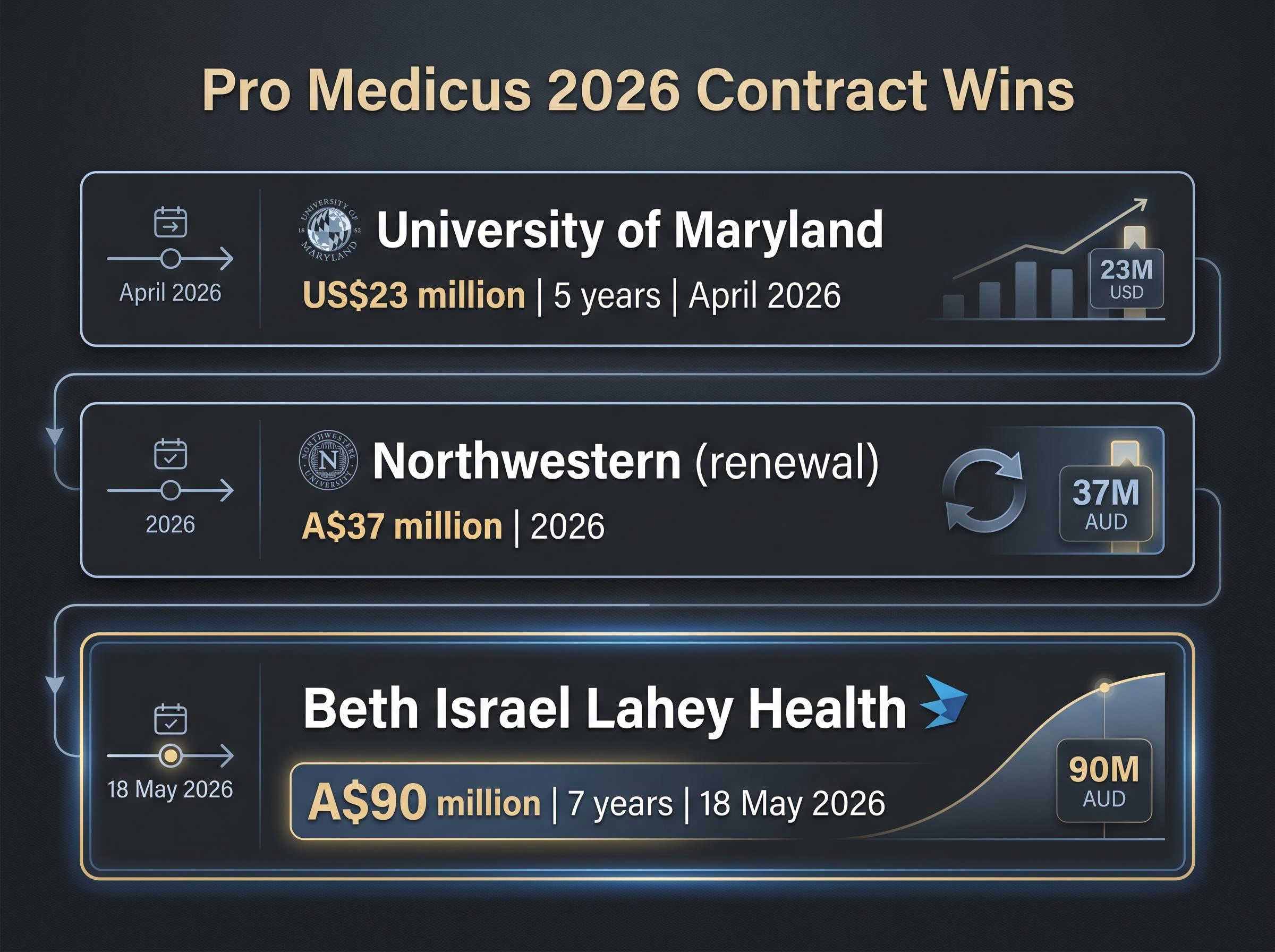

Three confirmed deals in recent months illustrate the cadence of wins that has defined Pro Medicus’s 2026.

| Client | Contract value | Term | Approximate announcement | Go-live timing |

|---|---|---|---|---|

| University of Maryland | US$23 million | 5 years | April 2026 | Not disclosed |

| Northwestern (renewal) | Approximately A$37 million | Not disclosed | 2026 | Not disclosed |

| Beth Israel Lahey Health | A$90 million | 7 years | 18 May 2026 | Q1 2027 |

The BILH contract is the largest of the three by a considerable margin. Taken together, the pattern of wins aligns with CEO commentary describing a robust pipeline across all market segments.

The University of Maryland contract, signed in April 2026, covers Visage 7 Viewer and Workflow across the entire academic health network including trauma, oncology, and paediatric facilities, with transaction-based pricing that creates potential revenue upside beyond the A$23 million baseline if imaging volumes exceed projections.

One detail investors should note: Pro Medicus’s contract revenue model means announced deals convert to revenue at go-live rather than at the point of signing. For the BILH contract, that means Q1 2027 is the relevant timing marker for when contract-related revenue begins materialising. The gap between announcement and revenue recognition is a recurring feature of the company’s financials, and readers assessing near-term earnings impact should calibrate accordingly.

The most recent verified closing price for PME on the ASX was A$122.11, recorded on 15 May 2026, with intraday trading in the A$121-123 range during mid-May. The BILH announcement landed on 18 May 2026; the immediate share price reaction was not quantified at the time of publication, and investors should monitor ASX price feeds in subsequent sessions for movement.

Pro Medicus’s price-to-earnings multiple remains elevated relative to broader ASX peers, a valuation that reflects the market pricing in continued contract momentum of exactly this kind. A deal of this size and duration is consistent with the growth thesis required to sustain that premium; it is not, however, a thesis-changing event in itself.

The healthcare IT valuation dynamics at play for Pro Medicus sit within a broader sector context worth understanding: ASX healthcare has delivered annualised returns of approximately -11% over five years despite intact structural demand, with the gap between price performance and business fundamentals driven primarily by interest rate compression rather than earnings deterioration, a distinction that matters when assessing whether current multiples are stretched or simply reflecting a high-growth software-style earnings profile.

According to recent financial commentary, Pro Medicus’s P/E multiple, while still elevated, has improved relative to prior levels as earnings growth has begun catching up with the share price. The source article’s author disclosed a personal ownership position in Pro Medicus shares at the time of publication.

Investors assessing whether each new win is already priced into the current valuation or represents incremental upside will need to weigh the BILH contract against the expectations already embedded in the share price. The deal confirms the trajectory. Whether it exceeds what the market anticipated is a question the next few trading sessions may begin to answer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The BILH deal confirms three things: demand for full-suite Visage 7 deployments continues at the large integrated health system tier, Pro Medicus can win and close contracts of this scale and complexity, and management’s characterisation of a robust pipeline has tangible evidence behind it.

What the deal does not resolve is whether the current valuation already accounts for this level of contract activity, or whether the pipeline commentary will translate into further announced wins in coming months.

For investors looking for forward-looking markers, three items warrant attention:

The A$90 million, seven-year deal with one of Boston’s most complex health systems is consistent with the growth trajectory investors have been pricing in. The next test is whether the pipeline delivers again.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Visage 7 is a cloud-native enterprise imaging platform that replaces fragmented legacy hospital imaging systems with a single, consolidated environment covering diagnostic viewing, workflow management, and cloud-based image archiving.

Revenue from the BILH contract is expected to begin in Q1 calendar year 2027, which is the targeted go-live date; Pro Medicus recognises contract revenue at go-live rather than at the point of signing.

Beth Israel Lahey Health operates 14 hospitals across eastern Massachusetts and southern New Hampshire, with approximately 39,000 staff and a physician network of around 4,700 doctors.

In addition to the A$90 million BILH contract, Pro Medicus announced a US$23 million deal with the University of Maryland in April 2026 and an approximately A$37 million renewal with Northwestern, also in 2026.

The most recent verified closing price for PME on the ASX prior to the announcement was A$122.11, recorded on 15 May 2026, with intraday trading in the A$121-123 range during mid-May.