The commercial closure of the Strait of Hormuz in late February 2026 has choked off 20% of global energy flows, rendering traditional cyclical recovery models ineffective. This severe logistical bottleneck requires a distinct approach to stagflation investing, as the physical absence of commodities overrides standard financial solutions. Unlike standard demand-driven recessions where consumers simply stop spending, this current crisis represents a physical supply-side shock.

The enduring energy constraint is forcing the Reserve Bank of Australia into difficult policy corners. Polymarket prediction indicators currently assign a 99.7% probability that commercial maritime traffic will not normalise by 30 April 2026. This analysis decodes how the extended bottleneck is reshaping asset allocation rules for Australian capital.

Investors must understand the precise mechanics of this disruption to manage the ongoing volatility. Objective analysis of these macroeconomic pressures reveals that standard recovery frameworks will remain stalled until the physical movement of global commodities resumes.

The Anatomy of a Supply Shock: Why Current Markets Mirror the 1970s

Global markets are currently pricing in a severe logistical constraint rather than declining consumer appetite. The prolonged maritime chokepoint has severed access to critical petroleum and gas availability. Energy markets are absorbing the shock of restricted vessel movement across the Middle East.

QatarEnergy escalated the upstream pressure by declaring force majeure on liquefied natural gas exports shortly after the closure began. The direct consequences of the extended chokepoint have cascaded into global manufacturing and transportation networks. Without reliable access to these critical fuel inputs, industrial output faces an artificial ceiling regardless of underlying economic demand.

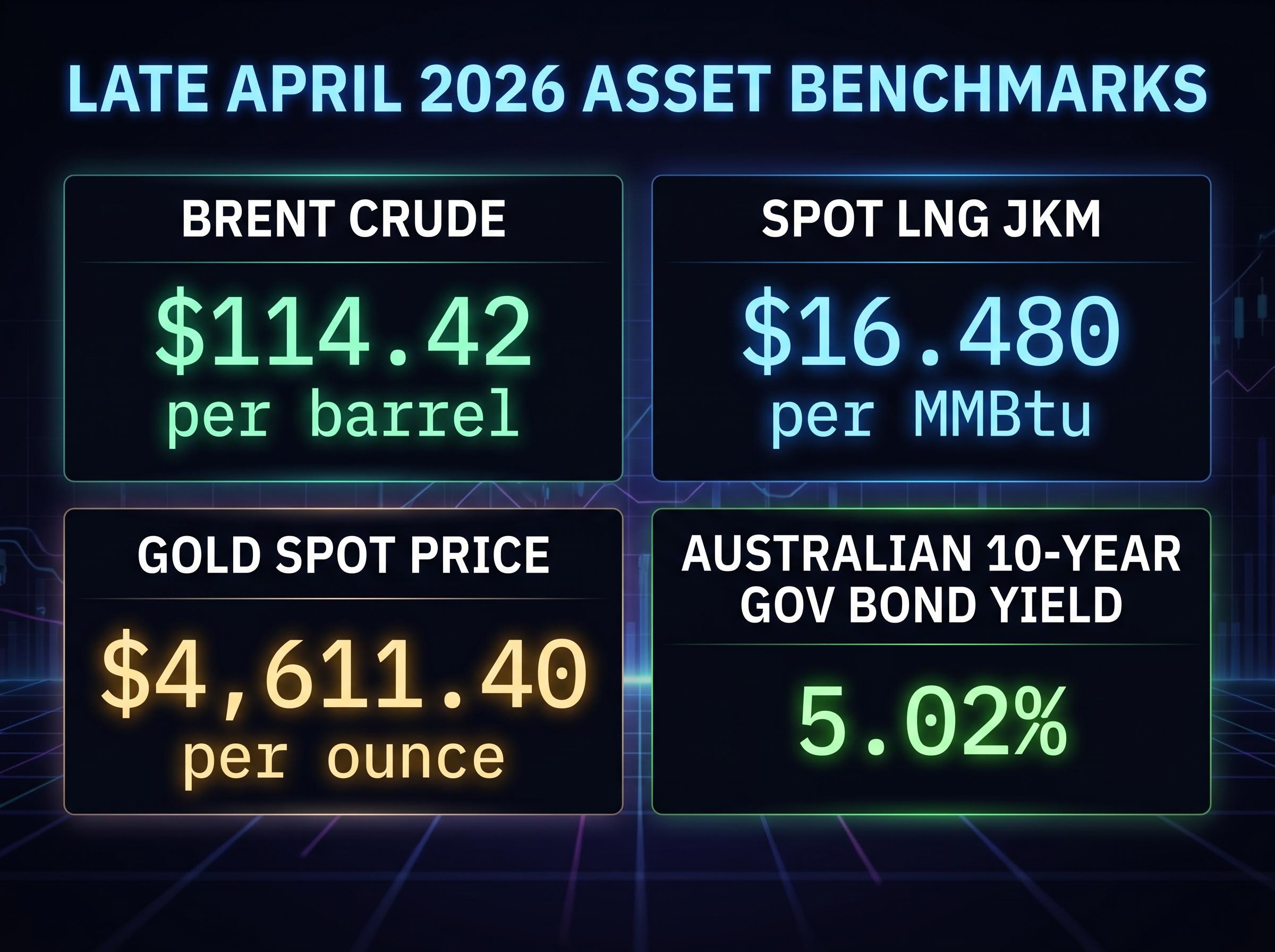

The pricing baselines established in late April 2026 reflect physical scarcity rather than financial imbalance. Brent Crude is trading at $114.42 per barrel, with recent spot highs fluctuating persistently between $109 and $114. Meanwhile, the global spot LNG JKM marker sits elevated at $16.480 per MMBtu. Traditional market recovery timelines do not apply until these physical shipping routes reopen.

The prevailing macro investing dynamics have shifted drastically as foreign exchange markets begin pricing currencies based almost entirely on a nation’s energy export capacity.

“The current logistical constraint mirrors the stagnant commercial expansion of the 1970s. Structural supply deficits have overridden standard economic cycles, rendering traditional monetary easing entirely ineffective in the short term.”

Investors must understand that because this crisis stems from missing physical commodities, financial engineering cannot provide an immediate solution.

When big ASX news breaks, our subscribers know first

Educational Breakdown: The Mechanics of the Stagflation Trap

A stagflation trap occurs when stagnant economic growth collides with severe, structural price increases. Energy shocks act as an immediate tax on consumption while simultaneously driving up industrial production costs across all sectors. For the past four decades, financial emergencies typically triggered central bank monetary easing as the standard solution.

That historical playbook fails completely when the economic crisis stems from missing physical commodities rather than a lack of liquidity. Readers new to complex macroeconomic theory must grasp exactly why their portfolios are experiencing simultaneous equity and fixed-income declines. Raising interest rates successfully curbs consumer demand, but it cannot produce more oil or clear geopolitical shipping lanes.

This creates a severe policy mismatch for institutions accustomed to managing purely financial crises.

Why Interest Rates Cannot Fix Supply Chains

Central banks face acute friction between containing second-round inflation and exacerbating domestic unemployment. When supply remains heavily constrained by external geopolitical forces, policymakers are forced to engineer demand destruction.

This severe but necessary macroeconomic outcome cools inflation by deliberately slowing economic activity until it matches the newly restricted supply baseline. Interest rates serve as a blunt instrument that crushes domestic spending to mask the inflationary impact of international logistical failures.

The March 2026 RBA monetary policy communications explicitly address this policy limitation, noting that while higher domestic borrowing costs successfully curb broad consumer demand, they cannot resolve the core inflationary pressures stemming from missing fuel imports.

The Australian Passthrough: Managing Domestic Fallout

The abstract global energy crisis has translated directly into immediate financial vulnerability for Australian consumers and industrial operations. Supply chain disruptions have hit construction materials heavily, exemplified by a 36% spike in PVC pipe prices alongside new transport surcharges at major supermarkets. The Reserve Bank of Australia has shifted from a cautious holding pattern to aggressive tightening to curb this entrenched inflation.

The RBA cash rate currently stands at 4.10% following the March 2026 hike. Forecasts now point toward a 5.00% terminal rate as policymakers explicitly target second-round price pressures. These local borrowing cost increases parallel a broader economic cooling.

GDP growth is forecasted to slow from 2.5% in the first half of 2026 to 2.0% or less in the second half. Annual inflation is surging to approximately 4.6%, with the trimmed mean forecast at 4.2% by the first quarter of 2027.

Despite these near-term economic drags, underlying structural deflationary counterweights like AI integration and global supply chain rebalancing are slowly building to offset these commodity spikes in the long run.

| Metric | Current Status April 2026 | Near-Term Forecast | Economic Impact |

|---|---|---|---|

| RBA Cash Rate | **4.10%** | **5.00%** | Elevated borrowing costs |

| Headline Inflation | **4.6%** | **4.2%** (Trimmed Q1 2027) | Reduced purchasing power |

| GDP Growth | **2.5%** (H1 2026) | **2.0%** (H2 2026) | Slowing domestic activity |

| Industrial Materials | PVC prices up **36%** | Sustained elevation | Construction margin pressure |

By linking global oil prices to these local RBA rate hikes, investors can accurately project their living expenses and borrowing costs through the remainder of 2026.

Asset Distortions: Why Traditional Safe Havens Are Fracturing

Prolonged high yields and shifting global trade dynamics have fundamentally rewired asset performance across international markets. The sustained elevation in oil prices creates a stark divergence between terms-of-trade winners and net-energy importers. This environment dismantles outdated portfolio protection myths, showing exactly why the standard crisis playbook is failing.

Precious metals are demonstrating highly counterintuitive performance profiles. According to market data, the global gold spot price sits at $4,611.40 per ounce, stalling against high bond yields after an 80% valuation surge over the preceding 24 months. High bond yields make non-yielding assets fundamentally less desirable despite their historical safe-haven status.

The Australian 10-Year Government Bond Yield has reached 5.02%, reflecting this hawkish global tightening environment. Currency valuations further highlight the fracturing of standard crisis playbooks. The performance characteristics of major currencies currently depend directly on their domestic energy self-sufficiency:

- The United States dollar maintains aggressive dominance due to domestic energy production and high comparative yields.

- The Australian dollar shows resilience, trading at $0.7188 against the USD, supported by broader commodity exports despite heavy fuel import reliance.

- The Japanese yen demonstrates extreme vulnerability, collapsing its former crisis reputation due to a near-total reliance on imported energy.

Capital flows are actively punishing nations that must import expensive hydrocarbons while carrying high debt loads. Investors holding yen or unhedged gold positions are learning that historical correlations break down when a geopolitical event directly targets physical energy logistics.

Investors exploring alternative defensive positions will find our detailed coverage of safe haven asset redefinition useful, as it outlines how active duration management and quality-focused ETFs can substitute for failing traditional bonds.

Capital Allocation: Frameworks for Stagflation Investing

Macroeconomic diagnosis must translate directly into concrete defensive posturing strategies for capital preservation. The current yield-heavy and low-growth environment requires strict discipline to manage simultaneous asset class drawdowns. According to Selfwealth data principles, retaining liquid capital allows investors to weather market volatility and capture discounted securities when disruptions eventually clear.

Independent Morningstar stagflation asset performance research reveals that conventional portfolio splits suffer heavy dual drawdowns when energy prices spike alongside aggressive central bank tightening.

Fixed-income coupon payments are providing a stabilising role for portfolios despite underlying price drops on the secondary market. According to market data, benchmark ten-year United States government debt currently generates returns exceeding 4.00%, offering substantial yield for cautious capital.

Investors managing personal portfolios or self-managed super funds should implement these four distinct pillars of strategic portfolio management during a supply-shock crisis:

Maintain elevated cash buffers to exploit tactical mispricing in equity markets as volatility spikes. Target terms-of-trade beneficiaries, specifically hydrocarbon exporters with unhedged energy exposure. Secure short-duration fixed income to capture rising yields without taking on long-term duration risk. Underweight energy-dependent industrial sectors facing severe margin compression from unavoidable logistical surcharges.

These frameworks are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Implementing these defensive postures prevents forced selling during the deepest phases of the market drawdown.

Approaching the Terminal Plateau

The duration of the Hormuz closure remains the absolute critical variable dictating all forward-looking asset allocation decisions. Analysts warn that an extended closure scenario lasting another 3 to 6 months will act as the primary catalyst for severe, irreversible demand destruction globally. Global central banks are grappling to find a terminal rate plateau that controls inflation without causing a severe policy overshoot.

The RBA faces a particularly delicate balancing act between cooling the domestic economy and triggering unnecessary corporate defaults in the construction and retail sectors. Once geopolitical resolutions become visible, equity markets historically front-run the physical recovery of shipping lanes. Until that clarity arrives, defensive capital deployment and strict adherence to valuation principles remain the most prudent path forward for Australian investors.

Deploying systematic equity investing strategies through dollar cost averaging during this volatile window allows patient capital to capture deeply discounted international opportunities before the broader market rebounds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.