Energy Funds Post Record Outflows as Global Equities Bleed Capital

1 hr ago

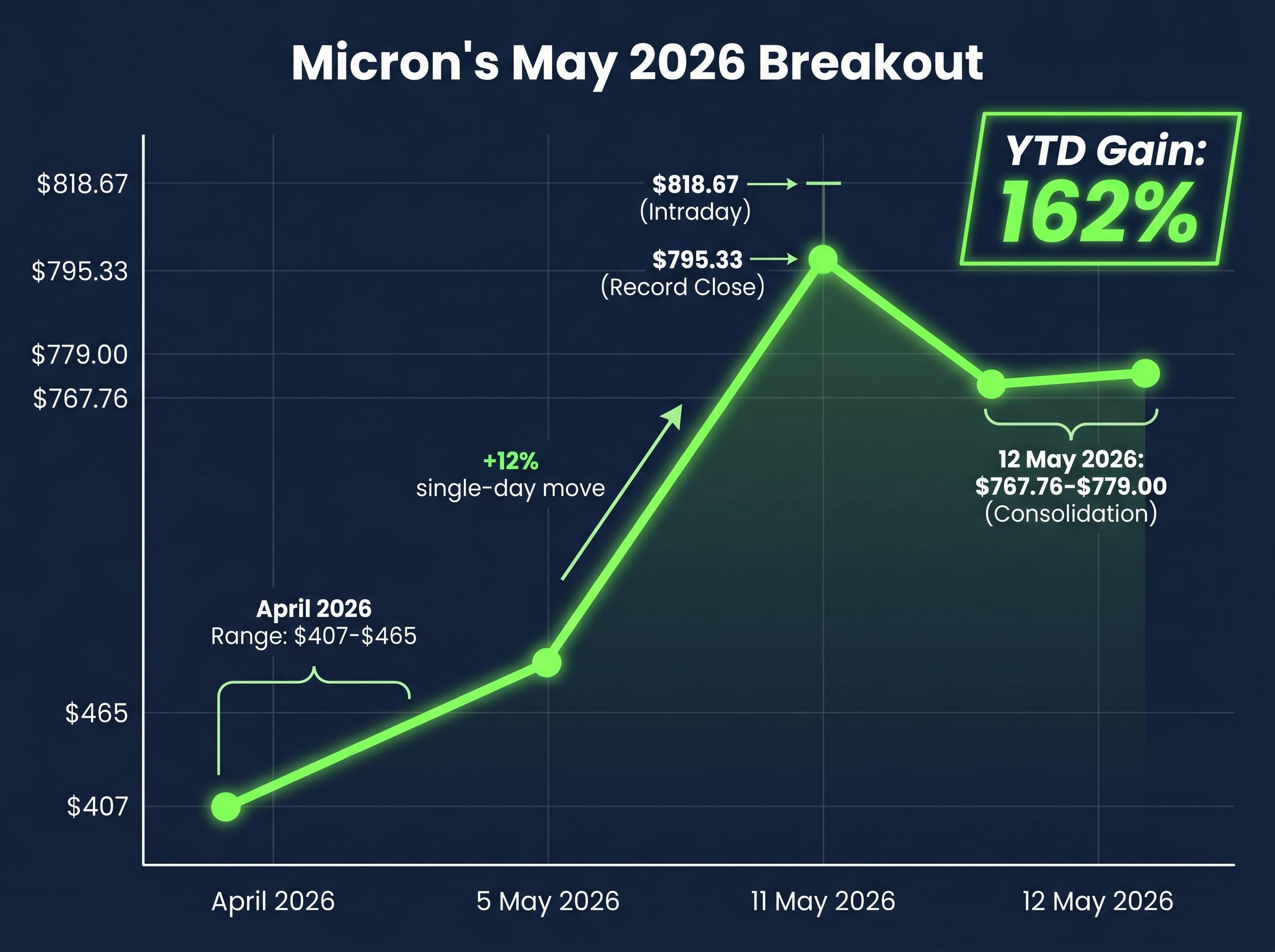

Micron Technology surged more than 20% over two consecutive trading sessions this week, reaching an all-time closing high of $795.33 on 11 May 2026, as a single geopolitical development reshuffled investor calculus across the entire memory chip sector. The catalyst was not an earnings beat, a product announcement, or an analyst upgrade. It was a guest list: specifically, who was and was not included in President Trump’s trade delegation to China during the week of 12 May 2026.

The Micron stock rally has added approximately 162% to the company’s share price year to date, turning a mid-cap semiconductor name into one of the most talked-about large-cap momentum trades of 2026. What follows breaks down the precise mechanism by which a diplomatic roster became a market catalyst, explains why analyst KC Rajkumar of Lynx Equity Strategies argues the most important signal was an absence rather than a presence, and maps the secondary forces amplifying the move for Micron and its memory sector peers.

The numbers are worth stating plainly before any interpretation.

Micron’s all-time closing high: $795.33 (11 May 2026). Intraday high: $818.67. YTD gain: approximately 162% as of 12 May 2026.

On 12 May, shares traded in a range of $767.76-$779.00, consolidating after the prior session’s record close. The two-day surge exceeded 20% across consecutive sessions, a move that is rare in any large-cap name and extraordinary for a company already deep into a multi-month run.

Key price milestones tell the story of acceleration:

In April 2026, Micron traded in a range of roughly $407-$465. A 12% single-day move on 5 May, accompanied by unusual options activity, signalled that something was building beneath the surface. Within a week, that signal became a re-rating.

President Trump’s trade delegation to China during the week of 12 May 2026 included more than 16 CEOs from technology, finance, and commercial sectors. The White House framed the trip around agricultural and commercial aviation topics rather than semiconductor technology. The roster, however, told a different story.

Confirmed attendees included:

Notable absence: Jensen Huang, CEO of Nvidia, was not included.

The roster appears to have begun circulating among market participants toward the end of the prior week before becoming widely known on the Monday of the surge. That timing gap may explain the unusual options activity observed on 5 May.

Mehrotra’s presence elevated expectations of improved Chinese market access or reduced tariff and export control pressure for Micron specifically. His seat on the plane linked Micron’s business interests directly to the trade talks, raising the company’s profile in the geopolitical narrative at a moment when memory demand was already accelerating.

No official White House or Micron investor relations statements confirmed specific policy outcomes as of 12 May 2026. The move was driven by expectation, not confirmed delivery.

The obvious reading of the delegation was straightforward: Mehrotra’s inclusion was bullish for Micron. KC Rajkumar, an analyst at Lynx Equity Strategies, offered a sharper interpretation.

The Rajkumar thesis: Micron may have benefited more from semiconductor capital equipment CEOs being excluded from the delegation than from Mehrotra’s own inclusion, according to analysis cited by Investing.com.

The logic runs through a specific chain:

The mechanism is the removal of a headwind, not the arrival of a direct positive catalyst. Equipment companies are the natural lobbyists for waiver access, since they are the direct suppliers who would benefit from resumed sales to Chinese chipmakers. Their exclusion from the delegation reduced the perceived likelihood that waiver discussions were on the agenda.

Rajkumar noted a caveat: whether Micron itself would receive favourable treatment regarding its own Chinese market access remained unresolved as of 12 May. In April 2026, U.S. legislation was advanced to restrict chip tool sales to YMTC and CXMT, and Micron was reported to be actively lobbying Congress to advance those restrictions.

YMTC and CXMT are Micron’s primary Chinese competitors in NAND flash and DRAM memory, respectively. Import waivers would allow these companies to acquire the advanced semiconductor manufacturing equipment currently restricted under U.S. export control rules, equipment they need to close the technology gap with Western chipmakers.

| Company | Product focus | U.S. regulatory status (May 2026) |

|---|---|---|

| YMTC (Yangtze Memory Technologies) | NAND flash memory | Subject to proposed federal procurement ban; chip tool sales restricted |

| CXMT (ChangXin Memory Technologies) | DRAM memory | Subject to proposed federal procurement ban; chip tool sales restricted |

| Micron Technology | NAND and DRAM | Active lobbyist for maintaining restrictions on rivals |

Micron’s lobbying posture is a business strategy, not merely a regulatory abstraction. With AI infrastructure buildout driving DRAM and NAND demand globally, shifts in the competitive structure of the memory market carry direct implications for revenue and margin trajectories.

HBM revenue growth of approximately 300% year-over-year has made high-bandwidth memory the most acutely constrained component in AI chip stacks, concentrating demand in Micron’s product lines at precisely the moment that geopolitical restrictions are limiting its primary competitors’ ability to expand capacity.

A waiver would allow Chinese chipmakers to import advanced semiconductor manufacturing equipment currently blocked under U.S. export controls. Without that equipment, YMTC and CXMT remain at a technology disadvantage relative to Micron, Samsung, and SK Hynix. In April 2026, U.S. proposed rules advanced to prohibit federal acquisition of certain semiconductors from YMTC and CXMT, directly protecting Micron’s government and enterprise customer base.

The proposed U.S. export control legislation targeting YMTC and CXMT advanced in April 2026 sought to apply Entity List-style restrictions covering not only equipment sales but also servicing and technical support, a scope that would substantially deepen the technology disadvantage facing Chinese memory chipmakers relative to Western competitors.

Micron did not rally alone. The delegation catalyst produced read-through effects across the memory and semiconductor sectors over the same two-day window.

| Ticker / Index | Two-day gain |

|---|---|

| MU (Micron Technology) | +20% |

| INTC (Intel) | +18% |

| SNDK (Sandisk) | +15% |

| AMD (Advanced Micro Devices) | +12% |

| SOX (Philadelphia Semiconductor Index) | +8% |

Over a broader 30-day window, Sandisk gained 82% and SK Hynix added 78%, suggesting the delegation catalyst accelerated a momentum trend already underway. Seagate’s upbeat storage outlook on 29 April 2026 and a D.A. Davidson Buy initiation in late April had already primed the sector’s demand narrative.

The memory sector repricing evident in SanDisk’s 78.4% non-GAAP gross margin and 252% revenue growth in Q3 2026 points to a structural shift that predates the delegation catalyst: AI data centres are absorbing approximately 70% of high-end NAND production under multi-year hyperscaler contracts, reducing the spot-market volatility that has historically capped memory valuations.

Samsung supply risk: A potential 18-day strike starting 21 May 2026 could cost an estimated $20 billion-plus if mediation fails.

Samsung’s union entered mediation on 11-12 May over an ongoing wage dispute. A prolonged Samsung production disruption would tighten global DRAM and NAND supply, benefiting Micron as a primary alternative supplier. Rajkumar assessed that even a successful resolution of Samsung’s labour negotiations would likely be insufficient to fully reverse the memory pricing gains already realised, limiting the downside from a positive Samsung outcome.

The delegation catalyst raised questions it did not answer. Three variables remain open:

At approximately $779 on 12 May, Micron has already surpassed most analyst consensus targets. The 42-analyst consensus carries a Strong Buy rating with an average price target of approximately $482-$521, well below the current price.

Legacy targets from TD Cowen ($660) and UBS ($535) have been blown through. The $1,000 high target now represents the bull case that is actively in focus. The stock is trading on forward estimate revision expectations rather than current consensus, a structural tension that places disproportionate weight on the Q3 earnings report to validate the re-rating.

Micron’s forward earnings multiple sits at approximately 7.58x-8.9x despite a 162% year-to-date run, a figure that places it well below historical memory-sector valuation peaks and explains why some analysts treat the current price as a re-rating rather than a bubble, even as the stock trades far above consensus price targets.

The week of 12 May 2026 delivered a two-tier catalyst for Micron. Mehrotra’s inclusion in the China delegation raised market access hopes, but the deeper analytical signal, as Rajkumar identified, was the exclusion of capital equipment CEOs that reduced Chinese rival waiver probability.

What remains unresolved is substantial: no confirmed policy outcomes, a Samsung strike deadline nine days away, and an earnings report six weeks out. Geopolitical sequencing has become as important to Micron’s investment thesis as product cycles or quarterly results, and the delegation roster proved it.

For investors tracking how quickly geopolitical signals can reverse semiconductor gains, our full explainer on the AI tax rumour selloff documents the intraday event on 12 May 2026 in which a single social media post erased more than $300 billion in market value from Samsung, SK Hynix, Micron, and AMD before coordinated government denials partially unwound the move within the same session.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

Micron surged over 20% across two consecutive trading sessions after President Trump's trade delegation to China was revealed to include Micron CEO Sanjay Mehrotra, raising expectations of improved Chinese market access, while the exclusion of semiconductor capital equipment CEOs reduced the perceived probability that Chinese memory rivals YMTC and CXMT would receive import waivers.

An import waiver would allow Chinese chipmakers like YMTC and CXMT to purchase advanced semiconductor manufacturing equipment currently blocked under U.S. export controls; without these waivers, Micron's Chinese rivals remain at a significant technology disadvantage, preserving Micron's competitive position in DRAM and NAND flash memory markets.

As of 12 May 2026, Micron was trading at approximately $779, well above the 42-analyst consensus average price target of roughly $482-$521, with legacy targets from TD Cowen at $660 and UBS at $535 already surpassed, leaving the $1,000 high target as the active bull case.

Micron gained approximately 162% year to date as of 12 May 2026, reaching an all-time closing high of $795.33 and an intraday high of $818.67, making it one of the most significant large-cap momentum trades of the year.

Micron's fiscal Q3 2026 earnings are expected around 24 June 2026, and the report is seen as the next critical data point to determine whether the geopolitical re-rating in the stock is supported by actual demand and margin performance, since the current rally is driven by expectation rather than confirmed results.