SanDisk just posted 252% year-over-year revenue growth and a 78.4% non-GAAP gross margin in Q3 2026, numbers that look less like a cyclical bounce and more like a structural repricing event in the semiconductor storage industry. The memory sector has historically been punished by investors for its boom-bust cyclicality. What is now being debated on Wall Street, with real money at stake, is whether AI-driven demand has permanently altered that dynamic, or whether the current rally is a sophisticated version of the same inventory-normalisation cycle the sector has repeated for decades. This analysis provides a framework for distinguishing structural from cyclical signals in the memory sector, evaluating the product catalysts that could extend SanDisk’s current pricing power, and understanding the valuation logic that could double or triple sector multiples if the bull case holds.

The numbers behind SanDisk’s Q3 2026 that demand a structural explanation

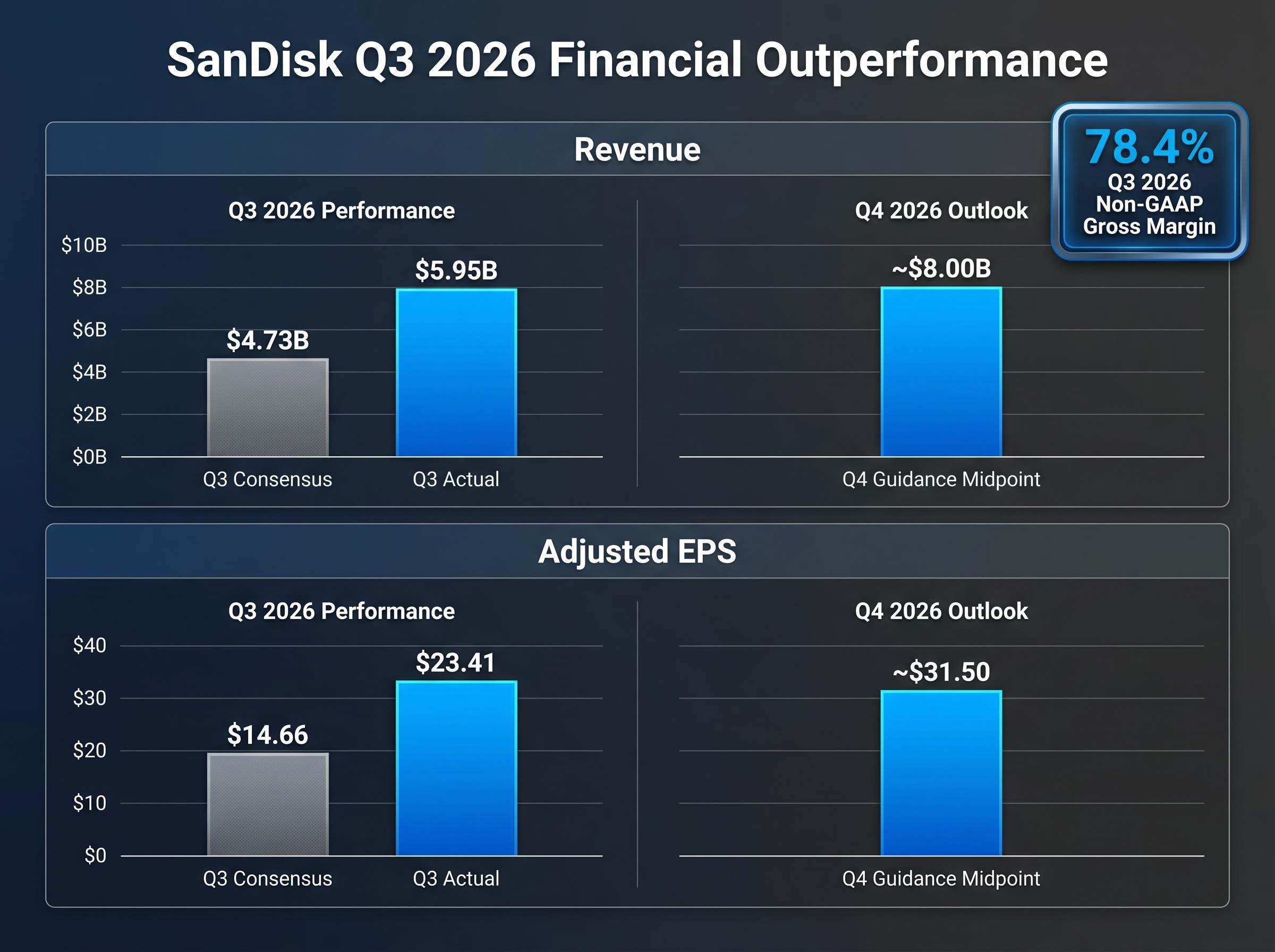

SanDisk reported Q3 2026 revenue of $5.95 billion, up 252% year over year and 97% sequentially. Non-GAAP gross margin reached 78.4%. Both figures landed well above Wall Street consensus: analysts had expected $4.73 billion in revenue and adjusted earnings per share (EPS) of $14.66; SanDisk delivered $23.41.

These are not numbers that a typical inventory restocking cycle produces. A demand recovery can drive volume and revenue growth, but it does not simultaneously deliver gross margins near 80% unless the seller has pricing power that the buyer cannot easily arbitrage away.

Management’s Q4 guidance reinforced the signal. SanDisk projected $7.75 to $8.25 billion in revenue with non-GAAP diluted EPS of $30.00 to $33.00, implying the current pricing environment is not a one-quarter anomaly. CEO David Goeckeler characterised the quarter explicitly as a shift in the company’s trajectory.

CEO Commentary David Goeckeler described Q3 2026 as a “fundamental turning point” toward higher-value end markets, framing the results as a structural repositioning rather than a cyclical peak.

Shares rose 4.89% in after-hours trading to $1,116.25. Wedbush raised its price target to $1,200 with an Outperform rating.

| Metric | Q3 Actual | Consensus Estimate | Q4 Guidance (Midpoint) |

|---|---|---|---|

| Revenue | $5.95B | $4.73B | ~$8.00B |

| Adjusted EPS | $23.41 | $14.66 | ~$31.50 |

| Non-GAAP Gross Margin | 78.4% | N/A | N/A |

When big ASX news breaks, our subscribers know first

What is actually driving NAND supply constraints, and why it matters for pricing

AI data centres are absorbing approximately 70% of high-end NAND production. That single statistic reframes the supply picture: the constraint is not a temporary bottleneck waiting for factories to catch up. It is a structural diversion of production toward a buyer cohort whose appetite is growing faster than the industry can add capacity.

IDC NAND market forecasts published in early 2026 identify hyperscaler procurement as the dominant driver of enterprise SSD price appreciation, with AI infrastructure build-outs absorbing supply at a pace that capacity expansion schedules cannot match in the near term.

Three distinct forces are compressing available supply:

- AI capex absorption: Hyperscaler data centre build-outs require enterprise-grade NAND at volumes that consume the majority of high-end output, leaving consumer and legacy enterprise channels competing for the remainder.

- Inventory correction amplification: Post-2024 inventory drawdowns temporarily sharpened the apparent tightness, creating a cyclical overlay on top of the structural demand pull.

- Hyperscaler contract behaviour: Major cloud operators are locking in multi-year supply agreements rather than purchasing on spot markets, a behavioural signal that these buyers expect supply to remain constrained relative to their forward needs.

Analysts forecast NAND and DRAM prices to rise 20-30% year over year through mid-2026, driven by this persistent imbalance between capacity expansion timelines and accelerating demand.

The data storage supply constraints now visible across the sector extend well beyond NAND into hard disk drives, with enterprise hardware prices for high-capacity models rising up to 60% and major suppliers reporting sold-out production capacity through the end of 2026.

Where the cyclical and structural signals diverge

Inventory normalisation alone cannot account for 78.4% gross margins at the volumes SanDisk is shipping. A cyclical recovery lifts volume; it does not hand the seller the pricing power to extract near-80% margins simultaneously. The dominance of multi-year contracts over spot purchases in the current environment further separates this cycle from prior inventory-driven rebounds, where spot pricing normalised quickly once restocking was complete.

Understanding NAND and the memory sector’s shift from commodity to infrastructure

NAND flash memory stores data without requiring power to retain it, making it the foundation of solid-state drives (SSDs) used in everything from laptops to data centres. SanDisk’s BiCS8 node represents the latest generation of vertically stacked NAND cells, where greater density and endurance specifications determine whether a drive qualifies for enterprise workloads that run continuously under heavy read/write loads.

For decades, the memory sector operated as a commodity cycle. Producers manufactured a largely undifferentiated product, competed primarily on price, and watched margins swing violently as supply and demand fell in and out of balance. The investment community priced the sector accordingly, applying low multiples that reflected the expectation of inevitable margin compression.

SIA semiconductor industry data tracking decades of memory market cycles provides the historical baseline against which the current pricing environment stands out most sharply, with prior peaks consistently followed by supply-driven margin compression that erased assumed structural gains.

The shift now visible is toward an infrastructure model. Hyperscalers do not simply purchase the cheapest available NAND; they run qualification processes that test specific products against their proprietary workload profiles. Once a product passes qualification, the supplier gains priority allocation status and multi-year contract visibility. This is the mechanism that converts a commoditised component into a semi-captive supply relationship.

| Dimension | Commodity Model | Infrastructure Model |

|---|---|---|

| Pricing Mechanism | Spot market / price-taker | Multi-year contracts / ASP premiums |

| Customer Relationship | Transactional, interchangeable | Qualification-driven, sticky |

| Margin Profile | Volatile, boom-bust | Higher floor, structurally supported |

| Valuation Multiple | 5-10x EV/EBITDA | 15-20x EV/EBITDA (if thesis holds) |

SanDisk’s BiCS8 QLC enterprise SSD qualifications at two major hyperscalers illustrate the new dynamic directly. Enterprise SSDs now represent a high-teens percentage of SanDisk’s total bit shipments, and that share is growing with the ramp.

BiCS8 and the product ramp that could extend SanDisk’s competitive moat

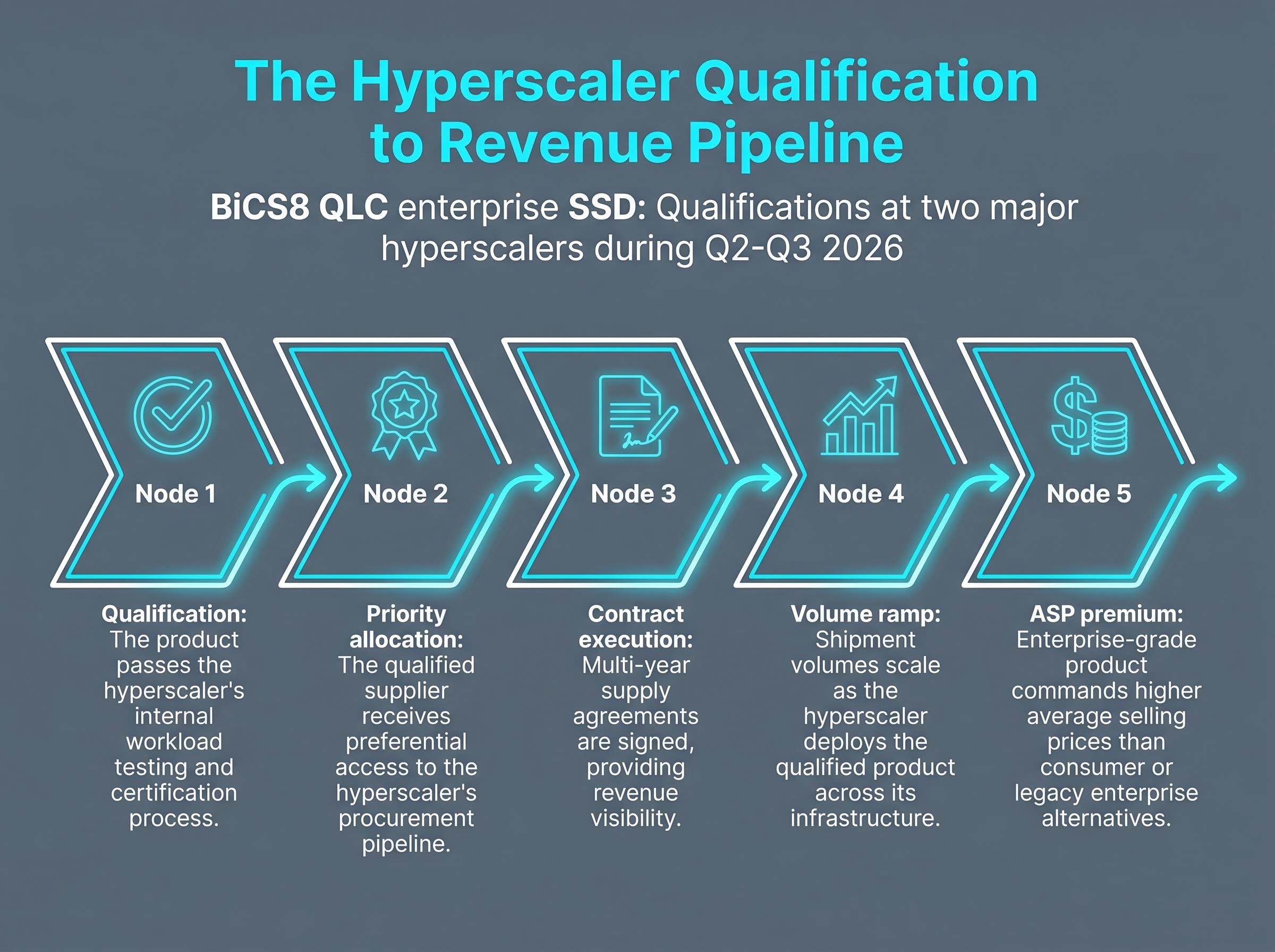

The BiCS8 QLC enterprise SSD platform received qualifications at two major hyperscalers during the Q2-Q3 2026 ramp period. The qualification process itself is the competitive advantage: competitors must replicate it from scratch, creating a lead-time barrier that outlasts any single pricing cycle.

The sequential logic of how a hyperscaler qualification converts into durable revenue follows a specific pathway:

- Qualification: The product passes the hyperscaler’s internal workload testing and certification process.

- Priority allocation: The qualified supplier receives preferential access to the hyperscaler’s procurement pipeline.

- Contract execution: Multi-year supply agreements are signed, providing revenue visibility.

- Volume ramp: Shipment volumes scale as the hyperscaler deploys the qualified product across its infrastructure.

- ASP premium: Enterprise-grade product commands higher average selling prices than consumer or legacy enterprise alternatives.

Enterprise SSDs at a high-teens percentage of total bit shipments, and growing, indicate that SanDisk is still in the early to middle stages of this ramp. Management has framed the transition explicitly.

Management Commentary SanDisk’s leadership described a shift toward a new business model built on extended customer relationships backed by firm financial commitments, positioning the BiCS8 ramp as a structural change in how the company contracts with its largest buyers.

The question for investors evaluating SanDisk at $1,116 per share is whether the full data centre revenue contribution from this ramp is already reflected in the stock, or whether the acceleration implied by Q4 guidance of approximately $8 billion suggests the ramp’s peak contribution remains ahead.

The bull and bear case for memory sector valuation through 2027

The structural-versus-cyclical debate carries direct valuation consequences. Both sides of the argument rest on specific, testable claims.

Melius Research analyst Ben Reitzes initiated coverage on memory sector peers with Buy ratings, setting a $700 price target on Micron and arguing that AI-driven memory demand creates durable, subscription-like revenue cycles. Under this framework, the sector could trade at 15-20x forward EV/EBITDA (enterprise value to earnings before interest, taxes, depreciation, and amortisation), with the potential for multiples to double or triple current levels through 2030.

Melius Research Thesis Analyst Ben Reitzes argues that subscription-like demand cycles in memory could support a doubling or tripling of current sector multiples, driven by durable AI infrastructure spend extending through 2030.

SK Hynix trades at approximately 12x forward EV/EBITDA, which some analysts characterise as undervalued relative to peers given its high-bandwidth memory (HBM) and NAND exposure. Historical memory sector volatility, however, gives sceptics a strong prior: the industry has produced margin peaks that looked structural before and were not.

The bear case centres on 2027 capacity convergence. If expansion programmes at Samsung, SK Hynix, Micron, and Kioxia deliver new capacity into a market where AI capital expenditure growth moderates, the oversupply event could compress margins sharply. The 97% sequential revenue growth in Q3 raises a legitimate question: is this a new baseline, or is it a peak?

The same capex commitments that are absorbing NAND supply carry hardware valuation risks that analysts are increasingly examining, including whether $610-650 billion in collective hyperscaler spending in 2026 can be sustained as investor scrutiny shifts from raw infrastructure deployment to demonstrable returns on that investment.

| Factor | Bull Case Reading | Bear Case Reading |

|---|---|---|

| AI Capex | Durable, multi-year build-out | Growth rate moderates by 2027 |

| NAND Pricing | Structurally higher floor | Cyclical peak, reversion ahead |

| Capacity Expansion | Lags demand through 2028 | Converges with demand in 2027 |

| Contract Structure | Multi-year, subscription-like | Reverts to spot once supply loosens |

| Sector Multiples | 15-20x justified, potential for higher | Current multiples already reflect optimism |

The specific forward indicators that would tilt the balance include hyperscaler capex trajectory disclosures in coming quarters, capacity expansion timelines from major NAND producers, and whether SanDisk’s Q4 2026 actuals land within or above the guided range.

What the memory sector supercycle thesis means for portfolio positioning in mid-2026

The structural signals sort into a hierarchy of conviction. The strongest indicators are the ones hardest to dismiss: multi-year hyperscaler contracts, BiCS8 qualifications at two major customers, and 78.4% gross margins sustained at scale. The contested indicators require further evidence: the precise attribution of demand to specific AI workload categories remains vague, and the 2027 oversupply risk is a calendared threat that cannot yet be dismissed. The unresolved variable is near-term: whether Q4 2026 actuals confirm or reset the revenue baseline established in Q3.

- High-conviction structural signals: Multi-year contracts, BiCS8 hyperscaler qualifications, 78.4% non-GAAP gross margins

- Contested indicators: Agentic AI demand attribution specifics, 2027 oversupply risk timeline

- Unresolved variables: Q4 2026 actuals versus guidance midpoint of approximately $8 billion

Relative value across memory sector peers

At $1,116.25 with Wedbush targeting $1,200, SanDisk’s near-term upside to that target is approximately 7%. SK Hynix at roughly 12x forward EV/EBITDA sits below the 15-20x sector framework that Melius applies, implying a discount that could close if the structural thesis holds. Micron, with a Melius price target of $700 and a Buy rating, offers a different exposure mix weighted toward HBM alongside NAND.

The AI storage supercycle argument has produced similarly aggressive analyst target revisions across adjacent hardware categories, with Morgan Stanley designating Seagate as its top IT hardware pick and projecting a structural HDD demand cycle driven by the same hyperscaler data centre build-outs that are absorbing high-end NAND production.

The Melius subscription-model multiple expansion thesis extends through 2030. For investors sizing positions in mid-2026, that timeframe means accepting potential 2027 volatility as the cost of a longer-duration structural bet, not a near-term trade. The sector-wide EV/EBITDA framework from Melius applies differentially depending on each company’s HBM, NAND, and enterprise SSD exposure mix.

Memory is repricing, but the investment case is not yet settled

The structural case rests on three interlocking conditions: AI capital expenditure durability, hyperscaler contract stickiness, and successful BiCS8 ramp execution. All three need to hold simultaneously. If any one fails, the margin and multiple expansion thesis weakens materially.

History gives memory sector sceptics a strong prior. The industry has produced earnings peaks that appeared structural before and proved cyclical. The 2027 capacity convergence from multiple major producers is a real, calendared risk, not a hypothetical concern.

The near-term data events that will sharpen the thesis are specific and trackable:

Mispriced volatility in AI hardware earnings is a risk that cuts across the entire memory sector positioning debate: if options markets are systematically underpricing post-earnings moves for the hyperscalers whose capex decisions set NAND demand, then memory equity investors may also be underestimating the magnitude of re-rating events in either direction when quarterly disclosures arrive.

- SanDisk Q4 2026 actuals versus the $7.75-$8.25 billion guidance range

- Hyperscaler capital expenditure revision announcements in coming quarters

- Competitor capacity expansion disclosures from Samsung, SK Hynix, Micron, and Kioxia

The evidence is mounting. The uncertainty is real and specific rather than vague. For finance-educated investors weighing exposure to memory names in mid-2026, the question is not whether the sector has repriced; it is whether the repricing reflects a permanent shift in how the market values storage infrastructure, or whether it will prove to be one more chapter in the longest-running cyclical story in semiconductors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.