How to Position for the Most Event-Dense Week of July 2026

2 hrs ago

Three memory chip stocks, Micron (MU), Sandisk (SNDK), and SK Hynix, combined for gains exceeding 250% over the trailing 30 days ending 12 May 2026. That compression of returns would normally take years to accumulate in a sector known for cyclical volatility. The move was not confined to a single ticker or a single catalyst. It arrived at the intersection of sold-out high-bandwidth memory (HBM) capacity, a threatened Samsung strike scheduled for 21 May, and a US-China trade delegation that reshuffled competitive dynamics faster than most investors anticipated. What follows breaks down the five forces behind the rally, explains how HBM supply constraints work for readers new to memory market cycles, and identifies the risks that could unwind recent gains if conditions shift.

The scale of the 30-day move is difficult to overstate. Micron gained approximately 90%. Sandisk rose roughly 82%, including a single-week surge of about 28%. SK Hynix climbed approximately 78% over the same window.

When three memory names with different product mixes, different geographic exposures, and different customer concentrations all move in the same direction at the same magnitude, the signal is structural. Investors are repricing the entire sector’s supply-demand outlook, not reacting to one company’s earnings beat or one product cycle. The broader semiconductor indices confirm the breadth: SOXX is up approximately 45% year-to-date in 2026, while SMH has surged more than 60%.

| Stock | 30-day return (approx.) | MU two-day surge |

|---|---|---|

| Micron (MU) | ~90% | ~20%+ |

| Sandisk (SNDK) | ~82% | N/A |

| SK Hynix | ~78% | N/A |

Within the broader 30-day trend, Micron recorded a standalone two-day surge of more than 20% during the week of 12 May. Intel gained approximately 18%, AMD roughly 12%, and the SOX index rose about 8% across those same two sessions. The catalyst was specific: the roster of the Trump administration’s China trade delegation became publicly known on Monday, with reports suggesting details circulated among market participants late the prior week. The two-day move was concentrated in memory and adjacent semiconductor names, not a broad market event.

High-bandwidth memory, or HBM, is the product category underpinning the entire sector repricing. For readers less familiar with memory market structure, HBM is not standard DRAM. It is a specialised, premium-priced memory product designed to sit directly alongside AI accelerator chips, most notably Nvidia’s GPU lineup, inside datacentre servers. Three characteristics separate it from commodity DRAM:

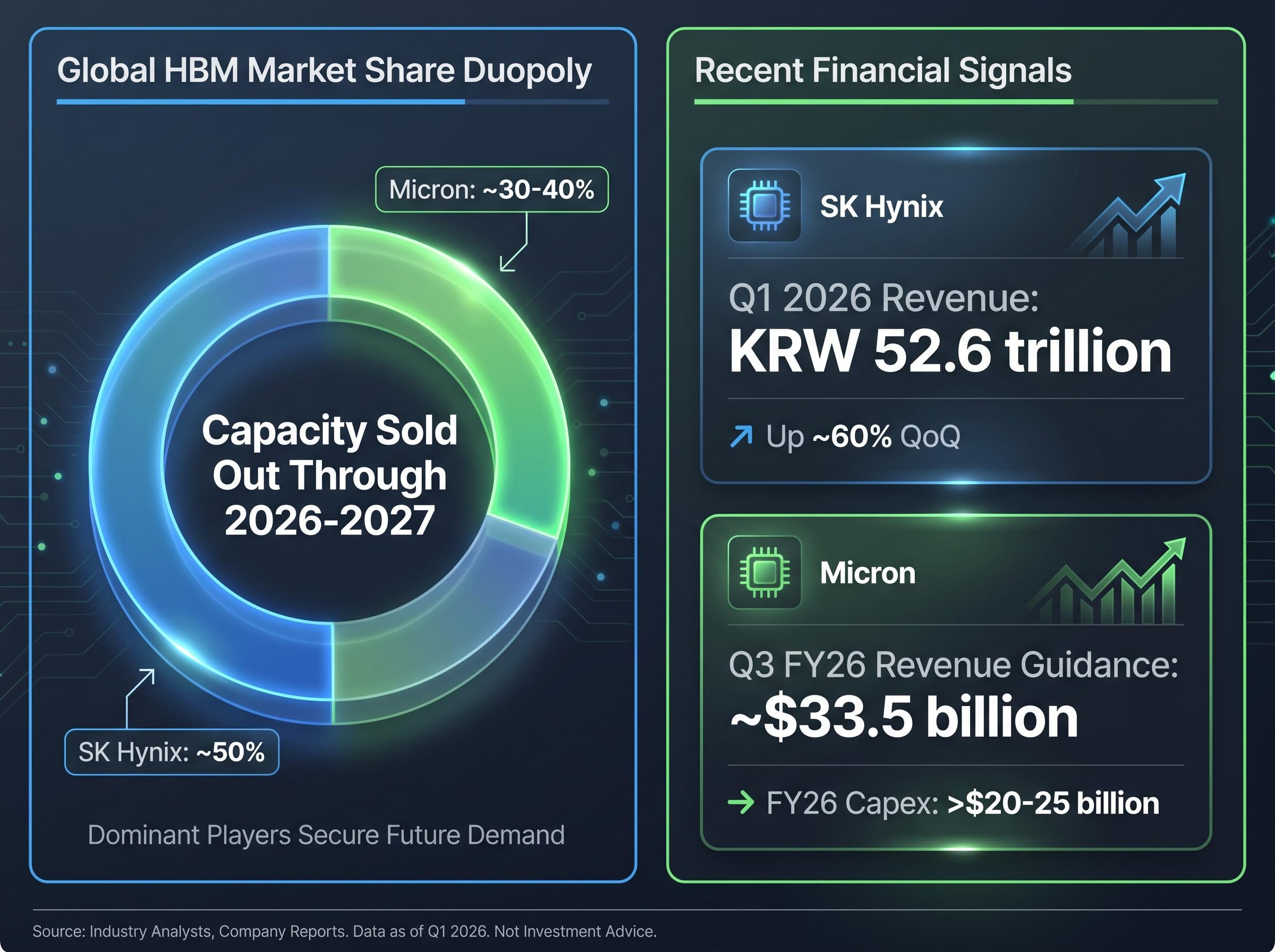

These constraints explain why two companies control the effective global supply. SK Hynix holds approximately 50% HBM market share and is Nvidia’s primary supplier. Micron holds roughly 30-40%. Together, their HBM capacity is sold out through 2026-2027.

AI-driven storage supply exhaustion is not isolated to HBM; enterprise hardware prices for high-capacity models surged up to 60% across the broader storage stack in early 2026, with major suppliers confirming sold-out production capacity through year-end and projecting further 10-20% price increases in H2.

HBM demand forecasts for 2025-2026 project year-on-year growth of approximately 130% in 2025 followed by 70% in 2026, a pace that outstrips the manufacturing capacity additions even the most aggressive capex programs can deliver in the same timeframe.

HBM capacity across SK Hynix and Micron is sold out through 2026-2027, a supply condition that persists not because producers are withholding investment, but because manufacturing complexity limits how quickly capacity can respond to demand.

The earnings confirm the demand pull. SK Hynix reported Q1 2026 revenue of KRW 52.6 trillion, up approximately 60% quarter-over-quarter. Micron guided Q3 FY26 revenue to approximately $33.5 billion, with full-year FY26 capital expenditure expected above $20-25 billion. SK Hynix has confirmed a US fab expansion in Indiana oriented toward HBM production. The capital is flowing, but the capacity is years away from relieving current tightness.

The delegation story was widely reported as a diplomatic headline. The more consequential signal was competitive.

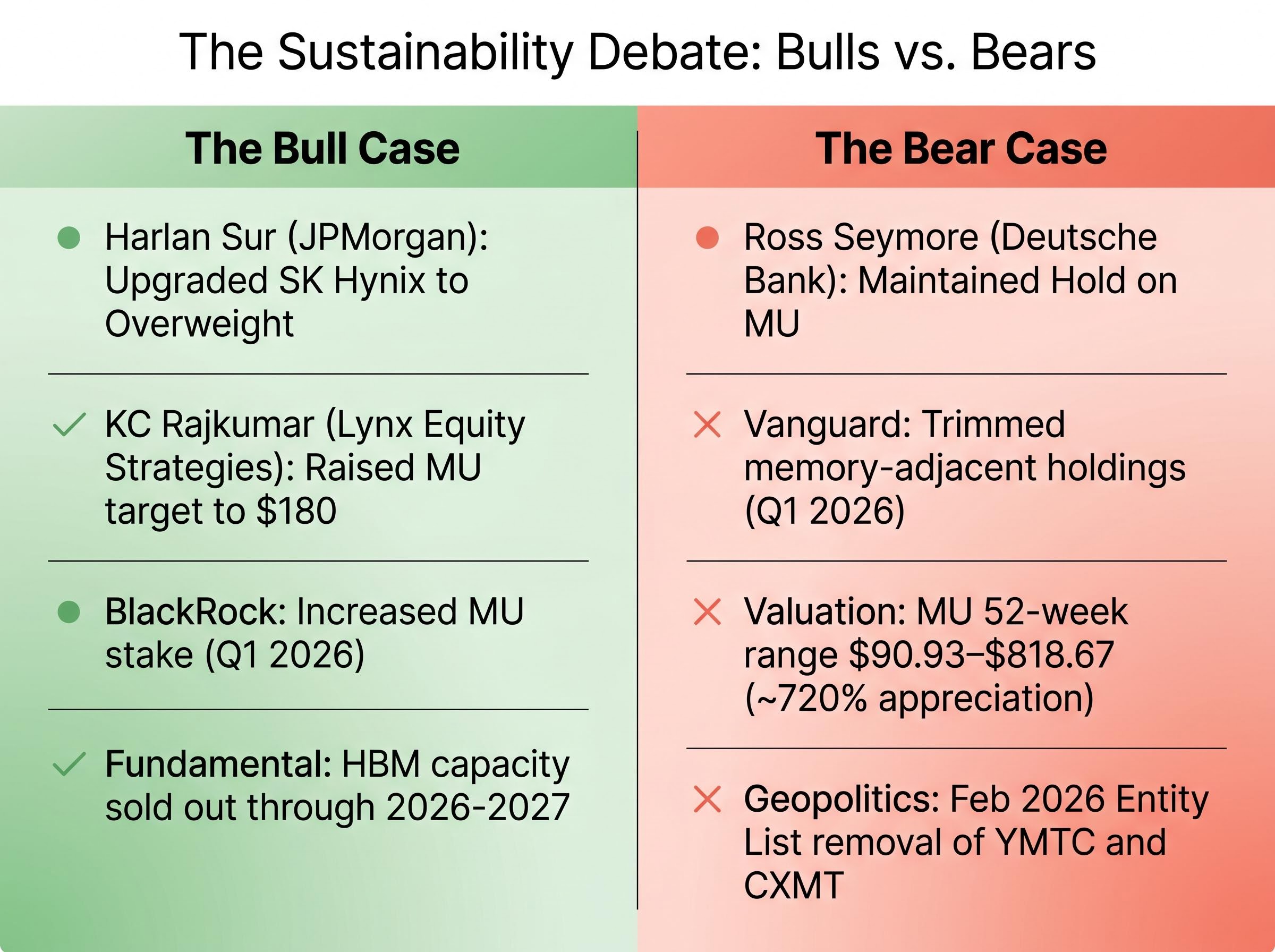

Micron CEO Sanjay Mehrotra joined the Trump administration’s China trade delegation. Nvidia CEO Jensen Huang was absent. Semiconductor capital equipment CEOs were also excluded. KC Rajkumar of Lynx Equity Strategies identified the analytical implication: Micron may have derived greater benefit from who was excluded than from its own CEO’s inclusion.

Rajkumar’s core observation was that the absence of equipment CEOs signals reduced likelihood of waivers for Chinese memory producers YMTC and CXMT, because those companies need access to advanced manufacturing tools to ramp competitive HBM capacity.

The chain of logic runs as follows:

A complicating fact: in February 2026, Reuters reported that YMTC and CXMT were removed from the Entity List, reversing 2022 additions. No confirmed waivers for advanced semiconductor manufacturing tools have followed as of 12 May 2026, but the Entity List removal introduces genuine ambiguity about the long-term trajectory of US-China memory chip policy. Micron’s own Chinese market access remains unresolved.

No production has been disrupted. No DRAM output has declined. The Samsung strike has not started. Markets moved anyway, and the reason illustrates how supply-side pricing works in concentrated commodity markets.

The timeline is precise. In April 2026, the National Samsung Electronics Union (NSEU), representing approximately 36,000-40,000 unionised employees, rejected Samsung’s wage offer and voted overwhelmingly to authorise a strike. As of 11-12 May, unions and Samsung management remain engaged in active mediation talks. A 17-18 day work stoppage is scheduled to begin 21 May if mediation fails.

| Date | Event | Market implication |

|---|---|---|

| April 2026 | NSEU rejects wage offer, votes to authorise strike | Supply-risk premium begins building into memory pricing |

| 11-12 May 2026 | Active mediation talks ongoing | Uncertainty sustains elevated risk premium |

| 21 May 2026 | Planned 17-18 day strike if talks fail | Estimated 3-4% DRAM supply decline if strike proceeds |

Analysts estimate a potential DRAM supply decline of 3-4% if the strike proceeds as planned. In a market where HBM capacity is already sold out, even a modest reduction in Samsung’s output disproportionately tightens conditions for the one product where supply has no slack. Samsung reported Q1 2026 revenue of KRW 134 trillion, up approximately 43% quarter-over-quarter, confirming the demand environment is strong regardless of the labour dispute’s resolution.

Samsung’s HBM yield challenges remain the most consequential competitive variable in the memory sector; the company holds below 30% of the HBM market compared to SK Hynix’s approximately 62% share, and a successful HBM4 qualification with Nvidia would represent a material shift in the supply concentration that currently benefits SK Hynix and Micron.

Rajkumar has noted that even a successful negotiation resolution would likely be insufficient to reverse gains already realised in memory chip pricing. Markets price in the probability of supply events before they materialise; the stock response can precede and sometimes exceed the actual operational impact.

The bull and bear cases for memory stocks are unusually far apart. That gap itself is informative.

The specific variable that most determines which camp proves correct: whether HBM pricing holds through H2 2026 or begins to soften as Samsung resolves its labour dispute and incremental capacity comes online. The next data point, whether it arrives from Samsung mediation, H2 pricing signals, or hyperscaler capital expenditure updates, will carry outsised weight.

The traditional memory chip cycle followed a predictable pattern: capex surge, oversupply, price crash, inventory correction, recovery. That pattern assumed memory was a commodity product where supply could scale roughly in proportion to investment.

HBM has altered that logic. Supply is structurally constrained by manufacturing complexity, not by capex decisions alone.

The advanced packaging for AI chip market outlook identifies the shift from traditional single-layer packaging to 2.5D and 3D stacking technologies as a structural inflection point, one that simultaneously drives AI accelerator performance gains and locks in the yield-constrained manufacturing dynamic that keeps HBM supply inelastic.

HBM capacity constraints are engineering-driven, not purely capex-driven, which limits how quickly supply can respond to demand even if producers commit capital aggressively.

Agentic AI demand as a permanent consumption floor is a key structural argument separating the current rally from prior memory supercycles; AMD procurement data cited in sector-wide analysis suggests agentic workloads running continuously 24/7 are converting episodic chip demand into baseline consumption, with the server CPU market projected to exceed $120 billion by 2030.

The three-catalyst convergence that produced this rally (AI demand pull, supply-side Samsung risk, and geopolitical trade policy) represents a pattern investors should expect to recur as AI infrastructure buildout continues through the late 2020s. The structural demand driver is not cyclical; it is tied to hyperscaler capital expenditure that shows no sign of moderating.

Three forward variables warrant close monitoring:

The five forces behind this rally, AI-driven HBM demand, sold-out supply conditions, the Samsung labour risk, competitive relief from US-China trade policy dynamics, and strong earnings confirmation, converged within a single 30-day window. That convergence explains the magnitude. Whether it persists depends on what happens next.

21 May is the immediate binary event. If Samsung mediation fails and the strike proceeds, the supply-risk premium embedded in memory stocks receives reinforcement. If talks succeed, some of the recent risk-driven multiple expansion may partially reverse.

The broader durability question rests on HBM sold-out conditions persisting through 2026-2027. Every data point on Nvidia capital expenditure, every hyperscaler AI spending update, and every BIS policy signal is now, by extension, a memory sector indicator. The structural case has been made. The market is now waiting to see if the structure holds.

The hyperscaler capex-to-revenue lag introduces a timing risk that sits beneath the structural supply thesis: Morningstar analyst Dennis Li has identified an 18-24 month gap between committed infrastructure spend and proven revenue generation, and Gartner estimates only 20% of current AI agent pilots are scalable to production by 2027, which means the demand floor for HBM could face a plateau before new supply capacity is fully absorbed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

High-bandwidth memory (HBM) is a premium, specialised DRAM product designed to sit alongside AI accelerator chips in datacentre servers. It matters for memory chip stocks because its complex stacked die architecture limits how quickly supply can be added, keeping prices elevated and benefiting dominant producers like SK Hynix and Micron.

The surge was driven by five converging forces: sold-out HBM capacity through 2026-2027, a threatened Samsung labour strike that raised supply-risk concerns, a US-China trade delegation seen as limiting Chinese memory producers, strong earnings from SK Hynix and Micron, and broader AI infrastructure demand pulling chip spending higher.

The National Samsung Electronics Union representing approximately 36,000-40,000 employees voted to authorise a 17-18 day strike scheduled for 21 May 2026 if mediation fails. Analysts estimate this could reduce DRAM supply by 3-4%, which disproportionately tightens conditions in a market where HBM capacity is already sold out.

The bull case rests on HBM capacity sold out through 2026-2027, strong earnings beats from SK Hynix and Micron, institutional accumulation, and analyst upgrades. The bear case centres on peak HBM pricing risk in H2 2026, low single-digit consumer DRAM growth, the February 2026 Entity List removal of Chinese producers YMTC and CXMT, and valuation stretch concerns.

Micron CEO Sanjay Mehrotra joined the Trump administration's trade delegation while semiconductor equipment CEOs were excluded, signalling the administration is unlikely to grant tool-access waivers to Chinese memory producers YMTC and CXMT. Without those waivers, Chinese competitors cannot meaningfully expand advanced memory capacity, preserving pricing power for SK Hynix and Micron.