How the US Government Became Intel’s Investor and Deal Broker

25 mins ago

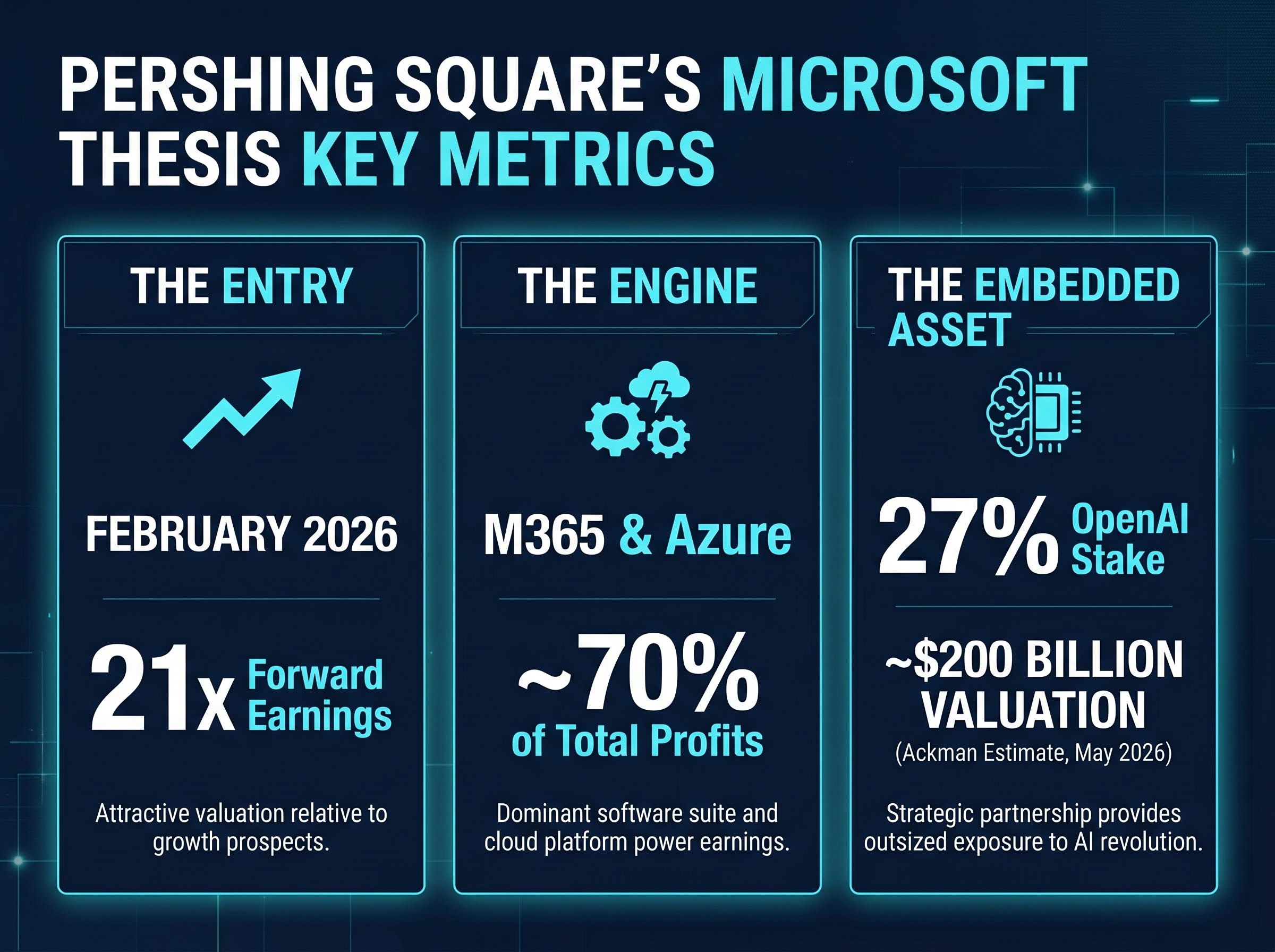

Bill Ackman bought Microsoft in February 2026 at roughly 21x forward earnings, a valuation below the stock’s own historical average, and publicly called it one of the most compelling large-cap setups he has seen. The disclosure, made via a 13F-HR filing on 15 May 2026 and confirmed by Ackman on X, arrives as Wall Street actively debates whether Microsoft’s approximately $190 billion capital expenditure commitment is a generational infrastructure bet or an exercise in excess. Ackman’s entry reframes that debate. What follows is a structured breakdown of the full Pershing Square investment thesis, translating Ackman’s specific arguments on M365, Azure, the OpenAI stake, and consumption-based pricing into a picture of how a high-conviction activist investor is sizing up one of the world’s most valuable companies right now.

The purchases began in February 2026, immediately following Microsoft’s Q2 FY2026 earnings release. Short-term investors sold on near-term concerns. Ackman bought into them.

His public argument, confirmed on X alongside the 15 May 2026 13F-HR disclosure, is that 21x forward earnings sits below Microsoft’s own historical valuation average. For a company generating the cash flows Microsoft generates, that multiple represented a structural discount rather than a fair reflection of the business.

Ackman characterised short-term investors as having “overreacted to transient challenges,” framing the February sell-off as a temporary dislocation in a franchise he considers durable.

The pattern is familiar. Ackman has made this move before: patient capital entering high-quality franchises during periods of market scepticism. The prior comparable positions and their outcomes tell the story:

The 21x figure is not incidental to the thesis. It is the thesis. Everything that follows in Ackman’s argument, the platform moat, the OpenAI optionality, the consumption-pricing transition, depends on that entry multiple being cheap relative to what the business will earn as AI monetisation scales.

The 21x forward earnings entry multiple looks different depending on where an investor positions Microsoft within the broader AI valuation cycle; with the S&P 500 Shiller CAPE at 40-41 and technology sector forward multiples running at 23-36x, a 21x multiple on a franchise generating 70% of profits from two entrenched cloud platforms sits at the lower end of the large-cap AI cohort by conventional metrics.

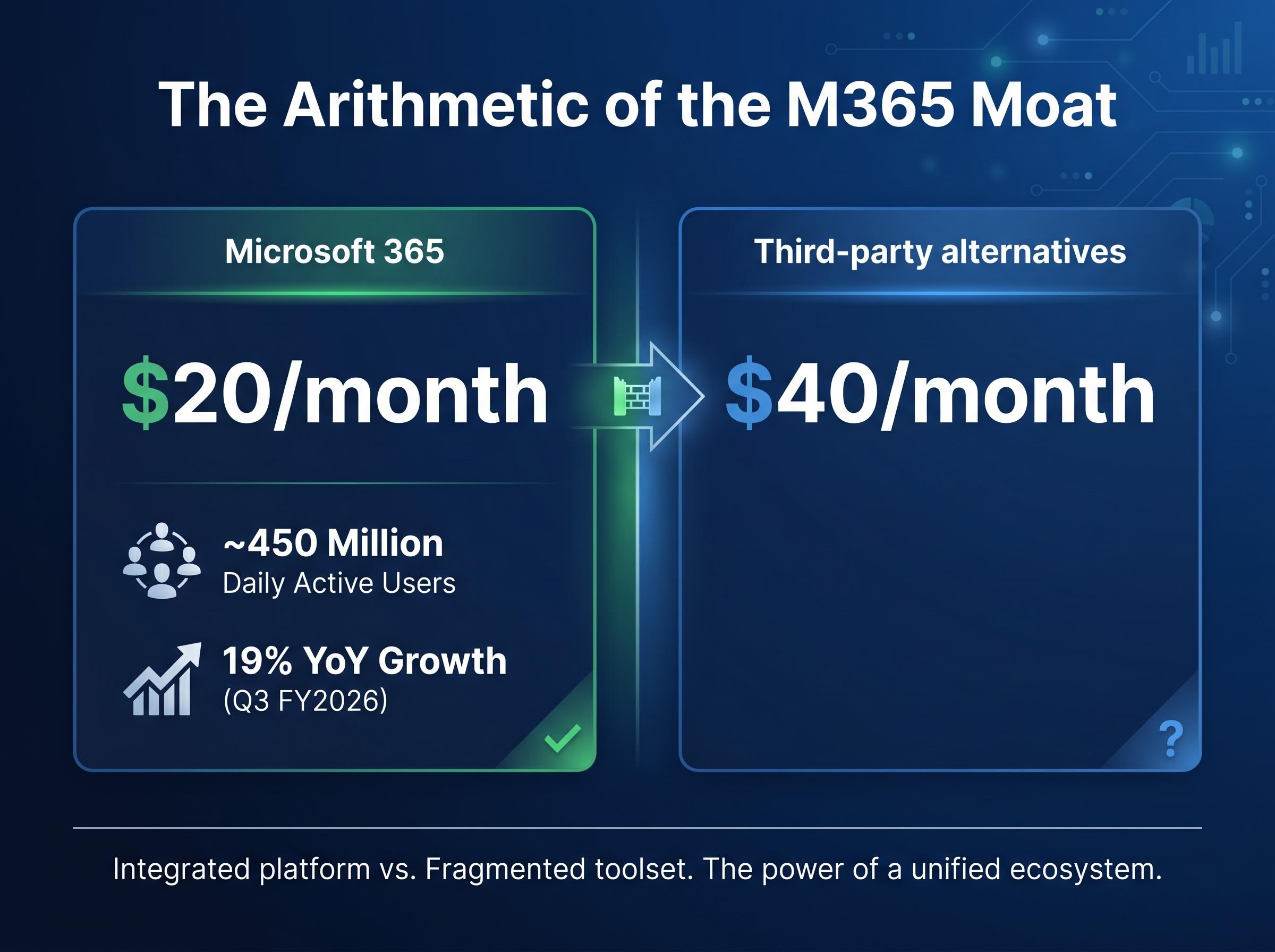

Microsoft 365 and Azure together account for approximately 70% of Microsoft’s total profits. That concentration is precisely why Ackman focuses on these two segments as the engine underneath everything else in the thesis.

M365 serves approximately 450 million daily active users. Its average pricing sits at roughly $20 per user per month, compared with approximately $40 for comparable standalone third-party applications. The pricing gap reflects the bundled value of security infrastructure, regulatory compliance tools, and an integrated productivity ecosystem that competitors, including Anthropic’s Claude Cowork offering, cannot easily replicate at equivalent cost.

| Metric | Microsoft 365 | Comparable third-party alternatives |

|---|---|---|

| Pricing per user per month | ~$20 | ~$40 |

| Daily active users | ~450 million | Varies by provider |

| Commercial cloud revenue growth (Q3 FY2026) | 19% YoY | N/A |

M365 commercial cloud revenue grew 19% year-over-year in Q3 FY2026 (quarter ended 31 March 2026). At that scale and at half the per-user cost of alternatives, the switching cost argument is not abstract. It is arithmetic.

Azure revenue grew 40% year-over-year in Q3 FY2026. Ackman’s thesis treats that figure not as a backward-looking metric but as prospective validation of the infrastructure investment Microsoft is making.

Azure’s competitive position within the hyperscaler tier looked different after Q1 2026 earnings, with Google Cloud growing 63% year-over-year against Azure’s 40% and AWS posting a 93% surge in backlog to approximately $364 billion, data points that complicate a thesis built on Azure as the primary AI infrastructure beneficiary while simultaneously confirming that enterprise AI demand is structurally real rather than cyclical.

The Microsoft Q3 FY2026 earnings release confirms total revenue of $82.9 billion for the quarter ended 31 March 2026, alongside the 40% Azure growth and 19% M365 commercial cloud growth figures that form the empirical backbone of Ackman’s infrastructure and monetisation argument.

The argument is that AI workloads are a structural demand driver for Azure, not a cyclical one. If enterprise AI adoption continues at scale, Azure’s growth rate becomes the most direct measure of whether the capital expenditure programme is generating returns. Ackman is underwriting that trajectory continuing rather than reverting.

The prevailing concern heading into 2026 was that Microsoft’s AI story carried more risk than reward. The DeepSeek disruption narrative raised questions about competitive moats in large language models. The OpenAI partnership restructuring prompted speculation about dependency risk. Ackman’s thesis inverts both concerns.

Ackman characterised the OpenAI restructuring not as a retreat but as a deliberate pivot toward a “flexible, multi-model AI framework” that reduces single-vendor risk while preserving the economic upside of the partnership.

Microsoft holds approximately a 27% economic interest in OpenAI. Ackman values that stake at approximately $200 billion, based on OpenAI’s most recent financing round as of May 2026, and argues that this value is not reflected in Microsoft’s prevailing market price at his entry point.

OpenAI’s March 2026 funding announcement confirmed a post-money valuation of $852 billion on $122 billion in committed capital, the financing round that Ackman cites as the basis for his approximately $200 billion valuation of Microsoft’s roughly 27% economic interest in the company.

That claim is the most provocative element of the thesis for sophisticated investors to interrogate. An economic interest in OpenAI, if valued at $200 billion, represents a substantial embedded asset that investors buying at 21x forward earnings are effectively receiving at a discount, or at least not paying a premium for.

Ackman’s specific rebuttals to the AI competition narrative break into three discrete arguments:

Microsoft has projected approximately $190 billion in capital expenditure for calendar year 2026, directed primarily at AI infrastructure and data centre buildout. Against Q3 FY2026 total revenue of $82.9 billion, the scale of that commitment is difficult to ignore.

The debate over whether this capex programme represents a competitive moat or a margin headwind is the single most contested question in Microsoft’s valuation today. Both sides have specific arguments:

Wall Street has developed increasingly specific frameworks for evaluating AI infrastructure spending credibility, with GPU utilisation above 80% by end of deployment year emerging as the single most widely cited metric across Goldman Sachs, JPMorgan, UBS, and Bernstein analyses of Microsoft’s $190 billion commitment, a standard that Azure’s 40% revenue growth rate partially satisfies but does not fully resolve.

How investors resolve this debate determines whether Microsoft’s current earnings multiple appears cheap or fair. That makes this section the hinge point of Ackman’s entire argument.

Per-seat subscription pricing, the traditional model for M365 and similar enterprise software, charges a fixed fee per user regardless of how much each user consumes. Consumption-based billing, by contrast, charges based on actual usage volume, meaning revenue scales directly with activity levels.

Ackman frames this distinction as central to the capex thesis. Per-seat pricing would cap revenue growth at the rate of new user additions. Consumption-based billing for Azure and Copilot removes that ceiling. As AI agent-driven activity scales within enterprise environments, each agent interaction generates metered revenue. The pricing model shift means the infrastructure investment could generate returns that accelerate alongside adoption, rather than growing linearly with headcount.

The 15 May 2026 13F-HR disclosure moved the conversation beyond Ackman’s individual thesis. Analysts revised Microsoft price targets upward following the filing, and institutional commentary characterised the position as a bullish signal for the company’s AI valuation narrative.

The signalling effect carries weight because of how Ackman disclosed it. Naming a specific valuation entry point (21x forward earnings), defending it publicly on X and in media interviews, and drawing explicit comparisons to prior successful positions in Alphabet, Meta, and Amazon is qualitatively different from passive large-cap accumulation. It carries more interpretive weight for other market participants.

Three layers of market reaction followed the disclosure:

One data point remains unresolved. The exact share count and dollar value of the Pershing Square position are referenced in media coverage but have not been independently confirmed from the SEC EDGAR filing itself, which remains the recommended source for precision.

Ackman’s public thesis is unusually detailed for a 13F disclosure context, which gives individual investors a rare window into how a sophisticated institutional fund is evaluating one of the most debated AI valuations in the market today.

The three strongest structural pillars are clear: the M365 and Azure installed base, generating approximately 70% of total profits with high switching costs; the OpenAI economic interest, valued by Ackman at approximately $200 billion and argued to be unrecognised in the current stock price; and the consumption-based pricing transition, which ties infrastructure spend to scalable revenue generation as AI adoption grows.

Ackman framed Microsoft as offering “one of the most compelling risk-reward opportunities in large-cap equities,” citing the combination of a below-average entry multiple and AI assets he considers mispriced by the market.

The genuine open questions sit alongside those pillars. Whether the $190 billion capex programme generates the ROIC Ackman is implying remains unproven at this scale. Whether consumption-to-revenue conversion materialises on the timeline the thesis assumes is not yet visible in quarterly results. Whether the OpenAI stake’s embedded value ever becomes formally recognised in Microsoft’s market price is an open structural question.

For investors wanting to stress-test the $200 billion OpenAI stake valuation that sits at the centre of Ackman’s sum-of-the-parts argument, our full explainer on the OpenAI governance investigation covers the House Oversight Committee probe into Sam Altman’s conflict-of-interest profile, the unresolved SEC inquiry, and historical precedents from Uber and Robinhood showing that governance controversies have produced IPO valuation discounts of 30-45% below private market expectations.

Investors tracking this thesis should watch three forward-looking data signals:

Ackman’s entry at 21x forward earnings is a specific, falsifiable bet. The claim is that Microsoft’s AI assets, particularly the OpenAI stake and Azure consumption growth, are undervalued relative to the earnings multiple at the time of purchase in February 2026. The comparisons to Alphabet, Meta, and Amazon position this explicitly as a multi-year re-rating thesis tied to AI monetisation becoming visible in reported earnings, not a short-term call.

What distinguishes this disclosure is the level of public detail. Ackman has named his entry point, identified the specific assets he considers mispriced, and provided a framework for how monetisation should unfold. That transparency means individual investors can benchmark and re-evaluate the thesis against each quarterly earnings cycle rather than treating it as opaque institutional positioning.

The evidence will arrive quarter by quarter. Azure growth rates, Copilot adoption figures, and any developments around the OpenAI stake’s valuation will either validate or challenge the thesis Ackman has laid out. The data, not the conviction, will determine the outcome.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

A 13F-HR is a quarterly regulatory filing required by the SEC for institutional investment managers holding over $100 million in assets, disclosing their equity holdings. Ackman's 13F-HR filed on 15 May 2026 revealed that Pershing Square had purchased Microsoft shares starting in February 2026.

Ackman argued that 21x forward earnings sits below Microsoft's own historical valuation average, representing a structural discount for a company generating approximately 70% of its profits from two entrenched platforms, M365 and Azure, with additional upside from an OpenAI stake he values at roughly $200 billion.

Microsoft holds approximately a 27% economic interest in OpenAI, which Ackman values at roughly $200 billion based on OpenAI's most recent financing round that placed a post-money valuation of $852 billion on the company. Ackman argues this embedded value is not reflected in Microsoft's prevailing market price.

Azure revenue grew 40% year-over-year in Q3 FY2026 (quarter ended 31 March 2026), which Ackman treats as prospective validation that AI workloads represent a structural rather than cyclical demand driver. The growth rate is the primary metric investors should monitor to confirm or challenge his thesis quarter by quarter.

The main open questions include whether the $190 billion capital expenditure programme generates the return on invested capital Ackman implies, whether consumption-based revenue conversion materialises on the assumed timeline, and whether the approximately $200 billion OpenAI stake valuation is ever formally recognised in Microsoft's market price.