Samsung Rout Anchors Global Selloff as Bonds and Stocks Fall Together

10 hrs ago

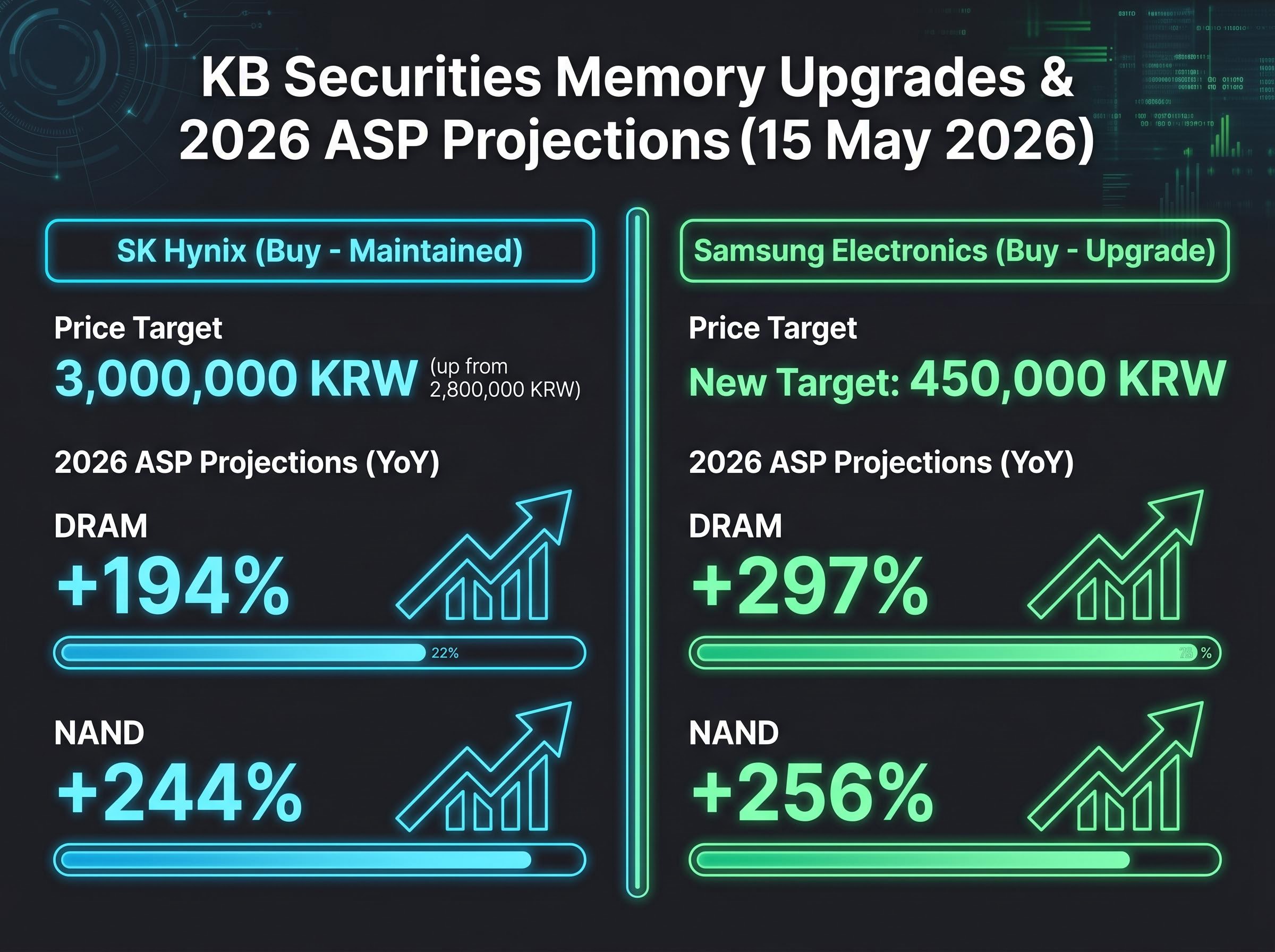

KB Securities analyst Jeff Kim has upgraded both SK Hynix and Samsung Electronics in a single note issued on 15 May 2026, projecting that SK Hynix will post the highest operating margin of any company on earth this year. The call rests on a structural memory supply deficit that Kim argues will persist until at least 2027, while hyperscaler capital expenditure accelerates toward $725 billion in 2026 alone. The simultaneous upgrades arrive as AI infrastructure spending has crossed from discretionary to non-negotiable for the world’s largest technology companies, with memory capacity the binding constraint on how fast that buildout can proceed. What follows is a breakdown of Kim’s specific price targets, earnings projections, and the structural rationale underpinning the call, offering a framework for evaluating both semiconductor stocks today.

The broader semiconductor supercycle that produced a $3.8 trillion market value gain over six weeks through mid-May 2026 is itself partly a product of the structural demand shift KB Securities is pricing: agentic AI workloads running continuously 24/7 are converting episodic chip consumption into permanent baseline demand, a dynamic that AMD procurement data suggests will expand the server CPU market above $120 billion by 2030.

Jeff Kim’s note sets a price target of 3,000,000 KRW for SK Hynix, up from a prior target of 2,800,000 KRW, while maintaining a Buy rating. Samsung Electronics receives a Buy upgrade with a new price target of 450,000 KRW.

| Company | Previous Target | New Target | Rating | Date |

|---|---|---|---|---|

| SK Hynix | 2,800,000 KRW | 3,000,000 KRW | Buy (maintained) | 15 May 2026 |

| Samsung Electronics | N/A | 450,000 KRW | Buy (upgrade) | 15 May 2026 |

The Samsung upgrade is the more significant rating shift, restoring positive coverage from a house that had previously been less constructive on the stock. The SK Hynix target revision, while incremental, sits atop an earnings forecast aggressive enough to require its own explanation.

The price targets are outputs of a supply thesis, not standalone optimism. Kim characterises the memory industry as entering a “de facto zero-supply phase” for new capacity, a framing that carries the full weight of the upgrade’s logic.

Three structural constraints underpin this view:

This contract structure mirrors the dynamics seen in semiconductor foundries such as TSMC, where customers commit to capacity years in advance. KB Securities views the shift as a valuation re-rating catalyst because it compresses earnings volatility and improves revenue visibility. AI data centre operators currently account for an estimated 70% of total memory shipment volumes, per KB Securities, and their willingness to lock in multi-year supply reflects how little spare capacity exists.

Investors wanting to understand the structural mechanics behind sold-out HBM capacity and what that means for pricing across the sector will find our full explainer on the HBM supply constraint driving memory repricing, which covers how manufacturing complexity, not capital investment alone, has locked out new supply through 2026-2027 and why a potential Samsung labour strike adds a further 3-4% DRAM supply risk on top of existing tightness.

Average selling prices (ASPs), the average price a chipmaker receives per unit of memory sold, are the primary earnings lever for memory producers. KB Securities’ 2026 projections for both companies sit well outside historical norms.

| Company | Product | 2026 ASP Change (YoY) | Source |

|---|---|---|---|

| SK Hynix | DRAM | +194% | KB Securities |

| SK Hynix | NAND | +244% | KB Securities |

| Samsung Electronics | DRAM | +297% | KB Securities |

| Samsung Electronics | NAND | +256% | KB Securities |

Samsung’s higher projected DRAM ASP gain (+297% versus SK Hynix’s +194%) may reflect a lower starting base or a deeper recovery from recent underperformance rather than structural outperformance in the product itself. The demand-side backdrop makes both projections directionally plausible: server DRAM reached an estimated 37.6% of 2023 total DRAM bit output, surpassing mobile DRAM at 36.8%, according to TrendForce/DRAMeXchange. That crossover marked the point where AI-driven server demand became the dominant force in memory pricing.

TrendForce DRAM market data published in May 2026 corroborates the direction of the server demand shift, with AI and hyperscaler procurement driving upward revisions to memory contract prices and next-generation HBM emerging as a primary revenue driver for leading chipmakers.

Whether gains of this magnitude materialise depends on the supply deficit holding as tightly as KB Securities projects. Readers weighing these numbers should treat them as scenario-dependent forecasts rather than consensus estimates.

The quarterly run-rate sets the context. KB Securities estimates SK Hynix’s Q2 2026 operating profit at 70 trillion KRW, representing more than an eightfold increase year-over-year.

That quarterly figure feeds into a full-year operating profit forecast of 277 trillion KRW, which, if realised, would rank SK Hynix fourth globally by that measure, per KB Securities.

The headline claim sits at the margin line.

KB Securities analyst Jeff Kim projects SK Hynix’s 2026 operating margin at 78.1%, a figure he characterises as the highest of any company worldwide.

The four key metrics in summary:

These figures are the direct financial outputs of the supply deficit and ASP thesis outlined above. For investors considering SK Hynix, the margin and global ranking claims provide a concrete benchmark against which to stress-test the bull case.

Combined 2026 capital expenditure from four major US cloud operators, including Alphabet and Amazon, is projected at $725 billion, a 77% year-over-year increase, according to KB Securities. The 2027 projection surpasses $1 trillion.

Jeff Kim characterises AI-related capital expenditure as having shifted from competitive expenditure to an “existential competitive requirement” for the world’s largest technology companies.

The spending is being pulled by consumption, not just pushed by corporate strategy. KB Securities projects:

Kim frames the next phase of demand as extending beyond cloud servers into on-device and physical AI use cases, a category he describes under the “agentic AI” label. The implication is that memory demand broadens even as the data centre buildout continues, compounding the supply deficit rather than allowing it to ease.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Three forward-looking catalysts will test the KB Securities thesis in the coming months:

Single-brokerage upgrade notes carry inherent concentration risk, particularly when ASP projections sit this far above broader market expectations. The specific figures in Kim’s note have not yet been echoed in open-web reporting from other sell-side houses, and investors should weigh them alongside consensus views as those emerge.

SK Hynix is the purer AI memory play. As the primary HBM3E supplier to NVIDIA, with capacity constrained by qualification and conversion timelines, its earnings leverage is concentrated in the highest-growth segment of the memory market.

Samsung’s upgrade reflects a recovery thesis layered onto its diversified semiconductor exposure. The higher projected DRAM ASP gain (+297%) may speak more to the depth of Samsung’s recent trough than to structural outperformance. Investors weighing both names are effectively choosing between a concentrated AI-memory bet and a broader semiconductor recovery story.

Asian semiconductor valuations present a structurally different picture from their US counterparts: as of early May 2026, SK Hynix and Samsung traded at a combined forward P/E of approximately 12x, roughly half the Nasdaq 100 multiple, despite earnings growth forecasts running nearly three times faster, a gap that the KB Securities upgrade argues reflects incomplete market pricing of the supply deficit rather than a genuine fundamental discount.

KB Securities’ call is not a cyclical one. The thesis rests on two mutually reinforcing forces: a supply deficit that cannot be resolved before 2027 and an AI demand acceleration that shows no sign of plateauing. If both hold, the earnings projections follow logically from the maths of constrained supply meeting surging willingness to pay.

The execution risks are real. Projections of this magnitude sit well beyond conventional forecasts, and the specific ASP and margin figures remain proprietary to a single brokerage note. The DRAM pricing data, quarterly earnings, and hyperscaler capex commentary identified above are the near-term validity tests. KB Securities’ own view is that AI-related investment will persist until adequate memory capacity and data centre infrastructure reach sufficient scale.

A Morningstar-identified capex-to-revenue lag of 18-24 months sits alongside the KB Securities bull case as the central bear-case counterargument, with Gartner estimating that only 20% of current AI agent pilots are scalable to production by 2027, a timeline that matters for whether the ASP and margin projections in Kim’s note materialise before hyperscaler spending discipline reasserts itself.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

High Bandwidth Memory (HBM) is an advanced type of DRAM stacked in layers specifically designed for AI processors. SK Hynix is the primary HBM3E supplier to NVIDIA, making its earnings heavily tied to AI data centre demand, and long qualification cycles for HBM limit near-term supply flexibility, supporting higher prices.

KB Securities analyst Jeff Kim set a price target of 3,000,000 KRW for SK Hynix (raised from 2,800,000 KRW) with a maintained Buy rating, and initiated a Buy upgrade on Samsung Electronics with a new price target of 450,000 KRW, both issued on 15 May 2026.

KB Securities identifies three structural constraints: no new greenfield memory manufacturing capacity is expected before 2027, HBM qualification cycles are lengthy and limit supply flexibility, and SK Hynix has shifted to multi-year advance-order contracts locking supply through 2028-2030, removing it from the spot market.

KB Securities projects combined 2026 capital expenditure from four major US cloud operators, including Alphabet and Amazon, at $725 billion, a 77% year-over-year increase, with the 2027 projection surpassing $1 trillion.

SK Hynix is considered the purer AI memory play, with earnings concentrated in the highest-growth HBM segment as the primary supplier to NVIDIA. Samsung's upgrade reflects a broader recovery thesis across diversified semiconductor exposure, with its higher projected DRAM ASP gain likely reflecting a recovery from a deeper recent trough rather than structural outperformance.