Brent Falls 3.3% as Trump Signals Imminent Iran Peace Deal

3 hrs ago

Samsung Electronics crossed $1 trillion in market capitalisation on 6 May 2026, becoming only the second Asian company in history to reach that threshold after Taiwan Semiconductor Manufacturing Company (TSMC). The milestone arrived at the intersection of a global AI infrastructure buildout, an acute shortage of high-bandwidth memory (HBM) chips, and a Bloomberg report that Apple held preliminary discussions with Samsung and Intel about processor manufacturing. Samsung’s shares have more than doubled year-to-date, a pace of appreciation that raises a question as important as the milestone itself: how much of this rally is structural, and how much is momentum that could reverse? What follows breaks down the three catalysts behind Samsung’s record run, places the milestone alongside TSMC’s own trillion-dollar moment, and maps the risks analysts say could unwind the gains.

Samsung reached approximately $1.037 trillion in market capitalisation on 6 May 2026, based on a share price of roughly 260,000 KRW and a single-day surge of 12-13%. The figure, equivalent to approximately 1,529 trillion KRW, places Samsung alongside a very short list of companies globally and marks the first time a Korean-listed company has carried a thirteen-digit dollar valuation.

Samsung’s shares have gained more than 100% year-to-date as of 6 May 2026, making it one of the fastest doublings among mega-cap technology stocks this cycle.

That doubling statistic is where the analytical tension sits. A 100% share price gain inside five months invites the question of whether price appreciation has outrun earnings growth. JPMorgan reportedly upgraded Samsung to “Overweight” around 5 May 2026, citing projected 2026-2027 earnings-per-share growth of approximately 35% to justify a forward price-to-earnings ratio of roughly 18x. The multiple is not extravagant by semiconductor standards, but the speed of the re-rating demands scrutiny of the catalysts underneath it.

High-bandwidth memory is a stacked DRAM architecture that delivers far greater data throughput than conventional memory. It sits alongside AI accelerator chips, such as Nvidia’s H100 and H200 series, and enables the volume of data movement required for large-scale model training and inference. Without HBM, the processors that power generative AI workloads cannot function at the speeds their designs require.

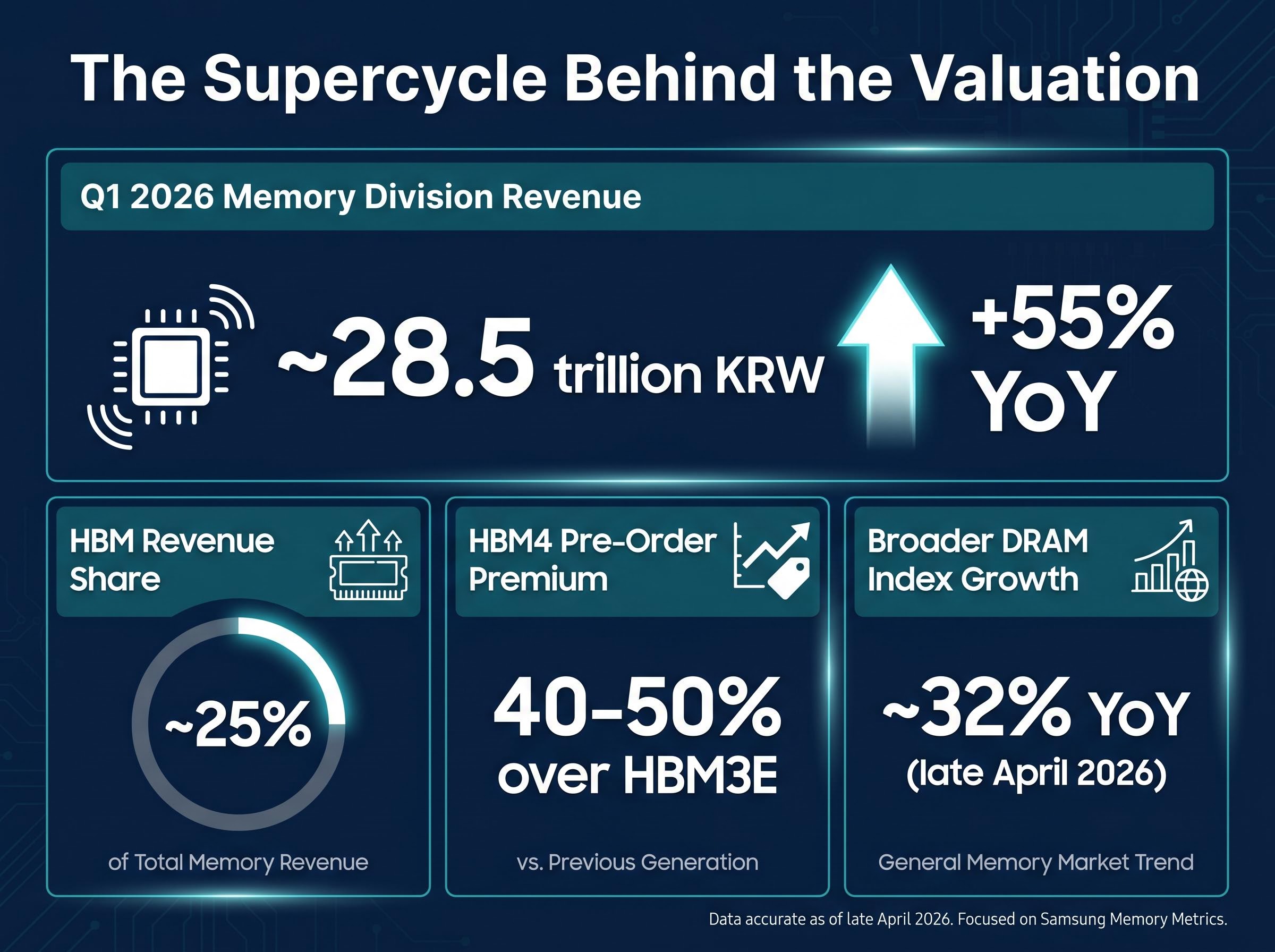

Supply constraints across the HBM market, not just Samsung’s output, have amplified pricing power industry-wide. HBM4 pre-orders were reported to carry a 40-50% premium over HBM3E pricing as of late April 2026, a signal that buyers are paying significantly more for next-generation capacity before it ships.

Samsung’s revenue exposure to this category is substantial:

These figures underpin the structural case for the rally. Without the HBM pricing and demand dynamic, the trillion-dollar milestone looks like pure momentum. With it, the revenue trajectory makes the valuation at least defensible.

Bloomberg reported in approximately late April 2026 that Apple held preliminary discussions with Samsung and Intel regarding processor manufacturing arrangements. No official confirmation or denial has emerged from any of the three companies.

Reuters characterised the Bloomberg report as “preliminary and unconfirmed” on 28 April 2026. The Financial Times reported no further developments as of 2 May 2026.

The gap between what was reported and how the market responded is instructive. A single Apple processor manufacturing contract would materially alter Samsung’s foundry revenue trajectory; Apple’s annual processor volume is among the largest in the industry, and any diversification away from TSMC would represent a structural shift in supply chain architecture.

The Apple chip supply chain talks broke on 5 May 2026 with asymmetric market reactions: Intel fell roughly 3.85% while Samsung surged, a divergence that reflects how investors priced execution risk at Intel’s unproven 18A node against Samsung’s Taylor, Texas facility that was approximately 90% mass production ready at the time.

That strategic logic explains why investors moved on the report despite its unconfirmed status. Samsung has the advanced foundry capacity that could theoretically accommodate Apple’s requirements, and the mere possibility of a contract at that scale changes the probability distribution around Samsung’s forward revenue. As of 6 May 2026, no confirmed financial terms, timelines, or official statements exist. The catalyst remains speculative, and investors should weigh it accordingly.

For investors wanting to assess the probability that preliminary discussions translate into contracted volume, our deep-dive into Apple’s foundry diversification strategy examines the three structural pressures driving Apple’s move, the manufacturing yield gaps Samsung and Intel must close, and TSMC’s 2nm exclusivity protection through the iPhone 18 cycle that limits near-term displacement.

The two companies reached the same number by very different paths. TSMC crossed $1 trillion on approximately 8 July 2024, fuelled by AI demand and strong Apple orders tied to the iPhone 16 cycle. Samsung arrived nearly two years later on the back of a memory chip supercycle and unconfirmed foundry speculation.

TSMC’s trillion-dollar crossing in July 2024 was driven by its position as the sole advanced-node supplier to both Apple and Nvidia, a concentrated customer dependency that gave it premium logic multiples Samsung’s more diversified business mix has never commanded.

| Metric | Samsung (6 May 2026) | TSMC (approx. 8 July 2024) |

|---|---|---|

| Market cap at milestone | ~$1.037 trillion | ~$1 trillion |

| YTD gain pre-milestone | ~100%+ | ~80-90% |

| Primary catalyst | HBM/AI memory demand | AI infrastructure + iPhone 16 |

| Forward P/E at milestone | ~18x | Mid-20s |

Samsung crossed at a lower forward P/E than TSMC, which suggests the market viewed Samsung’s earnings growth as more tangibly grounded at the time of the milestone. The difference also reflects the companies’ distinct business mixes: TSMC is a pure-play foundry commanding premium logic multiples, while Samsung’s conglomerate structure and lower HBM market share attract a structural discount.

Together, TSMC and Samsung now represent approximately 35% of global semiconductor market capitalisation. That concentration places enormous chip manufacturing value in Asia and amplifies the geopolitical supply chain risk discussions that have driven US reshoring policy for the past three years.

The Asian semiconductor valuation discount is a central feature of the current cycle: the MSCI AC Asia Pacific IT Index was trading at a forward P/E of approximately 12x as of early May 2026, roughly half the Nasdaq 100’s multiple, despite earnings growth forecasts running nearly three times faster than US peers, a gap that partly explains why the Kospi gained approximately 57% in the first four months of 2026 while the S&P 500 gained just 5.6%.

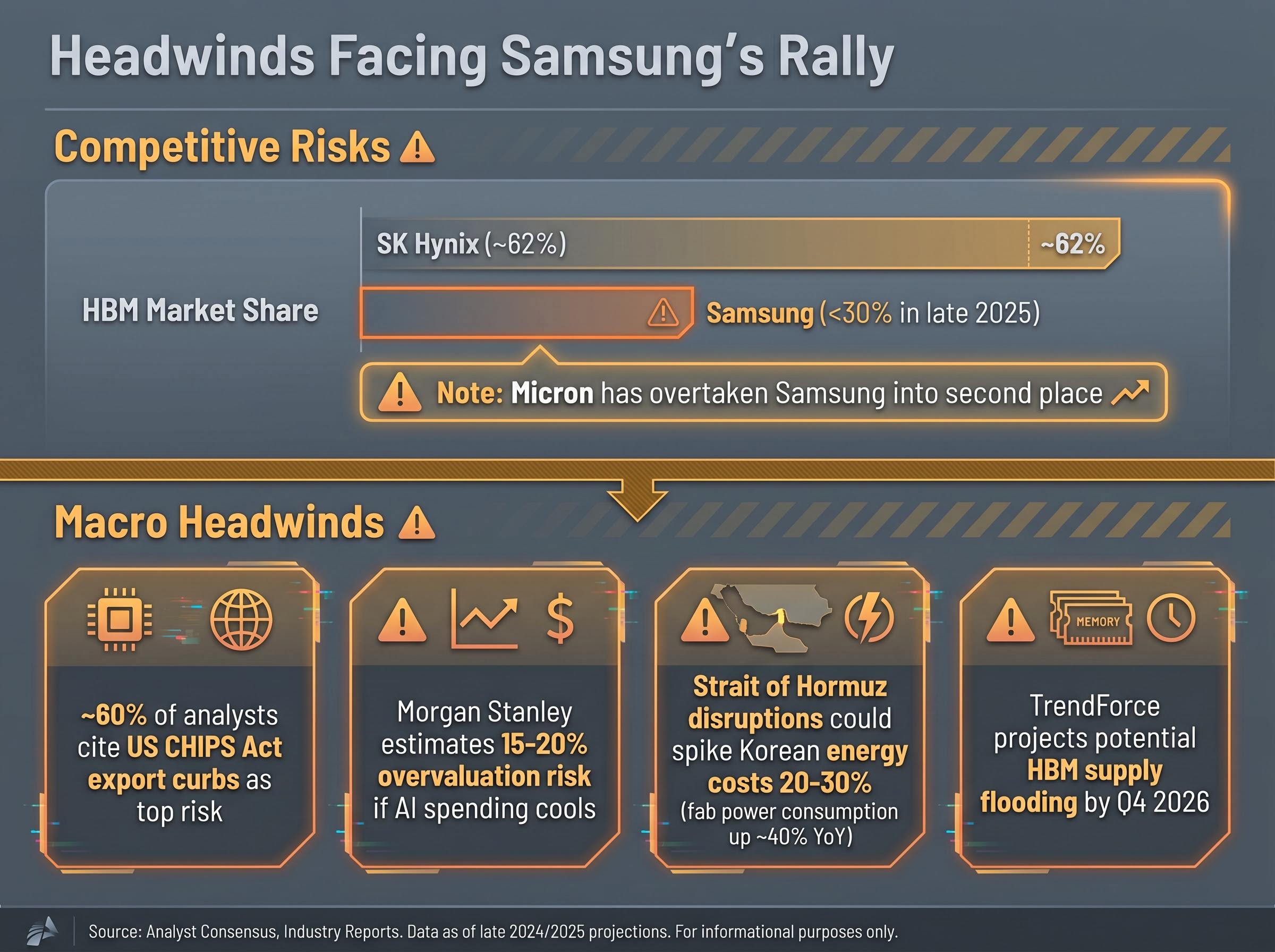

The competitive risks are specific and near-term. Samsung holds below 30% of the HBM market versus SK Hynix at approximately 62%, and Micron has overtaken Samsung into second place. SK Hynix leads on HBM3E and HBM4 yields, a gap Samsung can address but has not yet closed.

The macro risks are conditional but carry large consequences:

The distinction matters. Yield lag and market share are challenges Samsung can potentially address through execution. Export curbs, energy supply disruptions, and AI capital expenditure sentiment are external forces that no single company controls. Investors should be able to separate the two categories when assessing risk.

Investors tracking the downside case should read our full explainer on the AI hardware bubble thesis, which examines how escalating inference costs are making generative AI applications structurally unprofitable, why derivative markets appear to be underpricing the correction risk, and what 2027 capex guidance from Microsoft, Amazon, Alphabet, and Meta would constitute the clearest warning signal.

With TSMC and Samsung together at approximately 35% of global semiconductor market capitalisation, the centre of gravity in chip manufacturing and AI infrastructure value sits unambiguously in Asia, regardless of US reshoring policy ambitions. AMD’s Q1 2026 data centre revenue growth of 57% year-on-year confirms that AI chip demand is broad-based, not Samsung-specific.

The milestone arrived on a day when Strait of Hormuz tensions were easing, with Brent crude at approximately $108 per barrel (down 1.5% on the session), and US equity futures were climbing. That risk-on backdrop amplified the move.

Whether Samsung sustains this valuation depends on three conditional factors:

Approximately 70% of analysts rated Samsung “Buy” around the milestone date, according to aggregated consensus data.

The trillion-dollar crossing is a market verdict on where AI infrastructure value is concentrating globally. Understanding that verdict, and its fragility, is the context that matters for anyone tracking semiconductor stocks, supply chain policy, or the next phase of AI buildout.

Samsung crossed $1 trillion on the strength of a genuine structural driver (HBM demand from AI infrastructure) combined with a speculative catalyst (Apple processor talks) and a macro tailwind (easing Hormuz tensions). Each component carries a different degree of durability, and the share price reflects all three simultaneously.

The competitive reality is clear. Samsung is not the HBM market leader; SK Hynix holds the dominant position at approximately 62% share, and Samsung’s valuation depends on closing the yield gap in advanced memory nodes. The longer-term signal may be the most consequential: two trillion-dollar chipmakers now sit in Asia, concentrating semiconductor value in a region subject to distinct geopolitical pressures.

Investors tracking Samsung’s trajectory from here should monitor HBM4 yield progress, the status of the Apple processor discussions as they develop, and the broader trajectory of AI infrastructure capital expenditure. These are the indicators that will determine whether the milestone holds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

High-bandwidth memory is a stacked DRAM architecture that delivers far greater data throughput than conventional memory, sitting alongside AI accelerator chips like Nvidia's H100 and H200 to enable large-scale model training. Samsung's memory division generated approximately 28.5 trillion KRW in Q1 2026 revenue, up roughly 55% year-on-year, with HBM accounting for about 25% of that figure.

Samsung reached approximately $1.037 trillion in market capitalisation on 6 May 2026, based on a share price of roughly 260,000 KRW and a single-day surge of 12-13%, driven by AI infrastructure demand for HBM chips, a Bloomberg report on preliminary Apple processor discussions, and easing geopolitical tensions in the Strait of Hormuz.

TSMC crossed $1 trillion in approximately July 2024 on the back of AI demand and iPhone 16 orders, trading at a forward P/E in the mid-20s, while Samsung crossed at a lower forward P/E of roughly 18x in May 2026, reflecting its more diversified conglomerate structure and smaller share of the advanced HBM market.

The key risks include Samsung's below-30% HBM market share versus SK Hynix's roughly 62%, potential US CHIPS Act export curbs flagged by approximately 60% of analysts as the top geopolitical risk, a possible HBM supply glut projected by TrendForce for Q4 2026, and Morgan Stanley's estimate of 15-20% overvaluation risk if AI spending sentiment cools.

Bloomberg reported that Apple held preliminary discussions with Samsung and Intel about processor manufacturing arrangements, but as of 6 May 2026 no official confirmation, financial terms, or timelines had been announced by any of the three companies, meaning the catalyst remains speculative.