Kevin Warsh takes the oath as Federal Reserve Chair today, 22 May 2026, stepping into an institution already mid-argument about its own direction. Brent crude sits at roughly $105 a barrel. The Strait of Hormuz is effectively closed. The federal funds rate is parked at 3.50%-3.75% after the April meeting held it steady, and the committee that set that rate is, by its own minutes, more internally divided on the path forward than at any point in recent memory. Warsh is not inheriting a blank slate; he is inheriting a debate. What follows is an assessment of what his monetary policy instincts mean for the interest rate path, how his leadership differs from Jerome Powell’s, what historical Fed transitions reveal about near-term market behaviour, and what U.S. investors should be tracking in the months ahead.

The Fed Warsh inherits: a divided committee and an inflation problem that won’t wait

The 29-30 April 2026 FOMC meeting, likely Jerome Powell’s final as Chair, produced a hold at 3.50%-3.75% and no change to forward guidance. But the minutes told a more fractured story than the headline decision suggested.

Three findings from the April minutes stand out:

The April 2026 FOMC minutes confirm that almost all participants cited Middle East energy risks as a driver of upside inflation risk, and that many favoured removing the easing bias language from the post-meeting statement, producing a documented internal record of hawkish drift that Warsh now inherits as the committee’s working consensus.

- The “vast majority” of participants judged that inflation could take longer than previously expected to return to 2%, citing geopolitical risks, tariffs, and energy cost pass-through.

- “Many participants” indicated they would have preferred removing the language suggesting an easing bias from the post-meeting statement.

- “Almost all participants” cited Middle East energy risks explicitly as a driver of upside inflation risk.

The divide is not subtle. TD Economics, analysing the minutes on 20 May 2026, characterised the shift directly:

The FOMC dissents in April numbered four, the most at any single Fed meeting since 1992, with one member favouring an immediate cut and three opposing the retention of any easing bias language, a split that makes Warsh’s consensus-building task considerably harder than a unified committee would.

“A clear shift toward a more two-sided or hawkish stance… one where participants disagree on the appropriate stance of policy to a wider extent than has been the case recently.”

Warsh steps into this environment not as a disruptor, but as a figure whose own instincts align with the committee’s pre-existing hawkish drift. The question is whether he accelerates it.

When big ASX news breaks, our subscribers know first

Who is Kevin Warsh and how does he think about inflation?

Kevin Warsh, 56, was confirmed by the Senate on 13 May 2026. His path to the Fed Chair is unusual in its directness: Morgan Stanley, then appointment as a Fed governor in 2006, service through the worst of the financial crisis, and a departure in 2011 that was followed by more than a decade of public commentary on what the Fed was getting wrong.

His scepticism of prolonged easy monetary policy is not campaign positioning. It is an on-record philosophical stance developed across years of internal dissent and external critique.

From crisis-era governor to inflation hawk: the policy record that shaped his nomination

During his tenure as a Fed governor from 2006 to 2011, Warsh dissented from the post-crisis expansion of quantitative easing programmes. He called for earlier normalisation at a time when the consensus favoured extending accommodation. The Wall Street Journal, profiling his nomination in March 2026, noted that market expectations implied “a higher terminal rate than under Powell, all else equal,” precisely because of this record.

His core rate view, reported by Bloomberg in March 2026, holds that the neutral rate is structurally higher than the pre-pandemic consensus. This shapes his resistance to near-term easing and his caution about pre-signalling cuts. CNBC and Barron’s characterised him in their nomination analyses as “more hawkish on inflation than Powell,” a description rooted in his prior Fed record rather than speculation about future behaviour.

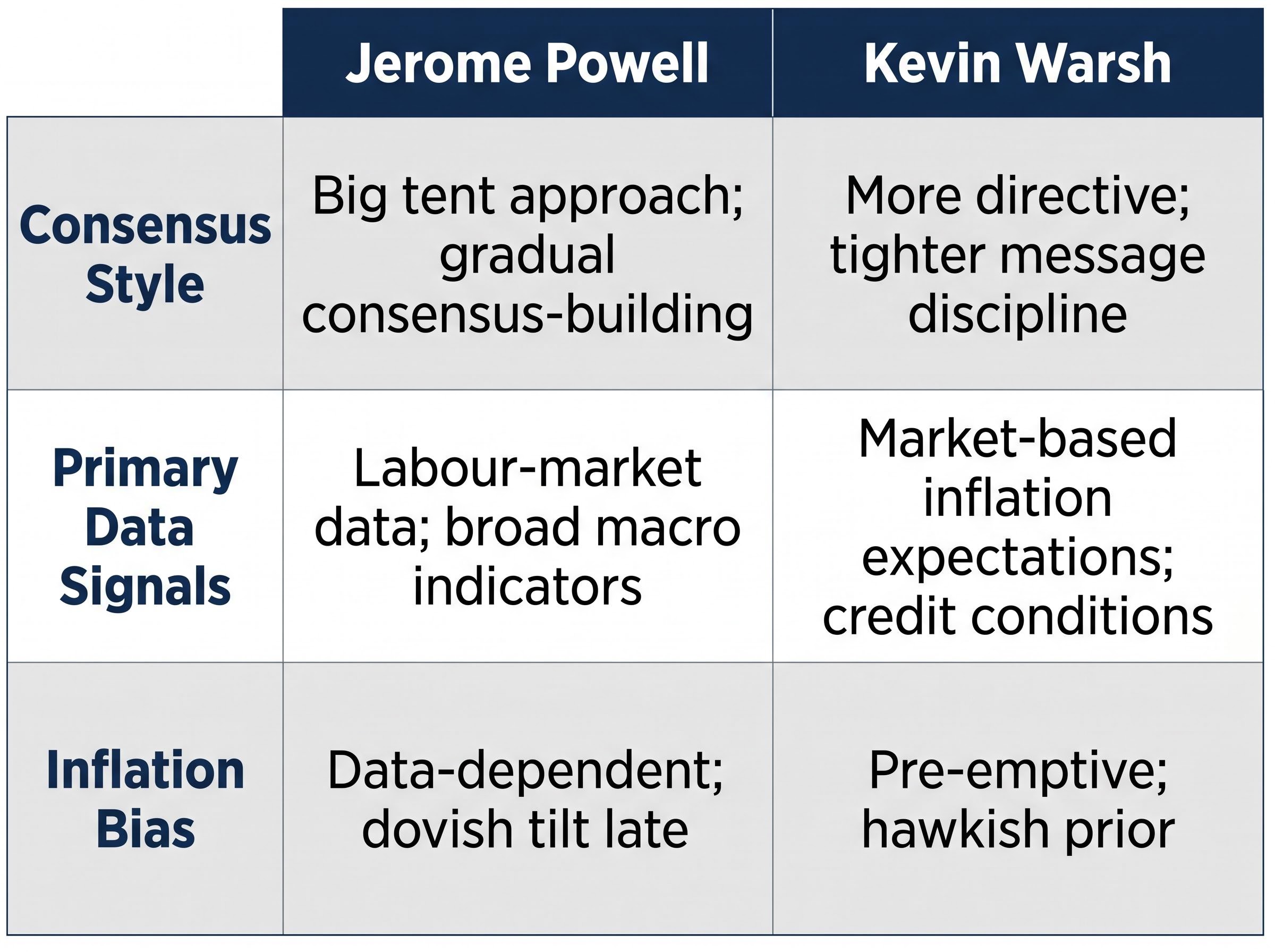

How Warsh differs from Powell: style, signals, and the market’s reaction function

The contrast between Powell and Warsh is not one of competence or commitment. It is a difference in operating system, and it matters for how investors read Fed signals.

| Dimension | Powell | Warsh |

|---|---|---|

| Consensus style | “Big tent” approach; tolerant of wide range of public speeches; gradual consensus-building | More directive; smaller inner circle; tighter message discipline |

| Primary data signals weighted | Labour-market data; broad array of macro indicators | Market-based inflation expectations; credit conditions; financial-market signals |

| Independence framing | Publicly framed disagreements with the White House as institutional battles | Pledges to “jealously guard” independence; less confrontational, more diplomatic tone |

| Inflation bias | Data-dependent; patient on rate action; dovish tilt in later tenure | Pre-emptive on inflation risk; higher neutral rate view; hawkish prior |

Bloomberg and the Financial Times reported in March 2026 that former Fed staffers described Warsh as “more directive, less consensus-driven” than Powell. CNBC added that strategists expect more weight on market-based inflation expectations in Warsh’s reaction function. Reuters, covering his Senate confirmation hearing in April 2026, reported his pledge to “jealously guard the Fed’s independence,” while the FT characterised his approach as “less confrontational, more diplomatic” without suggesting any softening of formal autonomy.

The shift in what data the Fed Chair watches most closely is not cosmetic. Investors who calibrate positions around labour-market releases may need to add market-based inflation expectations and credit spreads to their primary signal set.

The structural limits on Fed chair authority, including the 12-member voting committee, codified 2% inflation target, and Powell’s retained board vote through early 2028, mean that Warsh’s personal hawkish instincts face institutional friction that could slow any sharp policy pivot regardless of his individual preferences.

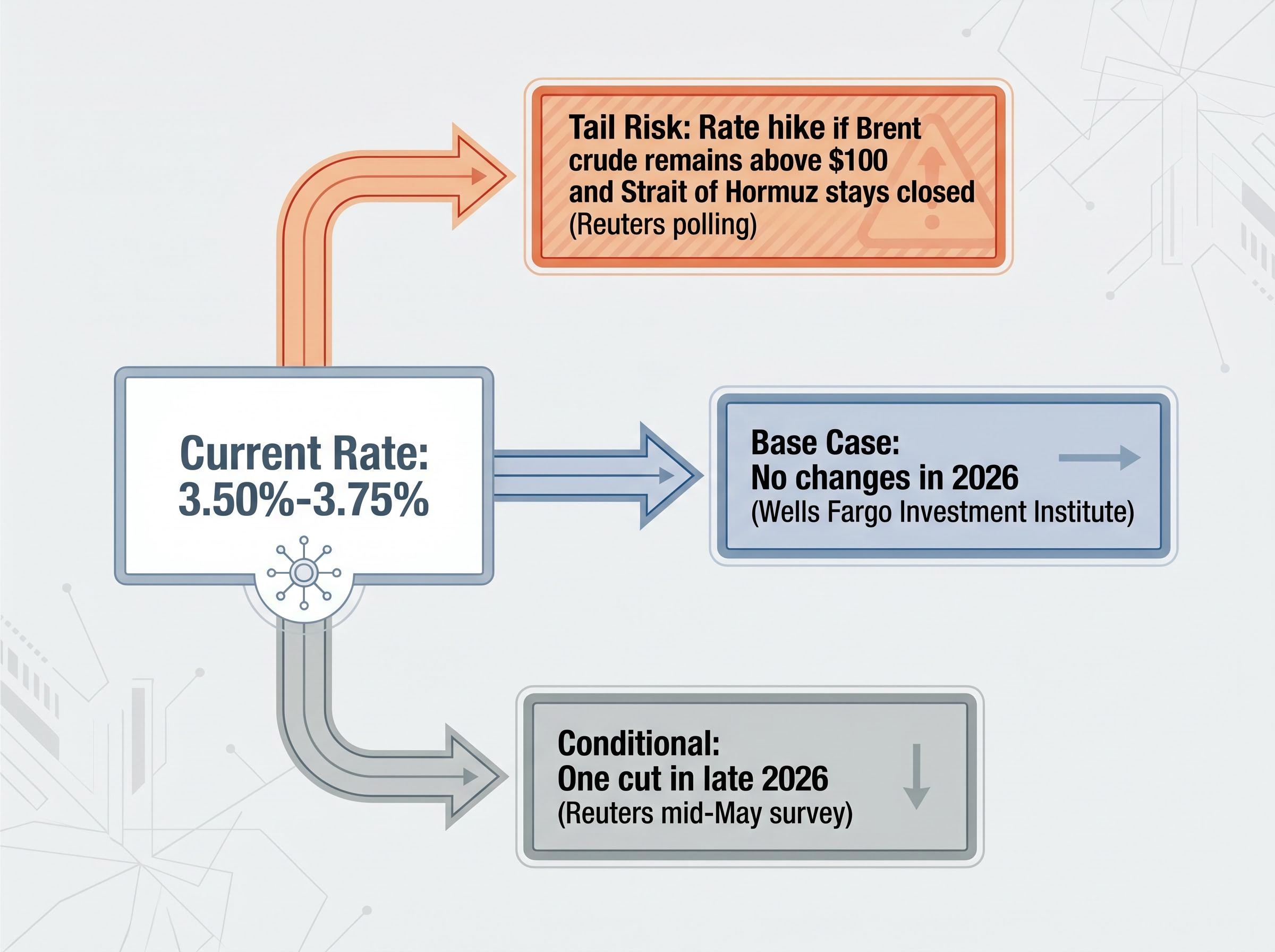

What the rate path looks like under Warsh, and what could change it

The analyst consensus is converging on a baseline that would have seemed unlikely 12 months ago: rates going nowhere, and possibly going up.

- No changes in 2026 (base case). Wells Fargo Investment Institute projects no federal funds rate changes this year, citing the elevated geopolitical environment and growing internal opposition to an easing bias.

- One cut in late 2026 (conditional). A Reuters primary dealer survey from mid-May found a majority expecting fewer and later cuts than they had anticipated under Powell. A single late-year cut remains possible if inflation progress resumes and energy prices moderate.

- Rate hike (tail risk, but non-trivial). Reuters polling flagged a non-trivial probability of a rate increase if Brent crude remains above $100 and the Strait of Hormuz stays closed. This scenario, which would have been dismissed six months ago, is now in the distribution.

“The bar for cuts has moved higher, and the Fed appears prepared to wait longer, or potentially tighten policy, if inflation does not convincingly return toward target.”

TD Economics, 20 May 2026

The logic of the two-sided reaction function is now embedded in both the April minutes and Warsh’s own prior views. Cuts require convincing disinflationary progress. Hikes are back on the table if energy prices become embedded in expectations. The gap between scenario one and scenario three is meaningful for bond duration, equity valuations, and commodity positioning.

History’s guide: what past Fed transitions tell investors about the next 12 months

Three prior transitions offer pattern recognition for the current moment.

| Transition | Year | Market characterisation | Investor lesson |

|---|---|---|---|

| Greenspan to Bernanke | 2006 | Bond and equity volatility as markets recalibrated to inflation-targeting approach | New reaction functions take time to price; expect recalibration volatility |

| Bernanke to Yellen | 2014 | Dovish handoff; relatively benign market performance | Continuity transitions produce less repricing than regime shifts |

| Yellen to Powell | 2018 | Communication shift; early-term volatility as markets reassessed drawdown tolerance | Even modest style changes can drive short-term dislocation |

| Powell to Warsh (current) | 2026 | Hawkish shift amid active supply shock (analyst positioning, not historical record) | A hawkish-leaning transition during an inflation episode may amplify repricing |

The Warsh transition is not a Bernanke-to-Yellen handoff. It is a hawkish shift relative to Powell’s late-tenure stance, arriving in the middle of a supply shock that the committee has already flagged as its primary inflation risk. Across Financial Times, Wall Street Journal, and Bloomberg analyses from March 2026, three patterns hold: short-term volatility is typical around leadership changes; macro fundamentals dominate over 6-12 months more than the identity of the Chair; and the biggest repricings occur when a new Chair is perceived as significantly more hawkish or dovish than anticipated.

Warsh is being positioned by analysts as moderately more hawkish than late-Powell expectations. The supply shock amplifies that positioning.

What investors should watch now that Warsh holds the chair

The leadership change converts into a concrete monitoring framework. Five signals will tell investors whether the hawkish baseline is holding or shifting:

- Brent crude trajectory relative to the $100 threshold. This is the single largest variable determining whether the hike scenario becomes material. A sustained move below $100 eases the committee’s inflation anxiety. Persistence above it keeps the tightening option live.

- Strait of Hormuz reopening timeline. The closure duration shapes the permanence of the energy shock and the degree to which it embeds in broader price expectations.

- Short-dated Treasury yield direction. Rising short-dated yields signal reduced cut probability; a reversal would indicate the market is pricing in faster resolution of the energy shock than the Fed’s own language suggests.

- Warsh’s first FOMC press conference tone on easing bias. Whether he retains, removes, or softens the easing language will be the earliest direct signal of his policy intentions.

- Financial sector versus growth equity relative performance. Bank and financial stocks outperformed on Warsh’s confirmation day, according to CNBC and Bloomberg. Continued outperformance would indicate the market is pricing in a sustained higher-for-longer rate environment.

Short-dated Treasury yields rose on reduced near-term cut probability following Warsh’s confirmation, per Reuters. Dollar firmness and tighter financial conditions have reinforced this trend, with Bloomberg and CNBC framing Warsh’s expected hawkish bias as a supporting factor. Powell’s continued presence as a Fed governor through early 2028 preserves some institutional continuity at the board level, reducing the risk of abrupt communication breakdowns during the transition.

For investors trying to model which rate scenario becomes most likely, our full explainer on Hormuz oil price scenarios maps Goldman Sachs, JPMorgan, and EIA projections across reopening and prolonged-closure cases through 2027, with Goldman assigning only a 55% probability to normalisation by mid-June and projecting $110-$142 per barrel under a sustained disruption.

A hawkish Fed at a hawkish moment: the transition that may define 2026 markets

Warsh arrives at a moment when the Fed’s own internal momentum was already shifting hawkish. His personal philosophy amplifies rather than contradicts that drift. The April minutes documented the division; Warsh’s record suggests he sits comfortably on the side that wanted to remove the easing bias entirely.

Genuine uncertainty remains. No one knows whether the Iran conflict resolves, whether energy prices moderate, or whether Warsh surprises markets with a more flexible approach once he faces his first live policy decision. The macro data may force a more nuanced hand than his reputation suggests.

Hormuz risk premium persistence is likely to extend well beyond any ceasefire announcement, given that commercial war-risk insurance has effectively withdrawn from the strait and the IEA projects a two-year supply chain recovery timeline even under a best-case resolution scenario, a structural consideration that keeps the tail-risk hike scenario in the probability distribution for longer than a simple reopening headline would suggest.

The first Warsh-era FOMC meeting will be the earliest real test. Until then, the baseline that Wells Fargo has articulated, no federal funds rate changes in 2026, remains the cleanest encapsulation of the consensus heading into this new chapter of Fed leadership.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding rate paths and market reactions are speculative and subject to change based on market developments and evolving geopolitical conditions.