Foxconn Beats Q2 Estimates by 6% as AI Server Demand Surges

15 hrs ago

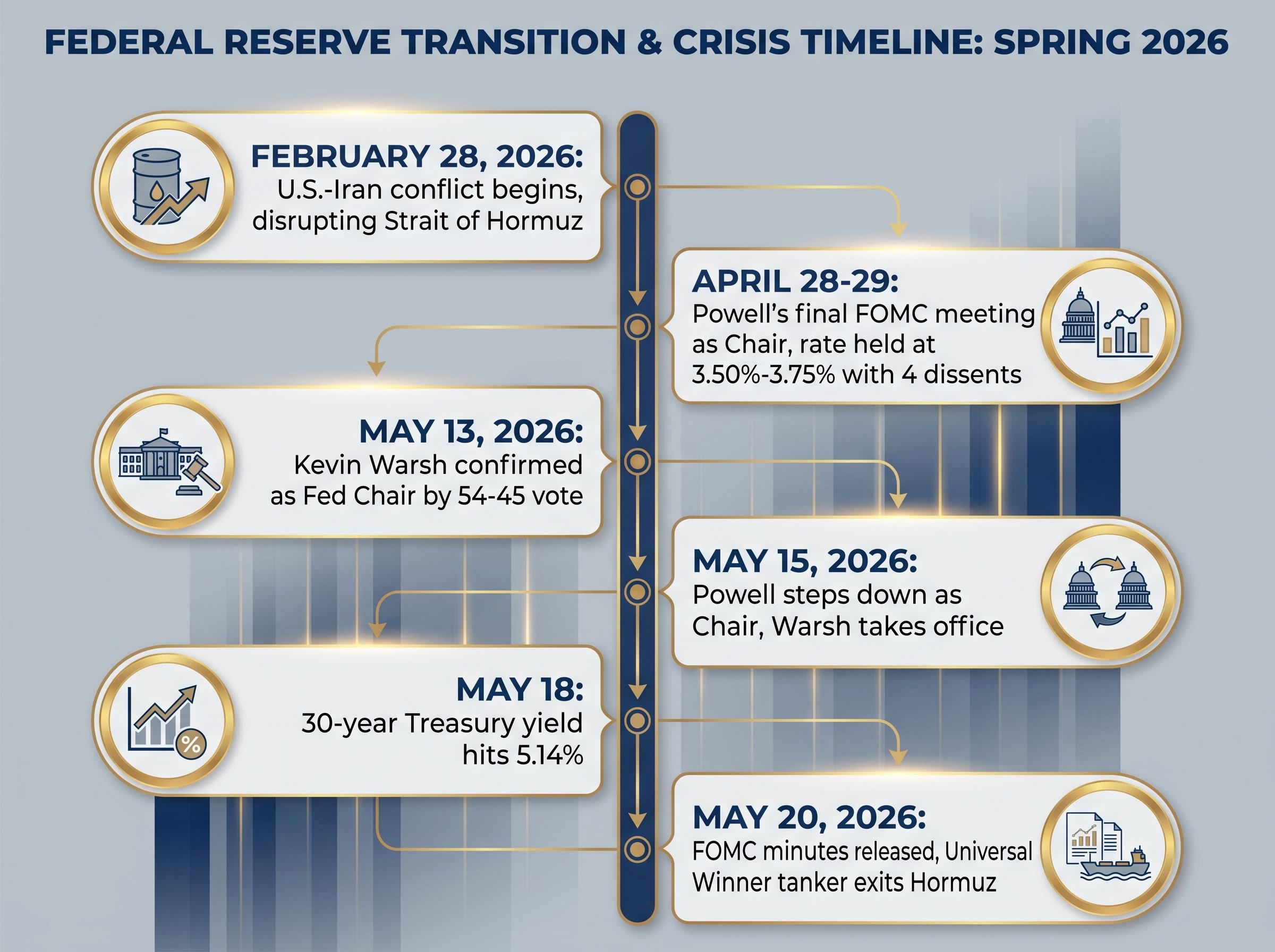

Four Federal Reserve policymakers voted against the majority at the April 28-29 FOMC meeting, producing the most dissents at a single Fed meeting since 1992 and exposing fractures inside the institution on the day Jerome Powell chaired his final meeting as head of the central bank. The minutes from that meeting were released today, 20 May 2026, arriving at a moment when the Fed is simultaneously navigating a U.S.-Iran conflict that has pushed 30-year Treasury yields to their highest level since 2007, a narrow and politically charged leadership transition, and an active Trump administration pressure campaign that has reached the Supreme Court. What follows is an account of what the April minutes reveal about internal divisions over rate guidance, why Powell is staying on the Board of Governors through 2028, and what the policy and institutional landscape looks like for incoming Chair Kevin Warsh.

The sharpest signal from today’s release is not the rate decision itself. It is the dissent count.

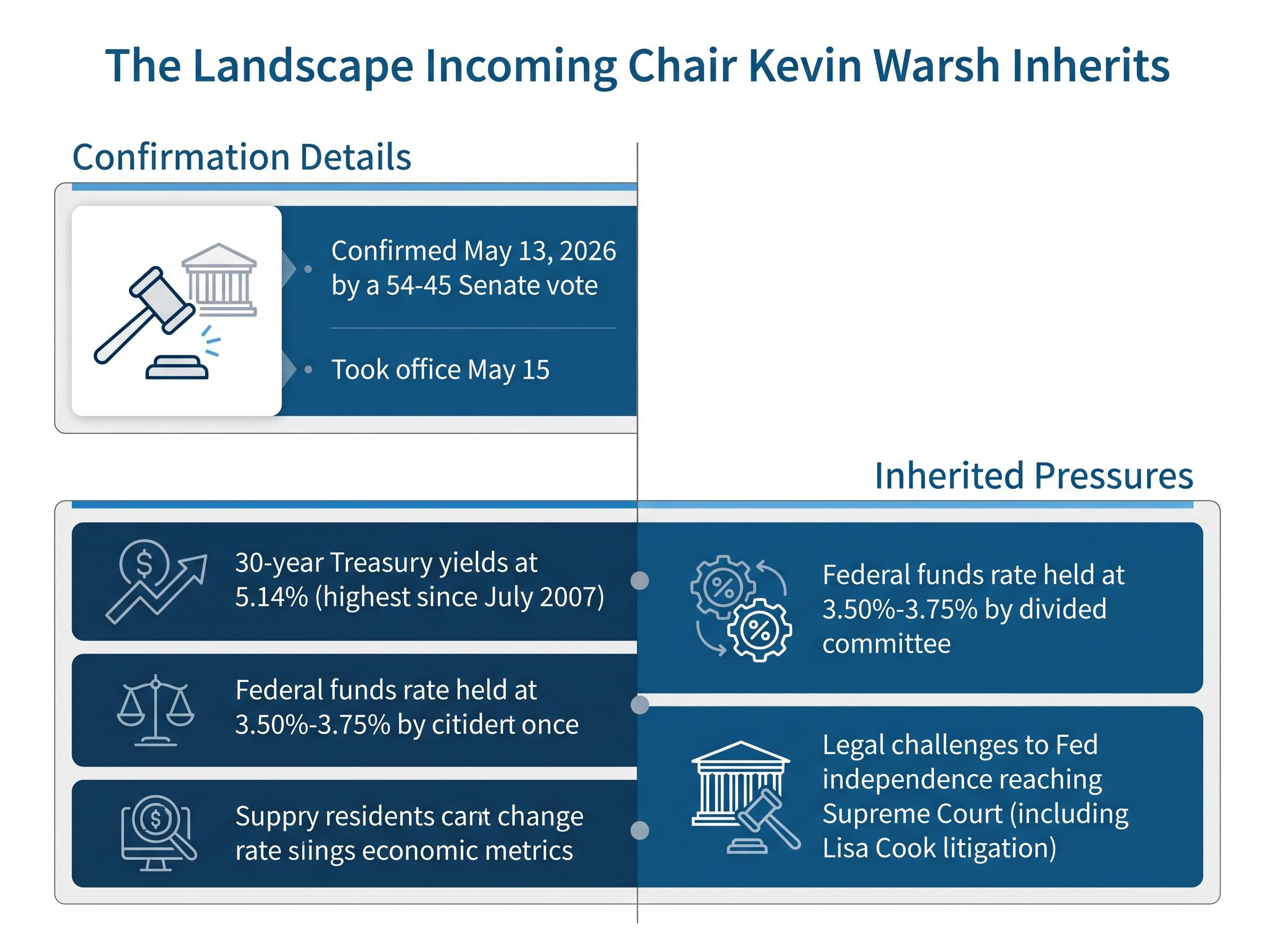

The April 29 rate decision held the federal funds rate at 3.50%-3.75% against a backdrop of PCE inflation running at 3.5% and unemployment rising to 4.3%, a dual-mandate conflict that gave each faction on the committee genuine grounds for its position.

The four dissents represent the highest number of opposing votes recorded at any single FOMC meeting since 1992, a span covering the global financial crisis, the pandemic response, and the fastest tightening cycle in a generation.

The St. Louis Fed history of FOMC dissents, which tracks every opposing vote recorded at committee meetings since the modern FOMC structure was established, places the April 2026 count in a lineage of contested decisions that includes the stagflation-era battles of the 1970s and the post-crisis rate debates of the early 2010s.

What dissent means in practice is straightforward: individual committee members publicly disagreed with the majority’s policy statement. The fault line, as the minutes describe it, ran through the question of forward guidance. One faction favoured continuing to signal future rate reductions; the other pressed for a more cautious, data-dependent posture that would strip out any implicit easing bias until the geopolitical picture clarified.

A committee divided four ways on guidance is not a committee that can communicate a predictable rate path. For markets pricing the next move, that ambiguity is itself the message.

The Strait of Hormuz is the world’s most significant oil chokepoint, and the U.S.-Iran conflict that began on 28 February 2026 effectively closed it to commercial tanker traffic, producing a supply shock that rippled directly into the inflation data the FOMC was evaluating in late April.

The yield response was immediate and persistent. Long-end Treasury rates absorbed both the energy-price inflation expectations and a broader geopolitical risk premium that repriced the cost of holding long-duration U.S. debt.

| Indicator | Value | Context |

|---|---|---|

| 30-year Treasury yield (18 May) | 5.14% (FRED DGS30) | Highest since July 2007 |

| Intraday highs (mid-May) | ~5.17%-5.19% | Pre-financial-crisis territory |

| Conflict onset | 28 February 2026 | Strait of Hormuz disrupted |

Yields at levels not seen since before the 2008 financial crisis represent a tightening of financial conditions that operates independently of the Fed’s own rate decisions, complicating the committee’s ability to calibrate policy through conventional tools.

The 30-year Treasury yield dynamics driving this tightening reflect more than a single geopolitical shock: the Moody’s sovereign downgrade, heavy Treasury supply, and a structural term-premium repricing have each contributed to a move that pushed yields briefly above 5.19% intraday on 19 May 2026 and introduced a 5.25% threshold that strategists cite as an institutional allocator inflection point.

Diplomatic movement emerged today. President Trump stated the conflict could conclude rapidly and disclosed that offensive actions had been delayed following requests from Gulf nations. Vice President Vance indicated that Iran had expressed willingness to negotiate.

Shipping data supported the shift: two Chinese-flagged supertankers and a South Korean-flagged VLCC, the Universal Winner, exited the Strait of Hormuz on 20 May, according to LSEG and Kpler tracking data. Oil prices declined on the optimism, though Brent crude remained substantially above pre-conflict levels.

If Hormuz tensions ease, the energy-price inflation component weighing on FOMC deliberations would diminish. The April minutes, however, reflect conditions as they stood in late April, when the disruption was fully active and unresolved.

Federal Open Market Committee minutes are the detailed record of the committee’s internal deliberations at each scheduled meeting, published on a roughly three-week lag after the meeting date. The April minutes were released today at federalreserve.gov, consistent with that standard timeline.

What the minutes typically contain, in order:

The post-meeting policy statement, released immediately after each decision, is a consensus document that compresses disagreement into carefully negotiated language. The minutes reveal what the statement conceals: the scale of disagreement, the specific arguments advanced by dissenters, and the reasoning behind the final language choices.

These particular minutes carry weight beyond the standard release. They are the final minutes from Powell’s chairmanship, they contain four dissenting votes that each require explanation, and they were drafted against the backdrop of active political pressure on the institution itself.

Powell stepped down as chair on 15 May 2026, but he did not leave the Federal Reserve. He remains on the Board of Governors through at least early 2028 and was designated chair pro tempore during the transition period.

The decision to stay is not procedural. It is a response to a specific set of institutional threats. The Trump administration’s pressure campaign against the Fed has included attempts to remove Governor Lisa Cook through litigation, subpoenas directed at Fed-related matters that were subsequently blocked by courts, and public demands for lower interest rates made directly by administration officials.

That campaign has now escalated to the Supreme Court, marking the most direct legal challenge to central bank operational independence in decades.

Powell’s continued presence on the Board preserves a vote and a voice from the pre-Warsh era at a moment when the institution’s independence faces simultaneous pressure from the executive branch, the courts, and the incoming leadership transition. For bond markets, the question of Fed independence is not abstract: a central bank perceived as subject to political direction loses credibility as an inflation anchor, with direct consequences for yields, currency valuations, and long-term rate expectations.

Brookings research on central bank independence and inflation credibility finds that perceived erosion of institutional autonomy feeds directly into long-run inflation expectations, providing an academic basis for the market concern that a Fed seen as politically directed would lose its anchor function in bond pricing.

Warsh was confirmed by a Senate vote of 54-45 on 13 May 2026, the narrowest confirmation margin in modern history for a Fed chair. He took office after Powell’s departure on 15 May.

Warsh’s confirmation committed him publicly to aggressively reducing the Fed’s 6.7 trillion dollar balance sheet through accelerated quantitative tightening, a pledge that, if executed alongside a prolonged rate hold, would tighten financial conditions through two channels simultaneously and push long-term Treasury yields higher independent of any rate decision.

The vote margin itself carried a signal. It reflected the degree of institutional and market anxiety about whether the incoming chair, nominated by an administration actively pressuring the Fed, would maintain the operational distance from the White House that gives rate decisions their credibility.

Warsh is known for advocating a more rule-based, market-signal-responsive approach to monetary policy, generally considered more hawkish than the Powell-era consensus. Where Powell’s committee operated with judgment-based flexibility, adjusting forward guidance to balance competing risks, a rule-based framework would anchor decisions more tightly to observable data and pre-committed criteria.

That hawkish lean may align with the dissenting bloc from the April meeting, or it may reconfigure the committee’s internal dynamics in ways the minutes do not yet reflect. The open questions facing Warsh are specific and simultaneous:

The April minutes are a snapshot of an institution under pressure from every direction at once. Geopolitical inflation from the Strait of Hormuz disruption, a four-dissent split over rate guidance, and a legal-political campaign testing the boundaries of central bank independence all converged in the final weeks of Powell’s chairmanship.

Warsh’s first FOMC meeting will be the next significant test of how these pressures interact under new leadership. Today’s release gives markets the clearest picture yet of the committee’s internal state at the moment of transition: a 3.50%-3.75% rate held by a divided committee, with 30-year yields at 5.14% and a new chair confirmed by a margin of 54-45.

What to watch from here:

The full minutes text is available today at federalreserve.gov.

For readers wanting to translate the yield environment into specific portfolio decisions, our full explainer on 30-year yield thresholds and investor positioning covers Bank of America’s 5.25% structural inflection framework, the historical precedents from Japan, the US, and China where yield spikes of this magnitude preceded major market cycle turns, and Hartnett’s preferred sector positioning under a sustained elevated-yield regime.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding monetary policy, geopolitical developments, and market conditions are subject to change based on evolving circumstances.

Federal Reserve minutes are the detailed record of the FOMC's internal deliberations at each scheduled meeting, published on a roughly three-week lag after the meeting date. They reveal the scale of disagreement, specific arguments from dissenters, and the reasoning behind forward guidance language that the official post-meeting statement compresses.

Four FOMC members dissented at the April 28-29, 2026 meeting, the highest number of opposing votes at any single FOMC meeting since 1992, covering a period that includes the global financial crisis, the pandemic response, and the fastest tightening cycle in a generation.

The 30-year Treasury yield reached 5.14% on May 18, 2026, its highest level since July 2007, driven by a combination of energy-price inflation expectations from the U.S.-Iran conflict disrupting the Strait of Hormuz, the Moody's sovereign downgrade, heavy Treasury supply, and a structural term-premium repricing.

Powell remained on the Board of Governors through at least early 2028 in response to specific institutional threats, including the Trump administration's attempts to remove Governor Lisa Cook through litigation, court-blocked subpoenas, and an active legal campaign that has escalated to the Supreme Court challenging central bank independence.

Warsh is known for advocating a more rule-based, market-signal-responsive approach to monetary policy, generally considered more hawkish than the Powell-era consensus, and publicly committed to aggressively reducing the Fed's 6.7 trillion dollar balance sheet through accelerated quantitative tightening.