ANZ Posts 70% Cash Profit Surge in Half-Year Results

48 mins ago

On 30 April 2026, the S&P 500 closed at 7,209, capping its strongest monthly gain since November 2020. The catalyst was not a single company or a single earnings beat. It was a synchronised declaration from four of the world’s largest technology companies that, collectively, they plan to spend more than $650 billion on artificial intelligence infrastructure in 2026 alone. Alphabet, Amazon, Meta, and Microsoft each reported Q1 results within days of one another, and each confirmed that the AI buildout is accelerating rather than plateauing. Yet the market’s response was selectively sharp: not all AI spenders were rewarded equally. What follows is a breakdown of what each company reported, why Wall Street punished some despite strong headline numbers, and what the $650 billion commitment signals for investors tracking the AI capital expenditure cycle in real time.

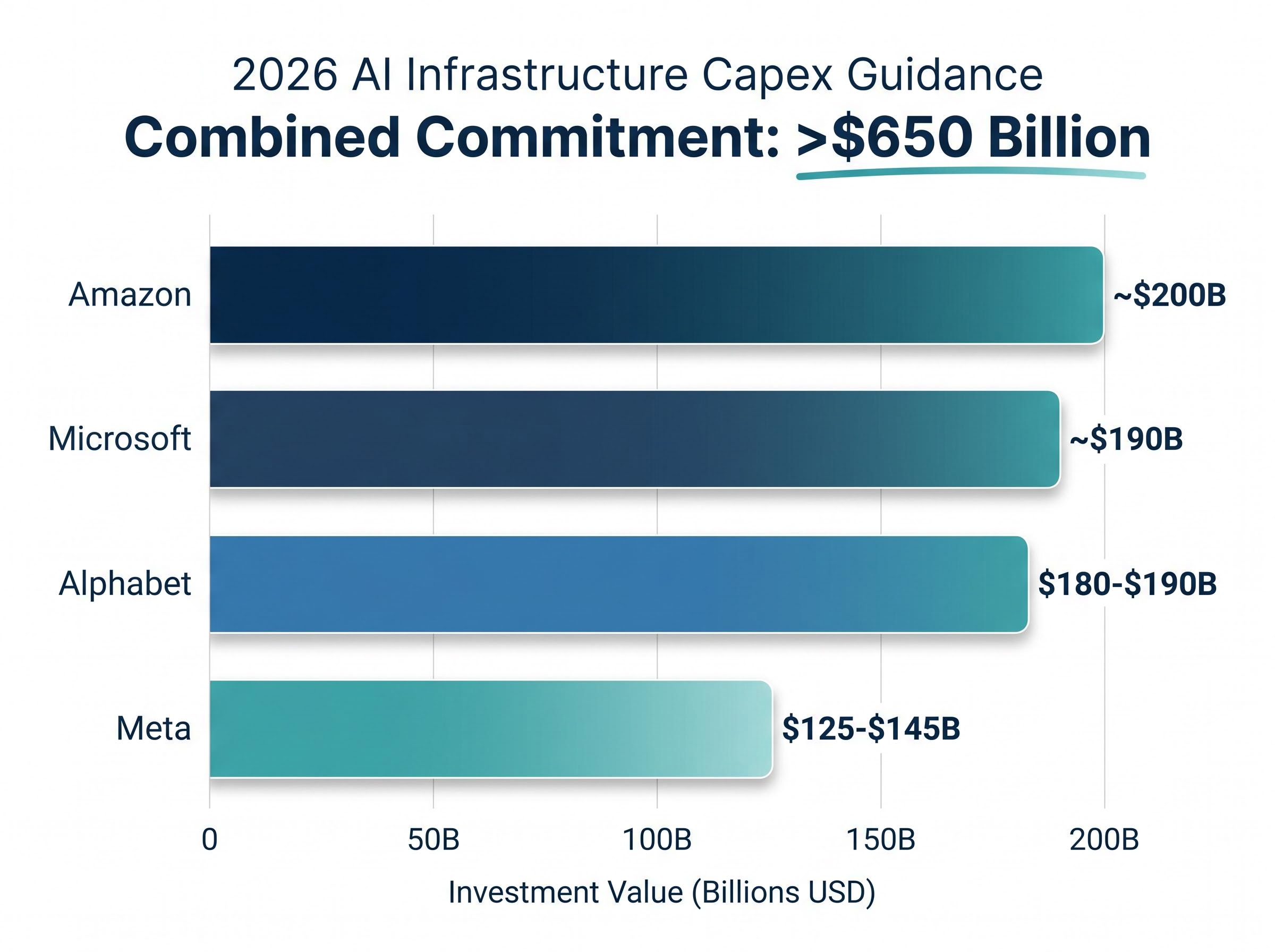

The aggregate figure is not a projection. It is the sum of guidance-level commitments made or confirmed on Q1 2026 earnings calls across four companies, each individually spending at a scale that would rank among the largest corporate capital programmes in history.

Alphabet raised its 2026 capital expenditure guidance to $180-$190 billion, after reporting Q1 capex of $35.7 billion, a 107% year-over-year increase. Amazon CEO Andy Jassy committed to approximately $200 billion in 2026 spending. Meta lifted its guidance range to $125-$145 billion, up from a prior range of $115-$135 billion, citing higher component costs and expanded data centre construction. Microsoft indicated fiscal-year capex is expected to reach approximately $190 billion.

Combined, these four commitments exceed $650 billion, a figure that surpasses the GDP of many individual nations.

Alphabet CEO Sundar Pichai stated the company is “compute constrained in the near term,” framing the spending not as speculative expansion but as a direct response to demand that existing infrastructure cannot serve.

| Company | 2026 Capex Guidance | Q1 2026 Capex |

|---|---|---|

| Alphabet | $180-$190B | $35.7B (107% YoY growth) |

| Amazon | ~$200B | $43.2B |

| Meta | $125-$145B | N/A |

| Microsoft | ~$190B | N/A |

The headline numbers were broadly strong, and the consistency of the beats is what makes the market’s selective punishment more analytically interesting.

Every one of these companies beat Wall Street’s estimates. The question that emerged was why beating estimates was not enough for two of them.

The strength on 30 April extended well beyond technology. Caterpillar shares jumped approximately 10% after a Q1 beat and an upgraded full-year revenue outlook, contributing to the Dow’s 790-point session gain. Eli Lilly reported Q1 2026 revenue of $19.8 billion, up 56%, with Mounjaro revenue of $8.66 billion representing 125% growth. Lilly shares gained approximately 9%.

The breadth matters. This was not a narrow AI rally propping up the index; the earnings season delivered across sectors.

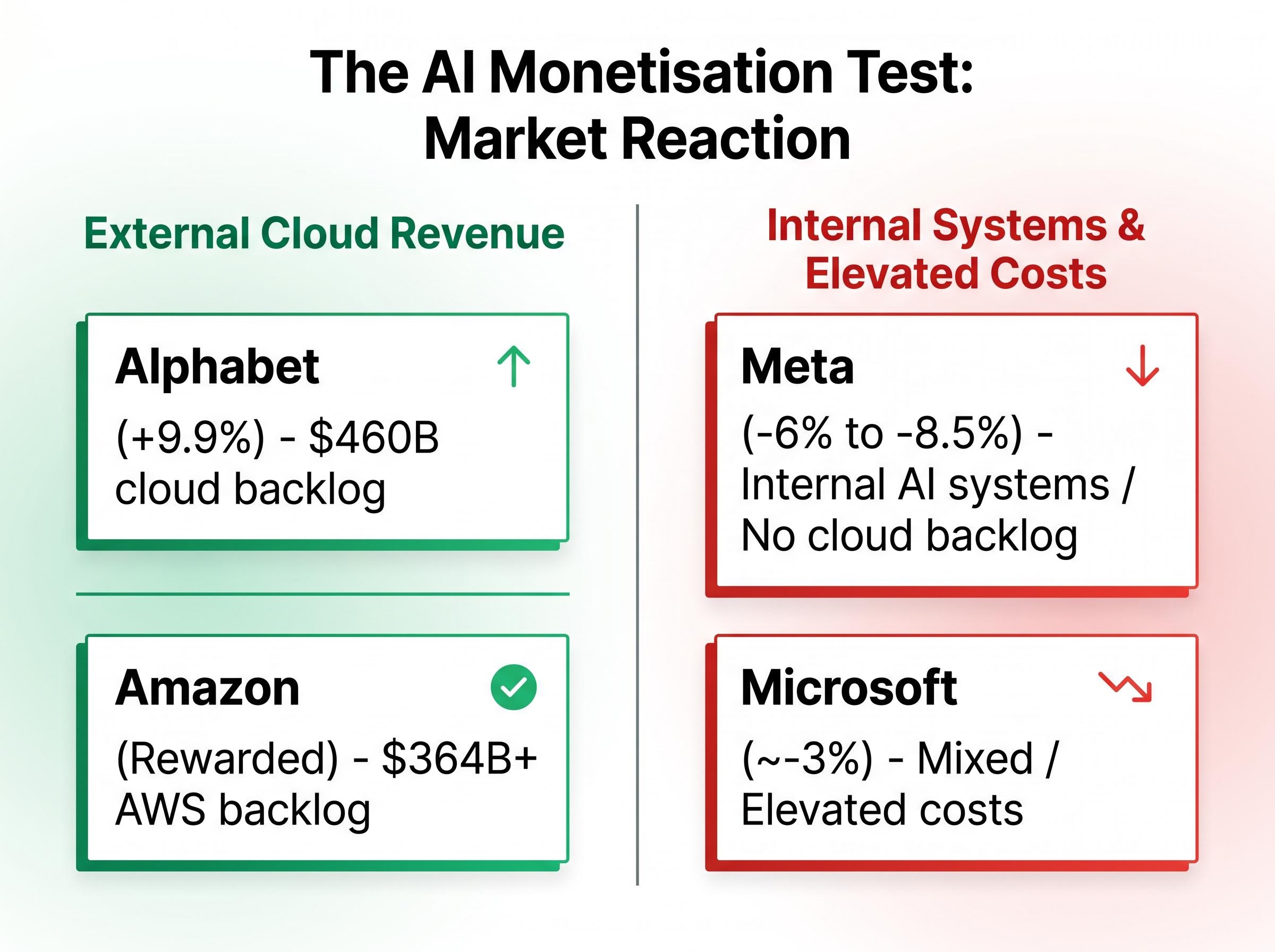

Alphabet and Amazon were rewarded. Meta and Microsoft were not. All four are spending at extraordinary scale. The difference is where the money goes and what it produces.

Alphabet’s $460 billion cloud backlog, nearly double the prior quarter, represents committed customer contracts waiting on infrastructure to be built. Google Cloud is generating incremental margins of 30-40%. Every dollar of capex has a visible revenue pathway. Amazon’s AWS backlog stands at $364 billion, excluding an Anthropic deal exceeding $100 billion. AWS growth of 28% validates the infrastructure investment as demand-driven.

Meta’s spending tells a different story. Its capex funds internal systems: recommendation algorithms, Llama model development, and advertising infrastructure. There is no external cloud revenue line to validate the outlay. Microsoft’s capex increase, driven partly by elevated memory costs, similarly lacks the near-term external revenue offset that cloud backlogs provide.

The market is not punishing AI spending. It is punishing AI spending that cannot yet point to external revenue.

The AI capex disconnect had already erased more than $1 trillion in combined technology market value in the weeks before these Q1 results landed, as investors priced in the risk that massive data centre commitments would compress free cash flow faster than cloud revenue could offset it.

Sundar Pichai described Alphabet as “compute constrained in the near term,” a framing that positions every new data centre as a revenue unlock rather than a cost centre. No equivalent statement emerged from Meta or Microsoft linking capex to constrained revenue.

| Company | Capex Direction | Demand Signal | Market Reaction |

|---|---|---|---|

| Alphabet | External cloud revenue | $460B cloud backlog | +9.9% |

| Amazon | External cloud revenue | $364B+ AWS backlog | Rewarded |

| Meta | Internal AI systems | No external cloud backlog | -6% to -8.5% |

| Microsoft | Mixed; elevated costs | Beat estimates but cost concerns | ~-3% |

The billions are not an abstraction. They buy physical things: data centres, AI chips, and compute capacity. Understanding what capex produces clarifies why backlog and capacity utilisation matter more than the headline spending figure.

The capex-to-revenue chain follows three stages:

Power grid constraints are emerging as the binding physical limit on data centre expansion timelines: US data centres are projected to consume 9% of domestic electricity by 2030, up from 4% in 2023, a trajectory that makes secured long-term power agreements as strategically important as chip procurement when assessing which hyperscalers can actually deliver on their capex commitments.

Alphabet’s “compute constrained” framing means its cloud revenue is actively held back by physical capacity limits, not by demand. Each new data centre directly unlocks revenue that is already contractually committed.

Network World’s hyperscaler backlog growth analysis, drawing on Dell’Oro Group research and statements from Amazon and Google executives, documents how cloud commitment backlogs have expanded in tandem with capex acceleration, providing independent validation that demand is outpacing currently available supply.

Meta’s capex, by contrast, funds internal systems that improve advertising targeting and content recommendation. The return on that investment flows through advertising revenue rather than a separable cloud business, making the monetisation timeline harder for analysts to isolate.

Public cloud baseline spending has tripled to 3-4x prior levels across the sector, a pace that creates cash flow risk if new capacity does not monetise quickly enough.

The S&P 500 advanced 10.42% across April 2026, its strongest monthly result since November 2020. The Nasdaq surged 15.29% over the same period. The VIX dropped approximately 10% to 16.9, its lowest reading since 3 February.

The S&P 500 and Nasdaq monthly performance data published on 30 April confirms the index closed at 7,209.01 with the VIX falling below 17, placing the session’s market-wide optimism in the context of the broadest monthly advance in more than five years.

Yet within that broad optimism, selectivity sharpened. The Communication Services sector gained 3.98% on 30 April. Information Technology was the sole sector to decline, falling 0.63%, with Nvidia dropping approximately 4% as broader AI capex scrutiny weighed on chip valuations.

Analyst commentary consistently identifies a single concern heading into the remainder of 2026: capex is broadly outpacing near-term revenue translation across the sector, and the timeline for that gap to close remains uncertain.

Valuation model recalibration is now a live challenge for institutional investors: traditional price-to-earnings and price-to-free-cash-flow multiples understate the capital intensity of the current cycle, and analysts covering Alphabet, Amazon, Meta, and Microsoft are being forced to rebuild models around operating cash margin and computing-driven revenue as primary gauges.

The unresolved question for the next two to four quarters centres on whether the companies currently being punished can close the monetisation gap. The forward watch list for investors:

The market is not divided on whether AI infrastructure matters. It is divided on which companies can prove the spending is already generating returns.

Investors wanting a framework for positioning around the infrastructure beneficiaries rather than the hyperscalers directly will find our dedicated guide to evaluating AI stocks in the hardware capex cycle useful; it covers how semiconductor suppliers like Nvidia, AMD, and Broadcom are capturing immediate revenue from hyperscaler procurement, the operating cash flow ratios that signal capex cycle durability, and the software monetisation lag risks that could pull hardware multiples lower.

The Q1 2026 earnings cycle confirmed that the AI investment supercycle is not slowing. More than $650 billion in combined 2026 capex commitments from four companies represents the largest coordinated private infrastructure investment cycle in recent history. The market’s response, however, was not a blanket endorsement. It applied a specific monetisation test: companies with external cloud revenue validating their spending were rewarded, while those directing capex toward internal systems without a near-term revenue offset were penalised.

The next earnings cycle will reveal whether Meta and Microsoft can demonstrate a clearer link between AI spending and revenue generation, or whether the divergence between cloud-revenue validators and internal spenders widens further. For investors, the framework is now visible: the question is not how much a company spends on AI, but whether that spending is pulling in revenue or deepening costs.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Q1 2026 big tech earnings revealed that Alphabet, Amazon, Meta, and Microsoft collectively committed more than $650 billion to AI infrastructure in 2026, with all four companies beating Wall Street estimates while receiving sharply different market reactions based on their ability to link spending to external revenue.

Meta and Microsoft were penalised because their AI capex is directed toward internal systems without a near-term external cloud revenue offset, whereas Alphabet and Amazon could point to massive cloud backlogs ($460 billion and $364 billion respectively) as direct validation that spending is demand-driven.

Alphabet guided to $180-$190 billion, Amazon committed to approximately $200 billion, Meta raised its guidance to $125-$145 billion, and Microsoft indicated approximately $190 billion in fiscal-year capex, bringing the combined total above $650 billion for 2026 alone.

A cloud backlog represents committed customer contracts for future infrastructure use; Alphabet's $460 billion and Amazon's $364 billion backlogs signal that their AI capex is being pulled by existing demand rather than speculative expansion, which is why the market rewarded their spending over rivals without equivalent external demand signals.

Investors should monitor Meta's monetisation timeline for internal AI systems, Microsoft's margin trajectory under elevated infrastructure costs, Alphabet's backlog conversion rate as new data centre capacity comes online, and whether AWS can sustain its 28% growth rate at scale.