According to market estimates, the combined market valuation of Microsoft, Alphabet, Amazon, and Meta Platforms now exceeds $10 trillion. Yet their continued market dominance rests on an unprecedented physical buildout that is fundamentally altering the global hardware supply chain. Following the explosive Q1 2026 earnings reports released recently, market attention has shifted entirely from software capabilities to the staggering capital required to build and power new computing facilities across the United States.

Understanding the mechanics of AI infrastructure investment is now critical for evaluating the sustainability of this technological arms race. This guide explains how these massive financial commitments operate and how they impact broader equity markets. It also clarifies the specific metrics that investors must monitor to determine if this highly capital-intensive strategy can succeed.

Decoding the Physical Reality of Artificial Intelligence Hardware

Artificial intelligence requires a vast industrial footprint that operates very differently from traditional cloud services. The new infrastructure class relies on specialised, highly localised hardware deployments rather than standard server racks. This shift replaces the famously high margins of software with the heavily capital-intensive reality of physical facility construction and processor procurement.

Industry analysis breaks down modern computing facilities into three core components:

Processing Units: High-density compute clusters designed specifically to handle complex machine learning algorithms. Networking Equipment: High-bandwidth optical cables and switches required to link thousands of processors together without latency. * Power Delivery Systems: Industrial-scale cooling arrays and electrical substations needed to prevent system failure.

The immensity of these power requirements is currently driving physical location decisions across the United States. Meta is actively developing a scalable 5GW data centre in Louisiana known as the Hyperion project. Meanwhile, Microsoft disclosed an $80 billion Azure orders backlog that remains specifically unfilled due to local power constraints.

The Power Grid Bottleneck

Electricity access has become the primary limiting factor for facility expansion across the technology sector. This limitation creates a hard ceiling on immediate deployment capabilities, regardless of how much capital corporations possess. Companies must secure guaranteed grid capacity before they can install the processors they have already purchased.

Official Department of Energy load forecasts anticipate a sustained surge in electricity demand through 2028 directly attributable to this new class of commercial data centers.

When big ASX news breaks, our subscribers know first

The 2026 Spending Surge and the Hyperscaler Arms Race

The capital expenditure guidance released by major technology firms for the 2026 fiscal year highlights a historic anomaly in corporate spending. Aggregate hyperscaler spend projections have reached $660 billion to $690 billion for 2026. These investments represent a coordinated race for computing supremacy where no single firm is willing to fall behind.

According to analysts, the broader market implications are profound, given that four companies account for roughly 17 percent of the S&P 500 total index weight. Directing such massive capital outflows creates a structural risk for the wider equity market if the spending cycle falters.

This unprecedented concentration creates structural vulnerabilities for passive investors, as broad market index funds are increasingly exposed to the specific capital expenditure cycles of these few dominant firms.

Amazon issued a staggering $200 billion guidance for the year, exceeding all consensus expectations. Alphabet projects $175 billion to $185 billion in capital expenditures, while Meta has allocated $115 billion to $135 billion. Microsoft is tracking toward $120 billion, having already deployed approximately $35 billion during the Q1 2026 quarter alone.

| Company | 2026 CapEx Guidance | Q1 2026 Spend/Signal |

|---|---|---|

| Amazon | $200 billion | AWS hit $142 billion annualised run rate |

| Alphabet | $175-$185 billion | Strong cloud revenue growth tied to hardware |

| Meta Platforms | $115-$135 billion | Hyperion scalable 5GW project active |

| Microsoft | $120 billion | Deployed $35 billion in Q1 FY26 |

Quantifying these exact financial commitments allows financial professionals to comprehend the scale of market risk currently in play. The sheer volume of capital moving from balance sheets into physical infrastructure is unprecedented in modern technology markets.

The Revenue Translation and Shifting Investor Patience

As the physical buildout accelerates, financial observers are increasingly scrutinising the return on investment for these massive capital deployments. The tension between immediate capital outlays and delayed revenue recognition is becoming the central debate among institutional shareholders. Markets are demanding proof that these facilities can generate sustainable cash flows in the near term.

This tension is further complicated by the risk of rapid hardware obsolescence, as the aggressive pace of innovation means facilities built today could require extensive physical retrofitting within a compressed three-year window.

Investment strategists estimate that technology firms face a tight window to justify their expenditures.

According to analysts, “Companies currently have a strict 12-month timeline to demonstrate actual top-line growth from their infrastructure investments before the market fundamentally reprices their valuation multiples.”

There are early signs of successful monetisation, such as Microsoft projecting Azure AI revenue of $25.7 billion for the year. Similarly, the Amazon AWS division recently hit a $142 billion annualised run rate. However, the gap between these revenue signals and the hundreds of billions spent on procurement remains vast.

Navigating Elevated Earnings Volatility

Options markets are already pricing in the risk of revenue misses and subsequent share price volatility following upcoming earnings disclosures. According to market data, derivatives pricing forecasts notable share price adjustments, ranging from 4 percent for Amazon to 7.1 percent for Meta. Financial analysts warn that current options pricing might actually understate the risk of a severe market pullback if any major player suddenly reduces its capital expenditure plans.

Downstream Beneficiaries in the Semiconductor Ecosystem

While the hyperscalers face uncertain software monetisation timelines, the semiconductor ecosystem is capturing immediate and guaranteed hardware revenue. There is a direct pipeline between Big Tech capital expenditures and semiconductor manufacturer revenues. Supply constraints and massive order backlogs have created unprecedented pricing power for chip designers and foundries.

This massive capital influx is fundamentally reshaping semiconductor ecosystem valuations as foundries and equipment providers capture guaranteed revenue streams from hyperscaler order backlogs.

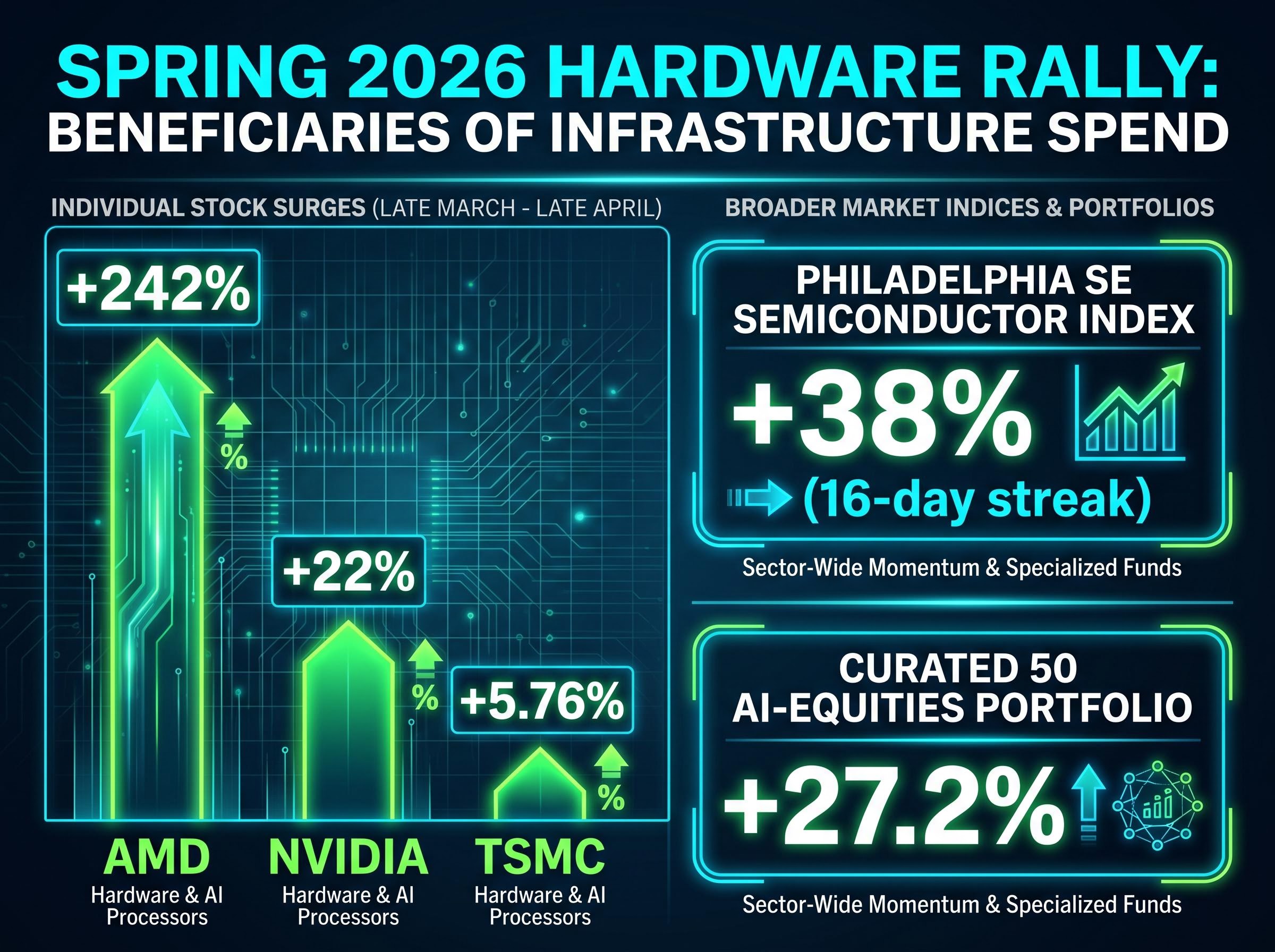

Following the early 2026 announcements of increased infrastructure spending, hardware markets experienced a historic rally. The Philadelphia SE Semiconductor Index achieved a 16-day winning streak, finishing up 38 percent by late April 2026.

According to market data, a curated portfolio of fifty artificial intelligence-focused equities advanced 27.2 percent between late March and late April 2026. This momentum highlights specific operational gains across the supply chain:

Nvidia shares rose 22 percent as demand for high-end processing units continued to outpace supply. AMD surged 242 percent, reflecting aggressive positioning in the enterprise compute market. * TSMC rallied 5.76 percent, driven by both the hyperscaler spending surge and its own massive capacity upgrades.

Looking beyond consumer-facing technology giants allows investors to identify where the capital is actually flowing today. The hardware supply chain is absorbing the billions of dollars that software companies are deploying.

Assessing the Long-Term Viability of Capital-Intensive Tech

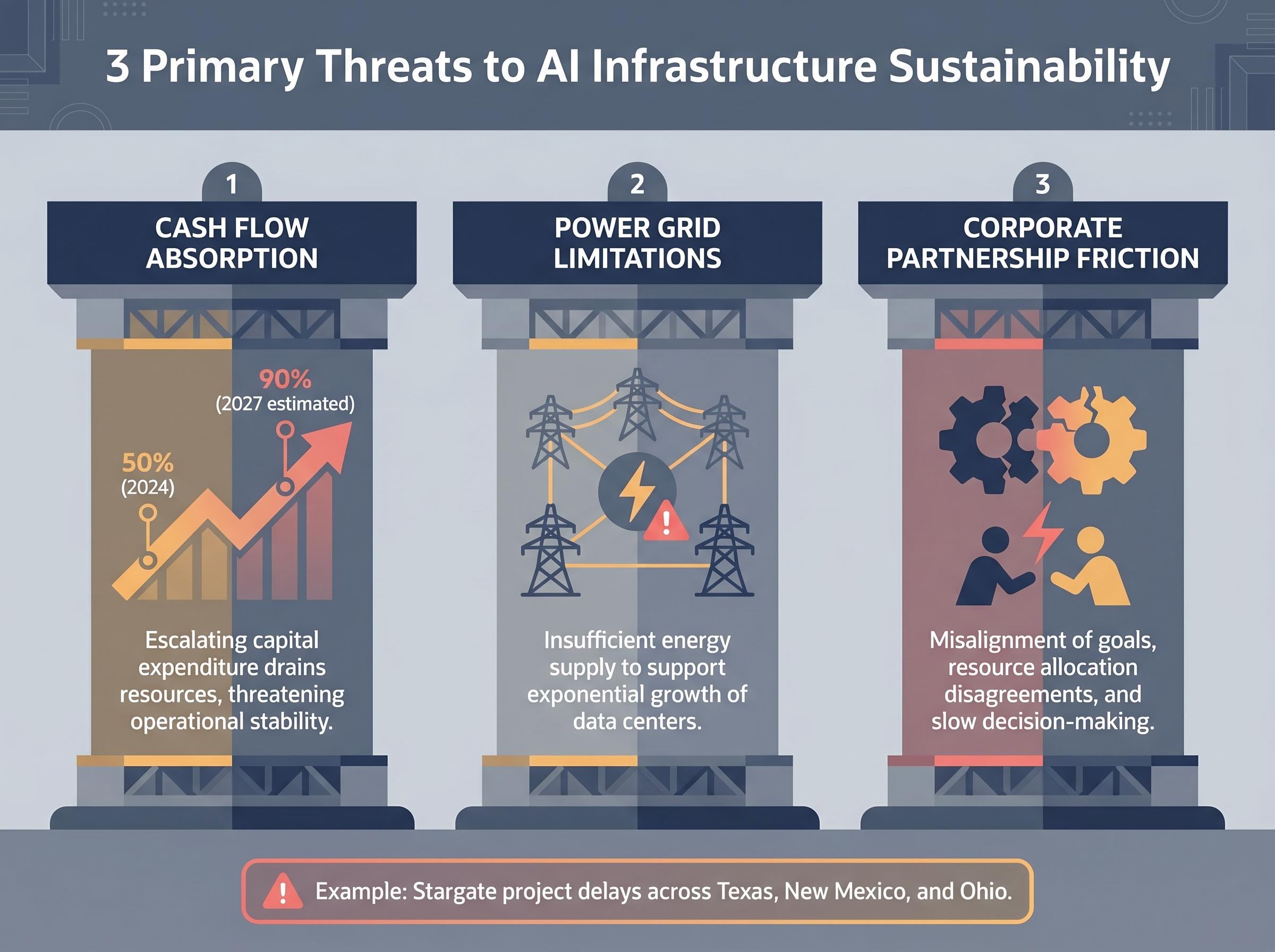

The ultimate test for the broader stock market rally over the coming year will be the long-term viability of this historically capital-intensive trajectory. According to industry estimates, financial models show that infrastructure expenditures for major tech firms are jumping from 50 percent of operational cash flow in 2024 to an estimated 90 percent by 2027. Sustaining this level of spending through the end of the decade requires perfect execution and uninterrupted revenue growth.

Beyond financial modelling, severe physical and operational roadblocks could force a slowdown independent of any corporate desire to spend. For example, the Stargate project has faced reported delays affecting planned infrastructure buildouts across Texas, New Mexico, and Ohio.

Industry analysis points to three primary threats to the sustainability of this investment cycle:

- Cash Flow Absorption: The risk that infrastructure costs will consume nearly all operational cash flow by 2027, leaving little room for error.

- Power Grid Limitations: Regional energy markets are struggling to provide the gigawatts required, stalling deployments regardless of available hardware.

- Corporate Partnership Friction: Disputes between hardware providers, cloud operators, and sovereign wealth partners, as seen with recent facility delays.

Evaluating these systemic risks is critical for long-term portfolio positioning. The transition from software agility to heavy industrial dependency changes the fundamental risk profile of the technology sector.

Investors exploring how these structural constraints impact broader market pricing will find our deep-dive into tech hardware valuations, which analyses how physical bottlenecks and shifting profit margins are fundamentally altering the growth trajectories of the wider supply chain.

The New Economics of Big Tech Valuation

The technology sector has formally transitioned from an era of high-margin software efficiency to a period of heavy, industrial-scale spending. The success or failure of the massive $660 billion to $690 billion spending cycle slated for this year will ultimately dictate the health of the broader equity market.

Investors must adapt their valuation models to account for this new reality. Traditional metrics focused on user growth and software subscriptions are no longer sufficient for evaluating companies that function more like regulated utilities or heavy infrastructure providers. The companies that successfully navigate the power constraints and monetisation delays will define the next decade of market leadership.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.