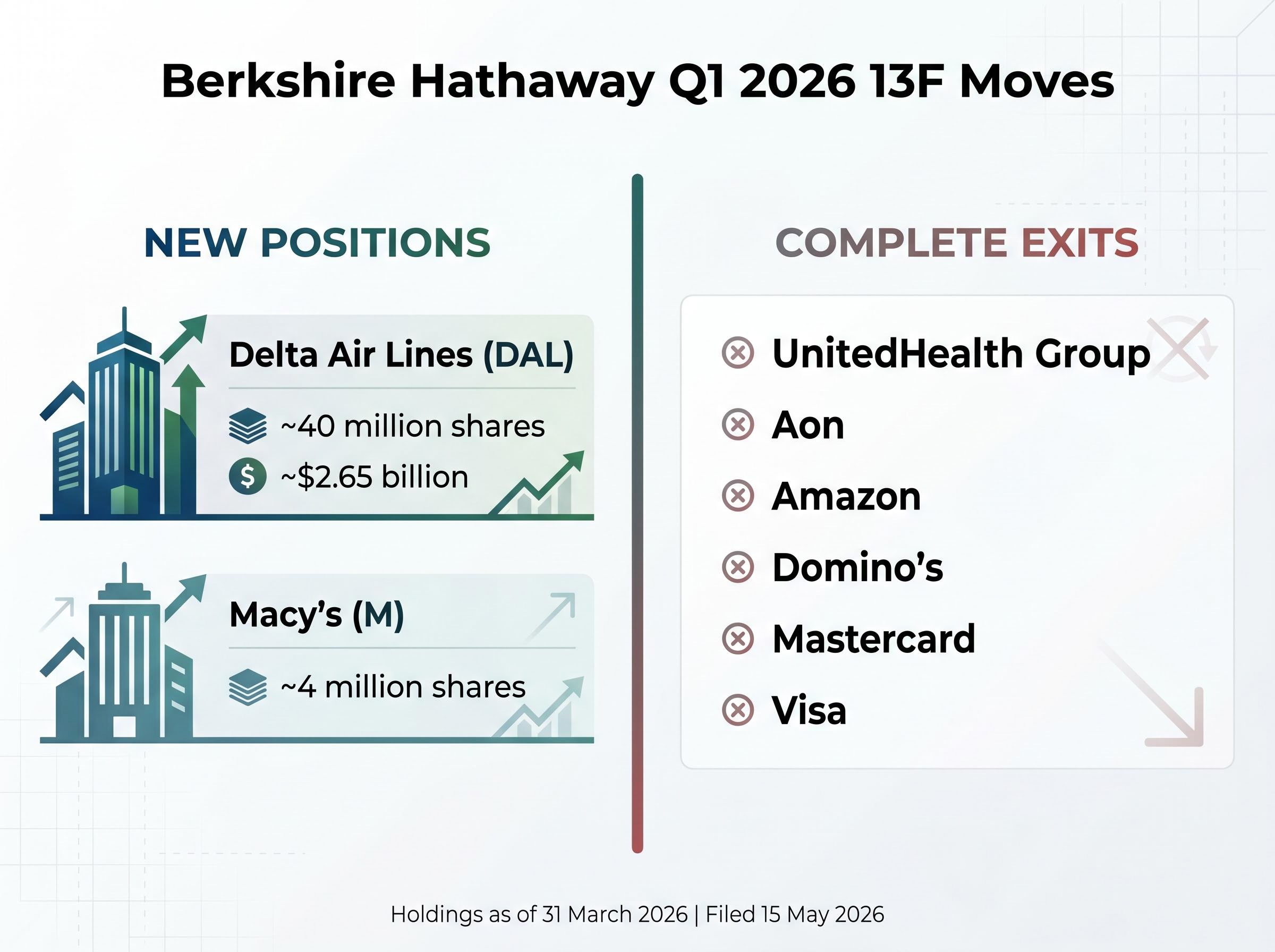

Berkshire Hathaway’s first 13F filing under Greg Abel landed on public databases this afternoon, and the market’s verdict arrived within minutes. The quarterly disclosure of Berkshire Hathaway holdings revealed two new positions, a $2.65 billion stake in Delta Air Lines and a smaller position in Macy’s, alongside the complete liquidation of six existing holdings. Delta shares climbed roughly 3% in after-hours trading. Macy’s jumped approximately 5%. The exits, including UnitedHealth Group, Visa, Mastercard, Amazon, Aon, and Domino’s, drew a sharper line between Abel’s first quarter as chief executive and the portfolio he inherited. What follows is a breakdown of what Berkshire bought, what it sold, why these two companies likely cleared Abel’s investment bar, and how the moves compare to Warren Buffett’s own track record in these sectors.

Delta and Macy’s shares surge as Berkshire’s new positions hit the tape

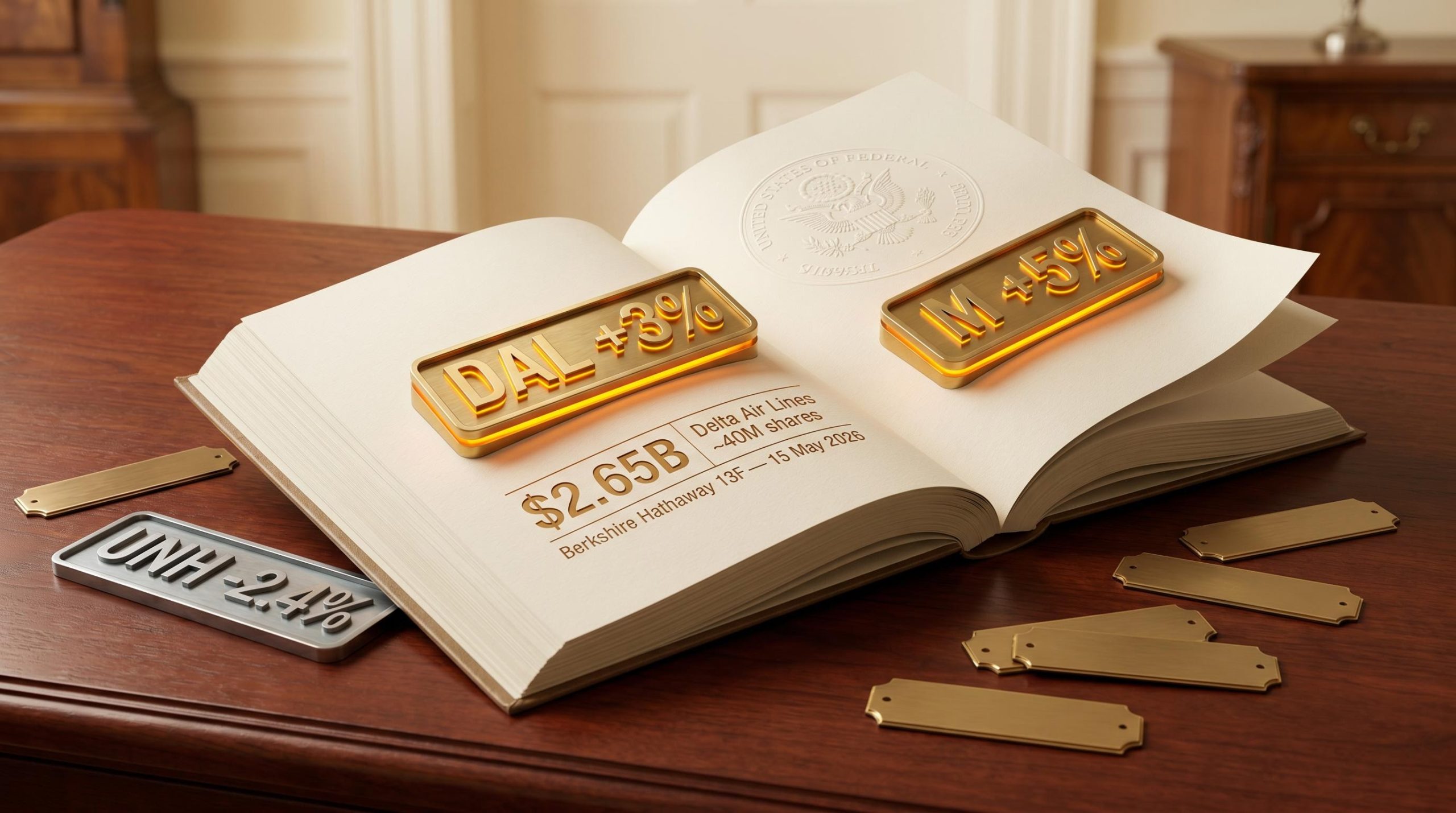

The after-hours tape told a clear story. Delta Air Lines (DAL), where Berkshire disclosed approximately 40 million shares valued at roughly $2.65 billion, rose about 3% within minutes of the filing’s publication on 15 May 2026. Macy’s (M), a smaller position of approximately 4 million shares, surged roughly 5%.

On the other side of the ledger, UnitedHealth Group (UNH) fell approximately 2.4% after hours as investors absorbed Berkshire’s complete exit. The five other liquidated positions, Aon, Amazon, Domino’s, Mastercard, and Visa, barely moved.

The asymmetry was telling. Markets treated the new buys as endorsements of two out-of-favour companies, while the exits, UNH aside, registered as housekeeping rather than conviction calls.

| Stock | Action | Approximate Size/Shares | After-Hours Move |

|---|---|---|---|

| Delta Air Lines (DAL) | New position | ~40 million shares (~$2.65B) | +3% |

| Macy’s (M) | New position | ~4 million shares | +5% |

| UnitedHealth Group (UNH) | Full exit | Entire position sold | -2.4% |

| Aon (AON) | Full exit | Entire position sold | Negligible |

| Amazon (AMZN) | Full exit | Entire position sold | Negligible |

| Visa (V), Mastercard (MA), Domino’s (DPZ) | Full exits | Entire positions sold | Negligible |

When big ASX news breaks, our subscribers know first

Why Delta cleared Berkshire’s bar: cash flows, low multiples, and a durable franchise

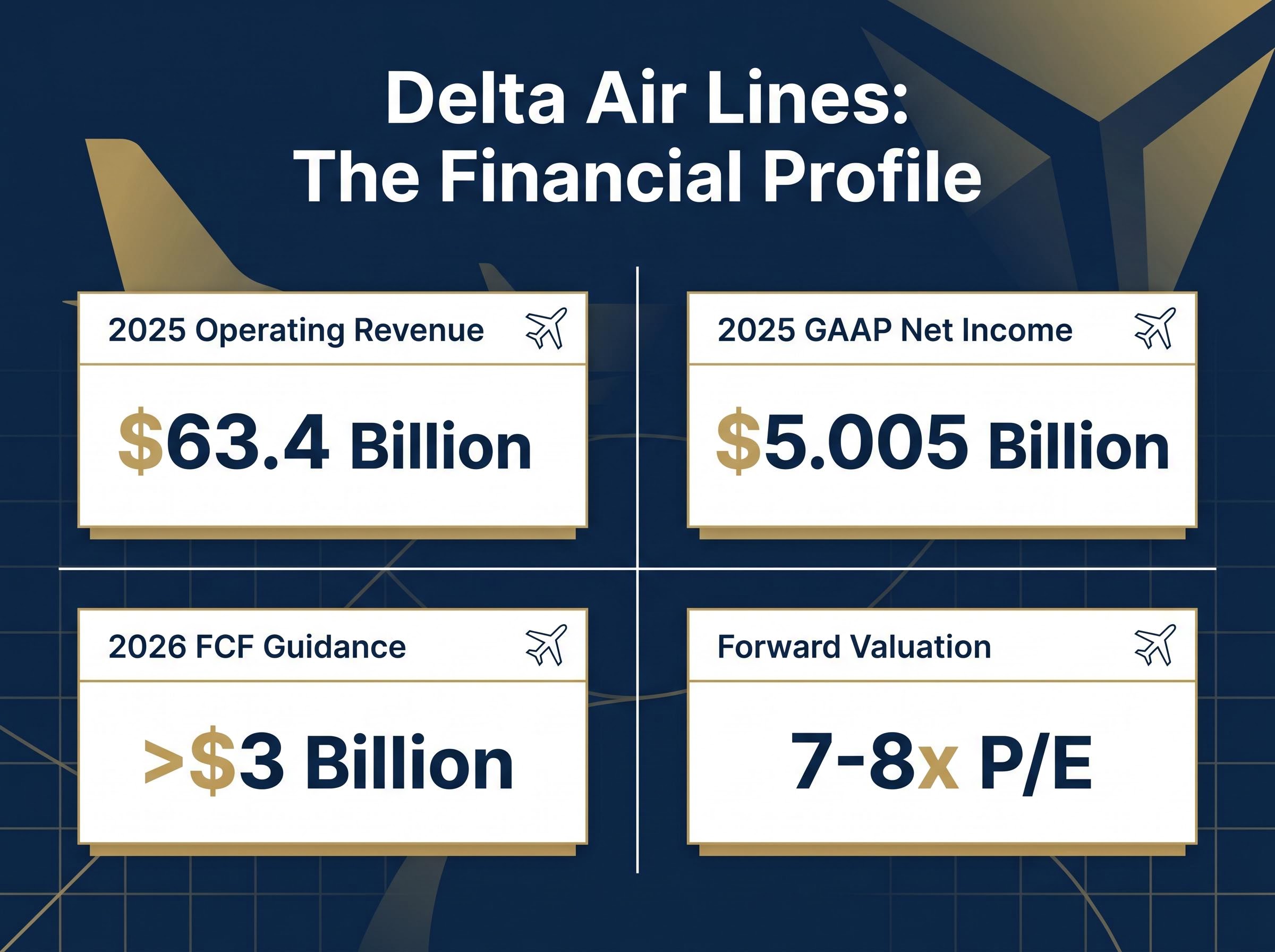

The numbers arrive first. Delta reported $5.005 billion in GAAP net income on $63.4 billion in operating revenue for 2025, with a pre-tax margin of 9.8%. Management guided for 2026 adjusted earnings per share of $6-$7 and free cash flow exceeding $3 billion, with revenue growth in the low- to mid-single digits.

At the time of Berkshire’s purchase, Delta was trading at roughly 7-8x its 2026 consensus EPS estimate, according to Barron’s, with an implied free-cash-flow yield in the low-teens percentage range. That placed it at a material discount to the broader market and to many industrial peers.

The qualitative case reinforces the valuation. The Financial Times described Delta in March 2026 as “the profitability leader among US legacy carriers,” citing its premium-cabin network and corporate-travel franchise.

“The profitability leader among US legacy carriers.” Financial Times, 18 March 2026

Three attributes likely cleared Abel’s bar:

- Durable free cash flow: More than $3 billion guided for 2026, with explicit capital returns to shareholders

- Low valuation: Single-digit forward P/E and a double-digit FCF yield

- Premium franchise position: Pricing power in premium cabins and corporate travel that separates Delta from commodity airline exposure

Analyst consensus as of late April to early May reflected broad agreement: approximately 23-26 analysts covered Delta, with the majority rating it buy or strong buy. Average 12-month price targets ranged from $78.82 to $81.68, with some as high as $95.

The Macy’s case: real estate, restructuring, and activist-flagged hidden value

On the surface, Macy’s looks like the opposite of a Berkshire pick. Net sales fell to $22.293 billion in 2024, down approximately 3.5% year over year, with comparable sales declining 3.9%. The department store sector remains under structural pressure from e-commerce.

The balance sheet tells a different story. Macy’s carried $3.1 billion in long-term debt against $1.0 billion in cash as of 28 January 2025, with net debt to EBITDA of approximately 2.1x, according to S&P Global. Adjusted EBITDA margin held at 9.1% in 2024, and free cash flow reached $1.1 billion.

Behind the headline sales decline: assets, cash flow, and a restructuring in motion

The asset picture is where the sum-of-the-parts logic sharpens. Analyst estimates cited by the Wall Street Journal in November 2025 placed Macy’s real estate value at $6-$8 billion, much of which was not reflected in the share price. When Arkhouse Management and Brigade Capital proposed taking Macy’s private, their 2025 bid implied an equity valuation of approximately $6.6 billion, a figure the board said undervalued the company.

Macy’s “Bold New Chapter” restructuring programme, announced in February 2024, targets approximately 150 store closures by 2026 while investing in its top 350 locations. By Q3 2025, roughly half the closures were complete, and upgraded stores were reporting mid-single-digit comparable-sales growth.

Three pillars underpin the investment thesis:

- Real estate value: $6-$8 billion in analyst estimates, largely unrecognised by the market

- Cash flow generation: $1.1 billion in annual FCF despite declining top-line revenue

- Restructuring progress: Measurable improvement at upgraded stores, with the activist bid establishing a floor on asset value

What a 13F actually tells you (and what it does not)

A 13F is a quarterly regulatory filing required of institutional investment managers overseeing more than $100 million in US-listed equity assets. It discloses long equity positions as of the end of the most recent quarter.

The SEC Section 13(f) reporting obligations apply to any institutional investment manager holding more than $100 million in US-listed equity securities, requiring disclosure of all long equity positions within 45 days of each calendar quarter-end, which is the regulatory framework that makes Berkshire’s portfolio visible to the public each quarter.

The positions published today reflect Berkshire’s holdings as of 31 March 2026. The filing deadline falls 45 days after quarter-end, meaning Berkshire could have added to, reduced, or fully exited either Delta or Macy’s in the six weeks since.

Berkshire’s total equity portfolio was estimated at approximately $274 billion across all holdings at the time of the 13F disclosure.

Three primary limitations are worth noting:

- The 45-day lag: Positions may have changed materially between quarter-end and filing date

- No short positions or derivatives: Options strategies, hedges, and short sales are not disclosed

- No non-US holdings or cash: The filing covers only US-listed equities, omitting international positions and the cash pile

Abel’s confirmed long-term core holdings provide continuity context: Apple, American Express, Coca-Cola, Moody’s, Bank of America, Chevron, and Occidental Petroleum all remained in the portfolio. The new positions and exits represent changes at the margins of a concentrated portfolio, not a wholesale reorientation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Abel’s stamp on Berkshire: how these picks fit his capital-allocation philosophy

The two new positions share a profile that maps closely to how Abel has described his investment approach. In a January 2026 CNBC interview, Edward Jones analyst Jim Shanahan characterised Abel as someone who “tends to think in terms of durable cash flows, regulated or semi-regulated environments, and disciplined reinvestment,” adding that Abel is “more comfortable with cyclical, asset-heavy businesses than Todd Combs or Ted Weschler.”

Mizuho analyst Dan Dolev, writing in Barron’s in April 2026, anticipated that Abel would “pare back the experiments that Todd Combs favoured and double down on core compounders and a few opportunistic value plays.” Morningstar’s Greggory Warren told the Wall Street Journal that “Abel seems intent on fewer, more understandable holdings.”

The Berkshire succession formalized Abel’s authority at the start of 2026, and his stated capital allocation framework, anchored in durable cash flows, disciplined reinvestment, and a wider aperture for cyclical businesses than Buffett typically favoured, provides the philosophical scaffolding that makes both picks legible.

Karen Firestone of Aureus Asset Management, speaking on CNBC on 15 May 2026, described the filing as “very much an Abel move: big swing at an industry leader with proven cash generation in Delta, plus a value-and-real-estate play in Macy’s. It’s tangible, cash-flowing businesses.”

Berkshire’s Q1 2026 earnings provided the immediate financial baseline Abel was working from when sizing these positions: $11.35 billion in operating profit, up 18% year-over-year, with insurance underwriting leading segment performance and a modest $234 million buyback resumption signalling that valuations were beginning to look more attractive.

“Big swing at an industry leader with proven cash generation in Delta, plus a value-and-real-estate play in Macy’s. It’s tangible, cash-flowing businesses.” Karen Firestone, Aureus Asset Management, CNBC, 15 May 2026

Continuity or departure? How analysts are reading Abel versus Buffett

The exits frame the other side of the question. Buffett exited all airline positions in 2020, telling shareholders “the world has changed for airlines.” He cautioned against department-store retail as early as 2017, telling CNBC “the department store is online now.”

CFRA’s Cathy Seifert told the Wall Street Journal that “Buffett swore off airlines after Covid; Abel is betting the industry’s structure and profitability have improved.” SoFi’s Liz Young, on CNBC, described Abel as “less constrained by Buffett’s past bruises in airlines and retail.”

The most defensible reading sits between the two camps. Philosophically, the picks are consistent with Berkshire’s emphasis on cash flow, concentration, and value. Sector-wise, they represent Abel’s independent judgement about where current valuations and cash flows warrant conviction, even where Buffett would not have gone.

Delta at 7x earnings, Macy’s at a real estate discount: the value logic that may outlast today’s headlines

The after-hours moves will fade. The investment cases will take years to resolve.

For Delta, validation over a 3-5 year horizon would mean sustained free cash flow above $3 billion annually and continued premium-cabin pricing power. The forward P/E of 7-8x and low-teens FCF yield, per Barron’s, leave room for multiple expansion if the airline cycle cooperates. The primary risks are macro-driven demand slowdowns and fuel-cost spikes.

For Macy’s, the thesis resolves through either a realisation of the $6-$8 billion real estate value or stabilisation of comparable sales at restructured stores. Continued pressure from e-commerce and restructuring costs that exceed projected savings represent the key downside scenarios.

Consumer spending durability is the macro variable that most directly tests both theses: Delta’s premium-cabin and corporate-travel franchise depends on sustained demand from business and affluent leisure travellers, while Macy’s restructured stores need comp-sales stabilisation in an environment where the US personal savings rate has fallen and aggregate retail data risks being flattered by upper-income cohorts absorbing tariff-driven front-loading.

| Attribute | Delta Air Lines | Macy’s |

|---|---|---|

| Valuation metric | ~7-8x forward P/E | Real estate valued at $6-$8B vs. market cap |

| FCF profile | >$3B guided for 2026 | $1.1B in 2024 |

| Key risk | Demand cycle and fuel costs | E-commerce pressure and restructuring execution |

| Thesis validation | Sustained FCF + premium pricing power | Real estate realisation or comp-sales stabilisation |

Barron’s noted on 16 May 2026 that “Abel is buying cash flows at single-digit multiples, very much in the Berkshire tradition, even if the sectors might have once been off-limits to Buffett.” The Financial Times observed that the new positions “adhere to the Buffett canon in scale and style.”

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The first 13F of the Abel era draws a clear line between his portfolio and Buffett’s

The filing disclosed more than $2.65 billion in new capital committed to Delta alone, with an additional position in Macy’s. Six positions were fully exited: UnitedHealth Group, Visa, Mastercard, Amazon, Aon, and Domino’s. Read together, the moves form a coherent statement: fewer holdings, concentrated in cash-generating businesses trading at material discounts, with Abel willing to enter sectors his predecessor publicly avoided.

One quarter’s filing, subject to a 45-day lag, is not a definitive portrait. The long-term core, Apple, American Express, Coca-Cola, and Moody’s among them, remains intact.

What is new is the evidence. Berkshire’s next chapter is no longer a matter of speculation about what Abel might do. As of this afternoon, it is on the tape.