Eli Lilly at 40x Earnings: Expensive Stock, Underpenetrated Market

2 hrs ago

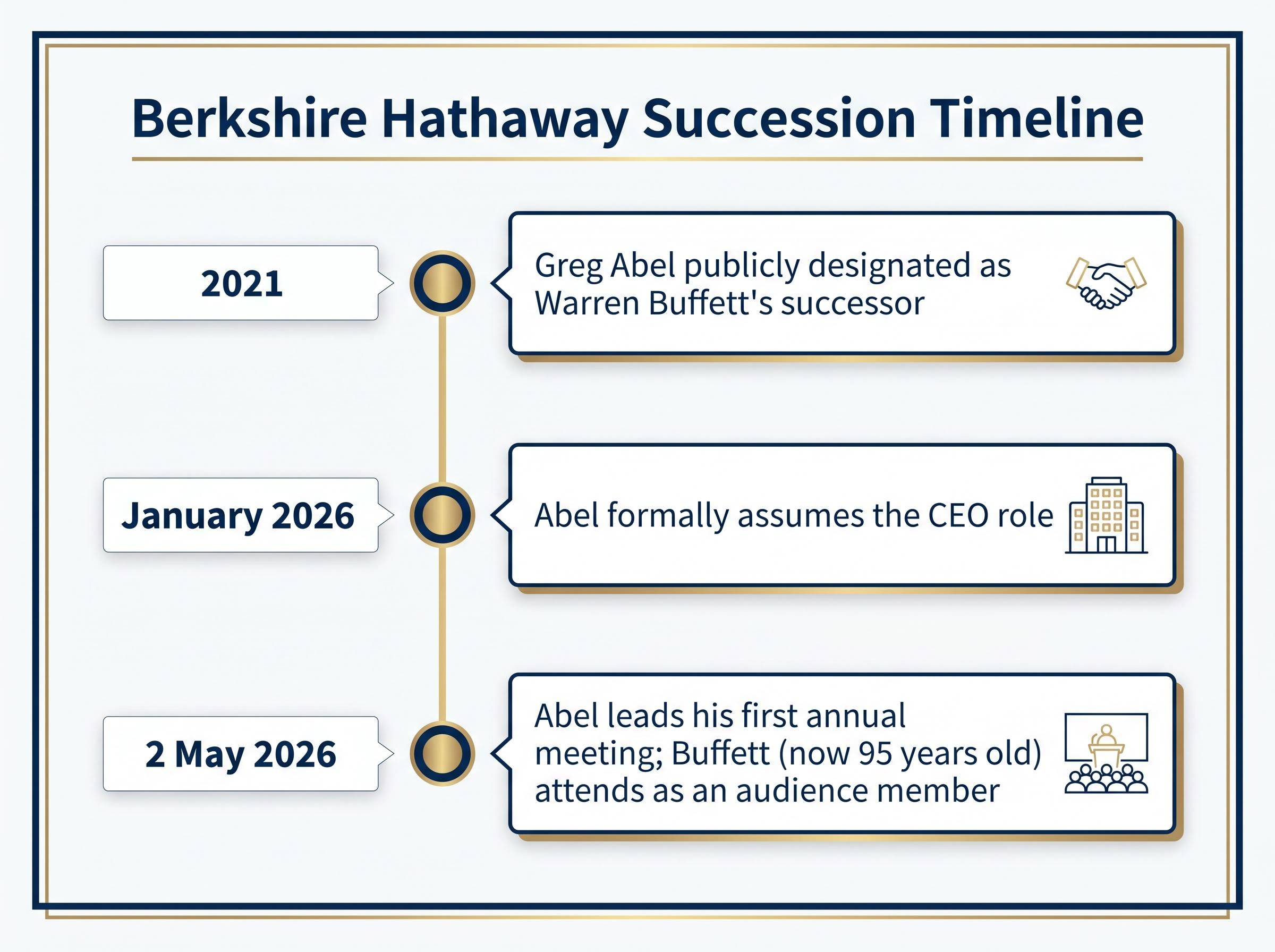

Warren Buffett took his seat in the audience at Berkshire Hathaway‘s annual meeting in Omaha this morning, 2 May 2026, as a spectator for the first time in decades. The man who built one of the most admired companies in American business history watched Greg Abel take the stage and run the show. The leadership handover had been publicly anticipated since 2021, when Abel was named Buffett’s successor, but the actual timing caught markets off guard. Abel formally became CEO at the start of 2026, making today’s annual meeting his first as the head of a company with nearly $400 billion in liquid reserves, a sprawling portfolio of operating businesses, and a shareholder base unusually attached to the personality of the outgoing leader. What follows is an examination of what the Warren Buffett succession means beyond the headline: how the handover unfolded, what Abel’s early moves signal about strategic direction, how financial performance is framing investor expectations, and what history says about the odds of successfully following an iconic founder-figure.

The succession timeline was never secret. Abel was publicly designated as Buffett’s eventual replacement in 2021. The board endorsed it. Shareholders digested it. Analysts modelled around it. Yet when Abel formally assumed the CEO role at the start of 2026, the market reacted as though the transition had arrived early.

The gap between those two facts is instructive. Knowing a succession is coming and knowing when it will happen are different forms of certainty. For five years, Buffett’s continued presence at the helm let investors defer the question of what Berkshire looks like without him. The precise date was never fixed, and that ambiguity allowed the market to treat the handover as a future event rather than a present one.

Buffett, now 95 years old, sitting in the audience rather than at the podium is itself a statement. The handover is not partial. It is not advisory. It is complete. That completeness is precisely what makes the market’s residual unease rational rather than irrational: succession planning and succession execution are different things, and the gap between them is where confidence gets tested.

Berkshire’s operating model has always been decentralised by design. Subsidiary managers run their businesses with a degree of autonomy that would be unusual at most conglomerates of comparable scale. The logic is straightforward: hire capable operators, give them room, hold them accountable for results.

Abel has framed this structure around a specific phrase.

In his 2026 shareholder letter, Abel described the cultural foundation of Berkshire’s management approach as “deserved trust,” a model in which operating subsidiaries retain autonomy paired with accountability to the parent company.

The question is whether that culture can hold without the figure who created it. Berkshire’s decentralisation was never codified in the way a formal governance framework might be. It was, in practice, the preference of a single individual whose reputation and judgment enforced its discipline. Subsidiary leaders operated freely because Buffett’s track record earned the trust that made freedom productive. Analysts have described the decentralised model as a “non-negotiable cultural constant” under Abel, but constants require institutional reinforcement, not just rhetorical commitment.

Berkshire’s 2026 proxy statement, filed with the SEC in March, details the corporate governance guidelines and board-level succession review processes that provide the formal institutional scaffolding around the decentralised operating model Abel has pledged to preserve.

Abel’s letter signals intentional preservation. He reiterated that acquisitions, organic growth, and disciplined repurchases remain the capital allocation framework. The language is continuity-first. For long-term Berkshire investors, whether the decentralised model endures as an institutional structure or fades as the echo of a single leader’s philosophy is the most consequential question the succession raises.

The clearest signal arrived before the annual meeting. In late 2025, Berkshire added a stake in Alphabet, a move that carried more analytical weight than its dollar value alone would suggest.

Buffett’s investment posture toward technology was defined by avoidance. He famously declined to invest in sectors he could not evaluate through the lens of durable competitive moats and predictable cash flows. AI-adjacent businesses, with their rapid iteration cycles and uncertain competitive dynamics, would not have fit comfortably in that framework. Abel’s willingness to take the position suggests a recalibration: not a repudiation of Buffett’s principles, but an acknowledgement that AI-influenced businesses now represent a category too large for a capital allocator of Berkshire’s scale to categorically avoid.

AI and infrastructure investment has moved from a speculative category to a structural capital allocation priority at institutional scale, with firms like Blackstone committing $69 billion in Q1 2026 inflows and anchoring their growth thesis explicitly around AI-adjacent physical and digital assets, a context that helps explain why Abel’s Alphabet stake carries more strategic weight than its dollar value alone suggests.

Abel’s 2026 shareholder letter also codified a specific repurchase policy requiring consultation with Buffett for any repurchases below conservatively estimated intrinsic value. The architecture is deliberate: new positioning in unfamiliar sectors, paired with a formal check on capital return discipline.

| Dimension | Buffett-era posture | Abel’s early signals |

|---|---|---|

| Technology sector stance | Broadly avoided; limited to Apple as an exception | Alphabet stake added; openness to AI-adjacent exposure |

| Capital deployment priority | Brand-moat acquisitions; patient cash accumulation | Acquisitions, organic growth, and operational improvement |

| Leadership communication style | Philosophical, wide-ranging annual letters | Operationally focused, business-specific |

| Repurchase policy | Discretionary, guided by Buffett’s personal judgment | Codified threshold with Buffett consultation requirement |

The Alphabet stake is the data point that matters most for investors calibrating their thesis on post-Buffett Berkshire. It suggests Abel’s investment aperture is wider than his predecessor’s, even as the underlying discipline remains anchored to the same valuation principles.

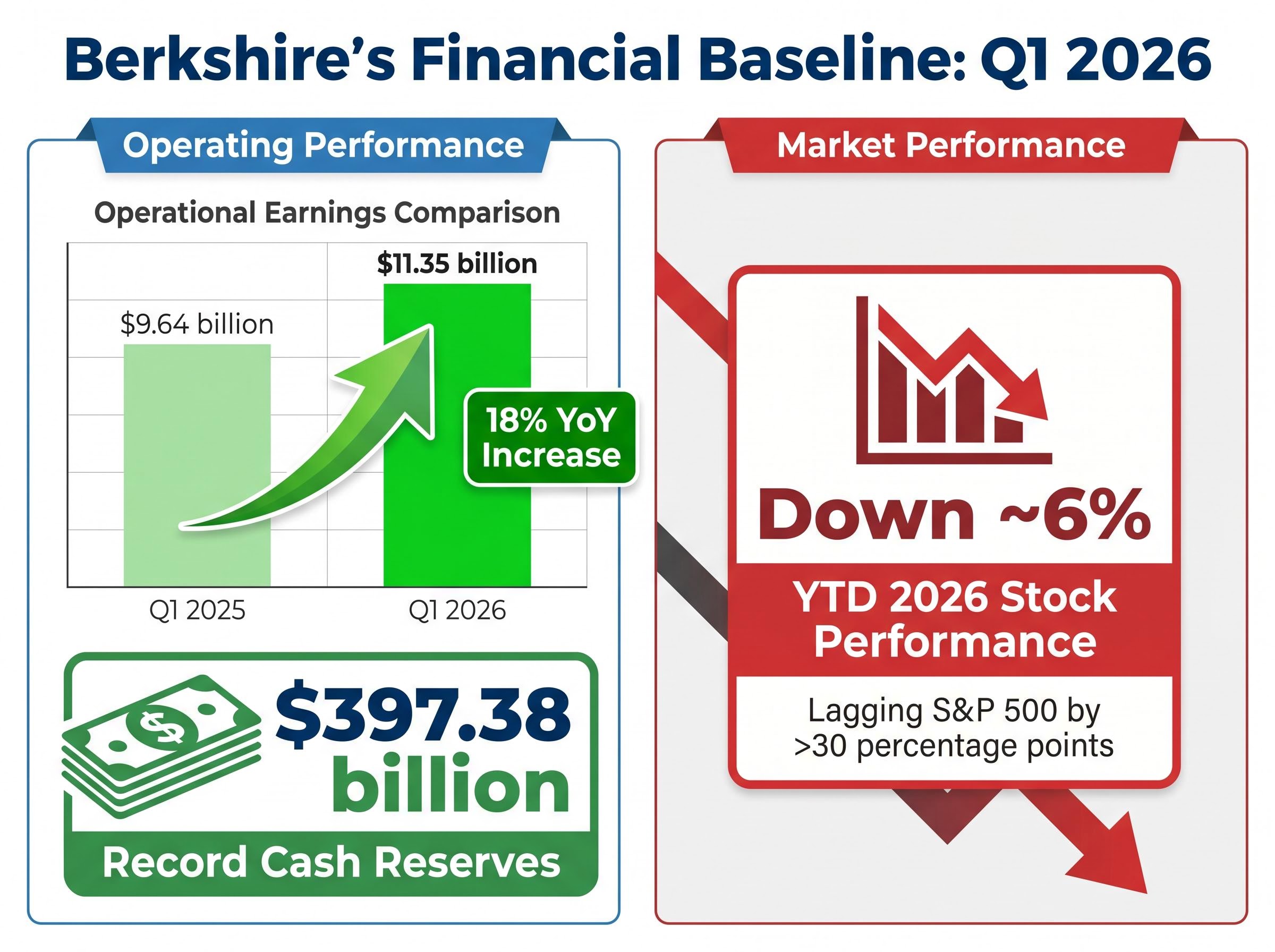

The operational foundation Abel inherited is strong by any measure. Q1 2026 operational earnings came in at $11.35 billion, up from $9.64 billion in Q1 2025, an 18% year-over-year increase. The cash position is extraordinary.

Berkshire held a record $397.38 billion in cash and liquid reserves as of Q1 2026, the largest war chest in the company’s history.

Berkshire’s cash reserve reached $373.31 billion at the close of 2025 before climbing further to $397.38 billion by Q1 2026, a position built through 19 months of deliberate abstention from large equity purchases that itself functions as an institutional signal about prevailing US market valuations.

Then the stock tells a different story. Berkshire shares have declined approximately 6% year-to-date in 2026, lagging the S&P 500 by over 30 percentage points since last May’s step-down announcement. The gap between operating performance and share price performance is the clearest expression of the market’s uncertainty about the post-Buffett era.

| Metric | Q1 2025 | Q1 2026 |

|---|---|---|

| Operational earnings | $9.64 billion | $11.35 billion |

| YTD stock performance | N/A | Down ~6% |

Analysts attribute the valuation gap primarily to muted 2026 earnings growth expectations and residual uncertainty about Abel’s capital deployment capacity at scale. The business is not struggling. The question investors are pricing is whether a structurally sound, cash-rich conglomerate can rerate upward once the new CEO demonstrates how he intends to put nearly $400 billion to work.

The most instructive comparison is Tim Cook at Apple. Steve Jobs’s cultural imprint on Apple was considered irreplaceable; the creative vision, the product instincts, the reality distortion field. Cook replaced none of it. He replaced it with something else: operational discipline, supply chain mastery, and a services revenue stream Jobs never prioritised. Apple’s market capitalisation roughly tripled under Cook’s leadership.

The comparison is not reassurance. It is a framework. Experts associate successful CEO successions of this type with three markers:

JPMorgan‘s succession planning under Jamie Dimon has also been referenced by analysts as a long-horizon proactive model, offering a reminder that the best successions are measured in quarters and years, not in a single meeting.

Abel’s early posture, operationally grounded and culturally conservative, has been characterised by analysts as an “evolutionary step.” The stock underperformance reflects the market’s standard lag in rerating a company after a leadership transition of this magnitude. History suggests the discount is typically transitional rather than structural, but it requires the incoming CEO to deliver proof points. Today’s meeting is Abel’s first opportunity.

Peer-reviewed research on founder-CEO succession finds that markets systematically apply a valuation discount when an iconic founder departs, with the discount typically compressing over subsequent quarters as the incoming CEO accumulates a visible track record, a pattern that maps closely onto Berkshire’s current 6% year-to-date share price lag.

The annual meeting’s format itself carries a signal. Abel’s session consists of a one-hour operational presentation followed by a 2.5-hour shareholder question-and-answer session. The structure is business-first, not philosophical.

Analysts have described today’s meeting as the “clearest read yet” on post-Buffett strategic plans, with particular attention on Abel’s capital deployment framework and sector positioning.

The variables long-term investors should be monitoring are specific and measurable:

Abel’s stated priorities from the 2026 letter remain anchored in acquisitions, organic growth, and disciplined repurchases. The cash reserve is both a near-term drag on returns and the single largest lever Abel holds. Investors do not need to decide today whether Abel will match Buffett’s legacy. They need to identify whether the next two to four quarters produce evidence that the transition is proceeding on the right trajectory.

Buffett sat in the audience this morning. He is 95 years old, and the company he built over six decades is now someone else’s to run. The formal transfer is complete.

Abel inherits an extraordinary platform: $11.35 billion in quarterly operational earnings, nearly $400 billion in deployable capital, and a decentralised operating model that has scaled without bureaucratic drag. He also inherits an extraordinary standard: the most closely watched value investing record in history.

The post-Buffett era did not begin with a dramatic strategic pivot. It began with an operational meeting in Omaha, a one-hour presentation, a question-and-answer session, and a new CEO demonstrating that he intends to run Berkshire the way Berkshire has always been run, with discipline, patience, and trust. That may be exactly the right register for what this company has always been.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The Warren Buffett succession refers to Greg Abel formally becoming CEO of Berkshire Hathaway at the start of 2026, following his public designation as Buffett's successor in 2021. Buffett, now 95, attended the 2 May 2026 annual meeting as an audience member rather than leading it.

Berkshire Hathaway shares have declined approximately 6% year-to-date in 2026, lagging the S&P 500 by over 30 percentage points since Buffett's step-down announcement, even as Q1 2026 operational earnings rose 18% year-over-year to $11.35 billion.

Abel has stated that acquisitions, organic growth, and disciplined share repurchases remain the core capital allocation framework, and his addition of an Alphabet stake in late 2025 signals a wider investment aperture that includes AI-adjacent businesses his predecessor largely avoided.

Analysts use the Apple example as a framework: Cook did not replicate Jobs's creative vision but replaced it with operational discipline and a services business, tripling Apple's market cap. The parallel for Abel is that matching Buffett's legacy is less important than building a distinct, demonstrably effective approach of his own.

Investors should monitor how Abel deploys the $397.38 billion cash reserve, the pace and type of acquisitions, evidence of operational improvement across subsidiaries, and whether the Alphabet stake marks the beginning of a broader technology and AI-adjacent allocation strategy.