US retail hubs remain crowded in April 2026, yet public economic optimism has collapsed to historic lows. This disparity between strong transaction volume and grim consumer sentiment reveals a complex macroeconomic vulnerability. Investors assessing current market conditions must look beyond top-line spending data, as immediate consumption levels are masking severe structural weaknesses. Evaluating true US recession risk requires understanding how households are temporarily preserving their lifestyles at the expense of their financial buffers. The widening wealth divide and rapid savings depletion are setting the stage for a sudden macroeconomic contraction. While broad equity markets continue to price in sustained growth, the underlying mechanics of consumer demand suggest this spending momentum is highly unstable. Financial models that extrapolate spring spending figures into forward-looking projections are missing the fundamental exhaustion of the middle-class consumer.

The Illusion of Consumer Strength in Spring Retail Data

The spring retail data presented a highly contradictory picture for financial professionals attempting to measure economic health. March 2026 retail sales surged 1.7% month-over-month, following a revised 0.7% gain in February. On a year-over-year basis, retail sales increased by a substantial 3.3%. A recent report published on 22 April 2026 by consumer behaviour firm Circana also showed unit demand increasing by 1.0% in discretionary categories. This immediate spending strength completely contradicts the historic collapse in public economic optimism.

The final University of Michigan Consumer Sentiment Index for April 2026 dropped 6.6% to a historic low of 49.8. This stark divergence is not a sign of economic resilience or hidden consumer strength. It represents a temporary and unsustainable preservation of lifestyle habits, where households continue to purchase at established volumes despite holding severe pessimism about their financial futures. Relying solely on headline retail figures is currently dangerous for equity positioning, as these transaction volumes reflect past momentum rather than forward-looking capacity.

Ongoing Federal Reserve research on consumer sentiment confirms this specific behavioral anomaly, demonstrating that households frequently sustain their transaction volumes long after their forward-looking economic outlook has turned negative.

| Economic Indicator | March/April 2026 Reading | Trend Direction |

|---|---|---|

| Retail Sales Growth (YoY) | 3.3% | Positive |

| Retail Sales Growth (MoM) | 1.7% | Positive |

| Discretionary Unit Demand | +1.0% | Positive |

| Consumer Sentiment Index | 49.8 | Negative (Historic Low) |

When big ASX news breaks, our subscribers know first

How Savings Depletion Accelerates Macroeconomic Contraction

The personal savings rate traditionally functions as an economic shock absorber, protecting domestic consumption from sudden external pressures. It measures the percentage of disposable income households set aside after taxes and essential expenses. Behavioural economics indicates that residents will temporarily maintain their daily habits by depositing less money into savings rather than immediately reducing their purchases. This psychological dynamic explains exactly why spending remains elevated while the underlying financial buffer rapidly deteriorates.

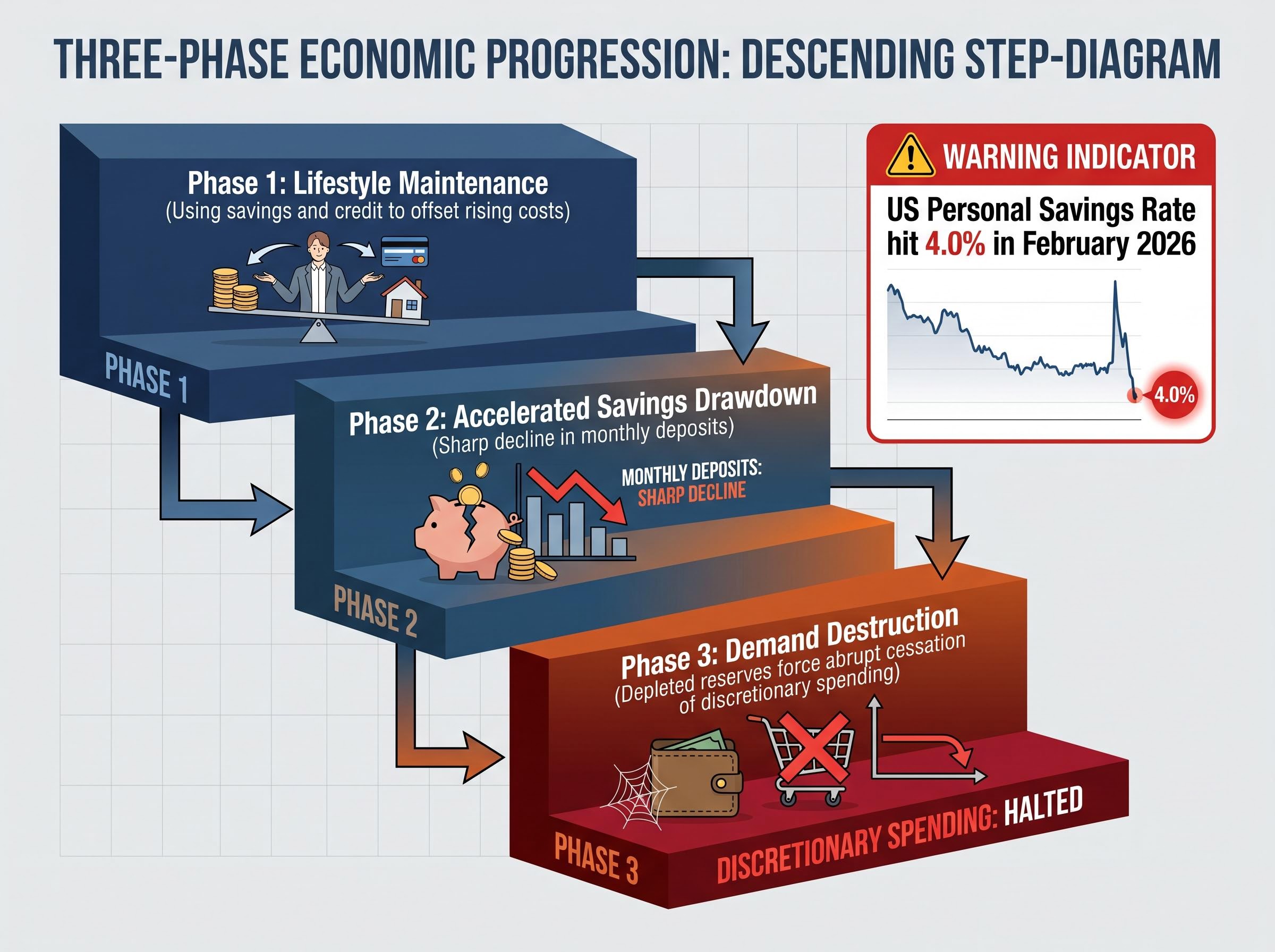

The US personal savings rate sat at just 4.0% in February 2026, representing a critical depletion of reserve capital. Financial professionals are closely anticipating the updated March savings rate, scheduled for release on 5 May 2026, to gauge the acceleration of this depletion. Once savings exhaustion reaches a mathematical limit, it inevitably triggers a sudden and aggressive halt in consumer demand. This process shifts the analytical focus from monitoring current spending indicators to tracking the remaining financial buffers.

The underlying BEA personal income and outlays data reveals that this sharp decline in household reserves is being driven almost entirely by the rising cost of essential services and non-discretionary goods.

The sequence of consumer strain typically follows a distinct progression before impacting broad market indices:

Phase one begins with lifestyle maintenance, where households use savings and credit facilities to offset rising basic costs. Phase two involves accelerated savings drawdown, marked by a sharp decline in monthly deposits despite outwardly stable consumption patterns. * Phase three culminates in demand destruction, as depleted reserves force an abrupt and systemic cessation of discretionary spending.

The Dipping E Pattern and the Deepening Wealth Divide

The optimistic retail forecasts for the year rely heavily on a fractured demographic foundation rather than broad-based economic health. The National Retail Federation (NRF) forecast projects 4.4% consumer-driven retail sales growth for 2026. However, this aggregate figure obscures the reality that affluent spenders are temporarily carrying the entire domestic economy. Less affluent households are quietly cracking under the pressure of compounding inflation, dedicating increasing fractions of their income strictly to basic survival.

This growing economic divergence leaves broad market indices looking healthy, while mass-market retailers face imminent demand cliffs. Capital allocation based on top-line aggregate data fundamentally misprices the risk profile of companies exposed to lower-tier consumers.

Unpacking the Dipping E Consumer Dynamic

The current retail environment is characterised by the “dipping E” pattern identified by consumer research analysts at Circana. This specific dynamic occurs when lower-income consumers actively retreat from discretionary spending while middle-income growth flattens completely. The top tier of earners remains the sole driver of transaction volume, masking the underlying decay in mass-market participation.

When slowing growth eventually reaches this top tier, it removes the final structural pillar supporting aggregate retail figures. Investors must distinguish carefully between sectors supported by broad structural demand and those relying entirely on the continued spending of a narrowing affluent demographic.

Wall Street Apathy and the $100 Crude Oil Threat

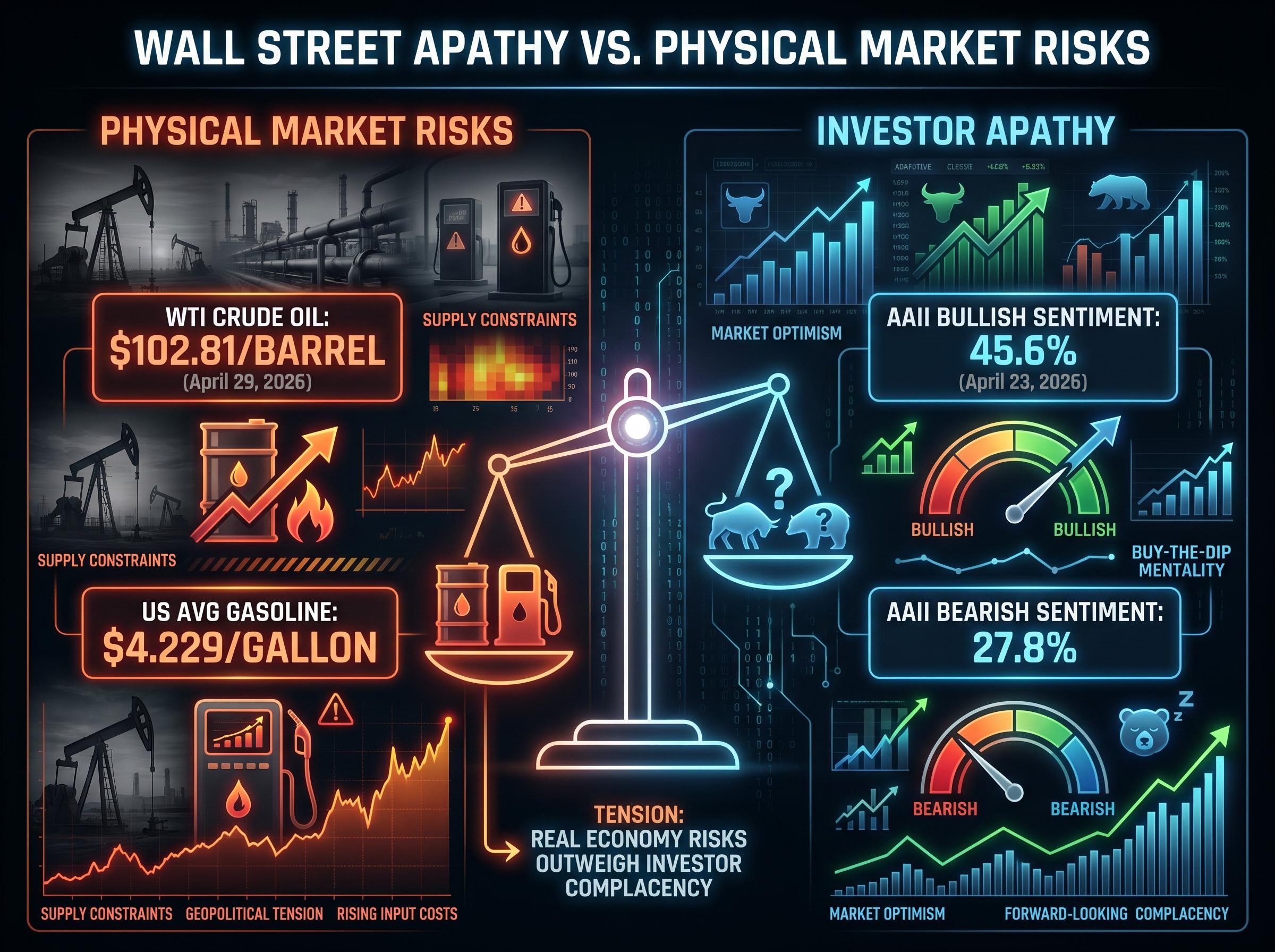

Mounting external pressures from surging energy costs are directly threatening domestic purchasing power, yet equity markets appear entirely unconcerned. Hostilities in the Middle East have driven the West Texas Intermediate (WTI) crude oil price to $102.81 per barrel as of 29 April 2026. This commodity spike has pushed the US national average gasoline price to $4.229 per gallon, creating an immediate and unavoidable tax on average households that further accelerates the savings depletion cycle.

When evaluating historical stock market returns following periods where gasoline breached the $4.00 threshold, equities have routinely suffered double-digit declines as the compounding effects of sustained fuel costs erode discretionary corporate earnings.

Despite these escalating physical market risks, retail and institutional investors continue to project historically high levels of bullish sentiment. The AAII Investor Sentiment Survey for the week ending 23 April 2026 showed bullish sentiment sitting at 45.6%, with bearish sentiment trailing at just 27.8%. Financial professionals appear to be actively bypassing structural concerns regarding persistent inflation and petroleum constraints.

This systematic apathy leaves equity valuations highly exposed to external macro shocks. Main street pain has not yet translated into Wall Street exposure, creating a significant analytical blind spot for portfolio managers.

Specific future catalysts capable of triggering a severe market recalibration include:

- A sustained crude oil price above the $100 threshold, forcing immediate and unmanageable reductions in discretionary spending.

- A negative revision in top-tier consumer spending data, eliminating the final demographic support for retail aggregates.

- A rapid recalibration of algorithmic trading models to account for protracted supply chain and energy market disruptions.

The Final Tipping Point for US Equity Markets

The clash between unsustainable consumer habits and unpriced geopolitical realities has created a highly fragile domestic economic environment. The current period of strong retail data is a lagging indicator of past financial health rather than a forward-looking promise of continued economic expansion. The NRF has explicitly stated that they have not factored a drawn-out Middle East conflict into their 4.4% baseline growth forecast, leaving that projection highly vulnerable to revision.

The impending collision between $102.81 crude oil and a heavily depleted 4.0% personal savings rate leaves the US consumer with no remaining economic shock absorbers. Investors watching the growing divergence between consumer sentiment and actual market activity must prepare for a sudden structural contraction. The current environment demands critical evaluation of overly optimistic market narratives, as the mechanical limits of domestic consumer resilience have essentially been reached.

For readers interested in how these macroeconomic pressures threaten current valuations, our detailed coverage of S&P 500 mispricing explores why hitting year-end equity targets early has historically preceded severe drawdowns during periods of geopolitical instability.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.