Tesla Posts Record 480,126 Deliveries, Ending Two-Year Sales Slump

2 hrs ago

Berkshire Hathaway’s cash pile hit $397 billion in Q1 2026, a record that would rank it among the largest sovereign wealth funds on earth if it were a country. And yet its new chief executive just spent only $234 million of it buying back stock. The Q1 results, released 2 May 2026 alongside the annual shareholder meeting, represent the first full quarterly earnings under Greg Abel, who assumed the CEO role from Warren Buffett at the start of the year. Investors and analysts are reading every line for signals about whether Berkshire’s capital allocation philosophy will shift or hold. What follows is a breakdown of what the numbers show, what the buyback resumption means, how the subsidiaries performed, and what Abel’s early decisions reveal about the direction of one of America’s most influential conglomerates.

The headline number looked strong. Berkshire Hathaway reported operating earnings of $11.35 billion for Q1 2026, an 18% increase from the $9.64 billion posted in Q1 2025.

Q1 2026 Operating Earnings: $11.35 billion, up 18% year-over-year

Then came the complication. The result missed the FactSet analyst consensus of $11.56 billion, a gap of roughly $210 million that reframed a strong absolute quarter as a modest shortfall against expectations.

The miss matters less for its size than for its timing. This was Abel’s first full quarterly report as CEO, released on 2 May 2026 concurrent with the annual meeting. Expectations had been set high, and the underlying performance, while solid, did not clear the bar Wall Street had established for the new leader’s opening act.

Forward guidance signals have consistently moved markets more than reported results in recent quarters, a dynamic that applies directly to Berkshire: with no acquisition announcements and no deployment timeline given, what Abel says at future investor events may matter more than what the income statement shows.

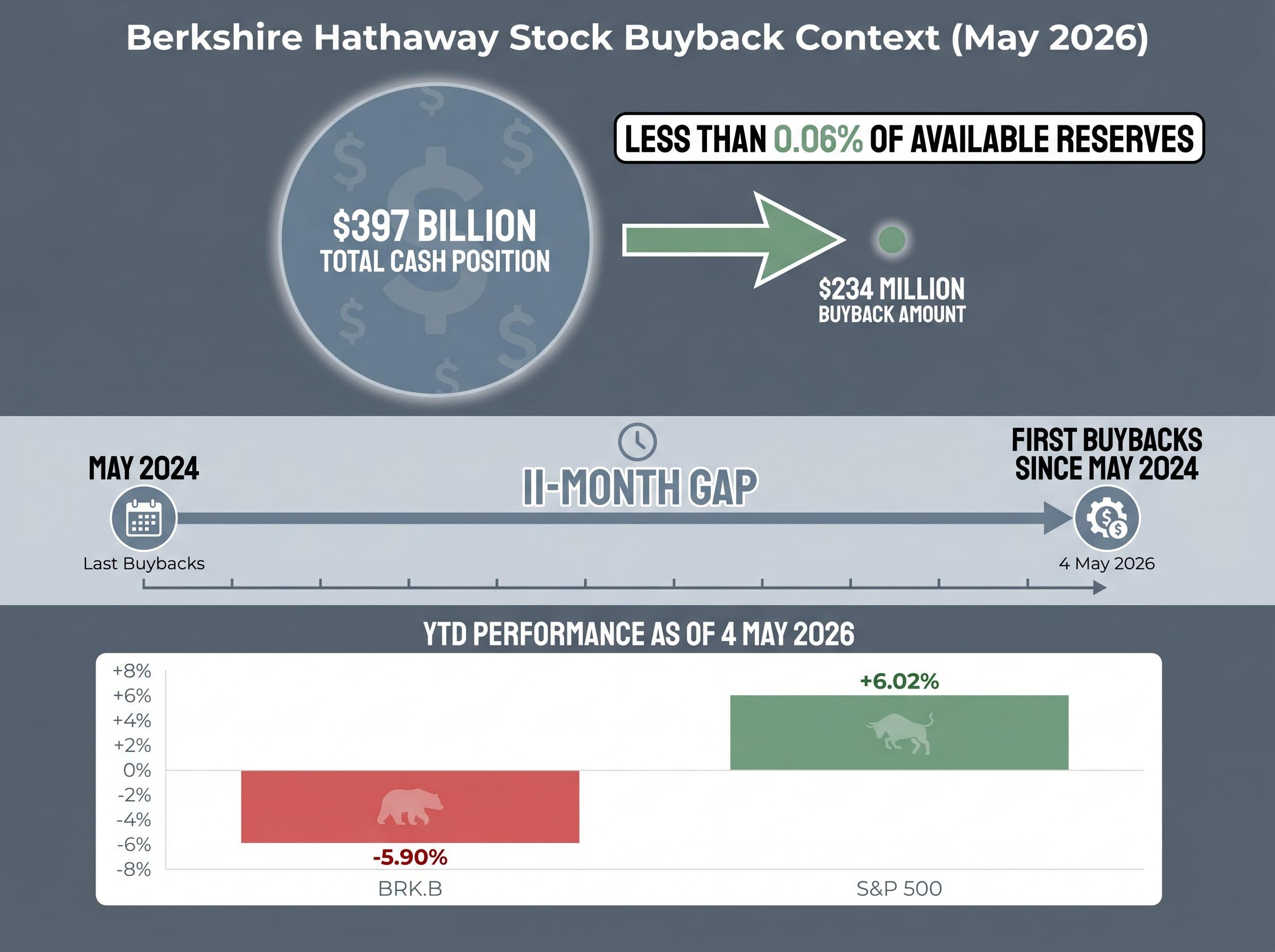

The cash pile grew again. Berkshire’s reserves rose to a record $397.38 billion, up from $373 billion the prior quarter, a single-quarter increase of more than $24 billion.

That accumulation continued despite no shortage of market activity. Berkshire offloaded $24.1 billion in equities while purchasing $15.9 billion, producing net stock sales of $8.2 billion and extending the company’s streak as a net seller to 14 consecutive quarters.

The sovereign wealth fund rankings maintained by the SWF Institute place the largest state-controlled reserves in the $300-900 billion range, a scale that contextualises Berkshire’s $397 billion cash position as genuinely comparable to the world’s most capitalised government investment vehicles.

| Period | Cash Reserves | Net Equity Position | Direction |

|---|---|---|---|

| Q4 2025 | $373 billion | Net seller | Accumulating |

| Q1 2026 | $397 billion | Net seller ($8.2B net sold) | Accumulating |

The restraint is itself the signal. Abel is not sitting on cash because he lacks authority to deploy it. He is operating in the Buffett tradition of disciplined patience when valuations do not meet Berkshire’s criteria. Fourteen quarters of net selling under two different CEOs suggests a consistent reading of the opportunity set, not indecision at the top.

The scale of Berkshire’s cash accumulation is not just a corporate balance sheet story; it also functions as a live reading of equity market conditions, with the Buffett Indicator, the ratio of total US market capitalisation to GDP, sitting near 223-230% across late 2025 and early 2026, territory historically associated with suppressed forward returns.

Berkshire’s insurance operations delivered the quarter’s strongest segment result. Overall insurance underwriting earnings grew 28% to $1.717 billion in Q1 2026, providing the single largest driver of the operating earnings increase.

The breadth of subsidiary contribution insulated the overall result from any single line of weakness. BNSF, the energy segment, and manufacturing businesses all added to operating growth, though FX headwinds trimmed the aggregate gains.

Geico’s underwriting earnings declined during the quarter due to higher claims costs, a pattern that diverged from the broader insurance unit’s strong showing. Berkshire’s Q1 report confirmed lower results at the auto insurer without specifying a percentage decline, and no independently verified figure has been published.

The softness is worth monitoring. Geico is one of Berkshire’s most visible consumer-facing businesses, and sustained claims inflation could weigh on the insurance segment’s trajectory in coming quarters even as the broader underwriting book performs well.

Berkshire repurchased $234 million in shares during Q1 2026, the first buybacks since May 2024, a gap of approximately 11 months.

The dollar figure is small. Against a $397 billion cash position, $234 million amounts to less than 0.06% of available reserves. The significance is not in the size of the repurchase but in the fact that it happened at all.

BRK.B is down 5.90% year-to-date as of 4 May, compared with the S&P 500’s gain of 6.02% over the same period.

The resumption signals that Abel views Berkshire shares as attractively valued at current prices, a meaningful data point given the stock’s underperformance relative to the broader market. That no repurchases occurred in early April reinforces Berkshire’s established pattern: buybacks are opportunistic and price-sensitive, not scheduled.

Berkshire Hathaway reports operating earnings as its primary performance metric. This figure captures pre-tax earnings from wholly owned subsidiaries, including insurance, railway, energy, and manufacturing businesses, while excluding investment gains and losses.

The distinction matters because Berkshire’s GAAP net income, the standard accounting measure, includes unrealised gains and losses from its public equity portfolio. That portfolio is large enough to swing net income by billions in either direction based purely on stock market movements, not underlying business results.

Buffett long advocated for investors to focus on operating earnings as the cleaner measure of business health. Abel has continued this framework. In a quarter where the equity portfolio can add or subtract billions based on market swings alone, operating earnings isolate what the businesses themselves produced: $11.35 billion, up 18%.

Abel’s first full quarter reads as a statement of continuity. Methodical net selling, disciplined cash accumulation, a modest buyback resumption, and no acquisition announcements. The playbook is Buffett’s, executed by a different hand.

Abel’s investment aperture may be wider than Buffett’s in at least one measurable way: his addition of an Alphabet stake in late 2025 introduced AI-adjacent exposure that his predecessor largely avoided, a detail that complicates any reading of his first quarter as pure continuity.

Analysts characterise Abel’s approach as continuity-focused, with no signals of near-term large acquisitions or strategic pivots.

On 4 May 2026, BRK.B closed at $473.01, down 0.12% intraday, a muted reaction that reflects a market absorbing an expected result rather than repricing around a surprise. The question investors are asking is not whether Abel can run the business. Q1 suggests he can. The question is when, and at what scale, he will deploy a cash reserve that cannot grow indefinitely without a deployment decision.

Signals to watch in Q2 2026 and beyond:

The quarter provides a three-part verdict:

What Q1 does not resolve is the larger question: when and how the cash gets deployed at scale. Abel has earned credibility by demonstrating restraint in a market he appears to view as offering limited value. The next several quarters will reveal whether that restraint gives way to action, or whether patience itself becomes the defining feature of the Abel era.

Investors wanting to situate Berkshire’s result within the broader reporting cycle will find our full explainer on the Q1 2026 earnings season, which examines how a blended S&P 500 growth rate of 27.1% developed, where analyst estimates diverged most sharply from outcomes, and which macro headwinds, including rising Treasury yields and a softening labour market, could compress forward estimates heading into summer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Berkshire Hathaway reported Q1 2026 operating earnings of $11.35 billion, an 18% increase from $9.64 billion in Q1 2025, though the result fell slightly short of the FactSet analyst consensus of $11.56 billion.

Berkshire's $397 billion cash reserve reflects disciplined capital allocation under both Warren Buffett and Greg Abel, who have been net sellers of equities for 14 consecutive quarters, indicating that current market valuations do not meet Berkshire's investment criteria.

Berkshire repurchased $234 million in shares during Q1 2026, its first buyback since May 2024, signalling that Greg Abel views Berkshire shares as attractively valued at current prices, even though the dollar amount represents less than 0.06% of available cash reserves.

Abel's first full quarter as CEO shows strong continuity with Buffett's approach, including disciplined cash accumulation and no major acquisitions, though his addition of an Alphabet stake in late 2025 introduced AI-adjacent exposure that Buffett had largely avoided.

Berkshire reports operating earnings as its primary metric because GAAP net income includes unrealised gains and losses from its large public equity portfolio, which can swing by billions based on stock market movements rather than reflecting actual business performance.