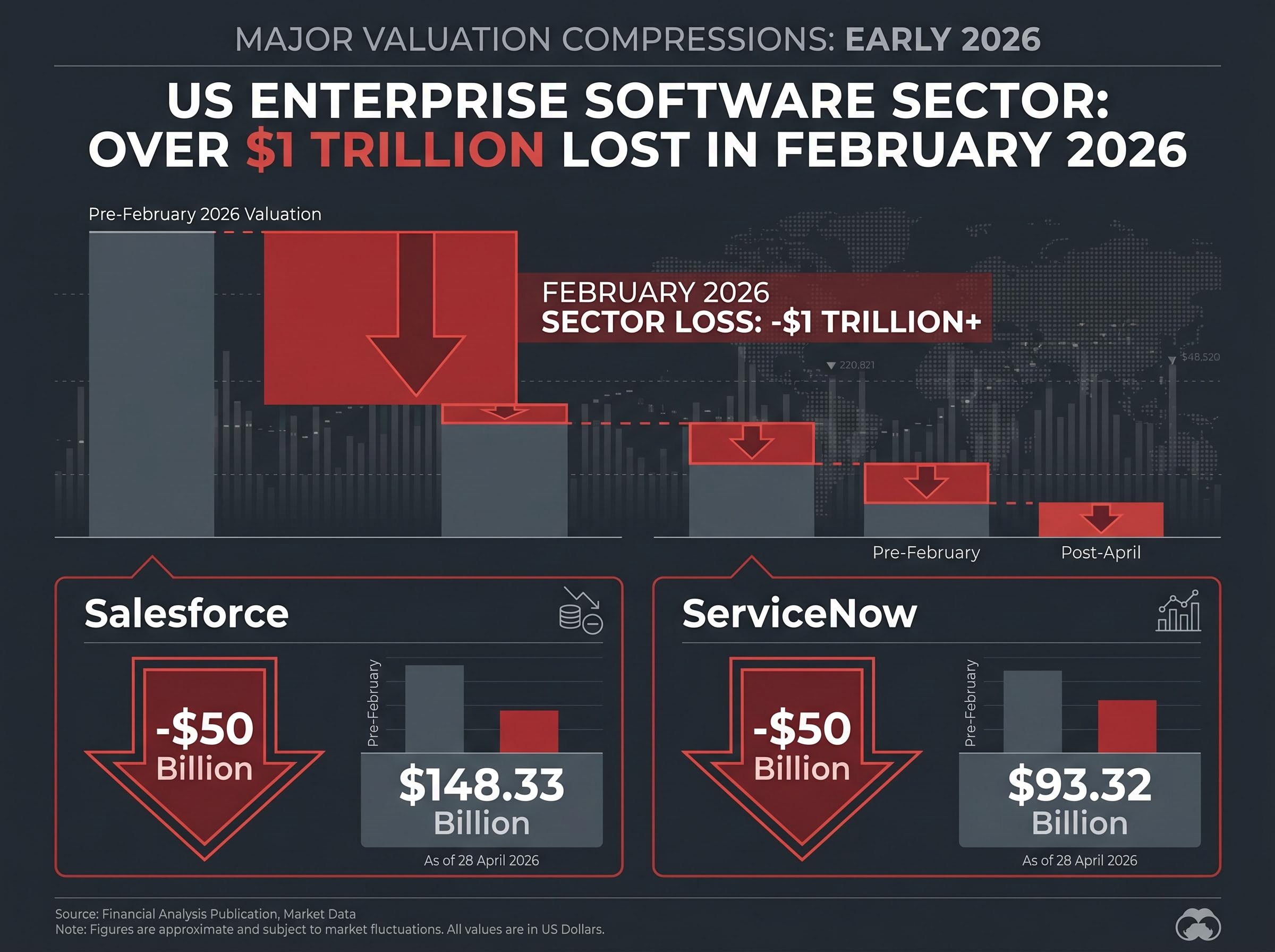

The US enterprise software sector lost over $1 trillion in aggregate market capitalisation over a single month in February 2026. This sudden erasure of value highlights how severely the AI market disruption is unwinding traditional software business models. Institutional capital is abandoning legacy per-seat licensing structures and rapidly rotating into pure-play generative technology startups. The speed of this capital reallocation caught many traditional technology funds unprepared for the resulting valuation compressions.

This analysis examines the mechanics of this value transfer across the United States technology sector. It details how autonomous agents are dismantling the financial foundations of software-as-a-service providers. The resulting flight to quality has created a concentrated boom in specialised marketing technology platforms. By examining Wall Street forecast revisions and defensive acquisition strategies, investors can identify where institutional money expects the highest future returns.

The trillion dollar haemorrhage in US enterprise software

The severity of the February 2026 selloff shocked institutional investors holding legacy technology portfolios. Over $1 trillion in market capitalisation vanished from established US technology providers in a matter of weeks. The punishment was swift, reflecting growing consensus that new autonomous technologies present existential risks to established commercial models.

The Wall Street Journal reported heavily on this capital flight, noting that traditional software metrics no longer justify historical valuation multiples.

Market Outlook Warning “Capital is shifting rapidly away from legacy SaaS models toward generative AI providers, creating an existential risk to traditional software business models that rely on volume-based human licensing.”

Examining the localised damage across major tech firms

The financial damage across US tech stalwarts remained severe through late April 2026. Salesforce lost over $50 billion in market capitalisation, dropping to a $148.33 billion valuation by 28 April 2026. The company faces mounting competition from automated agent networks that bypass their core customer relationship management interfaces.

ServiceNow mirrored this structural decline during the exact same trading period. The workflow automation company lost over $50 billion to land at a $93.32 billion market cap yesterday. Other heavily impacted firms like Microsoft, Intuit, and AppLovin experienced notable valuation compressions as their future earnings projections were revised downward.

These market capitalisation losses reflect broader Wall Street anxiety rather than isolated company failures. Analysts point to a fundamental repricing of the entire sector as investors re-evaluate long-term earnings potential.

For investors navigating this volatile reporting season, our dedicated guide to AI stock earnings and capital expenditures explores how mega-cap software buyers must justify their historic infrastructure spending to prevent further valuation corrections.

When big ASX news breaks, our subscribers know first

Decoding the threat: How autonomous agents break traditional SaaS

The technical mechanics driving this capital flight centre on the shift from traditional software applications to generative artificial intelligence. For decades, traditional software-as-a-service relied entirely on a per-seat pricing model. Companies paid individual subscription fees for human operators to access software interfaces.

Autonomous AI agents automate functions that previously required multiple human operators and their corresponding software licenses. Anthropic, a leading developer, introduced tools like Anthropic Cowork to execute complex digital tasks independently. This agent functions without continuous human supervision, directly removing the need for individual software seats. A single autonomous workload can replace dozens of standard user subscriptions.

As businesses scale these automated workflows, they are beginning to deploy interoperable enterprise agentic networks that connect multiple independent decision architectures across different departments.

The core differences between traditional limitations and autonomous capabilities include:

Execution capacity: Traditional models require a human user to drive the software interface, while autonomous agents complete multistep workflows independently. Licensing economics: Legacy models scale revenue through individual seat licenses, whereas artificial intelligence models scale through compute volume and workload execution. * Operational integration: Conventional software isolates data within specific applications, while autonomous agents operate across multiple platforms to synthesise information.

Understanding this shift provides the foundational explanation for the market crash. A technology that executes tasks independently directly cannibalises the revenue streams of established software vendors. Investors must evaluate which business models will survive this structural transition from human-operated software to autonomous task execution.

Capital rotation and the rapid rise of pure play AI MarTech

Capital did not simply evaporate during the first quarter of 2026; it reallocated toward specialised innovators. A massive influx of venture capital flowed directly into marketing technology platforms built natively on generative architecture. These startups prioritise rapid product expansion and synthetic media generation over near-term net earnings.

To maintain this aggressive expansion pace, many of these pure-play AI firms rely heavily on autonomous coding agents to multiply their software development output and bypass the traditional hiring bottlenecks that slowed legacy competitors.

Profound, a visibility platform designed for brands navigating generative search, exemplifies this aggressive funding trajectory. The company secured a $35 million Series B round led by Sequoia Capital in August 2025. By February 2026, Profound raised an additional $96 million in a Series C round, achieving a $1 billion valuation.

According to company data, simultaneously, a prominent custom artificial intelligence ad-tech firm secured $150 million in April 2026 at a $2.75 billion valuation. This represented a substantial increase from its valuation in February 2025. According to company data, the firm crossed $100 million in recurring revenue, backed by elite institutional investors including Goldman Sachs, Bain Capital Ventures, and TD7.

The company secured major client adoption from enterprise brands. These institutional funding moves provide a clear blueprint for identifying the next generation of enterprise technology winners.

| Company Profile | Funding Stage | Date | Capital Raised | Reported Valuation |

|---|---|---|---|---|

| Profound | Series B | August 2025 | $35M | Undisclosed |

| Profound | Series C | February 2026 | $96M | $1.0B |

Synthetic media and the new operational standard

New platforms merge synthetically generated elements with authentic customer archives to maintain brand alignment. This operational shift stems from a 2023 realisation that existing automated solutions repeatedly failed advertising professionals. The current generation of tools solves this deficiency by generating bespoke creative assets at scale without human intervention.

Navigating the chaos: Conflicting market forecasts for 2026

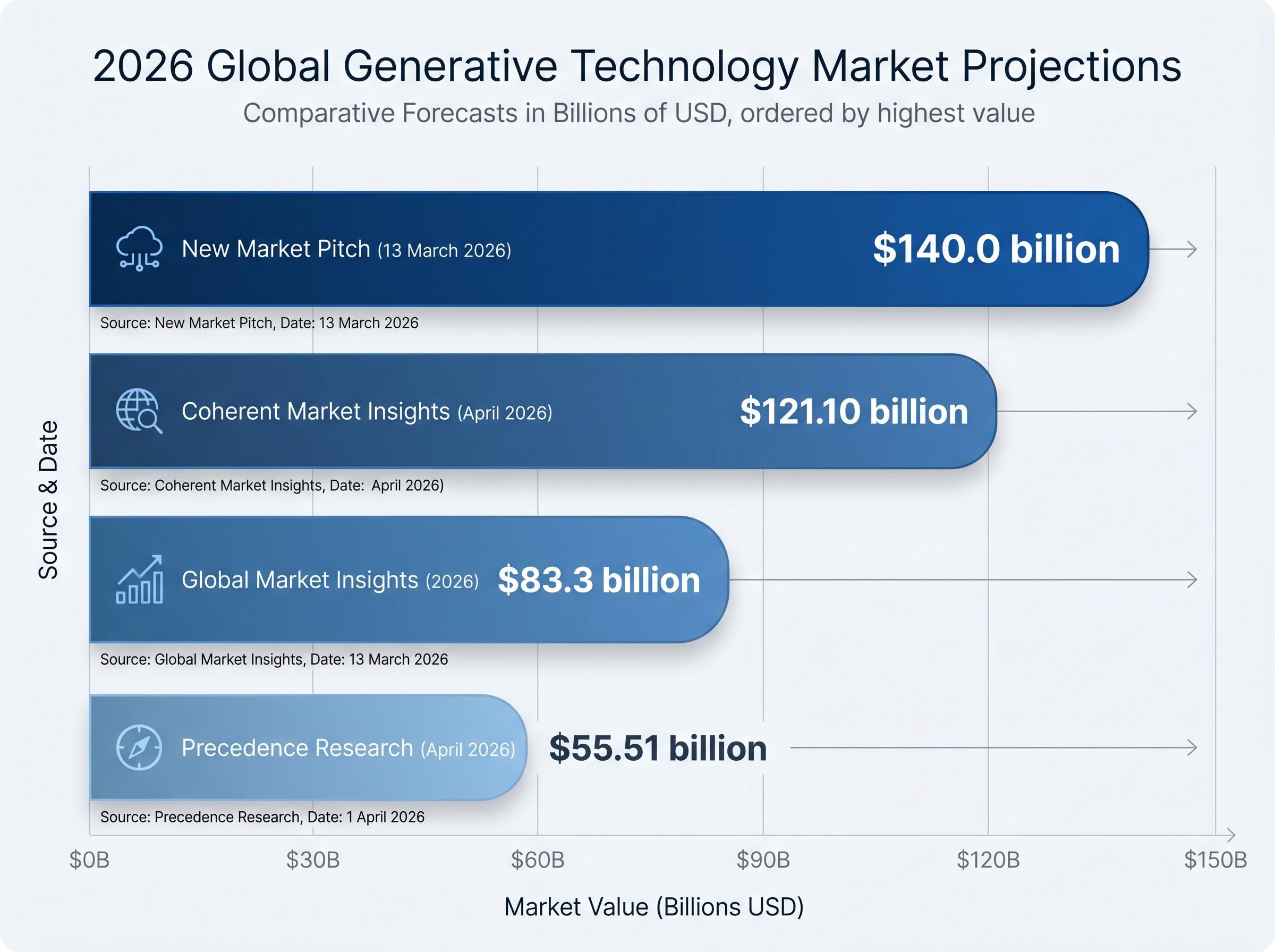

The rapid funding rounds contrast sharply with divided consensus among major research firms regarding the sector’s commercial ceiling. Analyst projections for the global generative technology market size in 2026 show a massive and conflicting forecasting spread. This analytical friction exposes the current investment environment as highly speculative despite concrete venture capital commitments.

This massive forecasting spread complicates capital allocation strategies for institutional investors aiming to build balanced portfolios. The direction of the trend is clear, but the absolute commercial ceiling remains deeply uncertain. Investors must navigate these wildly differing projections when weighting their technology exposure.

| Research Firm | Forecast Publication Date | 2026 Global Market Size Projection |

|---|---|---|

| New Market Pitch | 13 March 2026 | $140.0 billion |

| Coherent Market Insights | April 2026 | $121.10 billion |

| Global Market Insights | 2026 | $83.3 billion |

| Precedence Research | April 2026 | $55.51 billion |

Research models diverge significantly based on how quickly analysts expect enterprise adoption to translate into recognised revenue. For instance, Global Market Insights models its $83.3 billion projection from a 2025 baseline of $53.7 billion. This lack of consensus protects prudent investors from blind optimism by highlighting the severe unpredictability of short-term commercial outcomes.

The consolidation defence: Legacy giants turn to acquisitions

Established technology conglomerates are responding to the startup threat through aggressive mergers and acquisitions. These actions serve as defensive manoeuvres designed to bolt modern capabilities onto aging product suites. Legacy giants are effectively attempting to buy their way out of obsolescence to protect their historical market share.

These corporate maneuvers are happening alongside massive AI infrastructure investments from hyperscalers, creating a dual-front war where established players must simultaneously fund physical hardware expansion and specialized software acquisitions.

Adobe executed this survival playbook by finalising a $1.9 billion cash acquisition of Semrush on 19 November 2025. The transaction signals an aggressive attempt by legacy creative vendors to secure their footing in the new ecosystem. This strategy mirrors the 2008-era legacy acquisition playbook, contrasting sharply against the organic growth of natively founded AI firms.

Industry analysts are actively evaluating whether these acquisitions can successfully stave off the fundamental disruption of core business models. The primary strategic motivations behind these acquisitions include:

- Acquiring established engineering talent to accelerate internal product development timelines.

- Absorbing direct market competition before early-stage startups achieve unassailable operational scale.

- Integrating native generative capabilities into existing software interfaces to prevent immediate customer churn.

This pattern demonstrates how traditional tech stocks might still salvage shareholder value through strategic capital deployment.

The future architecture of enterprise software operations

The core tension between the $1 trillion legacy selloff and the billions flowing into custom media platforms defines the current market cycle. Corporate technology procurement will shift dramatically over the next 12 to 18 months as autonomous tools become the default operational standard. Enterprise software stacks will increasingly feature independent agent networks rather than isolated, human-operated applications.

Investors must recognise that legacy technology portfolios carry significant structural risk if their underlying companies fail to adapt their licensing models. The rapid capital rotation into synthetic media and visibility platforms signals where institutional money expects the highest future returns. Forward-looking portfolios will likely need to balance defensive legacy holdings with direct exposure to native generative platforms.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.