Why Your ETF Portfolio May Be Less Diversified Than You Think

17 hrs ago

A financial strategy can be mathematically sound and personally catastrophic at the same time. The difference has nothing to do with the maths. It has everything to do with who is applying it.

The problem is that you almost never hear from the people who applied these strategies and lost. Survivorship bias means the books, podcasts, and social media threads overwhelmingly feature people who leveraged, concentrated, or speculated their way to wealth. What those accounts routinely leave out are the structural prerequisites that made the strategy survivable for them specifically: diversified collateral, access to dozens of independent deals, and operational control over the businesses they held. In the American financial media environment, leverage, stock concentration, and asymmetric bets are presented as universally applicable playbooks. They are not.

Here is the framework for separating financial rules that work across all wealth levels from those that quietly require a structural position most readers do not have.

The distortion is not about dishonesty. It is structural. Investors who suffered serious losses rarely become public voices for the approach that cost them. They do not write bestsellers, build large audiences, or document the strategy that destroyed their finances. That systematic silence skews the public record heavily toward survivors, inflating the apparent safety and replicability of high-risk strategies in ways that accurate, well-intentioned advice cannot easily undo.

When a genuinely successful investor explains what produced their results, the account is almost always specific to conditions they held at the time, conditions they may take for granted and never explicitly mention.

Three structural prerequisites appear repeatedly behind the strategies most often promoted as universally applicable:

Financial rules requiring only patience and discipline remain valid at any wealth level. Rules depending on collateral, deal access, or business control do not. The distinction between “this worked for me” and “this works” is the central problem with retail financial advice, and it is the lens the rest of this piece applies to three of the most common strategies you will encounter.

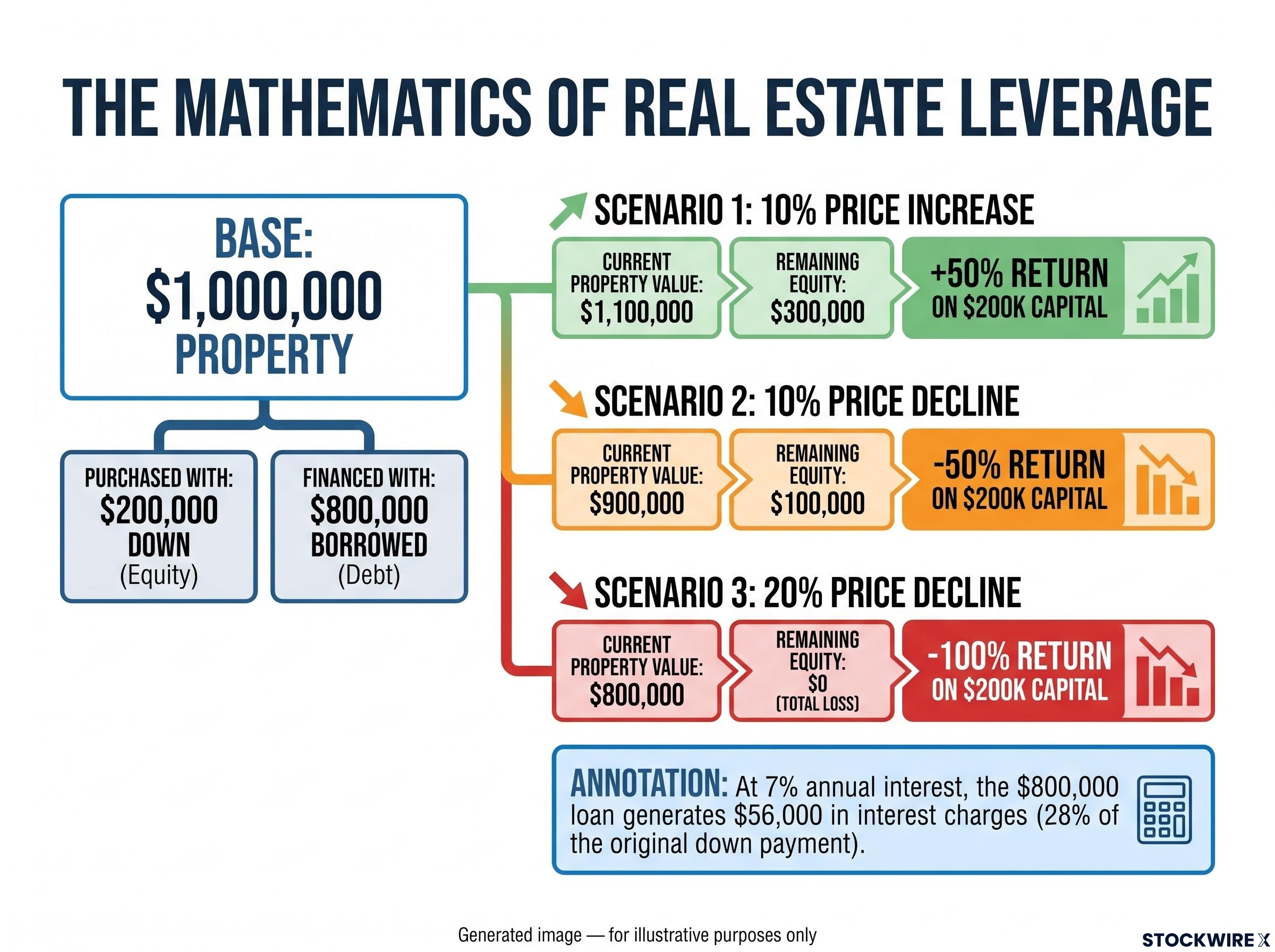

Leverage is mathematically symmetrical. It amplifies gains and losses with identical force. The variable that determines whether leveraged investing is survivable is not the asset itself; it is how diversified the borrower is.

The margin mechanics that govern leveraged products convert percentage price moves into amplified capital outcomes by a fixed multiplier, meaning a 5% adverse move on a 5:1 leveraged position produces a 25% loss on deployed capital, not a 5% loss, a distinction that changes the survivability calculation entirely.

A concrete scenario makes this visible. Take a $1,000,000 property purchased with $200,000 down and $800,000 borrowed.

| Scenario | Property Value | Remaining Equity | Return on $200k Capital |

|---|---|---|---|

| 10% price increase | $1,100,000 | $300,000 | +50% |

| 10% price decline | $900,000 | $100,000 | -50% |

| 20% price decline | $800,000 | $0 | -100% |

The symmetry is precise. A 10% rise in value delivers a 50% return on the capital actually deployed. A 10% fall strips away half of that equity. A 20% decline wipes out the full $200,000 contributed while leaving the $800,000 debt entirely unchanged. The borrower carries the full loan against a property now worth exactly what is owed on it.

At 7% annual interest, the $800,000 loan generates approximately $56,000 in interest charges in year one alone. That figure represents 28% of the original down payment, payable even if the property neither rises nor falls in value.

That cost accumulates whether the asset rises, falls, or sits flat. A standard residential mortgage is recourse debt secured against what is, for most borrowers, their single largest and most concentrated holding. The debt obligation persists regardless of what the asset is worth.

The structural divide is not about the percentage move. For a wealthy, diversified investor, a 20% loss on one leveraged property is a painful portfolio event absorbed across a larger holding. For you, if your net worth is largely concentrated in that single property, the identical move is total financial wipeout with recourse debt still attached. Many leverage blowups arise not from ultimate asset values but from timing: margin calls, job loss, or refinancing shocks that force liquidation before prices recover. A leveraged position on your primary asset is not the same strategy as a leveraged position within a large diversified portfolio, even though the promoter describing it will use exactly the same words.

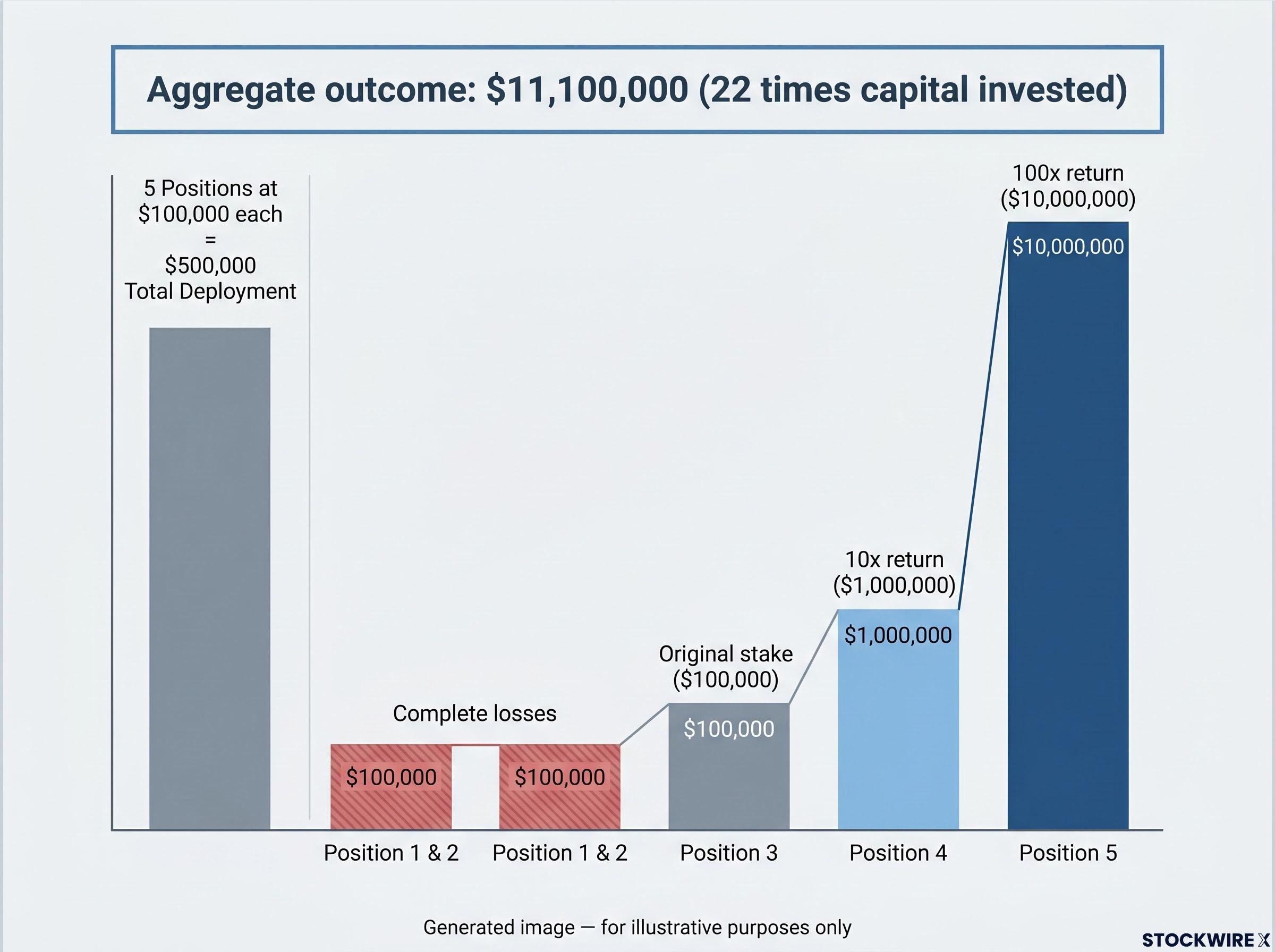

Venture capital returns follow a power-law distribution. Most investments fail. A small number break even. A tiny fraction produce extreme outliers that carry the entire fund. The strategy works because it is a portfolio phenomenon, not a single-bet phenomenon.

Equity returns follow a power-law distribution, not the bell curve that intuition assumes, and that structural asymmetry is precisely why venture capital’s portfolio logic cannot be replicated with one or two speculative positions in correlated assets.

To illustrate, imagine a hypothetical five-position fund committing $100,000 to each position, a total deployment of $500,000. The first two positions are complete losses. The third returns the original stake and nothing more. The fourth multiplies the investment tenfold. The fifth generates a 100x return. The aggregate outcome across all five is roughly $11,100,000, representing approximately 22 times the capital invested. The two total failures are absorbed entirely by the exceptional returns of the winners.

Retail financial content routinely reframes speculative positions in stocks, crypto, or early-stage companies as “asymmetric bets.” What is almost never included is the second half of the argument. Asymmetric bets are genuinely rational under only two conditions:

Without either condition, the maths works against you. A single speculative bet with a 10% probability of a 5x payout and a 90% probability of total loss has an expected value of $500 on a $1,000 investment.

On a $1,000 outlay, an expected value of $500 means the position is worth half what was paid for it. That outcome is not a favourable asymmetry. It is a negative expected-value transaction dressed in the language of venture investing.

Retail speculative positions tend to cluster in correlated assets, instruments that rise and fall together. This eliminates the independence that makes portfolio-level expected value function. If you are placing one or two speculative bets in correlated assets, you are not deploying venture logic. You are accepting concentrated risk while borrowing the language of a fundamentally different strategy.

Research by Hendrik Bessembinder on lifetime dollar wealth creation in U.S. equity markets examined nearly 26,000 stocks from 1926 onward. The findings quantify something most concentration advocates never mention.

Across the full sample, over four in seven stocks delivered returns below those of a one-month Treasury bill across their entire listed lifetime. Companies that were ultimately delisted had typically shed more than 90% of their value before removal. Roughly 96% of all stocks in the study produced collective returns that merely kept pace with Treasury bills in aggregate. The wealth-creating work was done almost entirely by the remaining 4%.

Within that top-performing group, just 86 companies out of nearly 26,000 were responsible for generating around half of all stock market wealth produced across the study period.

The compounding cost of concentration operates across three separate drag layers simultaneously: the base-rate disadvantage of picking among thousands of stocks, the tax friction generated by active turnover, and the behavioural penalty of reacting to volatility rather than holding through it.

The public narrative around concentration is dominated by investors who correctly identified those rare outliers. The base rate says a small portfolio of individual stocks is overwhelmingly more likely to miss them than to capture them. The far larger population of investors who concentrated and experienced chronic underperformance, or outright wipeout, does not produce visible public narratives.

The distinction matters. Two forms of concentration operate under fundamentally different structural conditions:

One of the most celebrated proponents of concentrated investing is reported to have directed in personal estate planning documents that assets intended for family members be placed 90% into a low-cost S&P 500 index fund. That instruction draws a clear line between the approach used to generate a fortune, which depended on an exceptional personal edge, and the approach considered appropriate for sustaining it. Concentrated stock picking without insider knowledge or operational control is not a different version of what those advocates did. It is a structurally different activity with materially different odds.

The structural prerequisites identified above convert into a set of diagnostic tests you can apply to any financial strategy you encounter. Each question is tied to a specific hidden requirement. A strategy that fails two or more of them is not suited to your balance sheet, regardless of how well it worked for someone else.

Approaches requiring nothing more than patience and discipline hold up at any level of wealth. Approaches that depend on collateral, deal access, or operational control do not transfer so cleanly. That gap is the real dividing line.

The contrast case is worth stating. Broad index fund ownership, accumulating equity through saving rather than borrowing, and long holding periods all carry positive expected value without requiring any structural advantage. They work precisely because they do not depend on starting conditions most people lack.

The strategies examined in this piece are not false. They are designed for a balance sheet that their promoters possess and that most listeners do not. Mathematical correctness and practical applicability are separable concepts, and the gap between them is where ordinary investors sustain the most avoidable damage.

| Strategy | What Promoters Typically Have | What Most Investors Lack |

|---|---|---|

| Leverage | A portfolio of assets spread across multiple holdings, with the capacity to absorb losses on any single position without facing insolvency | Single major asset; recourse debt; forced-sale vulnerability |

| Asymmetric bets | Many uncorrelated positions; capital to absorb repeated losses | One or few correlated bets; stakes meaningful to net worth |

| Stock concentration | Deep insider knowledge; operational control; information edge | Public information only; no control; no structural edge |

The five diagnostic questions are your portable tool. They apply not just to leverage, asymmetric bets, and concentration but to any wealth-building approach you encounter going forward. Run the strategy through the questions. If the structural prerequisites are not present in your own balance sheet, the strategy is not designed for your situation, however well it may have worked for the person promoting it.

The most powerful approaches for most investors, broad index ownership, patient compounding, and avoiding leverage against concentrated assets, require no special structural advantages at all. That is precisely their value.

Active manager underperformance is not a run of bad luck confined to a particular market cycle; two decades of SPIVA data show over 90% of large-cap fund managers failing to beat the S&P 500 over a 20-year horizon, a result William Sharpe’s arithmetic principle confirms must hold in aggregate after costs.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Survivorship bias in financial advice occurs because investors who lost money using high-risk strategies rarely become public voices, so the public record is dominated by the people who succeeded, making leverage, concentration, and speculative bets appear far safer and more replicable than they actually are.

Wealthy investors typically hold leverage as one position within a diversified portfolio, so a 20% loss on a single asset is absorbed across other holdings; for most investors whose net worth is concentrated in one leveraged asset like a primary home, the identical move produces total financial wipeout with recourse debt still attached.

Venture capital works as a portfolio strategy because extreme outlier returns from a tiny fraction of investments absorb all the losses; retail investors making one or two speculative bets in correlated assets cannot generate portfolio-level expected value, making the asymmetric bet framing cosmetic rather than structurally sound.

Bessembinder's study of nearly 26,000 U.S. stocks from 1926 onward found that over four in seven stocks returned less than a one-month Treasury bill across their entire listed lifetime, and just 86 companies were responsible for generating roughly half of all stock market wealth produced across the full period.

Broad index fund ownership, accumulating equity through saving rather than borrowing, and long holding periods all carry positive expected value without requiring diversified collateral, deal access, or operational control, which is precisely what makes them applicable regardless of starting wealth.