How the US Government Became Intel’s Investor and Deal Broker

17 hrs ago

Wall Street had Meta Platforms’ AI infrastructure costs wrong by a factor of nearly two. That is not a rounding error. It is a measurement failure worth billions of dollars in implied compute capacity, and it explains why META shares moved almost 6% on 10 July 2026.

The stock rally was not triggered by a product launch or an AI model announcement. It was triggered by an internal company memo, reviewed and reported by Reuters, that revealed Meta is building AI compute infrastructure at roughly half the cost analysts had been modelling. For institutional investors who had been pricing in a capital allocation concern, specifically that $145 billion in capital expenditure might not generate adequate returns, the memo reframed the question entirely. The market did not react to a new capability. It reacted to a recalibration of return expectations on capital already committed.

Here is what the cost data actually tells you about whether Meta’s infrastructure spend is a liability or an asset, and the analytical framework you need to form your own view on that question.

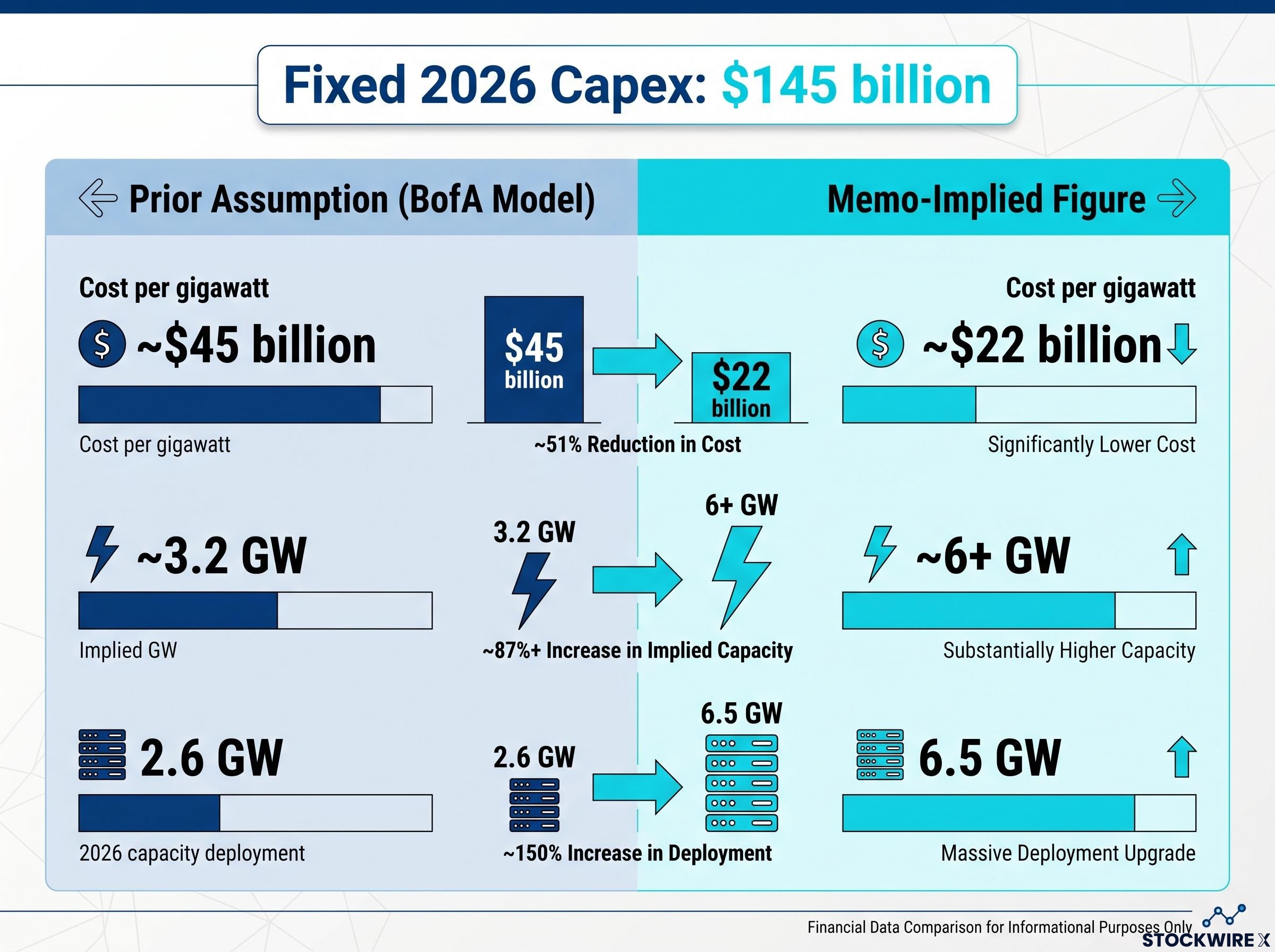

Before the memo surfaced, the standard Wall Street assumption for hyperscaler AI infrastructure was approximately $45 billion per gigawatt of compute capacity. That figure was the baseline BofA Securities analyst Justin Post and his peers used to model Meta’s capex returns. At that rate, $145 billion in 2026 capital expenditure implied roughly 3.2 GW of deployable capacity.

The memo told a different story. Based on the internal document reported by Reuters, Post revised BofA’s per-gigawatt cost estimate to approximately $22 billion. At that rate, the same $145 billion implies more than 6 GW of capacity.

At $45 billion per gigawatt, $145 billion buys approximately 3.2 GW. At $22 billion per gigawatt, the same capex buys more than 6 GW. The dollar commitment has not changed. The compute it purchases has nearly doubled.

The scale shift is further underscored by the capacity deployment figures. BofA’s prior 2026 model had assumed 2.6 GW of new capacity additions, while the memo points to a total of 6.5 GW for the year. Of that, around 1 GW had already come online by mid-2026, with the remaining 5.5 GW scheduled to be brought into service across the second half.

| Metric | Prior Assumption | Memo-Implied Figure |

|---|---|---|

| Cost per gigawatt | ~$45 billion | ~$22 billion |

| Implied GW from $145B capex | ~3.2 GW | ~6+ GW |

| 2026 capacity deployment estimate | 2.6 GW (BofA prior) | 6.5 GW (memo-implied) |

Meta is not simply spending less per unit. It is deploying nearly twice the compute its capex budget would have implied under the old model. For anyone evaluating the return potential of a fixed dollar of Meta infrastructure investment, the math has approximately doubled.

The natural follow-up question is whether the $22 billion figure reflects genuine operational efficiency or a one-time condition that flatters the numbers. The evidence points toward the former.

The $145 billion capex guidance range ($125-$145 billion, per Meta’s Q1 2026 earnings) is not a pure construction figure. It includes several distinct cost categories:

That composition matters. Memory and advanced packaging inflation has been a sector-wide headwind in 2026, affecting every major cloud and AI infrastructure builder. Meta achieved its $22 billion per gigawatt figure despite those input cost pressures, not because inputs were cheap. That tells you the efficiency gains appear to reflect operational and procurement decisions rather than favourable market timing, which is directly relevant to how durable the advantage is likely to be.

The $22 billion figure is a blended implied cost. Meta’s 14 GW infrastructure plan across 2026-2027 includes both internally built data centres and contracted third-party cloud capacity, and the company has not publicly disclosed the split between owned and outsourced.

That distinction matters for durability. Owned infrastructure typically carries different long-term unit economics than contracted cloud capacity, and the blended cost figure could shift materially depending on which side of the mix grows faster. This is not a red flag; it is the next data point investors should expect from upcoming earnings disclosures.

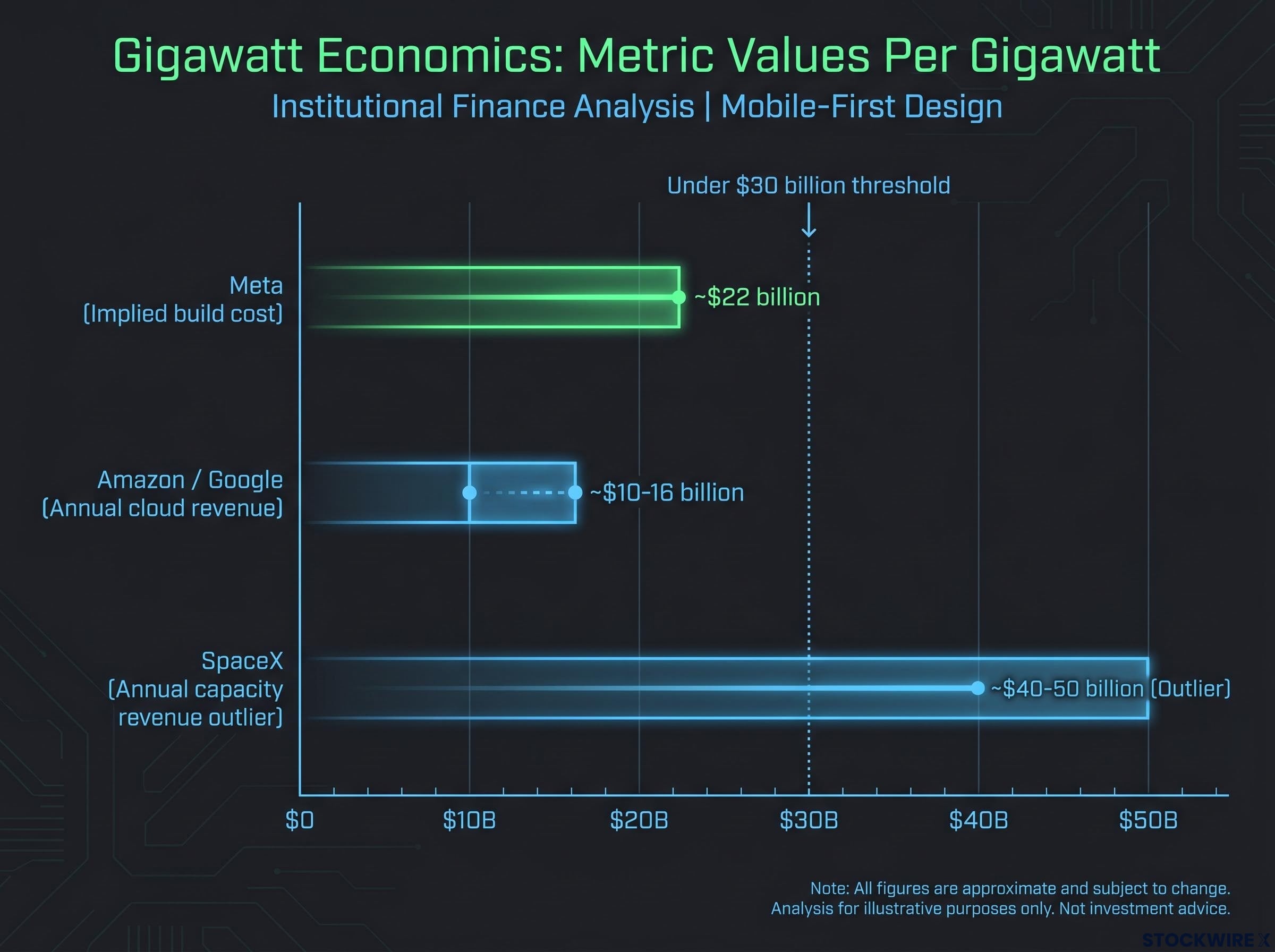

The competitive picture requires a specific kind of comparison. BofA’s benchmarking is not a build-cost-to-build-cost exercise. It measures Meta’s construction cost against the annual revenue that comparable infrastructure generates at rivals.

Amazon and Google generate an estimated $10-16 billion in annual cloud revenues per gigawatt of deployed infrastructure, according to BofA. Meta’s implied build cost sits at $22 billion per gigawatt.

Hyperscaler revenue per gigawatt is not a uniform figure: Google Cloud grew 63% year-over-year in Q1 2026 while AWS posted its fastest quarterly growth in over three years, meaning the $10-16 billion annual revenue benchmark used to evaluate Meta’s payback window reflects a range with meaningful variance depending on workload mix, customer concentration, and infrastructure cluster maturity.

The payback logic follows directly. If comparable infrastructure generates $10-16 billion per year in revenue, a $22 billion build cost implies a payback window somewhere in the range of 18 months to under three years.

According to BofA, constructing AI capacity at under $30 billion per gigawatt produces economics that compare very favourably against the $10-16 billion in annual cloud revenue per gigawatt that Amazon and Google generate, and against contracted capacity deals such as those attributed to SpaceX in the $40-50 billion per gigawatt range. Meta’s implied cost sits well inside that threshold.

| Entity | Metric Type | Value Per Gigawatt |

|---|---|---|

| Meta | Build cost (implied) | ~$22 billion |

| Amazon / Google | Annual cloud revenue | ~$10-16 billion |

| SpaceX | Annual capacity revenue (outlier) | ~$40-50 billion |

The SpaceX figure of $40-50 billion per gigawatt is driven by unique contracting and regulatory conditions and should be treated as an outlier, not a benchmark for what Meta or any other hyperscaler could realistically achieve.

For an investor comparing capital deployment, building below $30 billion per gigawatt means Meta is constructing capacity at a cost that cloud revenue benchmarks suggest should pay back within a commercially reasonable timeframe. BofA maintained its Buy rating on META with an $835 price objective, against shares trading at $668 on 10 July 2026.

Gigawatt figures have become central to hyperscaler infrastructure analysis, but the metric is worth understanding from the ground up if you have not encountered it in this context before.

Once you understand that gigawatts measure deployable compute capacity, the cost-per-gigawatt figure becomes a ratio that tells you how much productive infrastructure a company gets for each dollar of capital investment. It is the unit that makes hyperscaler capex comparable.

The cost advantage revealed in the memo was achieved before Meta’s custom silicon programme contributed anything. That distinction matters for how you weight the next phase of the thesis.

Iris, Meta’s proprietary AI chip being developed with Broadcom and TSMC, is scheduled to enter production in September 2026. Because the chip remains pre-production at the time of the memo data, BofA notes it cannot account for any of the 2026 infrastructure cost savings the document reveals.

Key programme details:

The cost advantage in the memo is not contingent on Iris succeeding. It already exists. Iris represents upside optionality on top of a baseline that has already been established.

Custom silicon typically reduces per-unit compute cost and improves energy efficiency relative to third-party accelerators, a pattern observed at other large technology companies that have made similar transitions. For your valuation model, the implication is that Iris is not priced into the current memo-driven re-rating. It is a distinct future catalyst, sitting entirely in front of you.

Nvidia’s competitive exposure to hyperscaler custom silicon programmes has been quantified by analysts tracking the inference workload shift: with inference projected to represent approximately 80% of the AI accelerator market by 2030, purpose-built chips from Meta, Google, and Amazon are most competitive precisely in the segment where GPU dominance is most contested, which is directly relevant to how durable the cost advantages Meta’s Iris programme targets.

The bear case on Meta’s AI infrastructure was straightforward: $145 billion in capex looked excessive relative to identifiable returns, with the implicit assumption that Meta was building at cost rates comparable to or worse than rivals. The memo data breaks that assumption.

Meta’s Q1 2026 capex selloff established the precise investor anxiety the memo now addresses: a $125-145 billion spend commitment, $107 billion in locked-in contractual obligations, and a free cash flow trajectory that prompted analysts to cut 2026 FCF estimates from approximately $35 billion to $25 billion despite record operating results.

What the memo resolves:

What remains unresolved:

The practical limiting factor on deploying 14 GW of compute is not capital. It is power grid availability. Meta is making multi-gigawatt energy commitments and investing in long-duration storage, which signals proactive planning but also confirms that power is a genuine gating variable.

The capex efficiency advantage is real, but the deployment timeline depends on energy procurement timelines that are largely outside Meta’s direct control. Grid constraints affect every hyperscaler, and they represent the operational bottleneck most likely to delay capacity deployment even when the economics justify building faster.

The memo resolves the cost-per-unit bear case. It does not resolve execution risk on scale, power procurement, or the future capex commitments that extend the plan beyond 2026.

The core recalibration is now plain. The memo shifts Meta’s AI build from a capital allocation concern to a capital efficiency story. Even accounting for the blended-cost caveat and the owned-versus-outsourced uncertainty, the directional shift is significant: roughly twice the compute per dollar of investment versus prior models.

Three specific data points would either confirm or stress-test the memo’s implications:

If Meta pursues external compute monetisation through a dedicated cloud infrastructure offering, the return model transforms from an indirect story (monetised through ads and engagement) to a hybrid cloud-plus-ads model. That optionality has not been confirmed, but it represents a strategically meaningful possibility that could materially expand the bull case.

BofA’s $835 price objective reflects the post-memo institutional positioning, with shares at $668 on 10 July 2026. The gap between current price and target represents BofA’s view of the re-rating opportunity, not a guaranteed outcome.

The memo provides directional clarity on cost efficiency. It leaves three specific disclosure gaps that the next earnings cycle should begin to close. For a reader deciding whether to initiate or add to a position, that is the framework: the direction of the data is clear, the magnitude is material, and the confirmations are identifiable and time-bound.

For investors wanting a structured framework for evaluating which part of the AI stack is most likely to retain durable value, our deep-dive into AI infrastructure binding constraints applies the railroad-era compounding playbook to power availability, cooling density, and grid interconnection, with a four-question checklist for separating genuine bottleneck positions from companies merely adjacent to one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cost per gigawatt measures how much capital a company spends to build each unit of deployable AI compute capacity; it strips out hardware differences across chip generations and lets investors compare capital efficiency across hyperscalers. For Meta, a revised figure of $22 billion per gigawatt versus the prior $45 billion assumption means the same capex budget now implies roughly twice the productive infrastructure.

An internal Meta memo reviewed by Reuters showed the company's AI infrastructure build cost was approximately half what analysts had assumed, shifting the narrative on $145 billion in capital expenditure from a capital allocation concern to a capital efficiency story and prompting a material re-rating of return expectations.

BofA estimates Amazon and Google generate $10-16 billion in annual cloud revenue per gigawatt of deployed infrastructure; at Meta's implied build cost of $22 billion per gigawatt, the payback window on comparable capacity falls somewhere between 18 months and under three years, which BofA characterises as commercially favourable economics.

Project Iris is Meta's proprietary AI chip being developed with Broadcom and TSMC, targeting production in September 2026; because it remains pre-production, none of its potential cost savings are reflected in the $22 billion per gigawatt figure already revealed by the memo, making it a separate future catalyst on top of an efficiency baseline that already exists.

The memo does not disclose the split between owned data centres and contracted third-party cloud capacity within Meta's 14 GW plan, which affects how durable the blended cost figure will prove; separately, power grid availability represents the binding operational constraint on deployment timelines, and future capex commitments beyond 2026 have not been locked in.