Roughly 90% of professional large-cap active fund managers fail to beat the S&P 500 over a 15-20 year horizon. These are not hobbyists. They operate with dedicated research teams, institutional-grade analytical tools, and decades of accumulated expertise. Yet two decades of consistent, cross-market data from S&P Dow Jones Indices deliver the same verdict, report after report, country after country.

The active vs passive investing debate is often framed as a matter of preference. The data frames it as a matter of arithmetic. This article examines why that underperformance is structural rather than a reflection of manager quality, what the odds imply for retail investors attempting stock selection with fewer resources, and how to construct a portfolio and tax architecture that accounts for both the evidence and current U.S. tax law.

What two decades of SPIVA data actually show about active fund performance

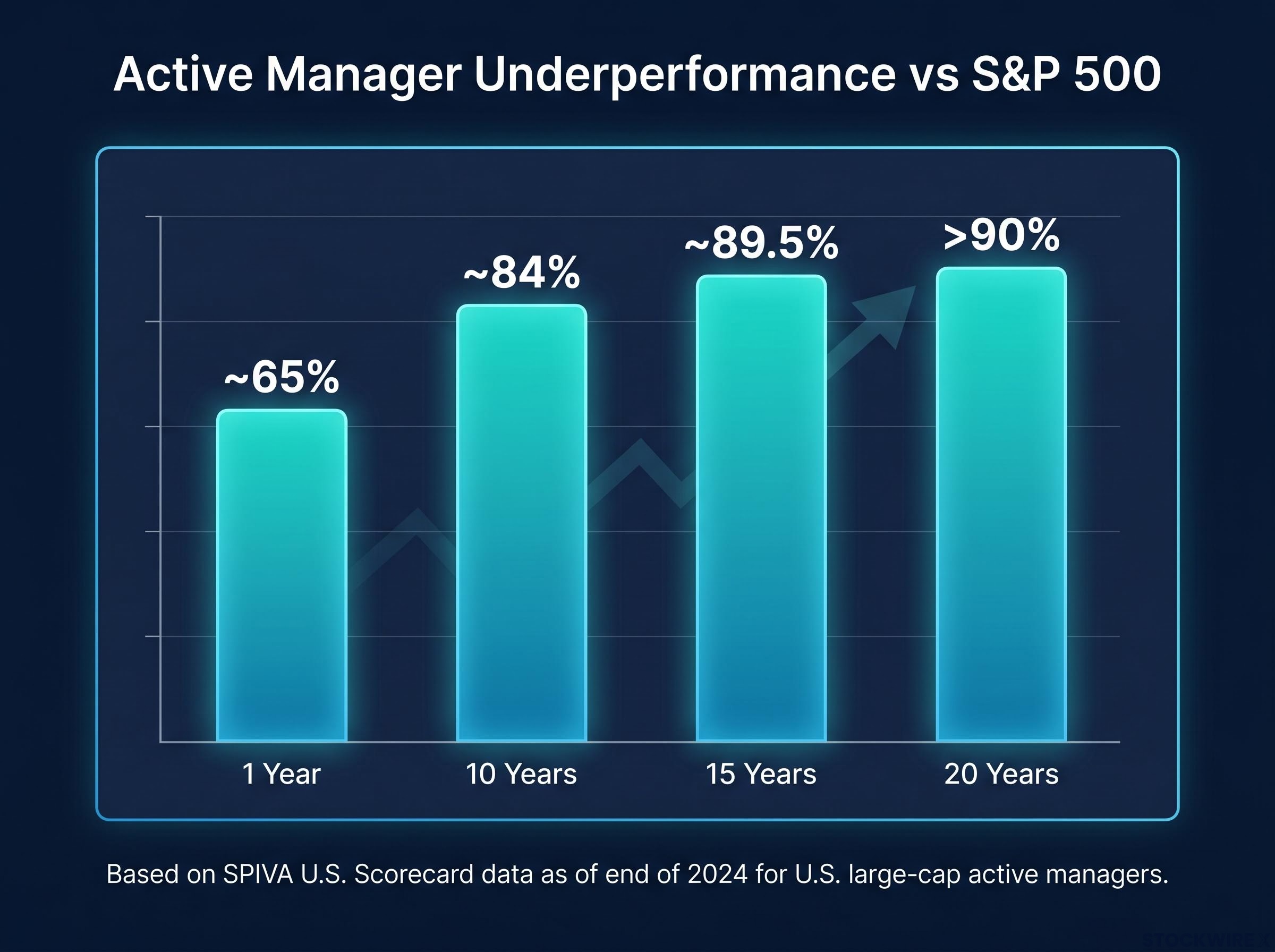

Start with one year. According to the SPIVA U.S. Scorecard as of the end of 2024, approximately 65% of U.S. large-cap active managers underperformed the S&P 500. Across different reporting periods, that one-year figure ranges between 60% and 70%. A majority underperform, but the margin leaves room for optimism.

The long-run verdict

Extend the window and the room disappears. Over 10 years, roughly 84% of active large-cap managers fell short. Over 15 years, the figure reached approximately 89.5%. Over 20-year windows, underperformance consistently exceeds 90% across multiple SPIVA reports.

Approximately 89.5% of active large-cap fund managers underperformed the S&P 500 over a 15-year horizon, according to SPIVA data through the end of 2024.

The pattern is not confined to U.S. large-cap equities. Across most major asset classes and regions, SPIVA reports consistently show that a large majority of active funds underperform their benchmarks over 10-20 year periods. SPIVA has tracked this performance across major equity categories in dozens of countries for over 20 years, making it the most comprehensive and consistently applied dataset available for this comparison.

Cross-market SPIVA results reinforce the same structural verdict beyond U.S. equities: in Australia, 74% of active equity managers failed to beat the S&P/ASX 200 in 2025 despite market conditions described as unusually favourable for stock selection, and 87% underperformed over a 15-year horizon.

| Time Horizon | Approximate Underperformance Rate | Implication |

|---|---|---|

| 1 year | ~65% (range: 60-70%) | A majority underperform even over short periods |

| 10 years | ~84% | The cost drag compounds; most managers fall behind |

| 15 years | ~89.5% | Fewer than 1 in 10 managers keep pace with the index |

| 20 years | Consistently exceeds 90% | The structural verdict is near-total |

The direction is consistent. The longer the horizon, the fewer managers survive the comparison.

When big ASX news breaks, our subscribers know first

Why this failure is structural, not a streak of bad luck

The instinct is to blame manager quality. The arithmetic says otherwise.

In 1991, William Sharpe published “The Arithmetic of Active Management,” which established a principle that SPIVA has since confirmed empirically over two decades. Before costs, active managers collectively hold the market, because they collectively own it. After fees and trading costs, they must underperform the market in aggregate by roughly the amount of those costs.

Sharpe’s arithmetic of active management, published in the Financial Analysts Journal and hosted by Stanford University where Sharpe holds a professorship, established that because active managers collectively own the market, their aggregate pre-cost returns must equal the market return, making any net outperformance after fees a mathematical impossibility for the group as a whole.

Before costs, active managers collectively hold the market. After fees and trading costs, they must underperform in aggregate by the amount of those costs.

This is not an indictment of any individual manager’s intelligence or effort. It is a structural arithmetic problem that applies to all active participants collectively. Three cost layers create the drag:

- Management fees: Active funds charge annual expense ratios that typically run many multiples of a low-cost index fund

- Trading costs: Portfolio turnover generates transaction costs that compound over time

- Bid-ask spreads: Each trade incurs a spread cost that is invisible on fee schedules but real in performance data

For comparison, Vanguard’s S&P 500 ETF (VOO) carries an annual expense ratio of 0.03% as of mid-2026. The gap between that figure and a typical active fund’s all-in cost structure is the mathematical headwind Sharpe described.

The financial services industry has limited incentive to publicise this data widely. There is no viable revenue model built around recommending low-cost passive funds, which helps explain why a finding confirmed across two decades of consistent SPIVA reporting remains underemphasised in mainstream financial marketing.

The odds for retail investors are structurally worse than for professionals

Professional managers operate with dedicated research analysts, advanced credentials, and institutional-grade tools. They still fail to outperform at rates exceeding 80-90% over long horizons. Retail investors attempting the same task do so with fewer resources, placing them below, not above, that performance ceiling.

The competitive environment explains why. Professional managers and institutions account for a large majority of trading volume, with roughly 90% frequently cited in market-structure commentary (estimates range from 63-90% depending on methodology). Most prices already reflect the analysis of highly resourced, highly informed participants. Approximately one million investment professionals compete globally, and millions of quantitative algorithms monitor the same publicly available signals simultaneously.

Real edge vs. the illusion of familiarity

A genuine informational edge is narrow, domain-specific, and difficult to replicate:

- What constitutes a real edge: Decades of operating experience in pharmaceutical drug development that generates insight not visible in public filings; deep enterprise software procurement expertise built over a career in the industry

- What does not: Brand recognition, product usage, consumer observation, or general enthusiasm for a company’s mission

The distinction matters. If an observation is available to a retail investor through normal consumer experience, it is available to the entire professional market simultaneously. Familiarity with a product is not the same as analytical advantage over one million competing professionals.

How to build a portfolio structure that accounts for these odds

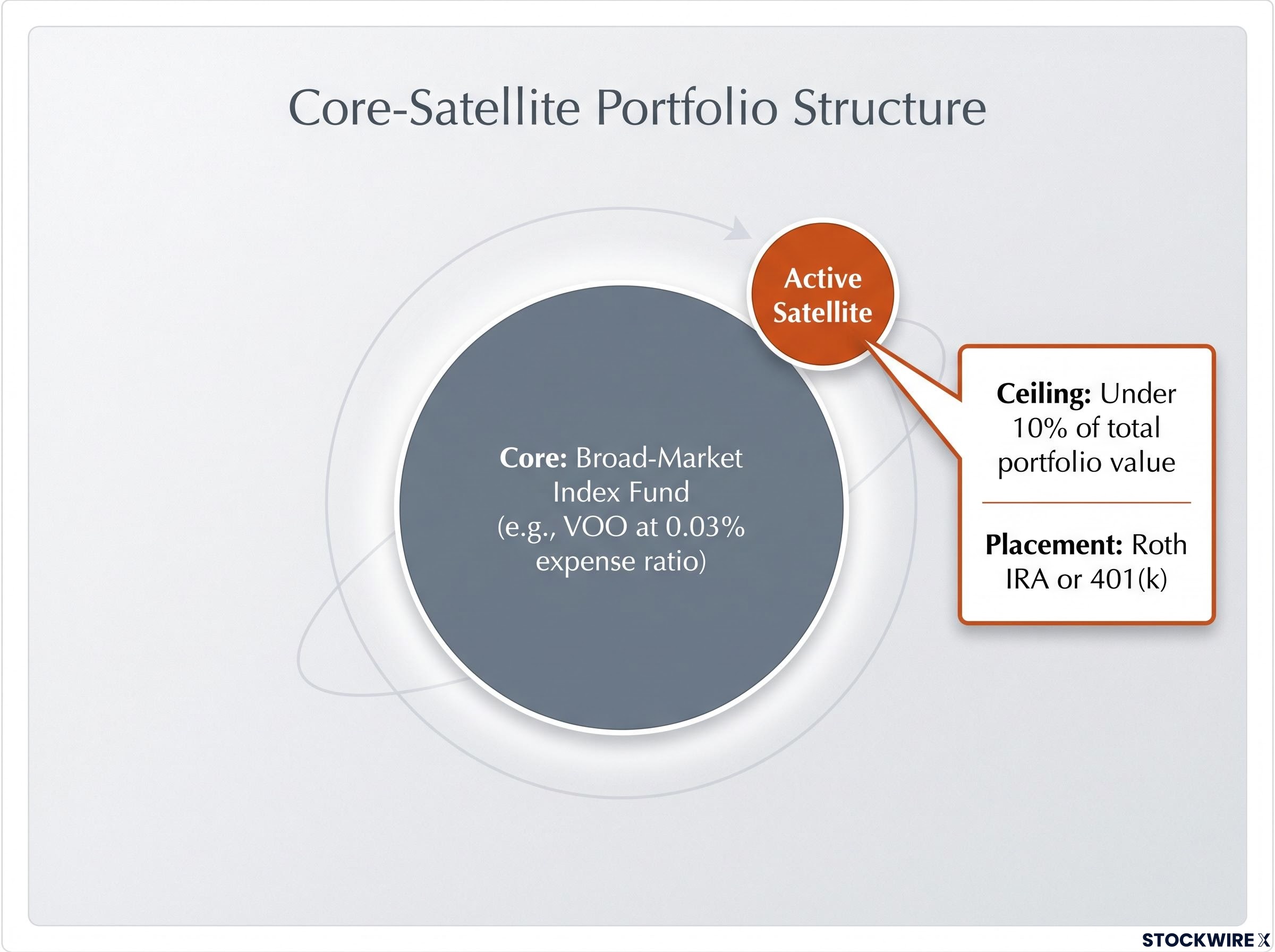

The evidence points toward a specific structural resolution: an index-core plus active-satellite portfolio.

- Establish the index core. A broad-market index fund, such as VOO at 0.03% annual expense ratio, serves as the primary wealth-building vehicle. Index funds automatically capture the small percentage of stocks responsible for driving overall market returns without requiring research or timing decisions.

- Set the satellite ceiling. Any individual stock exposure should remain below 10% of total portfolio value. This is a practical risk-management guideline, not an empirical law of finance. It limits idiosyncratic risk while preserving the index fund’s mathematical advantage.

- Place the satellite inside a tax-sheltered account. Active positions belong in a Roth IRA or 401(k) where turnover does not generate annual tax drag. The next section explains why.

The academic case for holding a small number of high-conviction positions for 30-plus years is logically coherent. In practice, sustained 50%+ drawdowns and extended periods of underperformance relative to a broad index make this approach practically unreachable for most investors.

Very few individuals maintain the behavioural discipline required to hold through severe drawdowns, life events, and the cognitive biases that create pressure to sell at precisely the wrong time.

The core-satellite framework also addresses the behavioural dimension that pure cost arguments tend to underweight: by giving investors a pre-committed, bounded outlet for active participation, the structure interrupts the FOMO-to-impulsive-trade sequence before a tip becomes a portfolio disruption.

The tax architecture that makes or breaks long-run outcomes

Every realised gain in a taxable brokerage account permanently shrinks the compounding base. For a retail investor with unused Roth IRA contribution room, trading in a taxable account is one of the costliest structural errors available, because unused Roth space is lost permanently at year-end and cannot be recovered retroactively.

Roth IRA mechanics are straightforward: contributions are made with after-tax dollars, all growth is tax-free, qualified withdrawals are tax-free, and trading inside the account triggers no capital gains tax. This makes the Roth (and 401(k)) structurally superior for any active or high-turnover strategy.

Using a taxable brokerage account for active stock picking while unused Roth contribution room remains available permanently forfeits tax-free compounding capacity.

Roth IRA contribution limits are income-phased, increase periodically with inflation, and vary by age. Sources conflict on exact 2026 figures; investors should verify current limits directly with IRS guidance before making contribution decisions.

The stepped-up basis advantage for index fund holders

Under current U.S. federal tax law, when appreciated assets are inherited, the cost basis resets to fair market value at the date of death (an alternate valuation date may be elected by the estate). Heirs can liquidate immediately with little or no federal capital gains tax attributable to the original owner’s lifetime of appreciation.

This benefit is particularly powerful for buy-and-hold index investors. An investor who holds a broad-market index fund for decades in a taxable account without triggering taxable events can, under current law, effectively pass decades of unrealised appreciation to heirs with full basis reset. An active trader who regularly realises gains throughout their investing years cannot recover those tax payments; each realised gain is permanently removed from the compounding base.

The IRS guidance on inherited property basis confirms that the cost basis of property received from a decedent is generally the fair market value at the date of death, establishing the legal foundation for the stepped-up basis benefit that buy-and-hold index investors can pass to heirs under current federal tax law.

| Strategy | Tax Treatment of Gains | Unused Contribution Cost | Estate Transfer Benefit |

|---|---|---|---|

| Active trading in taxable account | Capital gains taxed annually on realised gains | High: Roth space forfeited permanently | Stepped-up basis applies only to remaining unrealised gains |

| Active trading in Roth IRA | No annual capital gains tax; withdrawals tax-free | None: Roth space utilised | Roth assets pass tax-free to beneficiaries under current rules |

| Buy-and-hold index fund in taxable account | Minimal annual tax drag; gains largely unrealised | Depends on whether Roth space is also filled | Full stepped-up basis on decades of appreciation |

This describes the benefit under current U.S. federal tax law. The stepped-up basis provision has periodically been debated in policy discussions and could change. Investors should verify current rules with a tax adviser.

Unrealized gains tax proposals at the federal level have never been enacted as of mid-2026, but the Supreme Court’s 2024 decision in Moore v. United States left open the constitutional question of whether such taxation is permissible, and a future administration could revive Biden-era proposals if the fiscal environment shifts.

Why the evidence points in one direction but the industry points in another

Three independent lines of argument converge on the same structural conclusion:

- Cost arithmetic: Sharpe’s principle and two decades of SPIVA data confirm that active managers collectively must underperform after fees

- Competitive dynamics: Institutional participants dominate price discovery, leaving retail investors with fewer resources competing against a market that already reflects professional-grade analysis

- Tax law alignment: The U.S. tax system rewards the exact behaviour the evidence supports: buy-and-hold indexing, which minimises taxable events and maximises the stepped-up basis benefit at death

The financial services industry has no viable revenue model built around recommending passive investing. This structural incentive gap explains why a finding confirmed across over 20 years of consistent SPIVA data, spanning dozens of countries, competes against a marketing environment designed to obscure it.

The bounded cases where active engagement remains defensible are real but narrow: genuine domain expertise applied to a small satellite allocation, housed inside a tax-sheltered account, maintained with the behavioural discipline to hold through severe drawdowns. These exceptions define the boundaries of rational active participation. They do not undermine the default.

The framework that survives the evidence

The evidence does not argue against all active engagement. It precisely defines where active engagement is rational and where it is structurally costly. The decision sequence that accounts for both:

- Maximise Roth IRA and tax-sheltered contributions before opening any taxable positions. Unused Roth space is permanently lost at year-end.

- Establish a broad-market index fund as the portfolio core. This captures the mathematical advantage confirmed by two decades of SPIVA data at minimal cost.

- Limit individual stock positions to under 10% of total portfolio value. This is a practical rule of thumb that contains idiosyncratic risk without eliminating active engagement entirely.

- House any active positions inside tax-sheltered accounts. Turnover in a Roth or 401(k) generates no annual tax drag, preserving the compounding base regardless of trading frequency.

The long-run structural rewards for the patient index investor are the tax-free compounding available inside Roth accounts and the stepped-up cost basis at death for unrealised appreciation in taxable accounts. Both should be verified against current IRS guidance and with a tax adviser, as contribution limits and basis rules are subject to legislative change.

For investors who want a step-by-step implementation walkthrough, our dedicated guide to starting with index funds covers brokerage account selection, dollar-cost averaging mechanics, and the three behavioural mistakes that derail most beginner investors before the compounding base has time to grow.

The evidence does not argue against all active engagement. It precisely defines where active engagement is rational and where it is structurally costly.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. All tax-law references reflect the legal environment as of the date of publication and are subject to change.