Why Your ETF Portfolio May Be Less Diversified Than You Think

2 mins ago

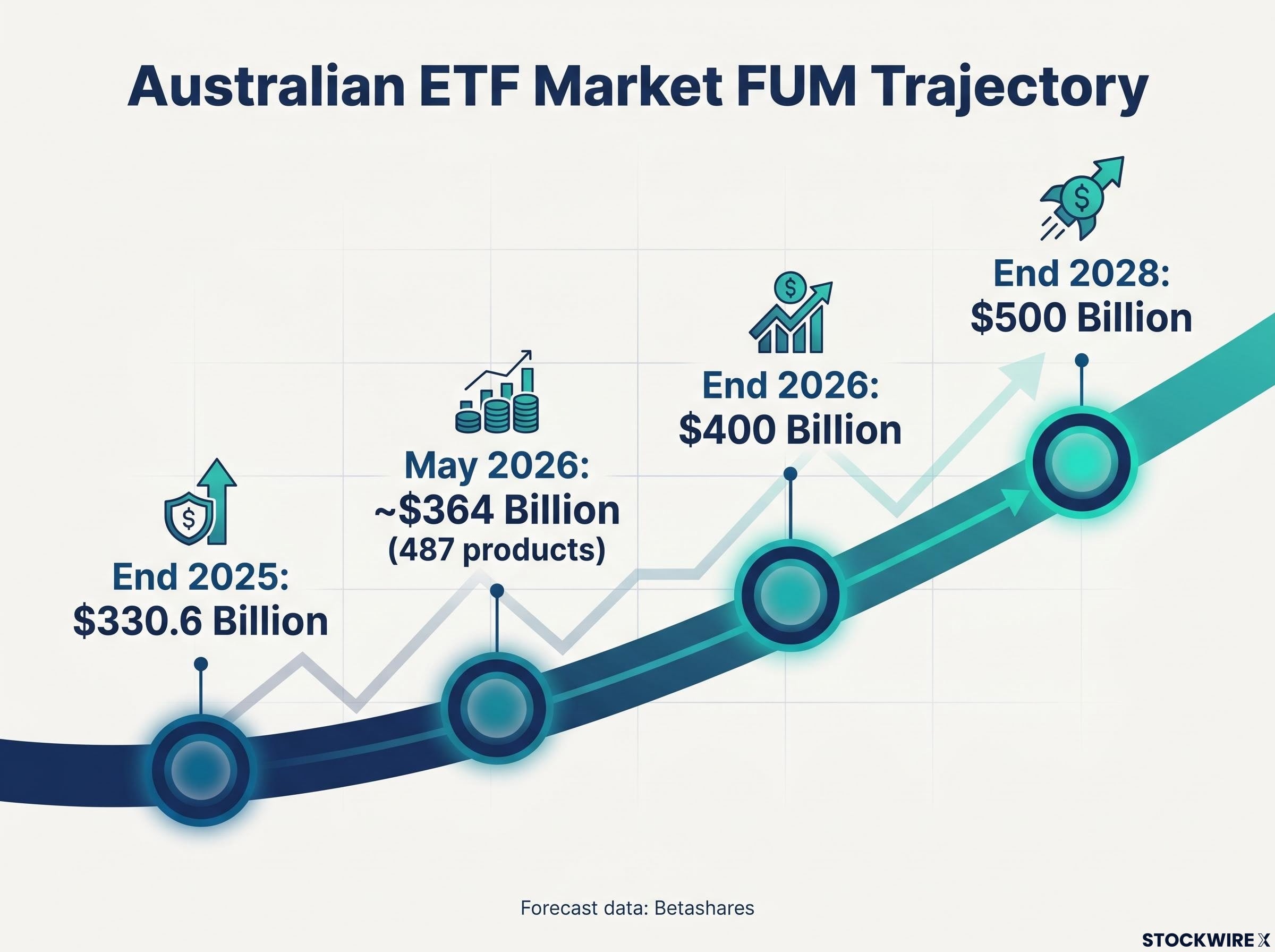

Australia’s ETF market has crossed $330.6 billion in funds under management and is tracking toward $400 billion before the end of 2026. The word “bubble” keeps surfacing in commentary about that trajectory. But a bubble describes an asset that has become detached from its underlying value, and an ETF is not an asset. It is a wrapper.

That distinction matters for roughly 2 million Australians who now hold ETFs as part of their wealth-building strategy. The growth is real: 34.2% year-on-year expansion, $53 billion in net inflows during 2025 alone, and a global industry that has reached US$21.9 trillion without a generalised structural collapse. This is not abstract finance news. It is the vehicle through which a growing share of ordinary Australian savings is being deployed.

Here is the distinction most bubble commentary misses, and what it means for your holdings specifically: the ETF structure itself has survived every major market crisis of the past two decades without breaking. The risks that do exist are concentrated in specific product types, and they are identifiable before they become problems.

The headline number is striking: $330.6 billion at the end of 2025, expanding to approximately $364 billion across 487 products by May 2026. Betashares forecasts the market will pass $400 billion during 2026 and reach $500 billion by the end of 2028. Globally, the ETF industry surpassed US$19.5 trillion by end-2025 and reached approximately US$21.9 trillion by April 2026.

The Australian ETF industry recorded net inflows of approximately $5.2 billion in April 2026 alone, making it the third-highest single month on record, with international equities capturing close to half of all new capital as home-bias among retail investors continued to decline.

But the composition of that growth matters more than the total.

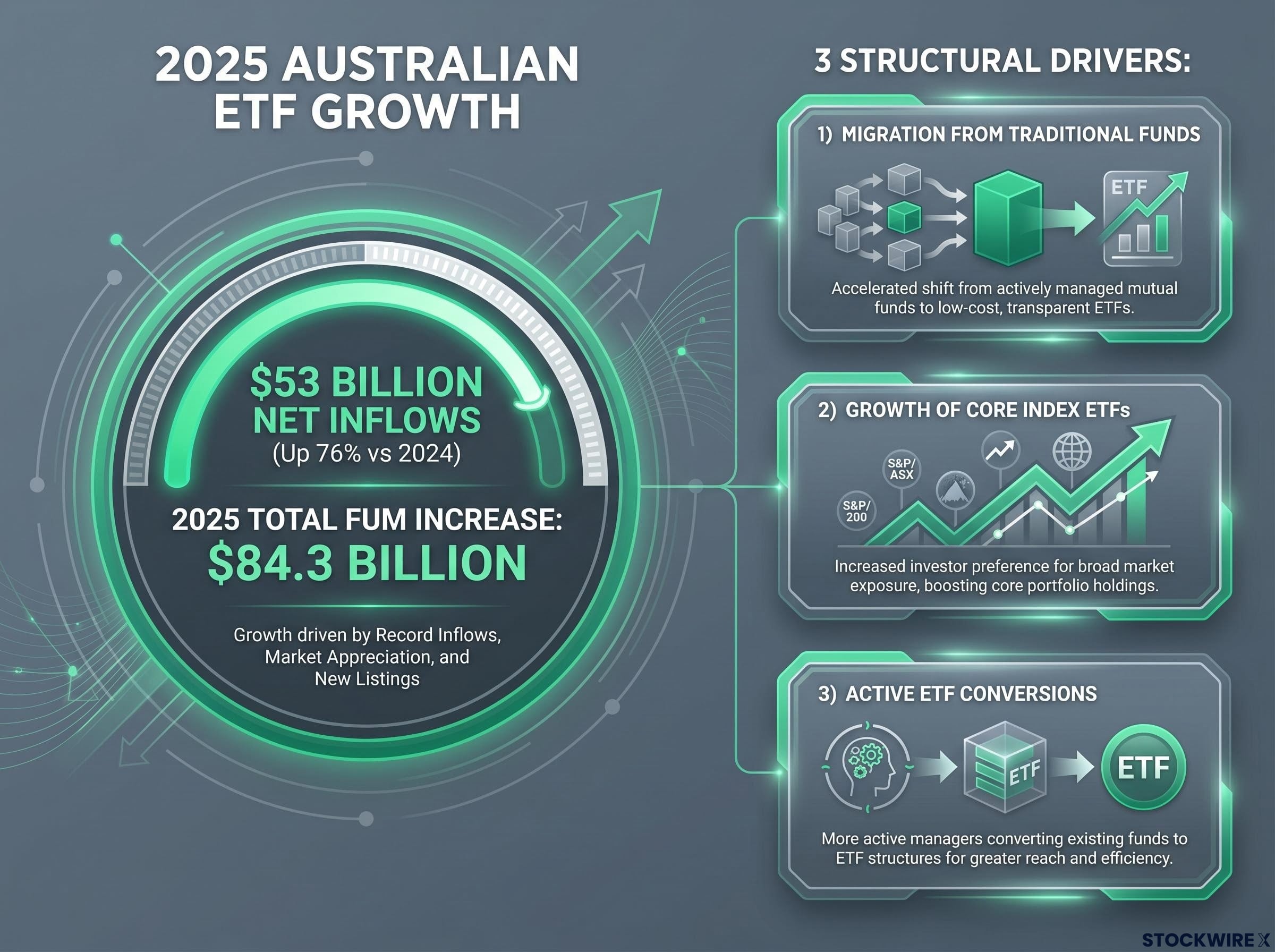

$53 billion in net inflows during 2025, up 76% versus 2024 levels, drove the majority of the expansion.

Of the $84.3 billion total FUM increase over 2025, net inflows accounted for the largest share. That tells you this expansion is being funded by deliberate savings decisions, not passive mark-to-market gains riding a bull market. Three structural drivers explain where the money is coming from:

This is meaningfully different from what typically characterises speculative mania. A market inflated by momentum and leverage behaves very differently from one growing through structural savings migration.

Every major speculative bubble in modern history has shared three traits. The dot-com boom and the US housing crisis both exhibited prices that detached markedly from fundamental value, buying driven primarily by the expectation of further price rises rather than underlying income, and leverage that amplified the cycle until it collapsed.

An ETF does not exhibit these traits at the product level. A broad market ETF tracking the ASX 200 holds a basket of underlying securities. Its price is designed to stay close to the net asset value (NAV), the total value of the securities inside the basket, through a structural mechanism that actively corrects dislocations.

The ETF wrapper is the structural layer between an investor and the underlying securities; whether that layer is transparent, how closely its market price tracks the basket it holds, and how it behaves under stress are distinct questions from whether the assets inside that basket are fairly valued.

The reframe that most commentary misses is straightforward.

If Australian equities or global growth stocks are overvalued, ETF investors carry that risk. But no additional bubble premium is created simply because the exposure is held in ETF form rather than via an unlisted fund or direct shareholding.

Authorised participants, typically large institutional firms, are responsible for keeping ETF prices aligned with NAV. When an ETF trades above its NAV, authorised participants create new ETF units by delivering the underlying securities to the fund, increasing supply and pushing the price back down. When it trades below NAV, they redeem units, reducing supply and pushing the price back up.

This arbitrage loop means the ETF itself cannot become structurally overpriced relative to what it holds. Small, temporary NAV dislocations can occur during extreme stress events, but the mechanism has held structurally across every major crisis of the past two decades. The implication for your portfolio is clear: redirect the bubble question toward your asset allocation, not your investment vehicle.

Theory is one thing. What matters is whether the structure holds when markets actually break.

During the Global Financial Crisis, broad equity ETFs fell roughly in line with the indices they tracked. The primary distress was located in credit markets and leveraged financial institutions, not in ETF plumbing. The ETF market navigated the crisis without notable structural failures.

Then came a faster, more violent test. During the COVID-19 correction in early 2020, broader equity markets shed more than 30% of their value across roughly 30 days of trading. That is the kind of speed and severity that exposes structural weakness if it exists. The creation/redemption mechanism continued to function. ETFs served as a key venue for price discovery and liquidity, particularly in fixed income markets where underlying bonds had become difficult to trade directly.

What both events demonstrated is consistent: investors in ETFs encountered broadly the same conditions as those who held the underlying assets through other structures. The ETF wrapper neither amplified the losses nor cushioned them. Your main protection against a crash is asset allocation and diversification, not a switch to a different investment vehicle.

| Factor | Global Financial Crisis | COVID-19 correction (2020) |

|---|---|---|

| Market severity | Prolonged bear market; major financial institution failures | More than 30% equity decline in approximately 30 days |

| ETF structural impact | No notable ETF-specific structural failures | Creation/redemption mechanism continued functioning; ETFs served as price discovery venue in fixed income |

| Key lesson for investors | Core risk resides in underlying assets, not the ETF wrapper | ETF structure held under rapid, severe stress across multiple asset classes |

The bubble question is largely misdirected at the structural level. That does not mean the Australian ETF market is free of risk. The risks that exist are specific, and they vary sharply by product type.

Three distinct risk categories deserve attention:

The RBA financial stability assessment published in March 2026 addresses concentration and liquidity dynamics in Australia’s growing ETF market, providing the regulatory perspective on systemic considerations that individual investors cannot easily observe from product-level data alone.

A simultaneous rush to exit widely held large ETFs during a market shock is a systemic consideration worth factoring into your liquidity planning, even if the probability remains low.

Leveraged ETFs aim to deliver a multiple (such as 2x or 3x) of the daily return of an index. Inverse ETFs aim to deliver the opposite of the daily return. Both are constructed using derivatives and rely on daily rebalancing.

The mathematics of daily compounding means their longer-term performance can diverge sharply from a simple “2x the index” expectation over weeks or months, even if the index finishes a period exactly where it started. The derivatives underpinning these products are subject to ongoing time-value decay, which acts as a persistent cost that erodes the ETF’s value regardless of how the underlying index moves.

These are short-term tactical instruments for sophisticated users, not long-term wealth-building tools. Familiarity with broad index ETFs does not transfer to these products. If you hold any leveraged or inverse ETFs, the risk profile is fundamentally different from what you encounter in a standard ASX 200 tracker.

For investors holding any leveraged or inverse ETFs who want to model the specific compounding effects in detail, our full explainer on leveraged ETF volatility drag covers the daily reset mechanism, path dependency, and worked examples showing how alternating market moves erode returns even when the underlying index ends flat.

Given the evidence above, the bubble question is the wrong one. These four questions are the right ones for the roughly 2 million Australians currently holding ETFs:

Owning several ETFs does not automatically mean your portfolio is well diversified. When multiple products track closely related indices or operate within the same sector, the underlying holdings can overlap substantially, leaving you with far less genuine spread than the number of funds might suggest. Identifying that kind of overlap takes deliberate analysis.

ETF portfolio concentration is a subtler risk than it appears: the top 10 ASX 200 companies hold approximately 48.6% of a cap-weighted domestic ETF, meaning investors who hold multiple broad Australian equity ETFs may carry far more exposure to banks and miners than they realise before adding a single active decision.

Each of these questions tracks directly to a specific risk identified in this analysis. Together, they form a practical framework for reviewing your own holdings.

The $330.6 billion boom reflects a durable structural migration of Australian savings into a more transparent, lower-cost vehicle. It is not speculative mania in the wrapper itself. The trajectory toward $400 billion and then $500 billion by 2028 is being powered by persistent inflows, fee compression, product conversion, and managed fund migration. These are structural forces that do not reverse easily.

Both industry participants and regulators have given sustained attention to the systemic dimensions of ETF growth, including questions around concentration, liquidity, and the risks carried by specialised products. Oversight of this market is active and ongoing.

But the ETF wrapper argument does not provide immunity from a correction in overvalued underlying assets. If Australian equities, global growth stocks, or other asset classes inside popular ETFs are overvalued for your time horizon, that risk is real and is not neutralised by the efficiency of the ETF structure.

The risk in your ETF portfolio resides in what those funds hold, not in the fund structure itself. That is a question every investor can answer for themselves with the right information.

The more useful ongoing concern is not whether ETFs as a category should be avoided, but whether your specific holdings reflect sound asset allocation. That question will remain relevant at $400 billion, at $500 billion, and beyond.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

The Australian ETF market is not a bubble in the structural sense because an ETF is a wrapper, not an asset. The $330.6 billion in funds under management reflects deliberate savings migration into a lower-cost vehicle, not speculative leverage or prices detached from underlying value.

During both the GFC and the COVID-19 correction (which wiped more than 30% of equity values in roughly 30 days), the ETF creation and redemption mechanism continued functioning without notable structural failures. ETF investors experienced broadly the same conditions as those holding equivalent assets through other structures.

The main risks are concentrated in three specific product types: large index ETFs that could amplify short-term volatility during a simultaneous exit event, thematic or synthetic ETFs carrying illiquidity or counterparty risk, and leveraged and inverse ETFs that use daily-reset derivatives and compound in ways that diverge sharply from simple index multiples over time.

Leveraged ETFs aim to deliver a multiple (such as 2x or 3x) of an index's daily return using derivatives, and their daily rebalancing means longer-term performance can diverge sharply from that multiple due to compounding effects and ongoing time-value decay. They are short-term tactical instruments, not long-term wealth-building tools.

Holding multiple ETFs does not guarantee diversification: the top 10 ASX 200 companies account for approximately 48.6% of a cap-weighted domestic ETF, meaning investors holding several broad Australian equity ETFs may carry far more exposure to banks and miners than the number of funds suggests.